Did you know that 37% of Americans cannot cover a $400 emergency expense with cash? This striking figure reveals how vulnerable most households remain to everyday financial shocks. Building an emergency fund, a dedicated pool of easily accessible savings for unexpected expenses, isn’t just smart planning. It’s your first line of defense against debt spirals and long-term financial damage. This guide explains why emergency funds matter, how to calculate your personal target, and practical strategies to build lasting financial security.

Table of Contents

- Why An Emergency Fund Is Essential For Financial Security

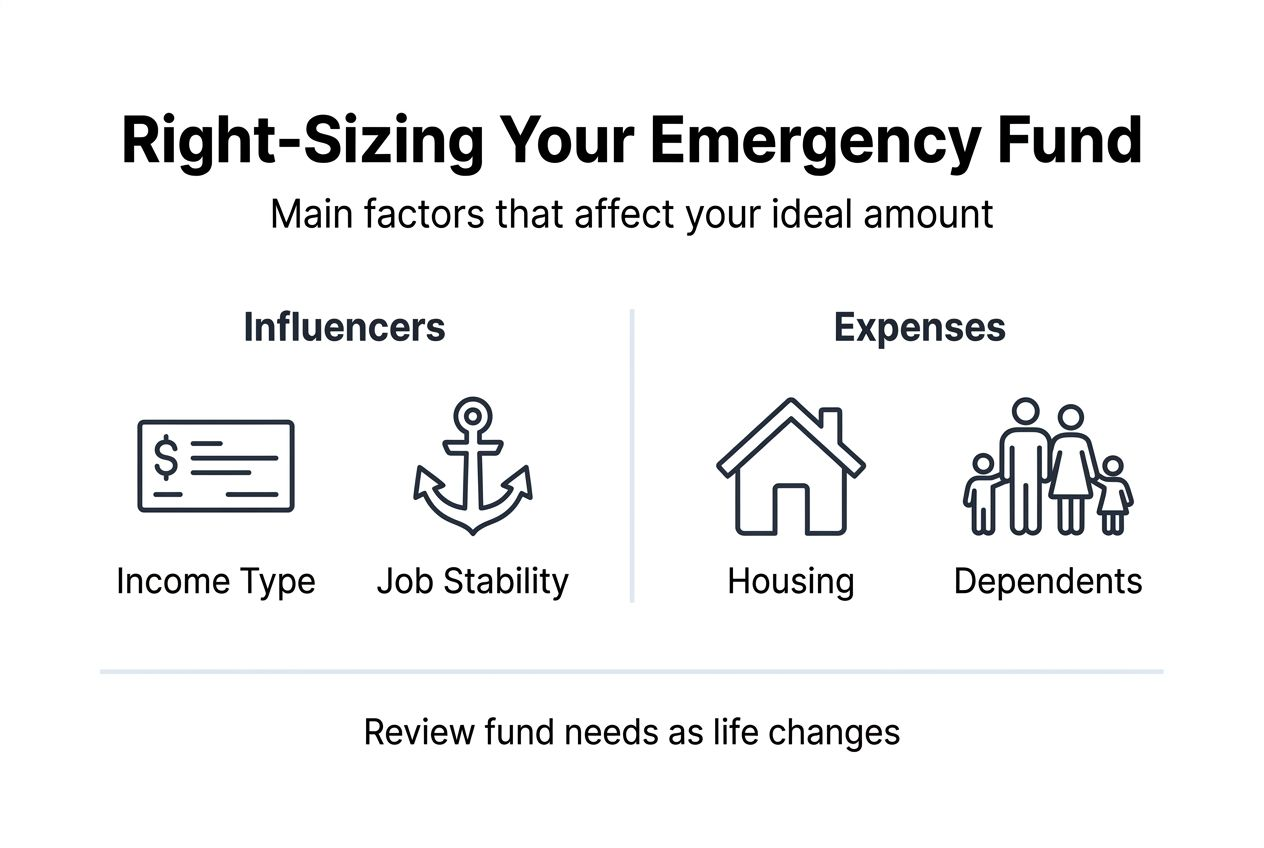

- How To Determine The Right Size Of Your Emergency Fund

- Practical Strategies To Build And Maintain Your Emergency Fund

- Adjusting Your Emergency Fund As Your Life Changes

- Enhance Your Financial Security With Expert Guidance

- Frequently Asked Questions

Key takeaways

| Point | Details |

|---|---|

| Standard target | Emergency funds should cover 3-6 months of essential expenses like rent, utilities, groceries, and insurance. |

| Personal factors | Self-employed individuals, single-income households, and those with dependents typically need larger reserves. |

| Primary benefit | An emergency fund prevents reliance on high-interest credit cards and protects long-term retirement savings from early withdrawals. |

| Building approach | Start small with automated contributions and increase savings as income grows or life circumstances change. |

Why an emergency fund is essential for financial security

Financial shocks from medical emergencies, car repairs, or sudden job losses hit hardest when you lack savings. Without a cushion, a single unexpected expense can trigger a cascade of problems: missed bill payments, mounting credit card debt, and damaged credit scores that take years to repair.

