TL;DR:

- Setting personal financial milestones based on life stages helps create achievable goals.

- Regularly assessing your current finances and tracking progress keeps you on course.

- Personalized plans, flexibility, and consistent reviews are key to long-term financial success.

Most people feel a quiet, persistent worry that they’re falling behind on the big financial goals that matter most. Retirement feels abstract. Homeownership feels out of reach. And without a clear plan, you end up making decisions by default rather than by design. That frustration is real, and it’s more common than you’d think. This guide gives you a practical, stage-by-stage framework for identifying your most important financial milestones, assessing where you stand today, building a realistic timeline, and staying on track even when life throws curveballs. By the time you finish reading, you’ll have a personalized blueprint for turning financial anxiety into forward momentum.

Table of Contents

- Define your financial milestones by life stage

- Assess your current financial status

- Map out milestone timelines and actionable steps

- Track progress, adapt, and avoid common pitfalls

- What most milestone guides get wrong—and how to do better

- Take the next step: Build your milestone map now

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Customize milestones | Design your financial milestones based on your age, goals, and personal circumstances. |

| Track and adjust | Regularly review progress and adapt your plan to stay on course as life changes. |

| Start with the basics | Prioritize an emergency fund and debt payoff before aiming for larger, long-term goals. |

| Benchmarks are guides | Use common targets like 3x income by 45 as references, but don’t let them discourage your unique journey. |

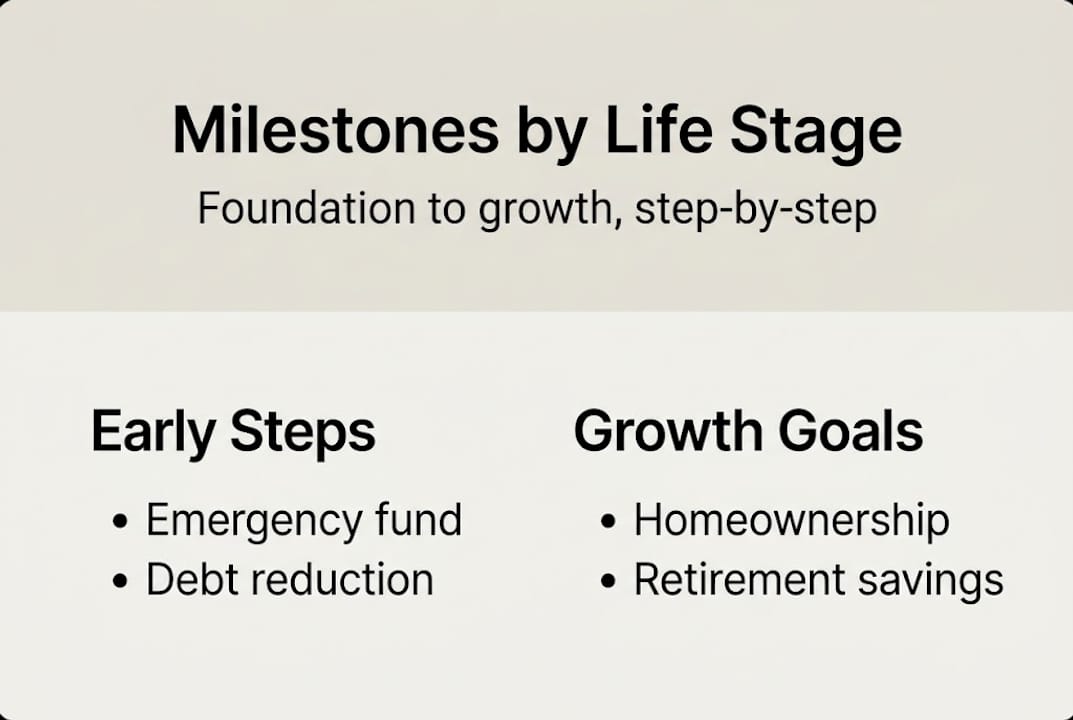

Define your financial milestones by life stage

Now that you know what this guide will cover, it’s essential to clarify exactly which milestones you’ll be planning for. Not every goal applies to every person, and that’s the point. Financial milestones are personal checkpoints, not a universal checklist.

