Managing your money consistently feels impossible when paychecks disappear before you realize where they went. You know saving matters and investing makes sense, yet somehow bills pile up while retirement accounts stagnate. The good news? Building smart money habits transforms chaotic finances into predictable wealth accumulation. This guide walks you through evidence-based strategies that turn scattered efforts into systematic financial progress, helping you take control and build confidence in your money decisions.

Table of Contents

- Prerequisites: What You Need Before Building Smart Money Habits

- Step 1: Define Clear And Achievable Financial Goals

- Step 2: Master Budgeting Techniques

- Step 3: Automate Your Savings And Investments

- Step 4: Diversify Your Investment Portfolio

- Step 5: Regularly Review And Adjust Your Finances

- Common Mistakes And How To Avoid Them

- Expected Results And Success Metrics

- Discover More Financial Insights And Tools

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Foundation matters | Emergency funds, budgeting tools, and financial literacy create the base for lasting money habits. |

| Automation drives results | Automated savings increase rates by 30% while reducing decision fatigue and missed contributions. |

| Simplicity wins | Complex budgets fail 60% of the time; zero-based budgeting cuts overspending by 25%. |

| Consistency builds habits | Practicing money behaviors for 66 days makes them automatic and sustainable. |

| Reviews optimize progress | Monthly financial check-ins improve investment returns by 5% and keep goals on track. |

