Many people use the terms saving and investing interchangeably, but this confusion can cost you thousands in missed opportunities or unnecessary risk. While both involve setting money aside, they serve fundamentally different purposes in your financial life. Saving protects your short-term needs with guaranteed security, while investing grows your wealth over time despite market fluctuations. Understanding when to use each strategy transforms your ability to build financial security and achieve your goals. This guide breaks down exactly what separates saving from investing, their unique risks and returns, and how to balance both for maximum benefit.

Table of Contents

- Key takeaways

- What is saving? Understanding its purpose, risk, and returns

- What is investing? How it differs in risk, returns, and time horizon

- Comparing saving and investing: risk, return, liquidity, and time horizon

- Balancing saving and investing: practical tips for working professionals

- Explore more financial insights and tools at Finblog

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Guaranteed short term protection | Saving offers guaranteed protection for immediate needs while investing carries risk for long term growth. |

| FDIC protection and liquidity | Savings provide FDIC insurance and instant access, whereas investments do not. |

| Long term growth potential | Investing historically delivers higher growth over the long term, often beating inflation. |

| Balance saving and investing | Effective financial planning balances both saving and investing to fit your goals and risk tolerance. |

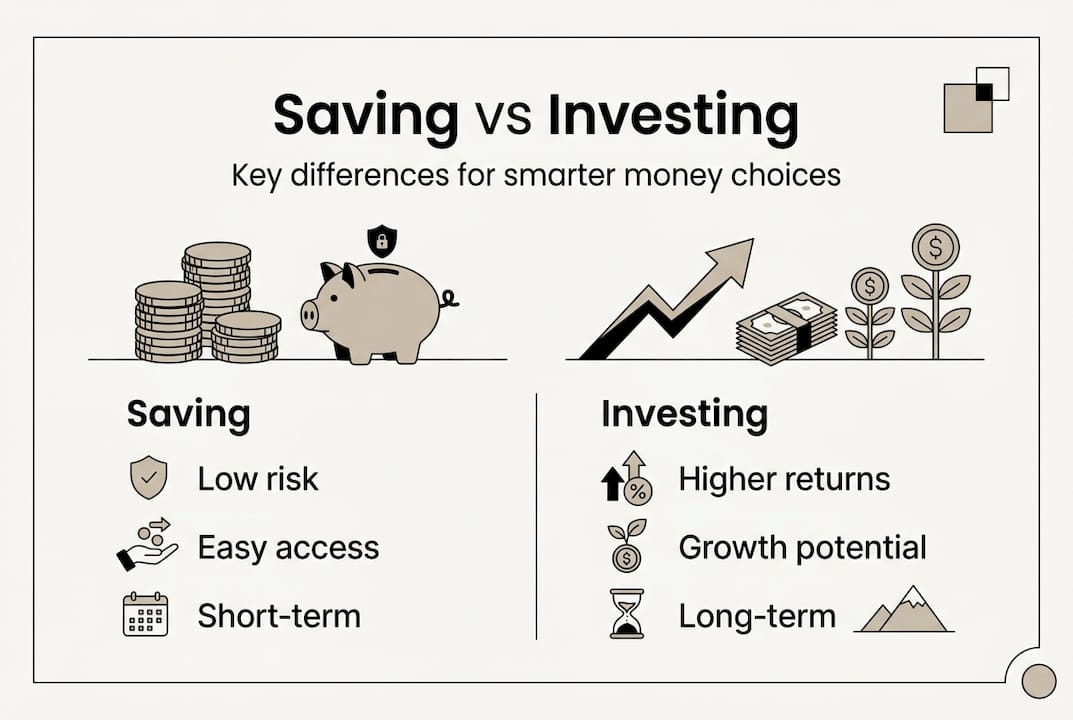

What is saving? Understanding its purpose, risk, and returns

Saving means placing money in secure accounts like savings accounts, certificates of deposit, and money market accounts. These products prioritize capital preservation over growth, making them ideal for short-term financial needs. Your principal remains protected regardless of economic conditions, giving you complete peace of mind for funds you’ll need soon.

FDIC insurance covers up to $250,000 per depositor at member banks, eliminating virtually all risk of losing your money. This government backing makes savings accounts the safest place for your emergency fund or down payment savings. Even if your bank fails, you receive your full balance back within days. No investment product offers this level of security.

Liquidity stands as saving’s greatest practical advantage. You can withdraw money instantly without penalties in most cases, though some accounts like CDs require you to keep funds deposited for a set term. This immediate access proves critical when unexpected expenses arise or opportunities require quick action. Your money stays available exactly when you need it.

Current returns on high-yield savings accounts range from approximately 3% to 5% in 2026, significantly higher than traditional savings accounts offering under 1%. While these rates beat keeping cash under your mattress, they barely keep pace with inflation over time. Your purchasing power stays relatively flat rather than growing substantially.

Savings work best for goals within the next five years. Building an emergency fund covering three to six months of expenses, saving for a wedding, or accumulating a house down payment all fit perfectly in savings accounts. The guaranteed returns and zero risk align with these shorter timelines where you cannot afford market volatility.

