TL;DR:

- Building credit involves establishing a track record that proves responsible borrowing and repayment. Using tools like secured credit cards and credit-builder loans effectively helps create credit history from scratch. Consistently paying on time, maintaining low utilization, and avoiding unnecessary inquiries are key to building and maintaining a strong credit profile.

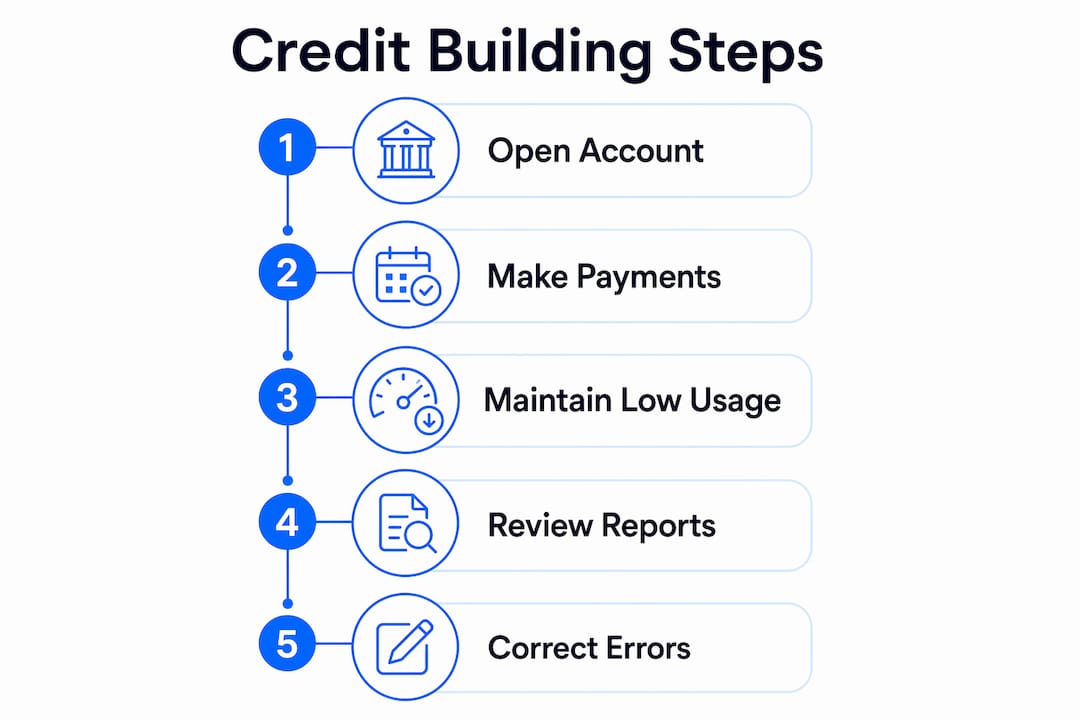

Building credit is the process of establishing a financial track record that proves to lenders you can borrow and repay responsibly. Your credit score, generated by models like FICO®, determines whether you qualify for loans, credit cards, apartments, and competitive interest rates. Without a credit history, lenders have no evidence you’re a safe bet. The good news: you don’t need to start with perfect finances. You need the right tools, consistent habits, and a realistic timeline. This guide covers exactly how to build credit from scratch and keep it growing.

How to build credit: the best starting tools

The fastest way to establish credit history is to open an account that reports to the major credit bureaus, Equifax, Experian, and TransUnion. Several products are designed specifically for people with no credit or limited credit history.

Secured credit cards are the most accessible starting point. They require a refundable security deposit that equals your credit limit, typically ranging from $200 to $5,000. That deposit acts as collateral, which is why issuers approve applicants with no credit history. Use the card for small purchases, pay the balance in full each month, and the issuer reports your on-time payments to the bureaus. Over time, that record becomes your credit history.

Credit-builder loans work differently. The lender holds the loan amount in a savings account while you make monthly payments. Once you’ve paid off the loan, you receive the funds. This structure builds credit and savings at the same time, making it a strong option for anyone who wants to avoid the temptation of a revolving credit line.

