Did you know that around 30 percent of your credit score depends on your credit utilization ratio? Many people assume that closing unused credit cards or carrying a balance will help their score, but these myths can actually do the opposite. Understanding how credit utilization is calculated and the real impact on your financial health gives you the power to make smarter credit choices and avoid costly mistakes.

Table of Contents

- Defining Credit Utilization And Common Myths

- How Credit Utilization Is Calculated

- Types Of Credit Utilization Ratios

- Credit Utilization’s Role In Credit Scores

- Mistakes To Avoid And Optimization Strategies

Key Takeaways

| Point | Details |

|---|---|

| Understanding Credit Utilization | Credit utilization is the percentage of available credit used, significantly impacting credit scores; aim to keep it below 30%. |

| Myth of Closing Credit Cards | Closing credit accounts can harm your score by reducing available credit and increasing utilization ratio. |

| Importance of Individual Card Utilization | High utilization on individual cards can negatively affect your score even if overall utilization is low; monitor each card. |

| Optimization Strategies | Maintain low balances, consider timing payments before statement closing dates, and request credit limit increases to improve credit utilization. |

Defining Credit Utilization and Common Myths

Credit utilization represents the percentage of available credit you are currently using across all your credit accounts. It’s a crucial financial metric that significantly impacts your overall credit health and score. Think of it like a financial dashboard showing how much of your credit capacity you’re actively tapping into.

According to research from Experian, a common misconception is that closing credit cards will automatically improve your credit score. In reality, closing accounts can reduce your total available credit and potentially increase your utilization ratio, which might actually lower your score. This counterintuitive fact surprises many consumers who believe removing credit lines simplifies their financial profile.

Key credit utilization myths to understand:

- Carrying a balance improves your credit score (False)

- Closing unused credit cards always helps your credit (False)

- Only your current month’s balance matters (False)

As research from Upgrade highlights, paying off balances in full each month is more beneficial than maintaining recurring credit card debt. Financial experts recommend keeping your credit utilization ratio below 30% across all accounts to maintain a healthy credit profile. This means if you have a $10,000 total credit limit, you should aim to keep your combined balance under $3,000 at any given time.

Understanding these nuances can help you make smarter financial decisions and protect your credit score. Learn more in our comprehensive guide to credit utilization ratio.

How Credit Utilization Is Calculated

Credit utilization is a straightforward mathematical calculation that reveals how much of your available credit you’re actively using. According to Upgrade, the formula is simple: divide your total credit card balances by your total credit limits and convert the result to a percentage.

Here’s a practical breakdown of the calculation process:

- Add up all your current credit card balances

- Add up the total credit limits across all your cards

- Divide the total balance by total credit limit

- Multiply the result by 100 to get the percentage

For example, if you have two credit cards with the following details:

- Card 1: $3,000 balance, $5,000 limit

- Card 2: $1,500 balance, $7,000 limit

Your calculation would look like this:

- Total Balance: $4,500

- Total Credit Limit: $12,000

- Utilization Ratio: ($4,500 / $12,000) x 100 = 37.5%

As research from Experian indicates, keeping this ratio below 30% is generally recommended for maintaining a healthy credit score. Individual credit bureaus may calculate this slightly differently, but the core principle remains the same: lower utilization typically signals responsible credit management.

Check out our comprehensive guide to credit utilization ratio for more detailed insights into managing your credit health.

