Credit card debt weighs heavily on millions of Americans, creating stress and limiting financial opportunities. If you’re struggling with mounting balances and rising interest charges, you’re not alone. This guide delivers proven strategies to help you manage, reduce, and ultimately eliminate your credit card debt. You’ll discover how to assess your situation realistically, create a budget that works, choose the right repayment method, and avoid common pitfalls that derail progress. By following these actionable steps, you can regain control of your finances and build lasting financial health.

Table of Contents

- Understanding Your Credit Card Debt And Setting A Foundation

- Creating An Effective Budget To Control Spending And Allocate Repayments

- Executing Repayment Strategies: Comparing Debt Snowball And Debt Avalanche

- Avoiding Pitfalls And Maintaining Momentum During Debt Repayment

- Explore More Resources To Master Your Financial Freedom

Key takeaways

| Point | Details |

|---|---|

| Preparation is essential | Understanding your total debt, interest rates, and budget creates the foundation for successful repayment |

| Multiple strategies exist | Debt snowball builds motivation through quick wins while debt avalanche minimizes interest costs |

| Budget discipline prevents backsliding | Controlling spending and automating payments keeps you on track without accumulating new debt |

| Track and adjust regularly | Monthly progress reviews help you stay motivated and refine your approach as circumstances change |

| Avoid common mistakes | Ignoring interest rates, missing payments, or taking on new debt can derail even the best plans |

Understanding your credit card debt and setting a foundation

Before you can tackle credit card debt effectively, you need a complete picture of what you’re facing. Many people carry balances across multiple cards without fully grasping the total amount owed or the true cost of interest. This lack of clarity makes it nearly impossible to create an effective repayment strategy.

Start by gathering statements for every credit card you own. Write down each card’s current balance, annual percentage rate, minimum monthly payment, and due date. Create a simple spreadsheet or use a notebook to consolidate this information in one place. Knowing balances, interest rates, and minimum payments is essential to manage credit card debt effectively. This consolidated view reveals the full scope of your debt and helps you prioritize which balances to attack first.

Next, calculate your monthly income and expenses to determine how much money you can realistically allocate toward debt repayment. Include all sources of income and every expense, from rent and utilities to groceries and entertainment. The difference between what you earn and what you spend represents your available repayment capacity. Be honest during this assessment because overestimating your ability to pay leads to frustration and failure.

With your financial snapshot complete, set specific and measurable debt reduction goals. Instead of vague wishes like “pay off debt someday,” establish concrete targets such as “reduce total debt by $5,000 in 12 months” or “eliminate the smallest balance within 90 days.” These goals provide direction and motivation throughout your repayment journey.

Key preparation steps include:

- Compile all credit card details including balances, rates, and payment dates

- Calculate total debt across all cards to understand the full challenge

- Document monthly income and expenses to find repayment capacity

- Set specific, time-bound goals that match your financial reality

- Identify which expenses you can reduce to free up additional funds

This foundation work might feel tedious, but it’s the difference between random efforts and a strategic approach. You can’t fix what you don’t measure, and you can’t plan without data. Spend time on this step to set yourself up for success. For comprehensive guidance on this process, explore resources on master managing credit card debt strategies.

Creating an effective budget to control spending and allocate repayments

A well-designed budget is your primary tool for preventing new debt while funding aggressive repayment. Without one, you’re flying blind and likely to overspend in some areas while neglecting debt obligations. Budgeting is a fundamental skill to prevent new debt and enable faster credit card repayment.

Follow these steps to build a budget that supports debt elimination:

- Track every dollar of income from all sources including salary, side gigs, and any passive earnings

- Categorize your expenses into fixed costs like rent and variable costs like entertainment

- Set realistic spending limits for each category based on past patterns and future goals

- Prioritize minimum payments on all debts first to avoid late fees and credit damage

- Allocate any remaining funds to accelerated debt repayment using your chosen strategy

- Review and adjust monthly as your income or expenses change

The key to budget success is identifying non-essential spending you can cut immediately. Review the past three months of bank and credit card statements to spot patterns. That daily coffee shop visit, unused gym membership, or multiple streaming services might seem small individually, but together they can free up hundreds of dollars monthly for debt repayment. Be ruthless in this analysis because every dollar redirected toward debt saves you money on interest.

