TL;DR:

- Compound interest earns interest on both principal and accumulated interest, leading to exponential growth.

- Starting to invest early and consistently significantly boosts long-term wealth through compounding.

- Compound interest benefits savers and investors but works against borrowers with high-interest debt.

Most people assume their savings grow in a straight line. You put money in, it earns a fixed percentage, and that’s that. But compounding breaks this assumption completely. Instead of earning interest only on what you deposited, you start earning interest on your interest. That distinction sounds small, but over decades it produces results that feel almost unbelievable. A single $10,000 investment at 7% annual growth doesn’t just become $31,000 after 30 years with compounding. It becomes closer to $76,000. Understanding exactly how this works is the single most valuable financial concept you can carry into your investing life.

Table of Contents

- What is compound interest?

- How does compound interest work? Key formulas and examples

- How compound interest compares to simple interest

- How compounding works for investments and against debt

- The Rule of 72 and common compounding pitfalls

- A fresh perspective: Why most people underestimate compounding

- Put your knowledge to use and grow your wealth

- frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Compound interest basics | Compound interest means you earn money on both your original amount and the interest already earned. |

| Exponential growth advantage | Your savings or debt can accelerate quickly thanks to compounding, not just add up steadily. |

| Rule of 72 shortcut | Divide 72 by your interest rate to estimate how quickly your money will double. |

| Start early for best results | Beginning to invest or save early gives compounding time to multiply your gains. |

What is compound interest?

Compound interest is one of those concepts that sounds complicated until the moment it clicks, and then it seems obvious. “Interest on interest” is the most accurate short description: you earn interest not only on the money you originally put in, but also on all the interest that has already accumulated.

Here’s a simple contrast. If you put $1,000 in an account paying 10% simple interest, you earn $100 every single year, no matter what. After five years, you’ve earned $500 total. With compound interest, that first year still earns $100. But in year two, your balance is $1,100, so you earn 10% of $1,100, which is $110. In year three, you earn interest on $1,210. The growth feeds itself.

“He who understands it, earns it; he who doesn’t, pays it.” This quote, often attributed to Albert Einstein about compound interest, captures why getting this concept right is so important for your financial future.

This acceleration is why why investing early matters so much. Time is the engine that powers compounding. A 25-year-old who invests $5,000 and leaves it alone will dramatically outperform a 35-year-old who invests the same amount, even if both earn the same return. The extra decade makes an enormous difference because the compounding effect has more runway.

Another thing worth noting: you don’t need a massive starting amount. Even small, consistent contributions accumulate into significant sums over time. The key ingredient is patience. The benefits of early investing compound just like the interest itself.

Pro tip: Even investing $50 per month starting at age 22 can grow into tens of thousands of dollars by retirement age, thanks to compounding. Starting small beats waiting until you can start big.

How does compound interest work? Key formulas and examples

Now that you know the concept, let’s look at the actual mechanics. The standard formula is A = P(1 + r/n)^(n*t), where:

- A = the future value of the investment

- P = the principal (your starting amount)

- r = annual interest rate (as a decimal)

- n = number of compounding periods per year

- t = time in years

Here’s how to use it in three steps:

- Convert your annual interest rate to a decimal (7% becomes 0.07).

- Choose your compounding frequency: annually (n=1), quarterly (n=4), monthly (n=12), or daily (n=365).

- Plugin your principal and time horizon, then solve for A.

Using a real example: $10,000 invested at 7% annual interest, compounded annually, over 30 years becomes approximately $76,123. That’s more than seven times your original amount, just by letting compounding run.

Frequency matters too. The more often interest compounds, the faster your balance grows. Here’s what that looks like for the same $10,000 at 7% over 30 years:

| compounding frequency | ending balance | total interest earned | extra vs. annual |

|---|---|---|---|

| Annual | $76,123 | $66,123 | baseline |

| quarterly | $77,898 | $67,898 | +$1,775 |

| monthly | $78,489 | $68,489 | +$2,366 |

| daily | $78,663 | $68,663 | +$2,540 |

The differences between monthly and daily compounding are modest in practice, but they add up. For investing basics for young professionals, what matters more than frequency is starting sooner and staying consistent.

At the extreme end, mathematicians define continuous compounding using the formula A = Pe^(rt), where e is approximately 2.718. This represents the theoretical maximum, as if your money were compounding every millisecond. In the real world, daily compounding is close enough to this limit that the difference is negligible.