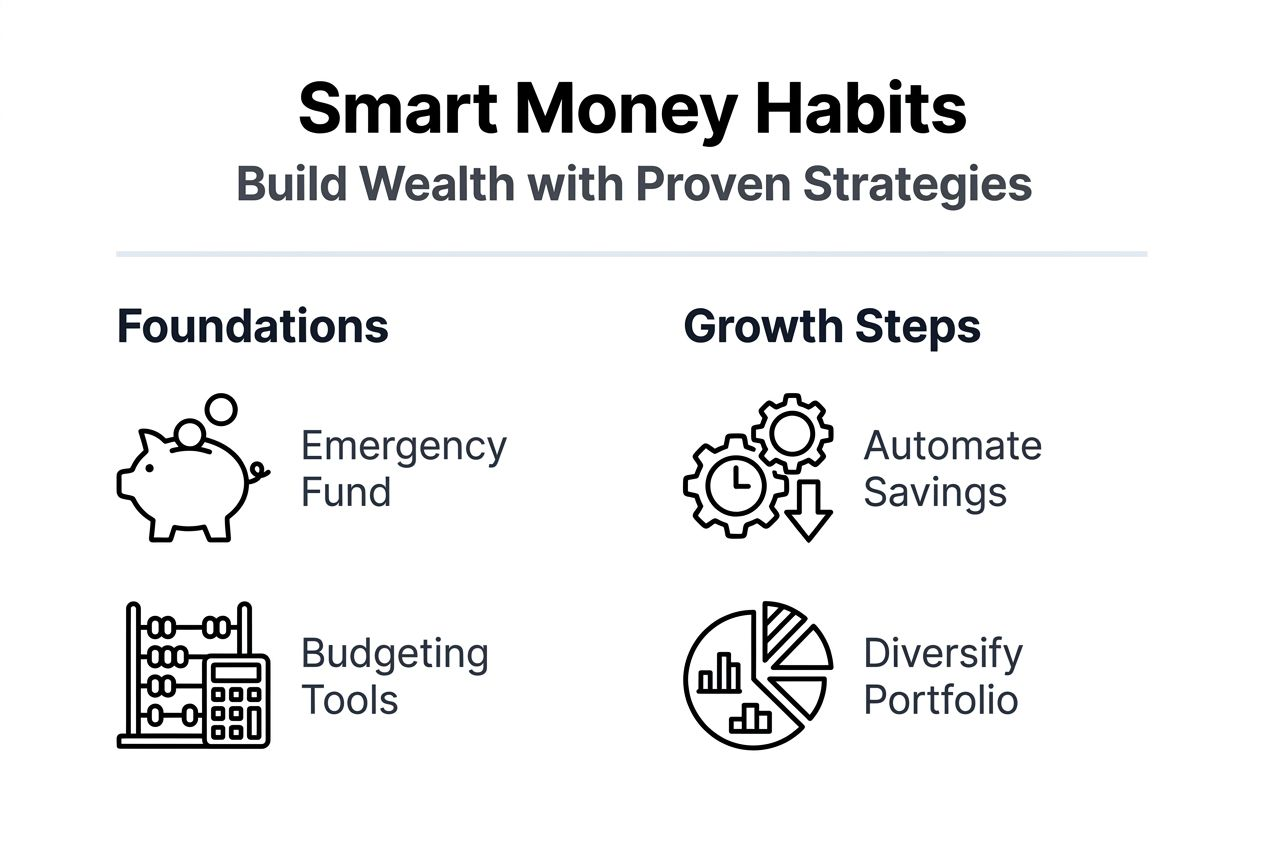

Prerequisites: what you need before building smart money habits

Before diving into specific money habits, you need foundational elements in place. Think of these as the tools and conditions that make everything else possible.

Start with an emergency fund covering three to six months of living expenses. This buffer protects you from derailing your progress when unexpected costs appear. Without it, a single car repair or medical bill forces you to tap credit cards or abandon savings goals.

Next, choose reliable tracking tools. Budgeting apps and investment platforms remove friction from monitoring your finances. Digital tools improve budget adherence rates by 35% compared to manual spreadsheets because they automate calculations and send reminders.

Develop basic financial literacy before implementing complex strategies. Understanding compound interest, tax advantages, and risk tolerance prevents costly mistakes. Recognize your own psychological biases too. Most people overestimate their willpower and underestimate emotional spending triggers.

Commit to consistent practice. Habit formation typically requires 66 days of deliberate effort before behaviors become automatic. Mark this timeline on your calendar and prepare for the initial discomfort of changing routines.

Essential prerequisites include:

- Emergency savings equal to 3 to 6 months of expenses

- Budgeting app or spreadsheet system you’ll actually use

- Basic understanding of interest, taxes, and investment fundamentals

- Realistic commitment to daily or weekly money management tasks

- Support system or accountability partner for motivation

Integrating these elements with broader financial wellness routines creates momentum. Once your foundation solidifies, building specific habits becomes dramatically easier.

Step 1: define clear and achievable financial goals

Vague wishes like “save more money” rarely translate into action. You need specific targets that guide daily decisions and motivate consistent effort.

SMART goals boost your achievement likelihood significantly. Research shows setting SMART goals increases success rates by 42% compared to general intentions. Structure each goal with these criteria:

- Specific: “Save $10,000 for a down payment” beats “save money for a house”

- Measurable: Track progress monthly with clear numbers

- Achievable: Set targets within reach given your current income and expenses

- Relevant: Align goals with your values and long-term vision

- Time-bound: Attach deadlines like “by December 2026” to create urgency

Break large objectives into smaller milestones. A $50,000 debt payoff goal feels overwhelming, but paying $850 monthly for five years provides actionable steps. Each milestone creates momentum and proves progress.

Common financial goals for working professionals:

- Eliminate $15,000 credit card debt within 18 months

- Build a six-month emergency fund totaling $18,000 by year-end

- Contribute 15% of gross income to retirement accounts starting next quarter

- Save $25,000 for a home down payment over three years

- Increase net worth by $30,000 in 12 months through debt reduction and investing

Write goals down and review them weekly. Seeing your targets regularly reinforces commitment and helps you spot when spending drifts off course. Adjust timelines if circumstances change, but maintain the core objective.

Tracking progress visually works remarkably well. Create a simple chart showing debt declining or savings growing. These visual cues trigger positive emotions that strengthen your habit loop.

Step 2: master budgeting techniques

Budgeting reputation suffers because most people choose overly complicated systems they can’t maintain. The right method feels simple enough to sustain while providing enough control to prevent overspending.

Zero-based budgeting works exceptionally well for professionals with irregular income or variable expenses. This approach assigns every dollar a job before the month begins. Income minus all planned expenses and savings equals zero. Zero-based budgeting reduces overspending by 25% because it forces intentional decisions about discretionary spending.