Financial milestones by life stage are structured starting with foundational goals like building an emergency fund covering 3 to 6 months of expenses, eliminating high-interest debt, and capturing your employer’s full 401(k) match during early adulthood, roughly ages 22 to 30. These aren’t optional steps. They’re the foundation everything else is built on.

As you move into your 30s and 40s, milestones shift toward homeownership, college savings if you have children, and accelerating your net worth growth. By your 50s, the focus becomes maximizing retirement contributions and stress-testing your plan. Knowing which phase you’re in helps you stop chasing goals that aren’t yours yet and start making real progress on the ones that are.

Here’s a quick breakdown of milestone categories by life stage:

| Life stage | Key milestones |

|---|---|

| Early career (22-30) | Emergency fund, debt payoff, 401(k) match |

| Building phase (30-45) | Home purchase, college savings, net worth growth |

| Pre-retirement (45-60) | Max retirement contributions, insurance review |

| Retirement (60+) | Withdrawal strategy, estate planning |

To customize your list, start by asking yourself a few questions:

- What major life events are you planning in the next 5 years?

- Do you have dependents whose needs affect your timeline?

- Is homeownership a priority, or does renting fit your lifestyle better?

- Are you carrying high-interest debt that’s slowing everything else down?

Your answers shape your personal milestone map. Emergency fund planning is almost always the right first move regardless of age, because it protects every other goal you’re working toward. And if you’re thinking across generations, generational financial planning can help you see how today’s decisions ripple forward for decades.

Pro Tip: Write your top three milestones on paper and put them somewhere visible. People who write down specific goals are significantly more likely to achieve them than those who keep goals vague and mental.

Assess your current financial status

Once you’ve defined your target milestones, the next step is to get a clear understanding of where you’re starting. You can’t map a route without knowing your current location.

Start by listing everything you own and everything you owe. Your assets include your savings accounts, retirement accounts, investment accounts, home equity if you own property, and any other items of real value. Your liabilities include credit card balances, student loans, auto loans, and your mortgage if applicable. Subtract liabilities from assets and you have your net worth.

Here’s a simple snapshot template to get you started:

| Category | Examples | Your amount |

|---|---|---|

| Liquid assets | Checking, savings, cash | $ |

| Invested assets | 401(k), IRA, brokerage | $ |

| Property | Home equity, vehicles | $ |

| Debts | Credit cards, loans | $ |

| Net worth | Assets minus debts | $ |

Some popular frameworks suggest benchmarks like having 3x your income saved by age 45, a figure cited by JP Morgan among others. But most households fall behind these benchmarks, and that’s actually normal. The benchmark exists to give you direction, not to make you feel like a failure.

Here’s what matters more than the benchmark:

- Is your net worth moving in the right direction year over year?

- Are you consistently saving something, even if it’s not the “ideal” amount?

- Do you have a buffer against emergencies, or would one car repair derail your finances?

Understanding the emergency fund importance in your overall financial picture is critical here. Without that buffer, every other milestone becomes fragile. Your baseline snapshot isn’t a report card. It’s a starting line. Once you know where you are, you can start measuring real progress.

Map out milestone timelines and actionable steps

With your baseline in hand, you’re ready to plot out how and when you’ll hit each critical milestone. A goal without a timeline is just a wish.

The key is breaking each milestone into smaller, specific sub-goals with deadlines attached. If your goal is to build a six-month emergency fund of $18,000, that’s $1,500 a month for 12 months, or $750 a month for 24 months. Suddenly it feels real and achievable. Prioritizing foundational goals first is critical for long-term financial stability, and that means tackling your emergency fund and high-interest debt before you focus on investing or saving for a home.

Here’s a step-by-step approach for building your milestone timeline:

- List your milestones in order of priority. Emergency fund first, then high-interest debt, then longer-term goals.

- Assign a target date to each milestone. Be realistic about your income and current obligations.

- Break each milestone into monthly savings or payoff targets. Smaller numbers feel more manageable and keep you motivated.

- Identify what needs to change in your budget to make those monthly targets possible.

- Build in a buffer of 10 to 15 percent on your timeline so that a single bad month doesn’t blow up your entire plan.

