Figuring out money as a couple is about more than who pays the bills or who picks up the tab. Most couples admit that differences over finances are one of the biggest sources of stress, but studies show that couples who talk about money openly are 70 percent more likely to say they’re happy in their relationship. You might think the secret is just budgeting smarter, but the real win comes when you plan for the good times and the rough patches together, turning money into a source of teamwork not tension.

Table of Contents

- Setting Shared Financial Goals As A Couple

- Combining And Managing Finances Effectively

- Smart Strategies For Budgeting And Saving Together

- Planning For Investments, Retirement, And Insurance

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand financial compatibility | Discuss individual financial values and goals to align perspectives. |

| Set SMART financial goals | Create specific, measurable, attainable, relevant, and time-bound goals for effective planning. |

| Establish financial ground rules | Develop spending guidelines to foster trust and respect in financial matters. |

| Choose a financial integration strategy | Decide how to manage finances together, balancing independence and collaboration. |

| Regularly review investment and retirement plans | Collaborate on strategies to optimize retirement income and manage risks effectively. |

Setting Shared Financial Goals as a Couple

Successful financial planning for couples requires more than just good intentions. It demands intentional communication, mutual understanding, and a collaborative approach to creating a shared financial vision. By working together, partners can transform their individual financial perspectives into a unified strategy that supports both personal and collective aspirations.

Understanding Your Financial Compatibility

Financial compatibility goes beyond simply agreeing on spending habits. According to Utah State University Extension, couples should start by having an honest discussion about their individual financial values and priorities. This means diving deep into personal money beliefs, past experiences, and long-term financial dreams.

Key areas to explore include:

- Personal spending and saving habits

- Financial goals and timelines

- Attitudes toward debt and risk

- Individual financial backgrounds

These conversations might feel uncomfortable initially, but they are crucial for building a strong financial foundation. By understanding each other’s financial perspectives, couples can develop a more empathetic and collaborative approach to money management.

Creating SMART Financial Goals

Effective financial planning requires setting goals that are realistic and achievable. The University of Arkansas Cooperative Extension Service recommends using the SMART framework for goal setting:

- Specific: Clearly define what you want to achieve

- Measurable: Establish concrete criteria for tracking progress

- Attainable: Set goals that are challenging but realistic

- Relevant: Ensure goals align with your shared life vision

- Time-bound: Create specific timelines for goal achievement

For instance, instead of a vague goal like “save more money,” a SMART goal would be “save $15,000 for a home down payment within 24 months by setting aside $625 monthly.”

Establishing Financial Ground Rules

PBS News highlights the importance of setting clear spending boundaries. This means establishing guidelines for financial decision-making that respect both partners’ autonomy and shared objectives.

Consider creating rules such as:

- Consulting each other on purchases over a specific dollar amount

- Maintaining individual discretionary spending accounts

- Regular monthly financial check-ins

- Transparent reporting of all income and expenses

By developing these ground rules together, couples can prevent potential conflicts and create a sense of mutual trust and respect in their financial relationship. Remember, successful financial planning is not about controlling each other but about supporting shared dreams and individual growth.

Combining and Managing Finances Effectively

Transitioning from individual financial management to a collaborative approach requires strategic planning and mutual understanding. Couples must navigate complex decisions about merging accounts, establishing financial responsibilities, and creating systems that support their shared economic goals.

Deciding on a Financial Integration Strategy

Couples have multiple options for combining finances, and there is no one-size-fits-all approach. According to research from the National Institutes of Health, the most successful financial management strategies are those that prioritize transparency, communication, and mutual respect.

Common financial integration approaches include:

- Fully Merged Accounts: All income and expenses are shared

- Partial Merge: Joint account for shared expenses with individual accounts maintained

- Proportional Contribution: Each partner contributes a percentage of income to shared expenses

- Separate Accounts: Maintaining completely independent financial systems

The right approach depends on individual preferences, income levels, financial history, and shared goals. Open discussions about comfort levels, financial independence, and long-term objectives are crucial in determining the most suitable strategy.