After cutting unnecessary expenses, focus on optimizing essential spending. Can you meal plan to reduce grocery costs? Switch to a cheaper cell phone plan? Negotiate lower insurance rates? Small savings in multiple categories compound into significant repayment power. The goal isn’t to eliminate all enjoyment from life but to temporarily prioritize debt freedom over discretionary spending.

![]()

Pro Tip: Automate your minimum payments and any extra debt payments to ensure consistency and avoid late fees. Set up automatic transfers on the day after your paycheck arrives so the money moves before you’re tempted to spend it elsewhere. This “pay yourself first” approach removes willpower from the equation and guarantees progress.

Consider using budgeting apps, spreadsheets, or even a simple notebook to track spending throughout the month. The method matters less than the consistency. Check in weekly to ensure you’re staying within limits and adjust as needed. Many people discover they spend far more than expected in certain categories once they start tracking. For detailed guidance on budget creation, review this creating a budget step guide and learn about common budgeting mistakes to avoid.

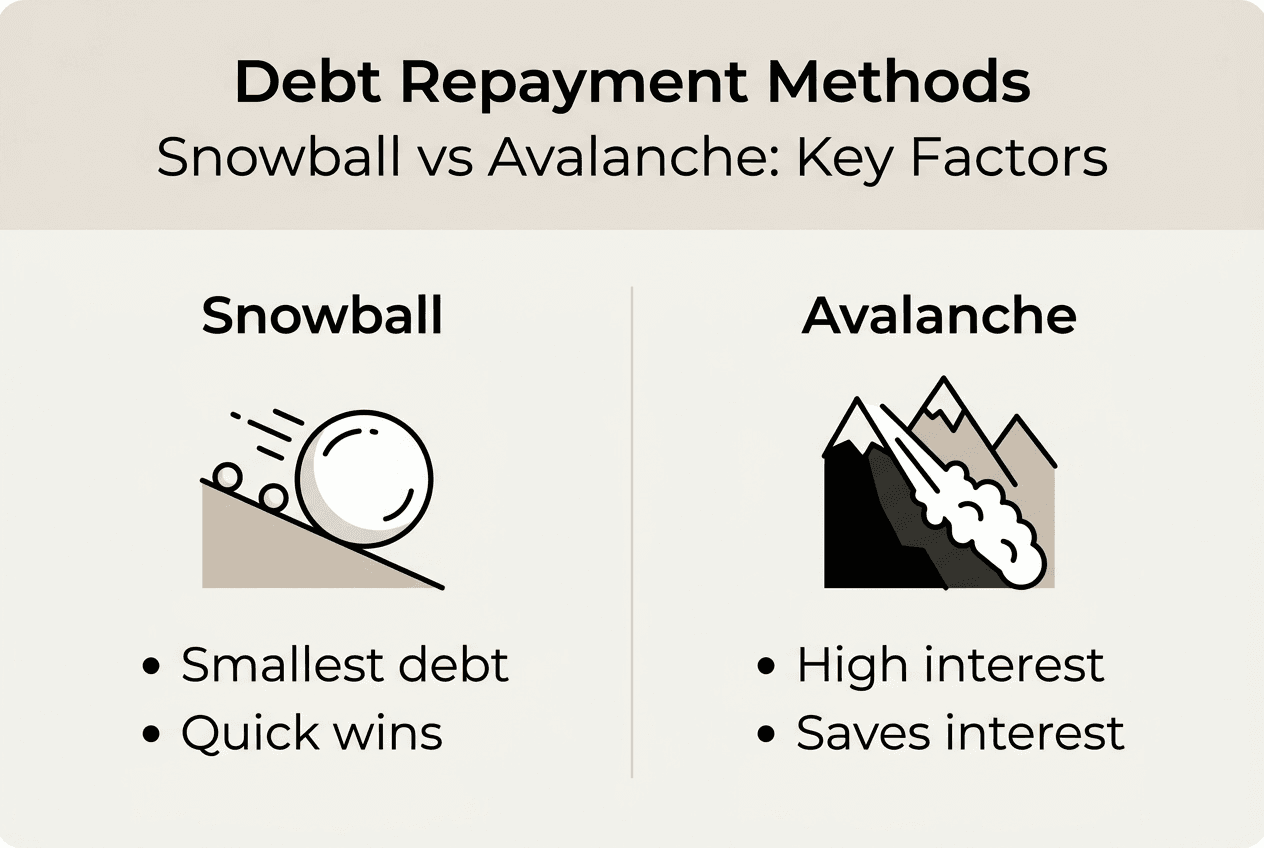

Executing repayment strategies: comparing debt snowball and debt avalanche

With your budget funding repayment, you need to decide how to allocate extra payments across multiple credit cards. The two most effective methods are the debt snowball and debt avalanche approaches. Each has distinct advantages depending on your personality and financial situation.

The debt snowball method focuses on psychological momentum. You list all debts from smallest to largest balance regardless of interest rate. Make minimum payments on everything, then put all extra money toward the smallest debt. Once that’s paid off, roll that entire payment amount into the next smallest debt. This creates increasingly large payments as you eliminate balances, building motivation through quick wins. Debt snowball and avalanche methods are proven strategies to accelerate credit card debt repayment.

The debt avalanche method prioritizes mathematical efficiency. You list debts from highest to lowest interest rate regardless of balance. Make minimum payments on everything, then direct all extra funds to the highest-rate debt. This approach saves the most money on interest over time because you’re eliminating the most expensive debt first. Once the highest-rate debt is gone, you tackle the next highest rate.