Digital tools dramatically improve adherence. Apps sync with bank accounts, categorize transactions automatically, and alert you when spending approaches limits. Using budgeting software improves adherence rates by 35% versus manual tracking because it removes tedious data entry.

Simplicity prevents abandonment. Complex budgets with 30+ categories cause 60% of people to quit within three months. Limit yourself to eight to ten broad categories like housing, food, transportation, and discretionary spending.

| Method | Best for | Pros | Cons |

|---|---|---|---|

| Zero-based | Variable income, detail lovers | Complete spending control, maximizes savings | Time-intensive setup, requires monthly adjustments |

| 50/30/20 | Beginners, simple preference | Easy to implement, flexible | Less precise, may not fit all situations |

| Envelope system | Cash spenders, visual learners | Tangible limits, prevents overspending | Inconvenient for online purchases, security concerns |

| Pay yourself first | Savers prioritizing goals | Automates savings, reduces temptation | Requires discipline for remaining funds |

Pro Tip: Review your budget on the same day each month, ideally right before payday. This timing lets you adjust categories based on the previous month while planning the upcoming period. Avoid creating categories you’ll never check or splitting hairs over small amounts.

Start with your current spending patterns rather than ideal targets. Track three months of actual expenses to establish realistic baselines. Then identify one or two categories to optimize rather than overhauling everything simultaneously.

Step 3: automate your savings and investments

Relying on willpower to save leftover money guarantees inconsistent results. Automation removes decision points and ensures consistent progress regardless of motivation levels.

Automated transfers increase savings rates by 30% on average. Set up recurring transfers from checking to savings accounts immediately after payday. Treating savings like a non-negotiable bill works because the money moves before you mentally allocate it to spending.

Retirement contributions benefit enormously from automation. Employer 401(k) deductions happen before you see the paycheck, making the reduction invisible. If you’re self-employed, schedule automatic IRA contributions bi-weekly or monthly to maintain consistency.

Investment accounts also support automated purchases. Dollar-cost averaging through regular investments reduces timing risk and builds positions steadily. This approach removes the paralyzing question of when to invest by making it automatic.

Automation setup steps:

- Link checking account to high-yield savings account

- Schedule transfers for one to two days after payday deposits

- Start with a comfortable amount, even just $50 or $100 per paycheck

- Automate retirement contributions to at least match employer programs

- Set up automatic investment purchases if using brokerage accounts

- Review and increase amounts quarterly as income grows or expenses decrease

Pro Tip: Increase automation gradually to avoid cash flow stress. Start with a modest percentage and raise it by 1% every quarter. This painless escalation compounds over time without shocking your budget. Many employers offer automatic annual increases in 401(k) contributions that you can enable once and forget.

Monitor automated transactions monthly to catch errors or overdrafts. Automation works best when combined with systematic saving best practices that align transfers with your cash flow patterns.

Step 4: diversify your investment portfolio

Concentrating investments in a single stock or asset class exposes you to unnecessary risk. Spreading money across different investments smooths returns and protects against catastrophic losses.

Diversification reduces portfolio risk by approximately 20% without sacrificing long-term returns. The key lies in choosing assets that don’t move in perfect sync. When stocks drop, bonds often hold steady or rise, cushioning overall portfolio impact.

Financial advisors recommend diversifying across at least five asset types. This includes domestic stocks, international stocks, bonds, real estate, and potentially commodities or cash equivalents. The exact mix depends on your age, risk tolerance, and timeline.

| Asset class | Risk level | Typical return | Role in portfolio |

|---|---|---|---|

| Domestic stocks | High | 10% annually | Growth engine for long-term wealth |

| International stocks | High | 8% annually | Geographic diversification, growth potential |

| Bonds | Low to medium | 4% annually | Stability, income generation |

| Real estate | Medium | 8% annually | Inflation hedge, income through rents |

| Cash/Money market | Very low | 2% annually | Liquidity, emergency access |

Younger investors can tolerate more stock exposure because time allows recovery from market drops. A common rule suggests subtracting your age from 110 to determine stock percentage. A 35-year-old might hold 75% stocks and 25% bonds, while a 60-year-old shifts to 50% stocks and 50% bonds.