Pro Tip: Keep your emergency fund in a high-yield savings account to maximize returns while maintaining complete liquidity and FDIC protection for immediate access during crises.

What is investing? How it differs in risk, returns, and time horizon

Investing allocates money to assets like stocks, bonds, exchange-traded funds, and mutual funds. Unlike saving’s guaranteed stability, investing accepts market risk in exchange for substantially higher potential returns. Your account value fluctuates daily based on market conditions, sometimes dramatically during volatile periods. This uncertainty makes investing unsuitable for short-term needs.

No FDIC insurance protects investment accounts. If the market crashes, your portfolio value drops accordingly, and you could lose a significant portion of your principal. This fundamental difference from savings requires you to have a longer time horizon, allowing years or decades for markets to recover from downturns. The 2008 financial crisis saw some portfolios lose 50% of their value, though patient investors who held on eventually recovered and gained.

Expected returns historically average 4-7% real returns for equity investments after accounting for inflation. Over decades, this growth compounds dramatically, turning modest regular contributions into substantial wealth. A $500 monthly investment earning 7% annually grows to over $600,000 in 30 years, demonstrating why investing proves essential for long-term financial goals.

Liquidity in investment accounts varies considerably. While you can typically sell stocks or funds within days, the value you receive depends entirely on current market prices. Selling during a downturn locks in losses permanently. Some investments like real estate or private equity require months or years to liquidate. This reduced liquidity means you should only invest money you won’t need for at least five years.

Investing suits goals like retirement, college funding, or wealth accumulation where your timeline extends beyond five years. The longer your horizon, the more time you have to ride out market volatility and benefit from compound growth. Starting early amplifies these benefits exponentially through decades of compounding returns.

Pro Tip: Diversify your investments across multiple asset classes including domestic stocks, international stocks, bonds, and real estate to manage risk while improving potential returns through different market conditions.

| Investment Type | Risk Level | Expected Return | Liquidity | Best For |

|---|---|---|---|---|

| Individual Stocks | High | 8-10% potential | High | Experienced investors |

| Index Funds/ETFs | Moderate | 6-8% average | High | Most investors |

| Bonds | Low to Moderate | 3-5% typical | Moderate | Income, stability |

| Real Estate | Moderate to High | 6-9% potential | Low | Long-term wealth |

| Money Market Funds | Very Low | 3-4% current | Very High | Short-term investing |

Comparing saving and investing: risk, return, liquidity, and time horizon

Risk represents the most fundamental difference between saving and investing. Savings accounts carry virtually zero risk of principal loss thanks to FDIC insurance, while investments expose you to market volatility that can significantly reduce your account value. Understanding your personal risk tolerance helps determine the right balance. Conservative investors prioritize capital preservation, while aggressive investors accept higher volatility for greater growth potential.

Returns tell the flip side of the risk story. High-yield savings accounts currently offer 4-5% with zero risk, but historical equity returns average 4-7% real returns after inflation over decades. That seemingly small difference compounds dramatically over time. A $10,000 investment growing at 4% reaches $21,911 in 20 years, while 7% growth produces $38,697, nearly double the lower rate.

Liquidity determines how quickly you can access your money without penalties or value loss. Savings accounts provide immediate access with no restrictions beyond occasional withdrawal limits. Investment accounts require selling assets at current market prices, which may take days and could result in selling at a loss during downturns. This distinction makes savings essential for emergency funds and near-term goals.

Time horizon fundamentally shapes which strategy fits your goal. Money needed within five years belongs in savings where principal protection matters most. Goals beyond five years benefit from investing’s superior growth potential, as longer timeframes allow recovery from temporary market declines. A 30-year retirement timeline can weather multiple market cycles, while a two-year house fund cannot risk a market crash.

Protections differ dramatically between the two approaches. FDIC insurance guarantees your savings up to $250,000 per account, while investments offer no such safety net. However, brokerage accounts do carry SIPC insurance protecting up to $500,000 if the brokerage fails, though this doesn’t protect against market losses. Understanding these protections clarifies the security level of each strategy.

| Factor | Saving | Investing |

|---|---|---|

| Risk | Virtually none | Market dependent, can lose principal |

| Returns | 3-5% current rates | 4-7% historical real returns |

| Liquidity | Immediate access | Days to sell, value varies |

| Time Horizon | Under 5 years | 5+ years recommended |

| Protection | FDIC insured $250K | No principal protection |

| Best Use | Emergency funds, short-term goals | Retirement, wealth building |

| Tax Treatment | Interest taxed as income | Capital gains rates may apply |

Your personal circumstances determine the right mix. Consider these decision points:

- Assess your emergency fund status. Do you have three to six months of expenses in accessible savings? If not, prioritize building this foundation before investing significantly.

- Identify your financial goals and their timelines. List each goal with its target date to determine which require saving versus investing.

- Evaluate your risk tolerance honestly. Can you watch your account value drop 30% without panicking and selling? Your emotional response to volatility matters as much as your financial capacity for risk.

- Calculate your income stability and job security. Volatile income or uncertain employment suggests maintaining larger cash reserves in savings.