Here is a summary table comparing different financial integration approaches for couples. This table can help you evaluate which strategy might suit your partnership best based on the methods described above.

| Integration Approach | Description | Pros | Potential Drawbacks |

|---|---|---|---|

| Fully Merged Accounts | All income and expenses are shared | Maximum transparency, unified finances | Less individual independence |

| Partial Merge | Joint account for shared expenses, individual accounts maintained | Balance of shared and independent funds | Complexity in account management |

| Proportional Contribution | Each contributes a % of income to shared expenses | Adjusts for income differences | Requires ongoing calculation |

| Separate Accounts | Completely independent financial systems | Full autonomy | Limited financial coordination |

Creating a Collaborative Financial Management System

Effective financial management goes beyond simply merging accounts. Successful couples develop robust systems for tracking expenses, making financial decisions, and maintaining accountability.

Key components of a strong financial management system include:

- Regular monthly financial review meetings

- Shared digital spreadsheets or budgeting apps

- Clear protocols for large purchases

- Transparent tracking of income and expenses

- Established emergency fund contributions

Technology can play a significant role in simplifying financial collaboration. Many couples now use digital tools that allow real-time expense tracking, automated savings, and joint budget planning. These platforms can help reduce friction and provide a clear, shared view of financial health.

Addressing Financial Challenges and Conflicts

Financial disagreements are inevitable in any partnership. The key is developing healthy communication strategies and conflict resolution mechanisms. Approach financial discussions with empathy, active listening, and a problem-solving mindset.

Strategies for managing financial conflicts include:

- Setting regular check-in times for financial discussions

- Using “I” statements to express concerns

- Focusing on shared goals rather than individual grievances

- Being willing to compromise and adapt

- Seeking professional financial counseling if needed

Remember that financial management is an ongoing process. As life circumstances change, your financial strategy should evolve. Flexibility, mutual respect, and a commitment to shared goals are the foundations of effective financial collaboration.

Smart Strategies for Budgeting and Saving Together

Budgeting as a couple transforms financial management from an individual challenge to a collaborative journey. Successful couples understand that effective budgeting is not about restricting spending but about aligning financial resources with shared life goals and dreams.

Developing a Comprehensive Budgeting Framework

Utah State University Extension recommends starting with a comprehensive conversation about financial goals and expectations. The key is creating a budget that feels inclusive and supportive of both partners’ needs.

