Credit card debt can pile up quickly and leave you feeling trapped. Yet almost half of Americans carry a balance each month and the average household credit card debt now exceeds $7,000. Most people assume getting rid of that debt takes drastic sacrifices or a huge income boost. The real shift happens when you follow a few practical steps that actually fit your everyday life.

Table of Contents

- Step 1: Identify Your Total Credit Card Debt

- Step 2: Create a Comprehensive Budget

- Step 3: Prioritize Your Debts Strategically

- Step 4: Negotiate With Creditors Proactively

- Step 5: Implement A Repayment Plan Consistently

- Step 6: Monitor Progress And Adjust As Necessary

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Identify total credit card debt | Gather all outstanding balances, APR, and minimum payments for a clear financial picture. |

| 2. Create a detailed budget | Track income and expenses to manage finances and identify areas to cut unnecessary costs. |

| 3. Prioritize debt repayment strategically | Use methods like debt avalanche or snowball to focus on high-interest or smaller debts first. |

| 4. Negotiate with creditors proactively | Communicate with creditors to request lower interest rates or flexible payment plans to ease financial pressure. |

| 5. Monitor progress and adjust regularly | Review your financial situation monthly to track debt reduction and make necessary adjustments for continued progress. |

Step 1: Identify Your Total Credit Card Debt

Begin your journey of managing credit card debt by developing a clear and comprehensive understanding of your current financial landscape. This critical first step requires honest self assessment and precise documentation of all outstanding credit card balances.

Gathering Your Credit Card Information

Start by collecting all credit card statements from the past two to three months. Pull physical statements or download digital copies from your online banking platforms. You will want to compile a complete list that includes every credit card account, regardless of whether it is currently active or has been temporarily unused.

For each credit card, record the following essential details:

- Current outstanding balance

- Annual percentage rate (APR)

- Minimum monthly payment requirement

- Total credit limit

The Federal Trade Commission recommends maintaining meticulous records of your debt to effectively communicate your financial situation with creditors. This documentation will become your strategic roadmap for debt reduction.

Calculating Your Total Debt Landscape

Once you have gathered all statements, add up the total outstanding balances across all cards. This number represents your total credit card debt and provides a stark, honest picture of your current financial obligations. Do not feel discouraged by the total amount — recognition is the first step toward meaningful financial transformation.

Pay special attention to cards with the highest interest rates, as these will cost you the most money over time. Identifying these high-interest accounts will be crucial in developing a strategic debt repayment plan in subsequent steps of your financial recovery journey. Your goal is not just to understand the numbers, but to develop a proactive strategy for reducing and ultimately eliminating your credit card debt.

Step 2: Create a Comprehensive Budget

Creating a comprehensive budget is your strategic blueprint for managing credit card debt and achieving financial freedom. This crucial step transforms your financial awareness from vague understanding to precise control, allowing you to allocate resources strategically and reduce unnecessary spending.

Begin by tracking every single financial input and output with unwavering commitment. Use digital tools like spreadsheet applications or dedicated budgeting apps that can automatically categorize your expenses. Bank statements and credit card records will serve as your primary source documents for understanding your actual spending patterns.

Breaking Down Income and Expenses

Calculate your total monthly take-home income after taxes. This includes your primary salary, any side hustles, freelance work, or additional revenue streams. Next, categorize your expenses into fixed and variable categories. Fixed expenses include rent, utilities, insurance, and minimum debt payments. Variable expenses encompass groceries, entertainment, dining out, and discretionary purchases.

As MoneySmart recommends, create a realistic budget that accounts for both essential and non-essential spending. Your goal is not extreme deprivation but strategic financial management. Look for areas where you can trim unnecessary expenses — subscription services you rarely use, frequent takeout meals, or impulse purchases.

Key expense tracking categories should include:

- Housing costs

- Transportation expenses

- Food and groceries

- Utilities

- Insurance premiums

- Debt payments

- Personal care

- Entertainment

Review your budget monthly and adjust as needed. Successful budgeting is an ongoing process of refinement. Learn more about optimizing your financial planning to develop sustainable money management skills that extend beyond debt reduction.

Step 3: Prioritize Your Debts Strategically

Strategically prioritizing your debts is a critical step in managing credit card debt effectively. This approach transforms your debt repayment from a random process into a calculated financial strategy that minimizes interest expenses and accelerates your path to financial freedom.