- Review your current allocation between saving and investing. Does it match your goals and risk tolerance, or have you drifted from your intended strategy?

Understanding liquidity in finance helps you appreciate why both strategies deserve places in your financial plan. They complement rather than compete with each other, serving different purposes in your overall wealth-building strategy.

Balancing saving and investing: practical tips for working professionals

Start by establishing a fully funded emergency fund before investing aggressively. This cash cushion covering three to six months of expenses protects you from forced asset sales during market downturns or personal crises. Without this foundation, you risk selling investments at losses to cover unexpected expenses, permanently damaging your long-term wealth building. Your emergency fund belongs in a high-yield savings account for maximum safety and accessibility.

Use investment accounts strategically for long-term goals exceeding five years. Retirement accounts like 401(k)s and IRAs offer tax advantages that amplify your growth over decades. Taxable brokerage accounts work well for goals between retirement and emergency savings, like future home purchases or children’s education. Match your account type to your goal’s timeline and tax situation for optimal results.

Avoid attempting to time the market by jumping in and out of investments. Research consistently shows that staying invested long term beats timing strategies, as missing just a few of the market’s best days dramatically reduces returns. Time in the market matters more than timing the market. Regular contributions through dollar-cost averaging smooth out volatility by buying more shares when prices drop and fewer when prices rise.

Diversify your investments across asset classes, sectors, and geographic regions to manage risk effectively. A portfolio mixing domestic stocks, international stocks, bonds, and real estate performs more consistently than concentrated holdings. As you age, gradually shift toward more conservative investments to protect accumulated wealth. A common guideline suggests holding your age as a percentage in bonds, though individual circumstances vary.

Regularly review and rebalance your portfolio and saving allocations at least annually. Market movements shift your asset allocation over time, potentially creating more risk than intended. Rebalancing sells appreciated assets and buys underperforming ones, maintaining your target allocation. Similarly, review whether your emergency fund still covers three to six months of current expenses as your lifestyle changes.

Pro Tip: Automate transfers to both savings and investment accounts immediately after each paycheck to stay disciplined and consistent, removing the temptation to spend money before saving or investing it.

Recognize the opportunity cost of holding excessive cash. While savings provide security, keeping too much in low-yield accounts means missing years of compound growth. Money sitting in savings earning 4% loses purchasing power over decades compared to invested funds potentially earning 7% or more. Calculate whether your cash reserves exceed your genuine short-term needs, and consider developing an investment strategy for surplus funds.

Consider your career stage and earning trajectory when balancing strategies. Early career professionals with rising incomes can accept more investment risk and smaller cash reserves, as their human capital provides a backup. Mid-career workers supporting families need larger emergency funds and balanced portfolios. Those approaching retirement should emphasize capital preservation and income generation over aggressive growth.

Understand why investing for retirement proves essential for financial security. Social Security replaces only about 40% of pre-retirement income for average earners, leaving a substantial gap you must fill through personal savings and investments. Starting early allows compound growth to do the heavy lifting, while delaying forces you to save much larger percentages of income later.

Explore more financial insights and tools at Finblog

Your journey to financial security doesn’t end with understanding saving versus investing. Finblog offers comprehensive resources to deepen your knowledge and refine your strategies. Our library includes detailed guides on everything from emergency fund optimization to advanced portfolio construction, all designed for working professionals and individual investors.

Explore our complete saving vs investing guide for additional perspectives and case studies showing how others balance these strategies. Learn specific techniques for maximizing returns while managing risk appropriately for your situation. Our articles break down complex financial concepts into actionable steps you can implement immediately.

Discover proven frameworks for investment strategy development that align with your unique goals, timeline, and risk tolerance. Whether you’re just starting or optimizing an existing portfolio, our resources provide the clarity and confidence you need to make informed decisions. Join thousands of readers building stronger financial futures through education and smart planning.

Frequently asked questions

What’s the main difference between saving and investing?

Saving places money in secure, low-risk accounts like savings accounts or CDs for short-term needs, preserving your principal with FDIC insurance and providing immediate access. Investing allocates money to assets like stocks and bonds for long-term growth, accepting market risk and potential principal loss in exchange for historically higher returns. The key distinction lies in risk level, time horizon, and return expectations.

Is it better to save or invest first?

Prioritize saving an emergency fund covering three to six months of expenses before investing significantly. This cash cushion protects you from forced asset sales during crises or market downturns. Once you’ve established this foundation, shift focus to investing for long-term goals like retirement to build wealth through compound growth over decades.

Can I lose money by saving?

Saving in FDIC-insured accounts carries virtually no risk of principal loss, as the government guarantees deposits up to $250,000 per account. However, low returns typically ranging from 3-5% often fail to keep pace with inflation over long periods, effectively reducing your purchasing power. Your account balance stays stable, but what that money can buy gradually diminishes.

How long should I keep money in savings before investing?

Savings work best for short-term goals within five years or emergency funds needing immediate accessibility. Money you won’t need for at least five years should generally be invested to leverage growth potential and compound returns. The longer your timeline, the more sense investing makes, as extended periods allow recovery from temporary market volatility and maximize wealth accumulation.