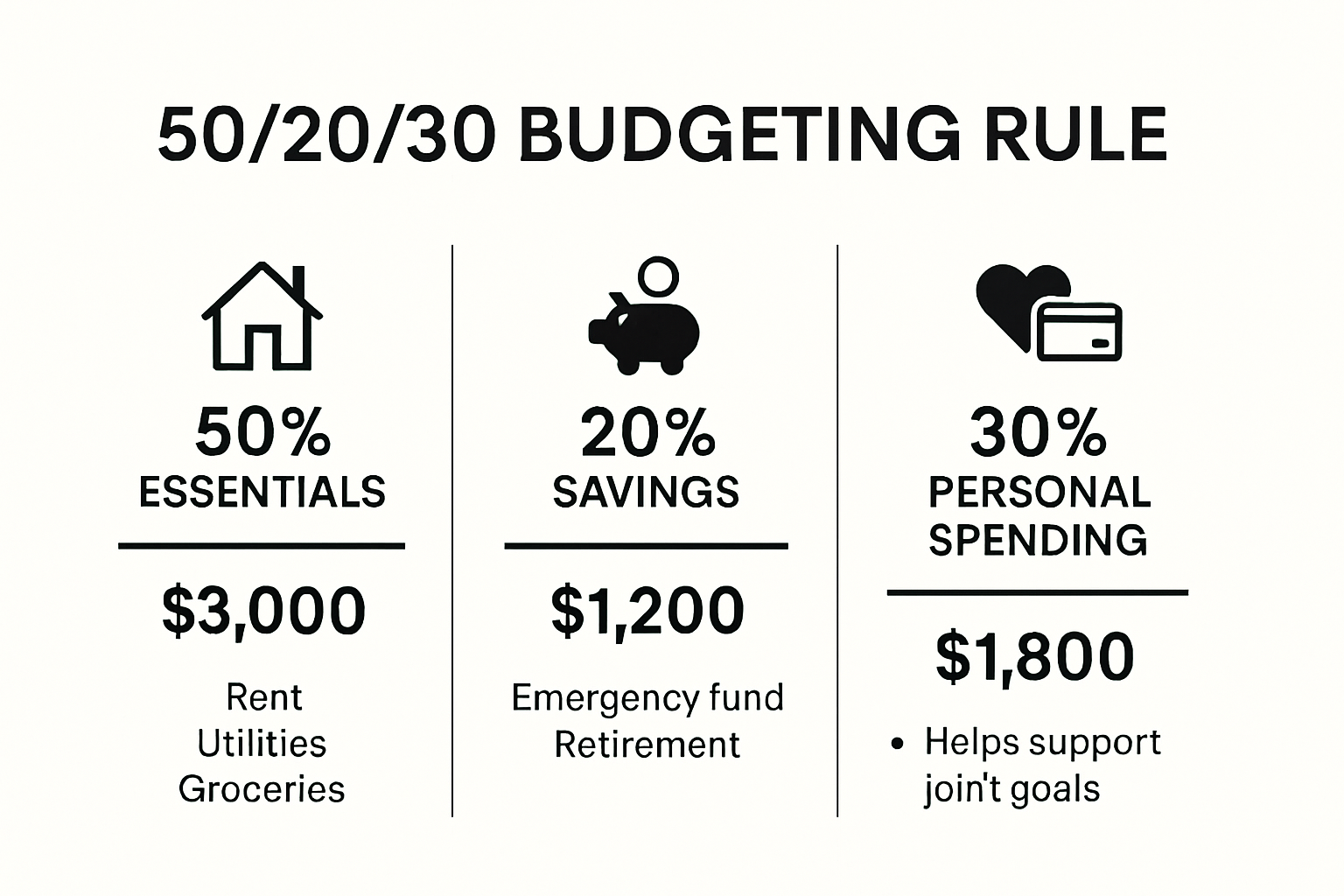

According to MIT’s Student Financial Services, the 50/20/30 budgeting strategy offers an excellent starting point for couples:

- 50% for Fixed Expenses: Essential living costs like rent, utilities, groceries

- 20% for Financial Goals: Savings, debt repayment, investments

- 30% for Flexible Spending: Entertainment, dining out, personal purchases

This framework provides a balanced approach to money management, ensuring that critical financial objectives are met while maintaining flexibility for personal enjoyment.

Technology and Tools for Collaborative Budgeting

Modern couples have access to numerous digital tools that simplify financial tracking and collaboration. Budgeting apps and shared financial platforms enable real-time expense monitoring, joint goal setting, and transparent financial communication.

Recommended budgeting features to look for:

- Expense Categorization: Automatic sorting of spending into predefined categories

- Real-time Synchronization: Instant updates across both partners’ devices

- Goal Tracking: Visual representations of savings progress

- Alerts and Notifications: Warnings about approaching budget limits

By leveraging technology, couples can transform budgeting from a potential source of stress into an engaging, collaborative process.

The following table summarizes essential components and features to look for when choosing collaborative budgeting tools and strategies. It highlights key functions to support effective financial management as a couple.

| Feature | Description | Benefits |

|---|---|---|

| Expense Categorization | Automatically sorts spending into categories | Easy tracking of spending |

| Real-time Synchronization | Updates instantly across both partners’ devices | Ensures transparency |

| Goal Tracking | Visualizes progress toward financial goals | Motivates saving and budgeting |

| Alerts and Notifications | Sends warnings when nearing limits | Prevents overspending |

| Shared Access | Both partners can view and manage finances | Promotes collaboration |

Building a Robust Savings Strategy

Successful financial planning goes beyond monthly budgeting. Couples should develop a comprehensive savings strategy that addresses short-term needs and long-term aspirations.

Key savings priorities include:

- Emergency fund covering 3-6 months of living expenses

- Retirement account contributions

- Specific goal-based savings (home purchase, travel, education)

- Mutual investment strategies

Consider creating separate savings accounts for different objectives. This approach allows for targeted saving while maintaining overall financial flexibility. Automate contributions whenever possible to ensure consistent progress toward financial goals.

Remember that budgeting and saving are skills that improve with practice. Regular communication, mutual respect, and a willingness to adapt will transform financial planning from a challenging task into a rewarding shared experience. Celebrate milestones together, learn from setbacks, and view your financial journey as a collaborative adventure toward mutual prosperity.

