Many professionals feel stuck, unsure how to begin their journey toward financial independence. The path forward seems complex, with conflicting advice everywhere. This guide provides a clear, actionable roadmap with specific steps you can implement immediately to take control of your finances, eliminate debt, build wealth through smart investing, and create the freedom you deserve.

Table of Contents

- Understanding Your Financial Situation

- Setting Realistic Financial Goals

- Creating And Maintaining A Budget

- Debt Elimination Strategies

- Automated Investment Strategies

- Diversifying Income Streams

- Common Mistakes And Troubleshooting

- Expected Timelines And Outcomes

- Explore Finblog’s Resources To Accelerate Your Journey

- What Is The First Step Toward Financial Independence?

- How Much Should I Save Monthly For Financial Independence?

- What Are The Best Investment Types For Beginners On This Path?

- How Do I Stay Motivated Throughout The Process?

Key takeaways

| Point | Details |

|---|---|

| Assess your complete financial picture first | List all income sources, categorize expenses, calculate net worth, and check your credit score to establish your baseline. |

| Eliminate high-interest debt aggressively | Use the debt avalanche method to pay off debts with the highest interest rates first, saving thousands in interest payments. |

| Automate investments and diversify income | Set up automatic monthly contributions to index funds and build multiple income streams including side businesses and passive investments. |

| Maintain discipline with budgeting | Use the 50/30/20 rule to allocate income toward needs, wants, and savings while staying flexible for life changes. |

| Review regularly and avoid common pitfalls | Track expenses consistently, resist emotional investing decisions, and adjust goals to stay motivated and on track. |

Understanding your financial situation

You can’t plan a route without knowing your starting point. Creating a comprehensive snapshot of your finances forms the foundation for every decision ahead. This clarity removes guesswork and reveals opportunities you might miss otherwise.

Start by listing all income sources. Include your primary salary, freelance work, rental income, dividends, and any variable earnings. Don’t overlook irregular income like annual bonuses or seasonal work. Tracking these over three months gives you an accurate average to work with.

Next, categorize your monthly expenses into fixed costs like rent and insurance, variable costs like groceries and entertainment, and discretionary spending. Apps or simple spreadsheets work equally well. The goal is identifying patterns and spotting areas where small changes create big savings. Most people discover they spend 20 to 30% more than they thought on categories like dining out or subscriptions.

Calculate your net worth by listing all assets including savings accounts, investment portfolios, retirement funds, and property values. Subtract all liabilities like credit card balances, student loans, car loans, and mortgages. This number might surprise you, but it’s your honest baseline. Many people on the steps to financial freedom for lasting independence discover their net worth is lower than expected, which actually motivates better decisions.

Finally, check your credit score and review interest rates on existing debts. Your credit score affects loan rates, insurance premiums, and even rental applications. Understanding where you stand helps you prioritize improvements. If your score needs work, focus on paying bills on time and reducing credit utilization below 30%. Following a structured financial freedom roadmap achieve independence ensures you address these fundamentals systematically.

Setting realistic financial goals

Goals without numbers and deadlines remain wishes. Transform vague intentions into specific targets that drive daily decisions and maintain momentum through inevitable challenges.

Tie each goal to your budget and a clear timeline. Instead of “save more money,” commit to “save $15,000 for emergency fund by December 2026.” Specificity creates accountability. Review your income and expense assessment to determine realistic monthly contributions. If you earn $5,000 monthly and can allocate 20%, that’s $1,000 toward goals.

Set challenging but attainable savings targets. Research shows people achieve more when goals stretch their capabilities without feeling impossible. Aim to save 20 to 30% of income if your situation allows, but start with 10% if that’s realistic for you now. The financial independence retire early guide demonstrates how consistent saving rates compound dramatically over time.

Align goals with your personal priorities to maintain motivation. If travel matters most, create a dedicated fund for it. If early retirement drives you, focus contributions toward investment accounts. When goals reflect your values, you’ll resist temptation more easily. Learning how to increase motivation naturally helps during difficult stretches when progress feels slow.

Break larger goals into smaller milestones. A $100,000 investment portfolio feels overwhelming, but saving your first $5,000, then $10,000, then $25,000 provides regular wins. Celebrate these achievements. Consider using how to create personal action plans to structure your approach with detailed steps and checkpoints.