Other practical options include:

- Becoming an authorized user: Authorized user status on a family member’s or trusted friend’s credit card lets you benefit immediately from their positive payment history, even without making purchases yourself.

- Co-signers: A creditworthy co-signer on a loan or card application can help you get approved when you otherwise wouldn’t qualify.

- Rent and utility reporting services: Platforms like Experian Boost report on-time rent and utility payments to credit bureaus, adding positive data to your file without opening new debt.

Pro Tip: Before applying for a secured card, confirm the issuer reports to all three major bureaus. Some report to only one or two, which limits how quickly your credit history grows.

What are the best practices for a strong credit profile?

Opening the right accounts is step one. Maintaining them correctly is what actually builds a strong score. These habits separate people who plateau at a fair score from those who reach excellent credit.

-

Pay on time, every time. Payment history accounts for 35% of your FICO® Score. That makes it the single most influential factor in your credit profile. One missed payment can set back a new credit file significantly more than it would an established one.

-

Keep your credit utilization below 30%. Credit utilization is the percentage of your available credit you’re using. Top scorers maintain utilization below 10%, which signals to lenders that you’re not dependent on borrowed money. If your secured card has a $500 limit, try to keep your balance under $50.

-

Pay your full statement balance monthly. Carrying a balance is not required to build credit. This is one of the most persistent myths in personal finance. Paying in full avoids interest charges and keeps your utilization low automatically.

-

Limit new credit applications. Each application triggers a hard inquiry, which temporarily lowers your score. Applying for multiple cards in a short window signals financial stress to lenders. Space out applications by at least six months when possible.

-

Request credit limit increases strategically. A higher limit lowers your utilization ratio without requiring you to spend less. However, some limit increase requests trigger hard inquiries, so always ask your issuer whether the request involves a hard or soft pull before proceeding.

-

Set up automatic payments. Experian recommends automatic minimum payments as a fail-safe. Even if you plan to pay in full, automating the minimum prevents a missed payment if you forget or face an unexpected disruption.

Pro Tip: Pair automatic payments with a calendar reminder to manually pay your full balance a few days before the due date. You get the safety net of automation and the financial benefit of paying in full.

Understanding what drives your score helps you prioritize. For a deeper look at the factors at play, Finblog’s guide on what affects your credit score breaks down each component with practical context.

![]()

How long does it take to build credit?

Credit building follows a predictable timeline, but the exact pace depends on your starting point and consistency.

| Stage | Timeline | What Happens |

|---|---|---|

| Credit invisible to credit visible | 0–6 months | You become scoreable after 6 months of account activity reported to bureaus |

| Fair credit range (580–669) | 6–12 months | On-time payments and low utilization push your score into a usable range |

| Good credit range (670–739) | 12–24 months | Consistent habits and account age move you into the good tier |

| Very good to excellent (740+) | 24+ months | Mix of account types, long history, and spotless payment record required |

The 6-month mark is the critical threshold. Regions Bank confirms that you become “credit visible,” meaning scoreable, only after maintaining a credit-reported account for at least six months. Before that point, lenders literally cannot generate a score for you.

Most people reach a solid, usable score in the 12–18 month range with disciplined habits. Stronger scores in the 700s typically take 18–24 months of consistent behavior. The NFCC advises waiting at least one year after opening a secured card or credit-builder loan before applying for unsecured credit. Jumping too soon leads to rejections, which add hard inquiries and can stall progress.

Quick wins do exist. Disputing errors on your credit report or paying down a high balance can improve your score faster than waiting for account age to accumulate. Check your reports at AnnualCreditReport.com regularly to catch inaccuracies early.

What mistakes derail credit building, and how do you fix them?

Even one misstep can set back a new credit profile by months. These are the most common problems and how to address them.

-

Missing a single payment. The most common beginner mistake is a missed payment. On a thin credit file, one 30-day late payment can drop your score dramatically. Set up automatic payments immediately after opening any credit account.

-

Carrying high balances. High utilization signals risk. If your balance regularly sits above 30% of your limit, your score suffers even if you pay on time. Pay down balances before your statement closing date, not just the due date, since bureaus typically report the balance shown on your statement.