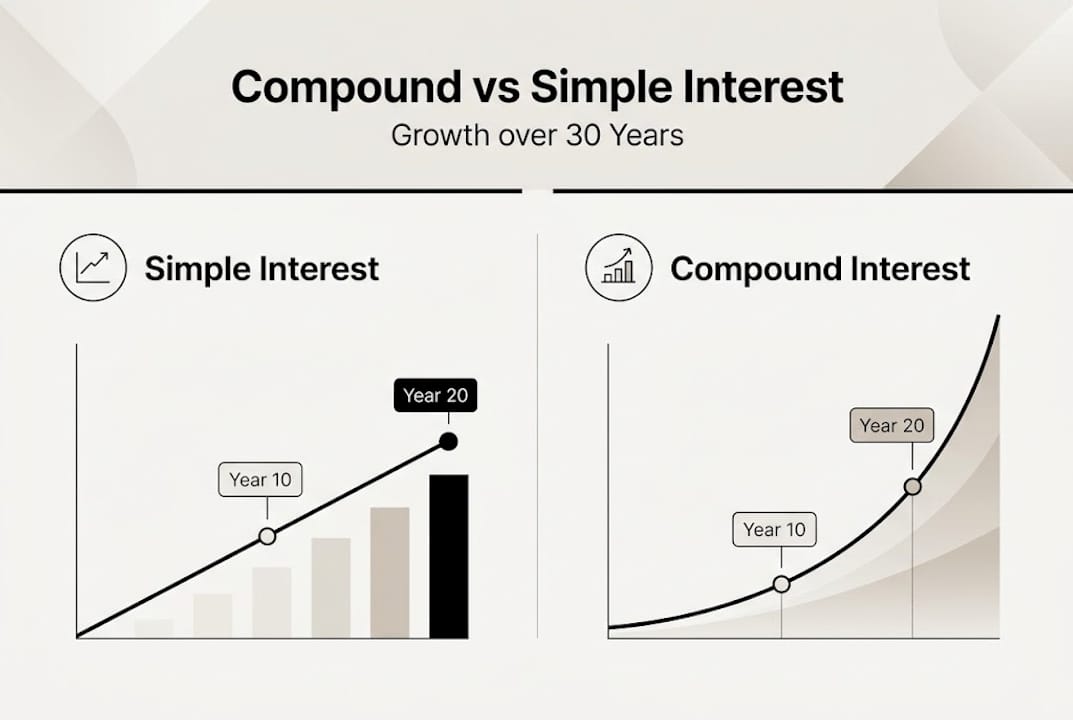

How compound interest compares to simple interest

Simple interest is calculated only on your original principal using the formula I = P x r x t. That means the interest you earn never earns more interest. Growth is linear and predictable, but it leaves a lot of potential on the table.

Here’s what that difference looks like side by side for $10,000 at 7% over 30 years:

| simple interest | compound interest (annual) | |

|---|---|---|

| Year 10 | $17,000 | $19,672 |

| Year 20 | $24,000 | $38,697 |

| Year 30 | $31,000 | $76,123 |

The gap widens dramatically over time. That’s the exponential vs. linear growth difference in action.

Here’s a quick breakdown of when each type appears:

- Simple interest: Common in short-term personal loans, auto loans, and some bonds.

- compound interest: Found in savings accounts, most investments, mortgages, and credit card debt.

- Who benefits from simple interest: The borrower, because growth is capped.

- Who benefits from compounding: The investor or lender, because returns accelerate.

- When compounding hurts: When you’re the borrower carrying a high-interest balance.

For anyone exploring saving vs investing differences, understanding which type of interest applies to each product is a critical first step. A savings account growing at compound interest and a car loan charging simple interest are two completely different financial animals.

How compounding works for investments and against debt

Compounding is not neutral. It works hard in your favor when you’re saving and investing, and it works just as hard against you when you’re carrying debt. This double-edged reality is something every young professional should internalize early.

Where compounding works for you:

- High-yield savings accounts that compound daily or monthly

- Index funds and ETFs where you reinvest dividends

- 401(k) and IRA accounts with decades of tax-advantaged growth

- Any investment where earnings are automatically reinvested

Where compounding works against you:

- Credit card balances (often compounding daily at 20% or higher)

- High-interest debt like payday loans

- Student loans where interest capitalizes if unpaid during deferment

- Any loan where you only make minimum payments

“compounding is a friend to investors, but a foe to borrowers.” The math is identical in both cases. The only difference is which side of the equation you’re on.