Pro Tip: Write your top three financial goals on a card and review them every morning. This simple habit keeps priorities front of mind when making spending decisions throughout the day.

Creating and maintaining a budget

A budget isn’t restriction, it’s permission to spend guilt-free on what matters while protecting your future. Think of it as a spending plan that directs money toward your goals automatically.

Implement the 50/30/20 budgeting rule as your framework. Allocate 50% of after-tax income to needs like housing, utilities, groceries, insurance, and minimum debt payments. Direct 30% toward wants including dining out, entertainment, hobbies, and non-essential purchases. Channel the remaining 20% into savings and debt repayment beyond minimums. This structure balances current enjoyment with future security.

Track expenses regularly using whatever method you’ll actually maintain. Apps like Mint or YNAB sync with bank accounts automatically. Spreadsheets offer more customization. Even a simple notebook works if you use it consistently. The tracking itself changes behavior because awareness precedes change. Review spending weekly at first, then monthly once habits solidify.

Adjust your budget for life changes like income shifts, new expenses, or changing priorities. A rigid budget breaks under pressure. When you get a raise, immediately increase your savings rate before lifestyle inflation creeps in. If expenses jump unexpectedly, temporarily reduce wants rather than abandoning the system. The how to create a budget step guide walks through adapting your plan as circumstances evolve.

Maintain discipline but stay flexible to avoid burnout. Build small rewards into your budget for hitting milestones. If you save $500 extra one month, allocate $50 toward something enjoyable. Extreme restriction leads to binge spending that derails progress. Sustainable budgeting feels manageable long term.

Pro Tip: Schedule a monthly money date with yourself or your partner. Review spending, celebrate wins, and adjust categories as needed. Making it routine removes the stress of constant monitoring.

Debt elimination strategies

Debt steals your future income and limits choices. Eliminating it, especially high-interest balances, accelerates wealth building more dramatically than almost any other financial move you can make.

Identify and list all debts with their interest rates, minimum payments, and balances. Create a simple table or use a debt tracker app. Seeing everything in one place often reveals the true cost. Credit cards charging 18 to 24% APR should trigger urgency.

Eliminating high-interest debt using the debt avalanche method accelerates wealth building by targeting the most expensive obligations first. Here’s how it works:

- Continue making minimum payments on all debts to avoid penalties and credit damage.

- Identify the debt with the highest interest rate regardless of balance size.

- Direct every extra dollar toward that highest-rate debt while maintaining minimums on others.

- Once the first debt is eliminated, roll that entire payment amount to the next highest-rate debt.

- Repeat this process, creating an avalanche effect as payments compound with each eliminated debt.

This mathematical approach saves more money than alternatives like the debt snowball method, which prioritizes smallest balances first for psychological wins.

Consider balance transfers with 0% APR offers to reduce interest temporarily. Many credit cards offer 12 to 18 months interest-free on transferred balances. This strategy works if you commit to aggressive repayment during the promotional period and avoid the trap of accumulating new charges. Read terms carefully because balance transfer fees typically range from 3 to 5%.

| Strategy | Best For | Key Benefit | Caution |

|---|---|---|---|

| Debt Avalanche | Maximum interest savings | Pays least total interest | Requires discipline |

| Balance Transfer | High APR credit cards | 0% interest period | Transfer fees apply |

| Debt Consolidation | Multiple high-rate debts | Single monthly payment | May extend repayment |

| Extra Payments | Any debt type | Shortens timeline | Must exceed minimums |

Avoid accumulating new high-interest debt during your payoff period. Cut up cards if necessary, or freeze them in a block of ice for emergency-only access. The debt repayment strategies achieve financial freedom article explores additional approaches including negotiating lower rates directly with creditors.

For comprehensive strategies covering everything from credit cards to student loans, review how to reduce debt fast and master managing credit card debt for detailed tactics.

Pro Tip: Every time you eliminate a debt completely, immediately redirect that payment amount into savings or investments rather than absorbing it back into your spending. This locks in your progress permanently.

Automated investment strategies

Manual investing invites emotional mistakes and inconsistency. Automation removes human error, builds wealth steadily, and frees mental energy for other priorities.