Emergency funds reduce dependence on costly credit and protect the retirement accounts you’ve worked hard to build. When crisis strikes, tapping a credit card at 24% APR or withdrawing from a 401(k) with penalties creates financial wounds far deeper than the original emergency. Your emergency fund acts as a buffer, absorbing shocks without derailing your broader financial plan.

Low-wage workers face disproportionate vulnerability because they typically lack employer benefits like paid sick leave or short-term disability insurance. A week without pay due to illness can mean choosing between rent and groceries. This reality makes emergency savings not a luxury but a survival tool for millions of American households.

“An emergency fund transforms financial anxiety into confidence. You sleep better knowing that a flat tire or broken furnace won’t spiral into a financial crisis.”

Beyond dollars and cents, emergency funds deliver psychological benefits that ripple through your entire life. The peace of mind from knowing you can handle unexpected expenses reduces stress, improves workplace focus, and strengthens relationships strained by financial worry. This financial security provides the foundation for long-term stability and opens doors to opportunities you might otherwise miss due to fear of financial risk.

How to determine the right size of your emergency fund

Calculating your target starts with honest assessment of essential monthly expenses. List only necessities: housing costs, utilities, minimum debt payments, groceries, insurance premiums, transportation, and healthcare. Exclude discretionary spending like dining out, subscriptions, or entertainment that you’d cut during a genuine emergency.

Most people need 3-6 months of essential expenses in their emergency fund, but this range varies significantly based on personal circumstances. Someone with stable employment, dual household income, and strong job prospects might target three months. Conversely, households with variable income, single earners, or industry-specific employment risks should aim for six months or more.

Key factors that increase your target:

- Self-employed or freelance income with irregular cash flow

- Single-income households lacking backup earning capacity

- Specialized careers with limited local job opportunities

- Health conditions requiring ongoing medical care

- Aging home or vehicle prone to major repairs

- Dependents relying on your financial support

Self-employed individuals face unique challenges because income fluctuates and they lack employer-provided safety nets. The CFPB recommends saving 9-12 months of expenses if you work for yourself, accounting for slower job replacement and gaps between contracts.

| Life Situation | Recommended Reserve | Reasoning |

|---|---|---|

| Dual income, stable jobs | 3-4 months | Lower risk with two incomes and employment stability |

| Single income household | 5-6 months | Higher vulnerability if sole earner loses job |

| Self-employed/Freelance | 9-12 months | Income variability and lack of unemployment benefits |

| Pre-retirement (55+) | 12-18 months | Age discrimination and longer job search timelines |

Homeownership adds another layer because property maintenance emergencies arise without warning. Renters typically need smaller funds since landlords handle major repairs, but homeowners must prepare for roof leaks, HVAC failures, and foundation issues that insurance won’t fully cover. If you own property, add 10-20% to your baseline target to account for these ownership-specific risks.

Practical strategies to build and maintain your emergency fund

Pro Tip: Open a separate high-yield savings account exclusively for emergency funds. Physical and mental separation from everyday checking prevents accidental spending while earning meaningful interest on your safety net.

Building significant savings feels overwhelming when starting from zero, but consistent small contributions create lasting habits that compound over time. Focus on sustainability rather than aggressive targets that become unsustainable and lead to discouragement.

Follow this proven step-by-step approach:

- Start with a micro-goal of $500 to handle minor emergencies like urgent care visits or minor car repairs.

- Automate weekly or biweekly transfers immediately after payday, treating savings like a non-negotiable bill.

- Direct windfalls like tax refunds, bonuses, or gift money straight into your emergency fund.

- Review spending monthly to identify small cuts that won’t impact quality of life but free up $25-50 for savings.

- Increase contribution amounts by 1-2% whenever you receive raises or pay off other debts.

- Track progress visually using apps or charts that celebrate milestones and maintain motivation.

The hardest part of maintaining an emergency fund is defining what actually constitutes an emergency. Create clear criteria before crisis strikes: job loss, major medical expenses, essential home or car repairs, or unexpected travel for family emergencies qualify. Annual holiday shopping, vacation plans, or routine purchases never do, regardless of how urgent they feel in the moment.

When legitimate emergencies deplete your fund, pause other financial goals temporarily to rebuild your emergency reserves before resuming investing or accelerated debt payoff. Your emergency fund is financial foundation, not a luxury to address after everything else. Treat replenishment with the same urgency you’d apply to fixing a leaking roof.