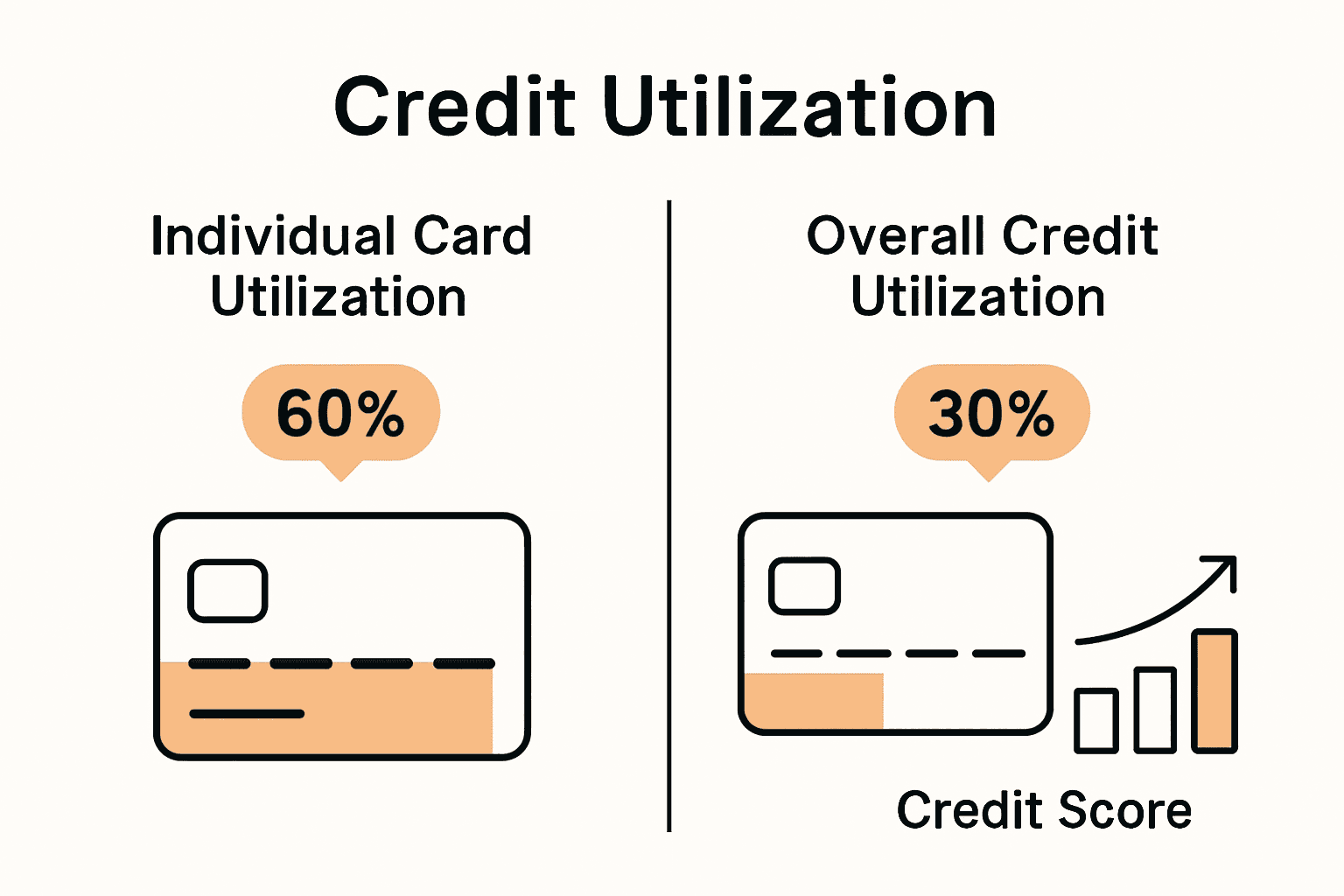

Types of Credit Utilization Ratios

Credit utilization is not a one-size-fits-all calculation. According to research from Upgrade, there are two primary types of credit utilization ratios that financial experts track: individual card utilization and overall credit utilization.

Individual Card Utilization

Individual card utilization focuses on the credit usage for each specific credit card. This means calculating the balance-to-limit ratio for each card separately. For instance:

- Card with a $5,000 limit and $2,500 balance = 50% utilization

- Another card with a $10,000 limit and $1,000 balance = 10% utilization

Even if your overall utilization looks good, high individual card utilization can still negatively impact your credit score. Some credit scoring models pay close attention to cards that are close to being maxed out.

Overall Credit Utilization

Experian explains that overall credit utilization provides a comprehensive view of your credit usage across all accounts. This is calculated by adding all your credit card balances and dividing by the total credit limits. Financial experts typically recommend keeping this ratio below 30% to maintain a healthy credit profile.

Practical example:

- Total credit limits across all cards: $25,000

- Total current balances: $5,000

- Overall utilization: (5,000 / 25,000) x 100 = 20%

Here’s a side-by-side comparison of individual vs. overall credit utilization:

| Aspect | Individual Card Utilization | Overall Credit Utilization |

|---|---|---|

| Definition | Ratio for each credit card | Ratio across all cards |

| Calculation | Balance ÷ Limit per card | Total balances ÷ Total limits |

| Impact on Score | High per-card use can hurt | High total use hurts overall |

| Monitoring Tip | Keep each card below 30% | Keep total use below 30% |

| Example | $2,500 / $5,000 = 50% | $5,000 / $25,000 = 20% |

Dive deeper into credit utilization strategies with our comprehensive guide to understand how these ratios impact your financial health.