Automating monthly investments into diversified index funds removes emotional bias and ensures consistent wealth accumulation regardless of market conditions. Set up automatic transfers from your checking account to investment accounts on the same day you receive income. This “pay yourself first” approach treats investing like any other non-negotiable bill.

Use dollar-cost averaging to reduce timing risk. Instead of trying to predict market peaks and valleys, invest the same amount on the same schedule regardless of price. You’ll buy more shares when prices drop and fewer when they rise, averaging your cost over time. This strategy eliminates the paralysis of waiting for the “perfect” entry point that never comes.

Choose low-cost index funds that track broad market indices like the S&P 500 or total stock market. These funds offer instant diversification across hundreds of companies with expense ratios typically below 0.1%. Over decades, the difference between 0.05% and 1% fees compounds to tens of thousands of dollars. Vanguard, Fidelity, and Schwab all offer excellent low-cost options.

Rebalance your portfolio quarterly to maintain your targeted asset allocation. If you aim for 70% stocks and 30% bonds but market movements shift this to 75/25, sell some stocks and buy bonds to restore balance. This disciplined approach forces you to sell high and buy low automatically. Most brokerages offer automatic rebalancing features.

Avoid emotional reactions to market volatility by relying on your automated system. Markets will drop 10 to 20% regularly and 30 to 50% occasionally. Your automatic contributions will buy shares at discount prices during these periods, setting up larger gains when markets recover. History shows patient investors who stay the course outperform those who panic and sell.

Pro Tip: Increase your automatic investment amount by 1% every time you receive a raise. You won’t notice the difference in your paycheck, but your wealth will compound faster without requiring additional willpower.