Celebrate milestones strategically to maintain momentum without undermining progress. Reaching $1,000, then $2,500, then full month coverage deserves recognition. Reward yourself with small, budgeted treats rather than large expenses that defeat the purpose of your discipline. These psychological wins reinforce positive money behaviors and help build wealth through consistent habits.

Adjusting your emergency fund as your life changes

Your emergency fund isn’t a set-it-and-forget-it element of financial planning. Life transitions demand periodic reassessment to ensure your safety net matches current realities. Marriage, divorce, childbirth, career changes, relocation, and aging all shift both your monthly expenses and your risk profile.

Trigger points for increasing your emergency fund:

- Adding dependents through birth, adoption, or supporting aging parents

- Purchasing a home and taking on maintenance responsibilities

- Starting a business or transitioning to self-employment

- Developing chronic health conditions with ongoing costs

- Approaching retirement and losing employment-based income

Retirement represents the most critical adjustment period. As you approach retirement age, increase reserves to 12-24 months because you no longer have decades to recover from market downturns or unexpected healthcare costs. Older job seekers face longer unemployment periods, and tapping retirement accounts early triggers taxes and penalties that permanently reduce your nest egg.

| Life Stage | Monthly Expense Coverage | Key Considerations |

|---|---|---|

| Young professional (25-35) | 3-4 months | Building career, lower obligations |

| Established career (35-50) | 4-6 months | Peak earning, children, mortgage |

| Pre-retirement (50-65) | 6-12 months | Age discrimination risk, protecting retirement assets |

| Retirement (65+) | 12-24 months | Fixed income, healthcare costs, market volatility |

Downsizing or simplifying life also permits reducing your target if done thoughtfully. Paying off your mortgage, relocating to lower cost-of-living areas, or transitioning from ownership to rental reduces monthly obligations and the corresponding emergency fund needed to cover them. Reassess annually or whenever major life changes occur, adjusting both up and down based on current circumstances rather than outdated assumptions.

Schedule an annual emergency fund review each January alongside other financial planning activities. Calculate current essential expenses, evaluate employment stability and household income sources, and adjust your target accordingly. This disciplined approach to emergency fund planning ensures your safety net grows with you rather than becoming inadequate through neglect.

Enhance your financial security with expert guidance

Building financial security extends far beyond emergency funds alone. Finblog offers comprehensive resources that guide you through every aspect of personal finance, from initial emergency savings through long-term wealth building and retirement planning. Our evidence-based articles translate complex financial concepts into actionable strategies you can implement immediately.

Explore our detailed emergency fund planning guide for calculators and worksheets that help you determine your precise target and create a personalized savings timeline. We also provide extensive coverage of best saving practices for investors that complement your emergency reserves with strategies for growing wealth systematically.

Whether you’re starting your first emergency fund or optimizing an established financial plan, Finblog delivers practical tools and expert insights that transform financial anxiety into confident action. Visit us today to access free resources designed specifically for working professionals and individual investors committed to building lasting financial security.

Frequently asked questions

What qualifies as a legitimate emergency?

True emergencies threaten your health, safety, housing, or ability to earn income. Medical crises, essential home repairs like furnace failures, car breakdowns preventing work commutes, and unexpected job loss all qualify. Planned expenses, wants versus needs, and predictable costs like annual insurance premiums never constitute emergencies regardless of timing.

How much should I save in my emergency fund?

Generally 3-6 months of essential expenses covers most situations, calculated from necessities like housing, utilities, food, insurance, and minimum debt payments. Self-employed individuals need 9-12 months due to income variability, while retirees should target 12-24 months. Your specific target depends on job stability, household income sources, dependents, and health status.

How can I start building an emergency fund if I have limited income?

Start with whatever amount you can sustain consistently, even $10 or $25 weekly. Automate transfers immediately after payday to remove decision fatigue. Focus on building the habit rather than the amount initially. As you identify small spending cuts or receive raises, gradually increase contributions. Progress matters more than perfection, and small consistent deposits compound significantly over time.

Can I use my emergency fund for non-emergency expenses?

No. Using emergency savings for discretionary purchases or planned expenses defeats the fund’s purpose and leaves you vulnerable when actual crises occur. If you frequently face “emergencies” that aren’t true threats, your budget likely needs adjustment to account for irregular but predictable expenses through separate sinking funds rather than emergency reserves.

Should I invest my emergency fund for higher returns?

Never invest emergency funds in stocks, bonds, or other volatile assets. Liquidity, meaning immediate access to cash without losses, matters more than returns for emergency savings. Use high-yield savings accounts or money market accounts that provide FDIC insurance, instant access, and modest interest without market risk. Investment accounts belong in separate long-term wealth building strategies, not emergency reserves.