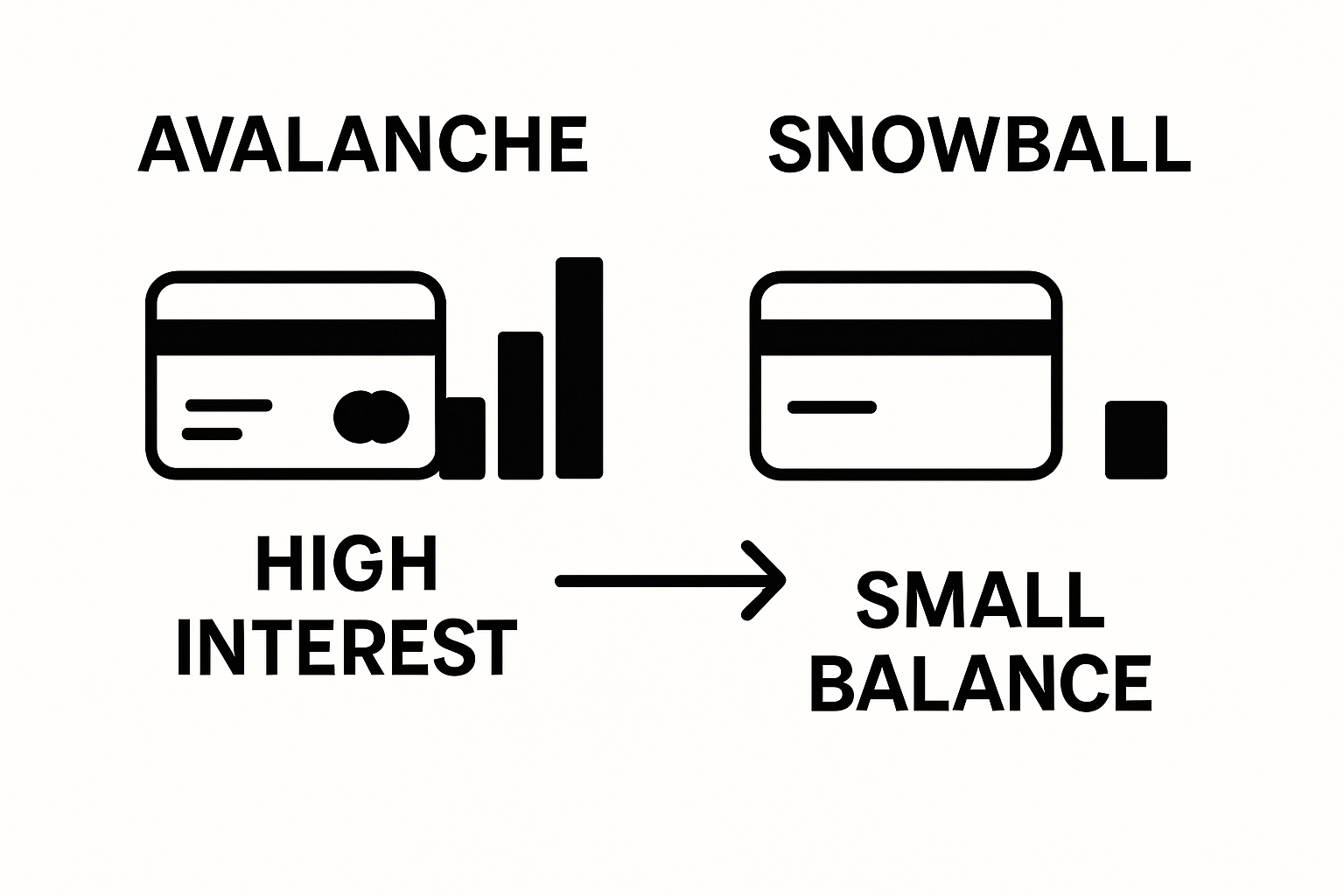

Two primary methods emerge as powerful approaches to debt reduction: the debt avalanche and debt snowball techniques. Each method offers unique psychological and financial benefits, and understanding their nuances will help you choose the most suitable approach for your personal financial situation.