Index funds and ETFs make diversification affordable and simple. Rather than picking individual stocks, these funds hold hundreds or thousands of companies in a single investment. Total market index funds provide instant diversification across entire economies.

Key diversification principles:

- Spread investments across multiple asset classes and sectors

- Include both domestic and international exposure

- Rebalance annually to maintain target allocations

- Avoid overconcentration in employer stock or single industries

- Consider real estate through REITs for added variety

Diversification doesn’t eliminate risk entirely but significantly reduces volatility. This stability helps you stay invested during market turbulence rather than panic-selling at losses. Learn more about strategic allocation through comprehensive guides on how to invest money wisely.

Step 5: regularly review and adjust your finances

Setting up systems once and forgetting them leads to drift and missed opportunities. Monthly reviews keep your financial habits aligned with goals and responsive to changing circumstances.

Regular portfolio reviews can improve investment returns by 5% annually. These check-ins let you rebalance allocations, harvest tax losses, and ensure your risk level still matches your timeline and comfort.

Schedule a consistent monthly review session. The last Sunday of each month or the first weekend works well. Dedicate 60 to 90 minutes to reviewing accounts, comparing actual spending to budget, and assessing progress toward goals.

Key metrics to track monthly:

- Net worth: assets minus liabilities, trending upward over time

- Savings rate: percentage of income saved, ideally 15% to 25%

- Debt payoff progress: balances decreasing according to plan

- Investment performance: returns relative to benchmarks and targets

- Budget variance: categories where spending exceeded or underran plans

- Goal milestones: percentage complete on each financial objective

Adjustments matter as much as tracking. If restaurant spending consistently exceeds budget, either increase the category or implement specific limits like eating out twice weekly maximum. When income rises, allocate the increase intentionally rather than letting lifestyle creep absorb it.

Life changes demand plan updates. Marriage, children, job changes, or health issues require budget and investment adjustments. Flexibility in response to these shifts boosts financial resilience and prevents derailment.

Quarterly, conduct deeper reviews examining insurance coverage, tax optimization opportunities, and long-term goal progress. Annual reviews should revisit overall financial strategy, retirement projections, and estate planning needs.

Detailed guidance on comprehensive planning appears in resources like this financial planning guide for beginners. Regular reviews transform static plans into dynamic systems that evolve with your life.

Common mistakes and how to avoid them

Even well-intentioned professionals fall into predictable traps that undermine wealth building. Recognizing these patterns helps you avoid expensive detours.

Neglecting emergency funds causes 40% of wealth-building failures. Without liquid savings, unexpected expenses force you to raid retirement accounts or accumulate high-interest debt. Both options derail long-term progress and create compounding setbacks.

Overly complex budgets lead to 60% abandonment within three months. Creating 30 spending categories and tracking every coffee purchase burns motivation quickly. Complexity creates friction that eventually overwhelms even determined individuals.

Improper debt management affects over 50% of investors negatively. Carrying high-interest credit card balances while investing in low-return assets makes no mathematical sense. Pay off debts above 7% interest before aggressive investing in most cases.

Ignoring tax optimization leaves money on the table unnecessarily. Maxing tax-advantaged accounts like 401(k)s and IRAs before taxable investing can save thousands annually. Similarly, tax-loss harvesting in investment accounts reduces bills without changing investment exposure.

Avoidance strategies:

- Build emergency fund to three months expenses minimum before aggressive investing

- Simplify budget to eight to ten broad categories you’ll actually monitor

- Prioritize high-interest debt payoff over additional investing

- Maximize tax-advantaged account contributions before taxable accounts

- Seek accountability through partners, advisors, or online communities

- Forgive occasional slip-ups and refocus rather than abandoning systems

Behavioral challenges undermine technical knowledge. Emotional spending, overconfidence in stock picking, and loss aversion all sabotage rational plans. Awareness of these biases helps you design systems that work with human nature rather than against it.