| Factor | Debt Snowball | Debt Avalanche |

| — | — |

| Primary focus | Psychological wins through quick payoffs | Maximum interest savings |

| Ordering method | Smallest to largest balance | Highest to lowest interest rate |

| Motivation style | Frequent victories boost morale | Logical efficiency appeals to analytical minds |

| Interest cost | Potentially higher total interest paid | Minimizes total interest paid |

| Best for | People who need encouragement and visible progress | Disciplined individuals focused on optimal math |

Choosing between these methods depends on your personal needs. If you’ve struggled with debt for years and need motivation to keep going, the snowball’s quick wins might be essential for your success. Seeing a card balance hit zero within a few months creates powerful momentum that keeps you engaged. However, if you’re disciplined and motivated by saving money, the avalanche approach will put more dollars back in your pocket over time.

Pro Tip: You don’t have to choose just one method. Some people use a hybrid approach, starting with snowball to build confidence by eliminating one or two small debts quickly, then switching to avalanche to optimize interest savings on larger balances. Assess your emotional state and financial data to create the approach that works best for you.

Key considerations when executing your strategy:

- Stay consistent with extra payments every month without exception

- Resist the temptation to split extra money across multiple cards

- Celebrate each debt elimination milestone to maintain motivation

- Recalculate your strategy if interest rates change significantly

- Document your progress visually with charts or debt trackers

Whichever method you choose, commit fully and trust the process. Both strategies work when executed consistently over time. For more detailed comparison and implementation guidance, explore comprehensive debt repayment strategies that can accelerate your journey to financial freedom.

Avoiding pitfalls and maintaining momentum during debt repayment

Even with a solid plan, many people stumble during execution. Understanding common mistakes helps you avoid them and maintain steady progress toward debt freedom. Many debtors lose progress due to overspending or ignoring warning signs that their strategy needs adjustment.