The debt avalanche method targets high-interest credit cards first, systematically reducing the total amount of interest you’ll pay over time. Begin by ordering your credit card debts from the highest interest rate to the lowest. Allocate maximum possible payments toward the highest-interest card while maintaining minimum payments on other cards. According to research from the Consumer Financial Protection Bureau, this approach mathematically saves you the most money in the long term.

Alternatively, the debt snowball method prioritizes paying off the smallest balance first, creating psychological momentum through quick wins. This approach can be particularly motivating for individuals who need visible progress to maintain financial discipline. Each time you eliminate a small debt, you experience a sense of accomplishment that can propel you forward in your debt reduction journey.

Below is a comparison table summarizing the differences between the debt avalanche and debt snowball methods, helping you choose the strategy that best fits your financial approach.

| Method | How It Works | Key Benefit | Best For |

|---|---|---|---|

| Debt Avalanche | Pay off highest-interest debt first; pay minimums on rest | Saves the most money on interest | Maximizing savings |

| Debt Snowball | Pay off smallest balance first; pay minimums on others | Builds quick confidence/momentum | Needing fast motivation |

Key considerations for debt prioritization include:

- Total outstanding balance

- Interest rates

- Minimum payment requirements

- Potential penalties for late payments

Whichever method you choose, consistency is paramount. Commit to your chosen strategy and make extra payments whenever possible.

Track your progress meticulously, celebrating small victories while maintaining focus on your ultimate goal of becoming debt-free. Learn more about developing sustainable financial strategies that extend beyond immediate debt management.

Track your progress meticulously, celebrating small victories while maintaining focus on your ultimate goal of becoming debt-free. Learn more about developing sustainable financial strategies that extend beyond immediate debt management.

Step 4: Negotiate with Creditors Proactively

Proactively negotiating with creditors is a powerful strategy that can significantly reduce your financial burden and create breathing room in your debt management journey. This step requires courage, preparation, and strategic communication with your credit card companies.

Before initiating conversations, gather comprehensive documentation of your current financial situation. Compile your income statements, budget breakdown, and a detailed explanation of why you are experiencing financial hardship. Creditors are more likely to work with you when you demonstrate transparency and a genuine commitment to resolving your debt.

When you contact your credit card companies, remain calm, professional, and focused on finding mutually beneficial solutions. Key negotiation strategies include requesting lower interest rates, exploring temporary payment reduction plans, or discussing potential debt consolidation options. According to the Federal Trade Commission, many creditors are willing to modify payment terms to prevent complete default.

Prepare specific requests before making the call. Potential negotiation outcomes might include:

- Reduced interest rates

- Waived late payment fees

- Extended payment timelines

- Temporary hardship programs

- Potential partial debt forgiveness

During negotiations, maintain a professional tone and clearly articulate your commitment to repaying your debt. Avoid making emotional appeals and instead focus on presenting a logical, well-documented case for why modifying your current payment terms would benefit both parties. Discover more about developing effective financial negotiation skills to enhance your long-term financial management approach.

Remember that successful negotiation is about finding a sustainable solution. Document every conversation, including the date, time, representative’s name, and details of any agreements reached. Always request written confirmation of any negotiated terms before concluding the discussion.

Step 5: Implement a Repayment Plan Consistently

Implementing a consistent repayment plan transforms your debt management strategy from theoretical concept to tangible financial progress. This critical step requires disciplined execution, unwavering commitment, and a systematic approach to reducing your credit card balances.

Automate your debt repayment process to eliminate human error and psychological resistance. Set up automatic monthly payments that exceed the minimum requirement for each credit card. Digital banking tools and mobile apps can help you schedule these payments precisely, ensuring you never miss a deadline. By automating payments, you remove the emotional friction associated with manually transferring funds and reduce the likelihood of accidentally skipping a payment.

Create a dedicated debt repayment fund separate from your primary checking account. This psychological separation helps you mentally compartmentalize your debt reduction strategy. Allocate a fixed percentage of your monthly income into this fund, treating debt repayment as a non-negotiable financial priority. Consider exploring additional income streams like freelance work, selling unused items, or taking on temporary part-time assignments to accelerate your debt elimination process.

Tracking your progress is crucial for maintaining motivation. Develop a visual representation of your debt reduction journey, such as a spreadsheet or debt tracking app that shows your declining balances. Celebrate incremental milestones to maintain your emotional momentum:

- First 10% of total debt eliminated

- Paying off individual credit cards

- Reducing total debt by significant percentages

- Achieving lower interest rates through consistent payments

Learn more about developing sustainable financial strategies that support long-term financial health. Remember that consistency trumps perfection. Some months you might pay more, some less, but the key is maintaining a steady, committed approach to debt reduction. Your future financial freedom depends on the disciplined actions you take today.