- Review the plan quarterly to see if your targets are still realistic.

If you’re carrying high-interest debt, learning how to reduce debt fast can free up significant cash flow for other milestones. Exploring debt repayment strategies like the avalanche or snowball method can help you choose the approach that fits your psychology and your numbers.

Pro Tip: If you’re behind on your timeline, don’t extend every deadline at once. Pick one milestone to accelerate and focus your extra effort there. Momentum on a single goal often creates habits that carry over to the next one.

Track progress, adapt, and avoid common pitfalls

Planning is nothing without follow-through. Here’s how to stay on track and adapt as life changes.

The most effective way to maintain momentum is to track your progress consistently. Use a spreadsheet, a personal finance app like Mint or YNAB, or even a simple notebook. What matters is that you’re checking in regularly and comparing your current position to your planned milestones.

Schedule a formal milestone review every six months. This doesn’t need to be complicated. Sit down, update your net worth snapshot, check your progress on each active milestone, and ask yourself whether your priorities have shifted. Life changes fast, and your plan needs to keep up.

“Regularly reviewing your progress against established financial milestones helps ensure sustained progress and timely adjustments.”

Here are the most common pitfalls that derail even well-intentioned milestone plans:

- Neglecting insurance. A single medical event or disability without adequate coverage can wipe out years of progress.

- Ignoring small debts. Small balances with high interest rates quietly drain your cash flow every month.

- Lifestyle inflation. Every raise that goes straight into a bigger lifestyle is a raise that doesn’t move your milestones forward.

- Skipping reviews. Plans that aren’t revisited become outdated and eventually abandoned.

- Quitting after a setback. Missing a month’s savings target is not failure. It’s data. Adjust and keep going.

If debt is your biggest obstacle, the debt snowball method is a proven way to build psychological momentum by eliminating smaller balances first. For revolving debt, managing credit card debt effectively can stop the bleeding quickly and redirect that cash toward your actual goals.

What most milestone guides get wrong—and how to do better

Most milestone guides hand you a list of benchmarks and call it a plan. Hit 3x your income by 45. Own a home by 35. Max your IRA every year. These numbers aren’t wrong, but treating them as universal truth is a mistake.

Most households fall short of standard benchmarks, which means the benchmarks are describing an ideal, not a reality. Your earning trajectory, family situation, career path, and values are unique. A freelancer in their 30s rebuilding after a business setback is not failing because they don’t match a benchmark designed for a corporate employee with steady raises.

What actually works is a plan built around your specific numbers, reviewed regularly, and adjusted honestly. The people who reach their financial goals aren’t the ones who followed a generic checklist perfectly. They’re the ones who kept showing up after setbacks, recalibrated their timelines, and stayed connected to why the goals mattered in the first place. Financial planning for couples adds another layer of complexity, because two people’s goals, incomes, and risk tolerances all need to align. But the principle is the same: personalization beats perfection every time.

Benchmarks are useful as a compass. They’re not a verdict on your worth or your future.

Take the next step: Build your milestone map now

You’re now ready to turn your vision into a step-by-step action plan, and we’re here to help you do exactly that. At Finblog, we’ve built a library of practical, no-fluff resources designed for people who are serious about reaching their financial goals. Whether you’re just getting started with your first emergency fund guide or you’re ready to tackle debt freedom and long-term wealth building, you’ll find detailed guides that meet you where you are. Explore our tools, bookmark the resources that match your current milestone, and take one concrete action today. Progress compounds, and the best time to start building your milestone map is right now.

Frequently asked questions

What is the most important first financial milestone?

Building an emergency fund covering 3 to 6 months of living expenses is the recommended first milestone because it protects every other goal you’re working toward.

Are benchmarks like ‘3x income by age 45’ realistic for most people?

Most households fall short of these benchmarks, so they’re best used as directional guides rather than strict pass-or-fail standards.

How often should I review my financial milestones?

Review your milestones at least twice a year and after any major life event, since timely adjustments are what keep your plan relevant and achievable.

What if I’m behind on most milestones for my age?

Focus on progress over perfection. Personalized planning always outperforms chasing an arbitrary number, so adjust your timeline, prioritize foundational steps, and keep moving forward.