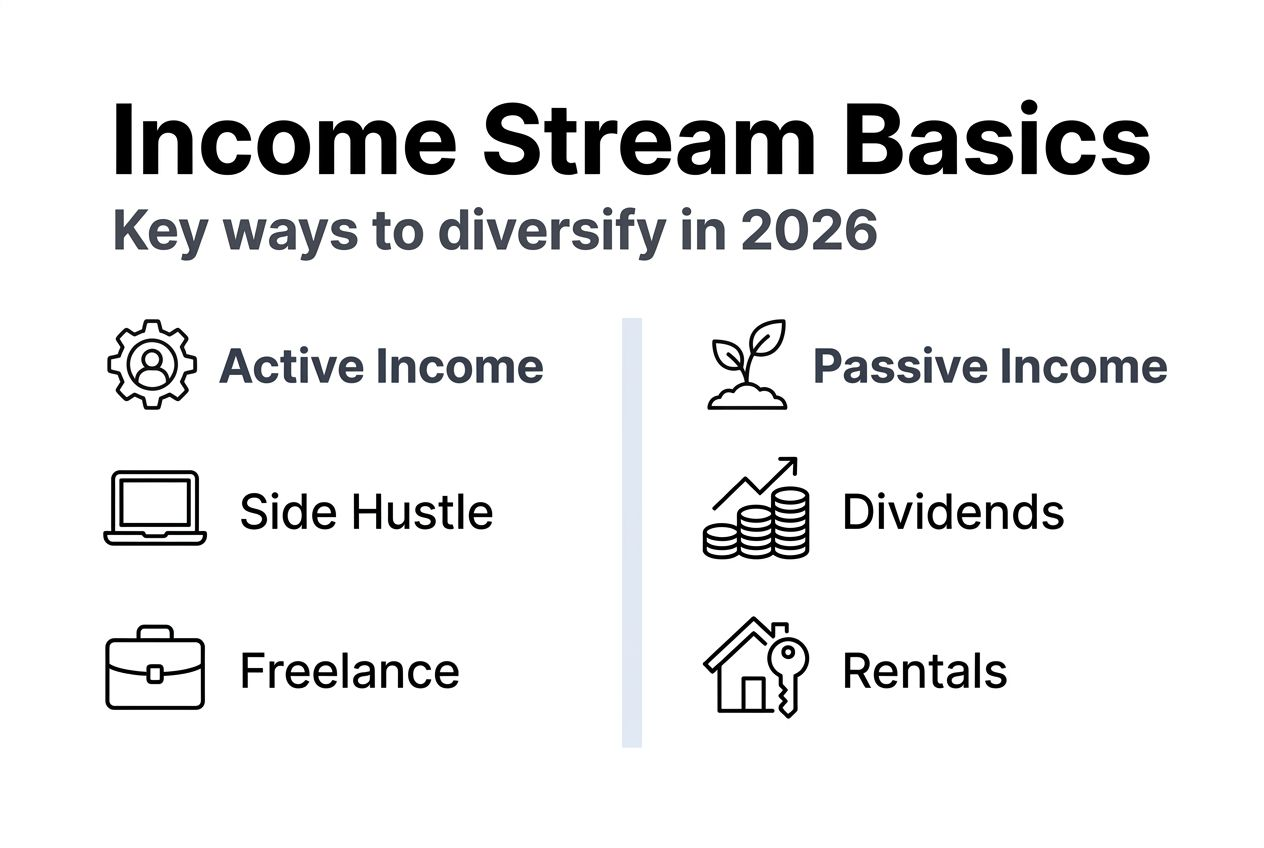

Diversifying income streams

Relying on a single income source creates vulnerability. Multiple streams provide security when one falters and accelerate progress when all flow simultaneously.

Creating multiple income streams including side businesses, dividend-paying stocks, and rental income enhances financial stability dramatically. Start by identifying skills or knowledge you can monetize beyond your primary job. Freelance consulting, online courses, writing, design work, and technical services all convert expertise into income.

Start side businesses that align with your skills and interests. The best side hustles solve real problems people will pay to fix. If you’re skilled at organization, offer decluttering services. If you understand marketing, help local businesses improve their online presence. Begin small, validate demand, then scale as time allows. Many successful entrepreneurs started with side projects that eventually replaced their primary income.

Invest in dividend-paying stocks and REITs for passive income. Quality dividend stocks from established companies provide quarterly cash payments regardless of market price movements. Real Estate Investment Trusts (REITs) offer exposure to property income without the hassles of direct ownership. Reinvest dividends during accumulation phases to compound growth faster. The best passive income ideas for smart investors explores strategies requiring minimal ongoing effort.

Monetize hobbies or digital products to create new income streams. If you enjoy photography, sell prints or stock photos. If you’re knowledgeable about a topic, write an ebook or create online courses. Digital products scale infinitely because creating one unit and one million units requires similar effort. Platforms like Etsy, Gumroad, and Teachable make this accessible to anyone.

Consider rental income opportunities to diversify cash flow. House hacking by renting extra bedrooms or basement apartments reduces your housing costs while building equity. Investment properties generate monthly income that typically increases over time. Even renting parking spaces, storage, or equipment creates passive streams. Start with what you have before buying additional properties.

Common mistakes and troubleshooting

Even solid plans fail when common traps go unrecognized. Knowing these pitfalls helps you spot and correct problems before they derail your progress entirely.

Failing to track expenses and categorize regularly leads to budget confusion. Without data, you’re guessing about spending patterns. Fix this by choosing one tracking method and committing to weekly reviews for 30 days until it becomes automatic. Apps make this nearly effortless by syncing transactions automatically.

Accumulating new high-interest debts while trying to pay off existing ones creates a devastating cycle. This happens when unexpected expenses hit and you lack an emergency fund. Build at least $1,000 in easily accessible savings before aggressively attacking debt. Then grow this to three to six months of expenses. Resources like how to manage debt provide frameworks for breaking this pattern.

Skipping automated savings and investments because you’ll “do it manually” rarely works. Life gets busy, and manual transfers become the first thing postponed. Set up automation immediately, even if you start with small amounts. You can always adjust upward, but starting creates momentum.

Setting unrealistic goals that demand extreme sacrifice leads to burnout and abandonment. If you currently save nothing, jumping to 30% savings creates unsustainable pressure. Begin with 5 or 10%, then increase gradually as your income grows or expenses decrease. Break large goals into smaller milestones that feel achievable within weeks or months rather than years.

Trying to time markets or reacting emotionally to volatility destroys returns. Studies consistently show active traders underperform passive investors who simply stay invested. When markets drop and fear peaks, your instinct screams “sell everything.” Successful investors do the opposite, continuing their regular contributions or even increasing them. Stick to your consistent strategy regardless of headlines.