Step 6: Monitor Progress and Adjust as Necessary

Monitoring your debt reduction progress is more than just tracking numbers — it is about understanding your financial journey, recognizing patterns, and remaining adaptable. This critical step transforms your debt management from a static plan to a dynamic, responsive strategy that grows with your changing financial landscape.

Establish a monthly financial review ritual where you comprehensively examine your debt reduction progress. During this review, pull your credit card statements, track your current balances, calculate the total interest paid, and compare your actual spending against your original budget. Digital tools and spreadsheet applications can help you visualize your progress through graphs and trend lines, making the data more engaging and easier to interpret.

Pay close attention to both quantitative and qualitative indicators of financial health. Quantitative metrics include reduced total debt balance, lower interest payments, and increased credit score. Qualitative indicators involve your emotional relationship with money — feeling less stressed about finances, experiencing more control, and developing healthier spending habits. According to the National Credit Union Administration, managing debt is a gradual process that requires continuous assessment and adjustment.

Key aspects to evaluate during your monthly financial review include:

- Total debt reduction amount

- Changes in interest rates

- Unexpected expenses

- Income fluctuations

- Credit score improvements

Remain flexible and prepared to modify your strategy. If you receive a bonus, unexpected income, or experience a reduction in expenses, immediately redirect those funds toward debt reduction. Learn more about developing sustainable financial strategies that support long-term financial resilience. Your ability to adapt and stay committed will ultimately determine your success in achieving financial freedom.

Here is a checklist table to help you organize and monitor your monthly financial review when tracking progress toward credit card debt reduction.

| Review Item | Description | Completion Status |

|---|---|---|

| Review credit card balances | Check current outstanding balances on all accounts | |

| Track total interest paid | Record interest accrued during the past month | |

| Compare spending to budget | Analyze if actual spending aligns with your budget | |

| Evaluate debt reduction | Calculate total debt paid down this month | |

| Check credit score | Review credit score for changes or improvements | |

| Assess any new expenses | Identify unexpected or irregular expenses incurred | |

| Adjust strategy if needed | Update repayment plan based on new information |

Take Control of Your Debt Journey with Expert Support from FinBlog

Facing mounting credit card balances and feeling overwhelmed by high interest rates can leave you frustrated and uncertain about the future. You have already taken the important first steps by identifying your debt, creating a plan, and trying to stay consistent with payments, but sticking with a repayment strategy can be difficult without the right tools and support. Whether you struggle with budgeting or need guidance on communicating with creditors, the path to financial freedom often requires more than self-education.

Ready to turn your knowledge into action? Let FinBlog help you accelerate your progress. Our financial experts offer personalized strategies that go far beyond general advice. Unlock insights for building sustainable habits, track your debt reduction using proven tools, and learn how to negotiate with lenders more effectively. Learn more about our debt management resources and take back control of your finances. Start your journey now—every day you wait is another day interest accumulates. Fill out our secure contact form today and get one step closer to a debt-free life.

Frequently Asked Questions

How do I calculate my total credit card debt?

To calculate your total credit card debt, gather all your credit card statements and add up the outstanding balances across each card. Be sure to document the current balance, annual percentage rate (APR), minimum monthly payment, and total credit limit for each account.

What is the difference between the debt avalanche and debt snowball methods?

The debt avalanche method focuses on paying off high-interest credit cards first to save on interest costs, while the debt snowball method targets the smallest balances first to build momentum through quick wins. Choose the method that best suits your financial situation and psychological needs.

How can I negotiate lower interest rates with my creditors?

To negotiate lower interest rates, contact your credit card companies and present a well-documented case of your financial situation. Be calm and professional, and request specific adjustments such as lower rates or waiving fees. Demonstrating a commitment to repaying your debt increases your chances of a favorable outcome.

What should I do if I experience changes in my income while managing my debt?

If your income changes, reassess your budget and repayment plan immediately. If you receive extra income, consider using it to pay down debts faster. Being flexible and ready to adjust your strategy can help you stay on track toward achieving financial freedom.