Credit Utilization’s Role in Credit Scores

Credit utilization is a critical factor in determining your overall credit score, acting like a financial report card that lenders use to assess your creditworthiness. This metric typically accounts for approximately 30% of your FICO credit score, making it the second most significant factor after payment history.

Imagine your credit score as a complex puzzle, where credit utilization represents a substantial piece. When you maintain lower credit card balances relative to your total available credit, you’re signaling responsible financial management. Credit scoring models interpret low utilization as an indication that you’re not overly dependent on credit and can manage your finances effectively.

The impact of credit utilization can be dramatic:

- Utilization below 10%: Considered excellent

- Utilization between 10-30%: Considered good

- Utilization above 30%: Potential negative impact on credit score

- Utilization near 100%: Significant risk to credit health

Understanding this relationship means recognizing that credit scores aren’t just about paying bills on time. They’re about demonstrating financial discipline and strategic credit management. Even if you pay your balances in full each month, the reported balance can affect your utilization ratio.

This means timing your credit card payments and monitoring your reported balances can be just as crucial as making timely payments.

This means timing your credit card payments and monitoring your reported balances can be just as crucial as making timely payments.

Explore our in-depth guide to credit utilization strategies to learn how to optimize your credit profile and improve your financial standing.

Mistakes to Avoid and Optimization Strategies

Optimizing your credit utilization requires strategic planning and avoiding common pitfalls. According to research from Upgrade, maintaining low credit card balances and understanding how your actions impact your credit profile are crucial steps in financial management.

Key Mistakes to Sidestep

- Closing Old Credit Cards: This reduces your total available credit and can unexpectedly increase your utilization ratio

- Maxing Out Credit Cards: Pushing your balance close to the credit limit signals financial stress to lenders

- Inconsistent Payment Patterns: Irregular payments can lead to unexpected high utilization reporting

- Ignoring Credit Limits: Not tracking your current balance against total credit limit

Optimization Strategies

Experian recommends several practical approaches to manage credit utilization:

- Request credit limit increases on existing cards

- Make multiple payments throughout the billing cycle

- Keep older credit accounts open, even if unused

- Spread expenses across different cards to maintain low individual card utilization

A powerful strategy is timing your payments. Since credit bureaus typically report your statement balance, paying down your balance before the statement closing date can dramatically improve your reported utilization. This means you can use your credit card regularly while maintaining a low reported balance.

Learn more about advanced credit utilization techniques in our comprehensive guide and take control of your financial health.

Take Control of Your Credit Utilization Today

Struggling to keep your credit utilization below the critical 30 percent threshold can feel overwhelming. Whether you are managing multiple credit cards or worried about how each payment impacts your credit score, understanding the nuances of individual and overall credit utilization is the key to protecting your financial reputation. The article highlights common pitfalls like closing old credit accounts or maxing out cards that can unknowingly damage your credit health.

At finblog.com, we specialize in turning these complex credit concepts into clear, actionable steps. Discover expert strategies to optimize your credit usage, avoid costly mistakes, and maintain a strong credit profile. Don’t wait until your utilization ratio harms your score or approval chances—get personalized guidance now. Explore our resources, learn practical tips on credit utilization ratio management, and start improving your financial standing today. Visit finblog.com and take the first step toward smarter credit management.

Frequently Asked Questions

What is credit utilization?

Credit utilization is the percentage of available credit that you are currently using across all your credit accounts. It is a key factor in determining your credit health and score.

How is credit utilization calculated?

Credit utilization is calculated by dividing your total credit card balances by your total credit limits and converting the result to a percentage. For example, if your total balance is $4,500 and your total credit limit is $12,000, your utilization ratio would be 37.5%.

What is considered a healthy credit utilization ratio?

A healthy credit utilization ratio is generally considered to be below 30%. Maintaining a lower ratio signals responsible credit management to lenders.

What are common mistakes to avoid with credit utilization?

Common mistakes include closing old credit cards, maxing out credit cards, inconsistent payment patterns, and ignoring credit limits. These can negatively impact your credit utilization ratio and, subsequently, your credit score.

Recommended

- Complete Guide to Credit Utilization Ratio – Finblog

- Master Managing Credit Card Debt: Achieve Financial Freedom – Finblog

- Understanding the Importance of Credit Score – Finblog

- Understanding Tax Efficient Investing: How It Works – Finblog

- Comprendre les risques du crédit à la consommation

- Understanding Insurance and Credit Score Interaction – Savvy Insurance