The practical takeaway: if you carry a credit card balance at 22% APR, that debt is compounding against you faster than almost any investment can grow in your favor. Managing credit card debt aggressively before focusing on investing is often the smarter financial move. This is also why debt consolidation can change a borrower’s financial trajectory entirely.

Compounding benefits savers and investors but actively punishes borrowers who let balances sit. The asymmetry is real and significant.

Pro tip: Before you invest a single dollar, pay off any debt above 10% interest. The guaranteed “return” of eliminating high-interest debt almost always beats the expected return from the market.

The Rule of 72 and common compounding pitfalls

Not everyone wants to run formulas every time they’re curious about a financial decision. That’s where the Rule of 72 comes in. It’s a mental shortcut: divide 72 by your annual interest rate to estimate how many years it takes for your money to double.

Here’s how to use it in three steps:

- Find your expected annual return (for example, 8%).

- divide 72 by that number: 72 / 8 = 9.

- Your money should approximately double in 9 years at that rate.

The Rule of 72 is most accurate at interest rates between 6% and 10%, which conveniently covers many realistic long-term investment scenarios. At very low rates (under 2%) or very high ones (over 20%), the estimate drifts.

But the Rule has real limits. It assumes constant returns and ignores market volatility, taxes on gains, investment fees, and dividends that aren’t reinvested. A mutual fund with a 1% annual fee doesn’t just cost 1% of your balance each year. It costs you the compounded growth that money would have generated. Over 30 years, a 1% fee can reduce your final balance by 20% or more.

For a deeper look at compounding in real market conditions, these friction costs deserve serious attention. Also consider that time in the market consistently outperforms attempts to time entry and exit points.

Pro tip: Use the Rule of 72 as a quick gut-check to evaluate financial decisions, not as a precise planning tool. For retirement planning, always run the actual numbers.

A fresh perspective: Why most people underestimate compounding

Here’s something worth sitting with: most people intellectually understand compound interest and still fail to act on it. The problem isn’t knowledge. It’s psychology.

Humans are wired to think linearly. We see patterns in straight lines, not curves. So when someone tells you your $5,000 investment will grow into $40,000 over 30 years, it sounds abstract. The payoff is so far away it doesn’t feel real. That’s why starting early is advice that’s heard constantly but followed infrequently.

For young professionals, time is the key multiplier and the biggest competitive advantage over older investors. You don’t need more money. You need more time.

There’s also a counterpoint worth acknowledging. Some research suggests that aggregate shareholder returns can fall short of headline compound rates when dividends can’t be fully reinvested at scale or when market timing erodes actual outcomes. Real-world results include taxes, fees, and human behavior. They rarely match the theoretical model perfectly. But here’s the thing: even an imperfect version of compounding beats doing nothing by a wide margin. Start now, stay consistent, minimize fees, and let time do the heavy lifting.

Put your knowledge to use and grow your wealth

You now understand how compound interest works, how it differs from simple interest, and how it can either work for or against you depending on where it’s applied. The next step is putting this knowledge into a real plan. At finblog.com, we publish guides on saving, investing, managing debt, and building long-term financial freedom, written specifically for people who are serious about growing their wealth. If you’re ready to make compounding work for your life, start with our guide on getting started with compounding and explore what a smarter financial strategy looks like for your specific situation.

frequently asked questions

What is the basic definition of compound interest?

compound interest is interest calculated on your initial principal plus any previously earned interest, so your balance grows faster with every passing period.

How is compound interest different from simple interest?

Simple interest grows only on your original amount, while compound interest also grows on interest already earned, producing exponential rather than linear growth.

How can I use the Rule of 72?

Divide 72 by your annual interest rate to estimate doubling time. At 6 to 10% rates, this shortcut is remarkably accurate for quick planning decisions.

Does compounding help with debt or just investments?

Compounding applies to both. It grows your savings and investments, but also increases what you own on high-interest debt, making it critical to pay off balances quickly.

When is compounding most powerful?

Compounding is most powerful when you start early, allowing even modest contributions to grow into substantial amounts over decades.

Recommended

- Why Invest Early: Everything You Need to Know – Finblog

- Understanding the Benefits of Early Investing for Everyone – Finblog

- JPMorgan Predicts Bitcoin Could Surge to $170,000 Within a Year

- Rising interest rates and investment strategies in 2026 – Finblog

- Can You Turn $100 Into Thousands Trading Forex? | FxShop24 Marketplace