-

Ignoring credit report errors. Errors are more common than most people realize. The good news: bureaus are legally required to investigate disputes within 30–45 days. File disputes directly with Experian, Equifax, or TransUnion through their online portals. A corrected error can produce a meaningful score jump quickly.

-

Believing you need to carry a balance. This myth persists because people confuse “using credit” with “carrying debt.” You only need to use the card and pay it off. Carrying a balance costs you interest and raises your utilization without any credit-building benefit.

“Building credit is a marathon, not a sprint. Patience and consistent responsible behavior are critical to long-term success.” — NFCC

- Applying for too many accounts at once. Multiple hard inquiries in a short period can lower your score and make you look financially desperate to lenders. If you’re managing credit card debt alongside building credit, prioritize paying down existing balances before opening new accounts.

Key takeaways

Building credit requires consistent on-time payments, low credit utilization, and the right starter accounts to establish a scoreable history within six months.

| Point | Details |

|---|---|

| Start with the right tools | Secured credit cards and credit-builder loans are the most accessible options for beginners with no credit history. |

| Payment history is paramount | On-time payments drive 35% of your FICO® Score, making them the single most important habit to maintain. |

| Keep utilization below 30% | Top scorers stay under 10% utilization; high balances hurt your score even when you pay on time. |

| Expect 6–24 months for results | You become credit visible after 6 months, but strong scores in the 700s typically take 18–24 months of consistent behavior. |

| Dispute errors promptly | Credit bureaus must investigate disputes within 30–45 days, and corrections can produce fast score improvements. |

The part nobody tells you about building credit

I’ve spent years watching people approach credit building the wrong way, not because they’re irresponsible, but because the advice they receive is either too vague or too optimistic.

The most underrated move is disputing credit report errors before you do anything else. Most people open a secured card and wait. But if your report already contains an error, a collection account that isn’t yours, or a payment marked late when it wasn’t, you’re building on a cracked foundation. Pull your reports from AnnualCreditReport.com first. Fix what’s wrong. Then start building.

The second thing I’d push back on is the idea that you need multiple credit products right away. One secured card, used consistently and paid in full, does more for your score than three cards managed poorly. Complexity is the enemy of consistency, especially when you’re starting out.

The third thing: don’t obsess over your score monthly. Credit scores are a lagging indicator. The behaviors, payment history, utilization, account age, are the leading indicators. Focus on the habits, and the score follows. Checking it every week creates anxiety without changing the outcome.

Credit building rewards patience and bores impatient people into making mistakes. The people who reach excellent credit aren’t doing anything clever. They’re doing the basics without exception, month after month.

— Povilas

How Finblog can help you build credit faster

Finblog publishes practical, research-backed guides designed for people who want to understand credit deeply, not just follow generic advice. Whether you’re working on credit utilization strategy or looking for credit score improvement tips tailored to your financial situation, Finblog covers the full picture. If you’re also building financial habits that support long-term credit health, the guide on lasting financial habits is worth your time. For personalized guidance and tools to support your credit journey, visit Finblog’s financial resources and explore what fits your goals.

FAQ

What is the fastest way to build credit from scratch?

Opening a secured credit card and becoming an authorized user on a trusted person’s account are the two fastest ways to start. Both methods begin reporting to credit bureaus immediately, and you can become credit visible within six months.

Does paying off a credit card in full each month help your credit?

Yes. Paying your full statement balance monthly keeps your utilization low and avoids interest charges. Carrying a balance is not required to build credit and provides no scoring benefit.

How many credit accounts do you need to build credit?

One responsibly managed account is enough to start. A single secured card with on-time payments and low utilization builds a solid credit history without the risk of overextending.

Can errors on your credit report hurt your score?

Yes, and they’re more common than most people expect. You can dispute errors directly with Experian, Equifax, or TransUnion, and bureaus must investigate within 30–45 days. Correcting an error can improve your score faster than months of new positive activity.

How does becoming an authorized user help build credit?

Authorized user status lets you benefit from the primary cardholder’s positive payment history and account age. Experian recognizes this as one of the quickest ways to add established credit history to a thin file.