Detailed guidance on avoiding costly errors appears in comprehensive resources about personal finance mistakes that cost stability. Prevention beats correction when building lasting wealth.

Expected results and success metrics

Understanding realistic timelines and measurable outcomes keeps expectations grounded while providing motivation to persist through challenging phases.

Habit formation requires consistent practice over approximately 66 days to become automatic. Initial weeks feel awkward and require conscious effort. Around week six, behaviors start feeling natural. By month three, most money habits operate with minimal willpower.

Measurable financial improvements timeline:

- Month 1 to 2: Budget stabilizes, overspending decreases by 15% to 20%

- Month 3 to 4: Emergency fund reaches first milestone of $1,000 to $2,000

- Month 6: Debt reduction of 15% achievable with focused effort and possible coaching

- Month 9 to 12: Savings rate increases to 15% to 20% of income

- Year 2: Net worth growth accelerates through compound interest and consistent contributions

- Year 3 to 5: Financial confidence rises as systems prove reliable through various challenges

SMART goal setting increases achievement rates by 42% compared to vague intentions. This improvement stems from clarity, measurability, and the motivation that comes from tracking visible progress.

Emergency funds reduce financial hardship risk by 70% according to financial wellness research. This single habit creates resilience that prevents cascading failures when unexpected costs appear.

“The habit of saving is itself an education; it fosters every virtue, teaches self-denial, cultivates the sense of order, trains to forethought, and so broadens the mind.” This wisdom reminds us that money habits build character alongside wealth.

Monthly reviews contribute to steady optimization. Small adjustments compound over years into significantly better outcomes. A 5% improvement in investment returns through regular rebalancing means tens of thousands of additional dollars over a 20-year period.

Track your progress against these benchmarks through resources like detailed guides on achieving financial goals systematically. Celebrate milestones to reinforce positive associations with your money habits.

Discover more financial insights and tools

Building smart money habits marks just the beginning of your wealth-building journey. Finblog offers comprehensive guides, practical tools, and expert insights tailored specifically for working professionals and individual investors like you. Whether you’re refining your budgeting approach, exploring advanced investment strategies, or seeking answers to specific financial questions, our resources provide actionable guidance at every stage. Visit Finblog to access our full library of articles, calculators, and planning templates designed to support your ongoing financial success and confidence.

Frequently asked questions

What are smart money habits?

Smart money habits are consistent financial behaviors that optimize how you save, invest, and spend to build lasting wealth. These practices help you avoid costly mistakes, stay aligned with your financial goals, and make progress automatically. They include budgeting systematically, automating savings, diversifying investments, and reviewing finances regularly.

How long does it take to form a money habit?

Forming a money habit typically requires consistent effort over 66 days before the behavior becomes automatic. The first few weeks demand conscious attention and willpower. By week six, actions start feeling more natural, and by month three, most people perform these behaviors with minimal effort.

What’s the best budgeting method for working professionals?

Zero-based budgeting proves highly effective for professionals because it controls every dollar and significantly reduces overspending. This method assigns all income to specific categories before the month begins, leaving zero unallocated. Using budgeting apps helps simplify the process and improves adherence through automatic tracking and alerts.

How can I avoid common financial mistakes?

Maintain an adequate emergency fund covering three to six months of expenses to prevent crisis-driven decisions. Keep your budget simple with fewer than ten categories to avoid abandonment. Review your finances monthly to catch problems early and adjust as needed. Manage debt proactively by prioritizing high-interest balances, and learn from comprehensive guidance on avoiding personal finance mistakes that undermine stability.

Recommended

- How to Build Wealth: Proven Steps for Lasting Financial Success – Finblog

- How to Pick Investments: Build Your Wealth Wisely in 2025 – Finblog

- 7 Essential Financial Habits for Success You Need to Know – Finblog

- Wealth Protection Strategies for Secure Financial Future – Finblog

- Come creare un piano di investimento:evita gli errori comuni – Avtonoma – La piattaforma di consulenza finanziaria indipendente