The most damaging mistake is accumulating new debt while trying to pay off existing balances. This creates a frustrating cycle where you make progress on one card only to add charges on another. To prevent this, consider these protective measures:

- Remove credit cards from your wallet and use only cash or debit for purchases

- Freeze cards in a block of ice so they’re available for true emergencies but not impulse buys

- Delete saved card information from online shopping sites to add friction to purchases

- Set up alerts that notify you immediately of any card activity

- Ask your card issuer to lower your credit limit to reduce temptation

Missing minimum payments derails progress by triggering late fees, penalty interest rates, and credit score damage. Even if you can’t pay extra some months, never skip the minimum payment. Set up automatic payments for at least the minimum amount on every card to ensure you never miss a due date. You can always make additional manual payments when you have extra funds available.

Another common pitfall is failing to track progress and adjust your strategy. Review your debt balances monthly and celebrate milestones like paying off individual cards or reaching percentage goals. This regular check-in keeps you engaged and allows you to spot problems early. If you’re consistently falling short of payment goals, revisit your budget to find additional cuts or explore ways to increase income through side work.

Consistent small actions compound into remarkable results over time. Every extra dollar you put toward debt today saves you multiple dollars in future interest charges and brings you closer to financial freedom.

Stay motivated by visualizing your debt-free future. What will you do with the money currently going to credit card payments? Build an emergency fund? Save for a home? Invest for retirement? Keep these goals visible as daily reminders of why you’re making short-term sacrifices. Some people create visual debt trackers, coloring in progress bars or crossing off amounts as they’re paid. These tangible representations of progress provide powerful motivation during difficult months.

Finally, prepare for setbacks without letting them derail your entire plan. Unexpected expenses will arise. You might have a month where you can only make minimum payments. Life happens, and perfection isn’t required. What matters is getting back on track quickly rather than using one setback as an excuse to abandon your strategy entirely. For additional guidance on accelerating debt reduction, review strategies on how to reduce debt fast while maintaining sustainable progress.

Explore more resources to master your financial freedom

Your journey to eliminate credit card debt doesn’t end with this article. Finblog.com offers comprehensive resources to support every stage of your financial transformation. Whether you need deeper guidance on specific repayment strategies, want to refine your budgeting skills, or seek motivation during challenging months, you’ll find expert advice tailored to your situation.

Explore our detailed guides on master managing credit card debt for advanced techniques beyond the basics covered here. Our budget creation guide provides templates and tools to optimize your spending plan. For ongoing strategy refinement, review our comprehensive analysis of debt repayment strategies that address various financial situations and goals. Return regularly as you progress to access new insights and maintain momentum toward lasting financial control.

FAQ

How can I choose between debt snowball and debt avalanche methods?

Choose the debt snowball method if you need motivation through quick wins by paying off smaller balances first. Select the debt avalanche if you’re disciplined and want to minimize total interest paid by targeting high-rate debts. You can also combine both approaches by using snowball initially for momentum, then switching to avalanche for optimal savings.

What should I do if I can’t make minimum payments on all my credit cards?

Contact your credit card issuers immediately to explain your situation and request hardship programs that may lower payments or interest rates temporarily. Consider working with a nonprofit credit counseling service that can negotiate with creditors on your behalf and create a manageable debt management plan. Acting quickly prevents further damage to your credit and provides options before accounts go into default.

How can I prevent accumulating new credit card debt while repaying existing balances?

Stick to a strict budget that prioritizes essential expenses and debt repayments, leaving no room for discretionary credit card purchases. Remove credit cards from your wallet and use only cash or debit cards for daily transactions. For comprehensive budgeting guidance that prevents new debt accumulation, follow the steps in our creating a budget step guide to maintain spending discipline.

How long does it typically take to pay off credit card debt?

Payoff time varies widely based on your total debt amount, interest rates, and monthly payment capacity, ranging from months to several years. Use online debt repayment calculators to input your specific numbers and see projected payoff dates under different payment scenarios. These projections help you set realistic expectations and stay motivated by showing exactly how extra payments accelerate your debt-free date.