Pro Tip: Create an “if-then” plan for common obstacles. Example: “If unexpected expenses arise, then I’ll use my emergency fund and pause extra debt payments temporarily.” Having predetermined responses prevents panic decisions.

Expected timelines and outcomes

Understanding realistic timeframes prevents discouragement and helps you measure progress accurately. Financial independence isn’t instant, but the compounding effects accelerate dramatically over time.

Saving 20% or more of income typically enables financial independence in 10 to 20 years, depending on your starting point and investment returns. If you save 20% and earn 7% annual returns, you’ll accumulate roughly 10 times your annual spending in 20 years. Increase savings to 30%, and the timeline drops to approximately 15 years. Push to 50%, and you could achieve independence in under a decade.

| Savings Rate | Years to FI | Key Factors |

|---|---|---|

| 10% | 30+ years | Standard retirement timeline |

| 20% | 20-25 years | Moderate acceleration |

| 30% | 15-20 years | Aggressive saving |

| 50% | 10-12 years | Extreme dedication |

| 70%+ | 5-8 years | Requires high income or minimal expenses |

Compound investing growth accelerates wealth over time in ways that feel slow initially but explosive later. A $10,000 investment growing at 8% annually becomes $21,589 in 10 years, $46,610 in 20 years, and $100,627 in 30 years. The final decade generates more growth than the first two decades combined. This mathematical reality rewards those who start early and stay consistent.

Emergency fund and debt elimination reduce unexpected timeline setbacks. Medical bills, car repairs, job loss, and other surprises derail plans when you lack reserves. A funded emergency account keeps you on track. Similarly, eliminating high-interest debt removes a major drag on wealth accumulation.

Tax advantages further improve retirement savings growth. Contributions to 401(k) and traditional IRA accounts reduce current taxable income, while Roth accounts offer tax-free growth and withdrawals. In 2026, you can contribute up to $23,000 to a 401(k) and $7,000 to an IRA annually. Maximizing these accounts accelerates progress significantly. Health Savings Accounts (HSAs) offer triple tax advantages when used for medical expenses.

Achieving milestones helps track and motivate progress. Celebrate your first $10,000 in investments, your first $1,000 in monthly passive income, or eliminating your first major debt. These markers prove the system works and fuel continued effort when motivation wanes.

Explore finblog’s resources to accelerate your journey

Building financial independence requires ongoing education and support. Finblog provides comprehensive guides, practical tools, and expert insights designed specifically for individuals pursuing financial freedom in 2026 and beyond.

Access expert articles covering everything from detailed budget creation techniques to sophisticated debt repayment strategies. Each guide breaks complex topics into actionable steps you can implement immediately. Whether you’re just starting or optimizing an existing plan, you’ll find resources matched to your current stage.

Stay updated with the latest strategies, tax law changes, and investment opportunities relevant to your journey. Financial rules and best practices evolve, and remaining informed helps you adapt and maintain progress.

What is the first step toward financial independence?

Begin by thoroughly understanding your current financial situation including income, expenses, debts, and assets. This baseline lets you make informed plans and set realistic goals. Without knowing where you stand, any plan becomes guesswork.

How much should I save monthly for financial independence?

A common benchmark is saving at least 20% of your income consistently. Higher savings rates shorten the time to financial independence significantly. If 20% feels unreachable now, start with 10% and increase as your income grows or expenses decrease.

What are the best investment types for beginners on this path?

Low-cost diversified index funds are ideal for beginners. They offer steady growth with reduced risk and require minimal ongoing management. Choose funds tracking broad market indices with expense ratios below 0.1% for optimal results.

How do I stay motivated throughout the process?

Set small, achievable milestones and align them with personal values to maintain momentum. Celebrate progress regularly and adjust goals to stay aligned with changing circumstances. Regularly reviewing wins reminds you why the journey matters and makes the long timeline feel manageable.

Recommended

- Achieve Financial Independence Retire Early: Step-by-Step Guide – Finblog

- Top Steps to Financial Freedom for Lasting Independence – Finblog

- Financial Freedom Roadmap: Achieve Independence Step-by-Step – Finblog

- Achieve Financial Freedom Goals with a Step-by-Step Guide – Finblog

- Dependent Visa UK: The Ultimate 2026 Guide to Requirements & Rules – METIN.LONDON