Planning for Investments, Retirement, and Insurance

Investment and retirement planning as a couple requires strategic coordination, mutual understanding, and a comprehensive approach to securing your financial future. By aligning your investment strategies and protecting your shared financial interests, you can build a robust foundation for long-term financial stability.

Coordinating Investment Strategies

TIAA emphasizes the critical importance of open communication and collaborative investment planning. Couples should view their investment portfolio as a unified strategy, considering both partners’ risk tolerances, financial goals, and individual retirement accounts.

Key investment coordination considerations:

- Balanced asset allocation across different investment vehicles

- Complementary investment approaches that minimize overall risk

- Regular portfolio reviews and rebalancing

- Diversification across different asset classes and investment types

- Understanding each partner’s individual retirement accounts and employer-sponsored plans

By developing a holistic investment approach, couples can maximize potential returns while maintaining a balanced risk profile that supports their shared financial objectives.

Retirement Planning and Social Security Strategies

According to the Consumer Financial Protection Bureau, effective retirement planning involves more than just saving money. Couples must strategically coordinate their retirement income sources, including Social Security benefits, pension plans, and individual retirement accounts.

Consider these critical retirement planning elements:

- Timing Social Security benefit claims for optimal lifetime income

- Understanding spousal benefit options

- Coordinating retirement account contributions

- Planning for potential healthcare expenses

- Creating a flexible withdrawal strategy

AARP warns that misaligned retirement goals can significantly impact long-term financial security. Regular discussions about retirement expectations, potential lifestyle changes, and financial capabilities are essential.

Comprehensive Insurance and Risk Management

Protecting your financial future requires a robust insurance strategy that addresses potential risks and provides financial security for both partners. This goes beyond basic health and life insurance to include comprehensive risk management.

Essential insurance considerations for couples include:

- Life insurance with appropriate coverage for both partners

- Disability insurance to protect income

- Long-term care insurance

- Umbrella liability protection

- Healthcare coverage that meets both partners’ needs

Regularly review and update insurance policies to ensure they reflect your current life stage, financial situation, and family responsibilities. As your life evolves, so too should your insurance protection.

Successful financial planning for investments, retirement, and insurance is an ongoing process. It requires consistent communication, mutual respect, and a willingness to adapt to changing circumstances. By working together and maintaining a proactive approach, couples can build a secure and prosperous financial future.

Frequently Asked Questions

What are the key components of financial planning for couples?

Successful financial planning for couples includes understanding financial compatibility, setting SMART financial goals, establishing financial ground rules, combining and managing finances effectively, and planning for investments, retirement, and insurance.

How can we determine our financial compatibility as a couple?

To determine financial compatibility, couples should discuss their individual financial values, attitudes toward spending and saving, financial goals, and past financial experiences. Open and honest communication is essential to understand each other’s perspectives.

What strategies can couples use to budget effectively together?

Couples can budget effectively by developing a comprehensive budgeting framework, using technology and tools for collaborative budgeting, and regularly reviewing their budget together. The 50/20/30 budgeting strategy is a popular method to ensure a balanced approach to expenses, savings, and discretionary spending.

How can we prepare for retirement as a couple?

Preparing for retirement involves coordinating investment strategies, planning for Social Security benefits, and developing a flexible withdrawal strategy. Regular discussions about retirement goals, expected expenses, and managing healthcare costs are crucial to ensure financial security in retirement.

Ready to Build Your Financial Future as a Team?

Trying to find real financial harmony can feel frustrating when you and your partner have different money histories or goals. Maybe you are sitting together, reviewing budgets, or even clashing over how to combine your accounts. You are not alone. The article explained how small misunderstandings about things like financial ground rules or inconsistent budgeting often drive tension and anxiety in relationships. If you want to replace those struggles with trust and shared progress, it helps to have expert tools and knowledgeable support.

Take your next step together by exploring finblog.com. Start turning shared goals into smart plans as a couple. You will find practical resources, simple checklists, and custom advice designed for partners who want more than just a budget, but a real financial partnership. Do not wait. These moments matter for your future security and happiness. Visit our site now to access personalized guidance and unlock the confidence your relationship deserves.