TL;DR:

- Improving your credit score focuses primarily on on-time payments and maintaining low credit utilization levels. Regularly dispute errors on your credit reports to prevent inaccurate negative items from lowering your score. Consistent responsible credit behavior over six to twelve months results in meaningful and lasting score improvements.

Your credit score is a three-digit number that determines whether lenders approve your loan, what interest rate you pay on a mortgage, and which credit cards you qualify for. Knowing how to improve your credit score is one of the highest-return financial skills you can develop. The FICO scoring model, used by most U.S. lenders, weighs five factors: payment history, credit utilization, length of credit history, credit mix, and new inquiries. Tools like Experian Boost and AnnualCreditReport.com give you immediate visibility into where you stand. This guide covers the credit score improvement strategies that move the needle fastest, in the right order.

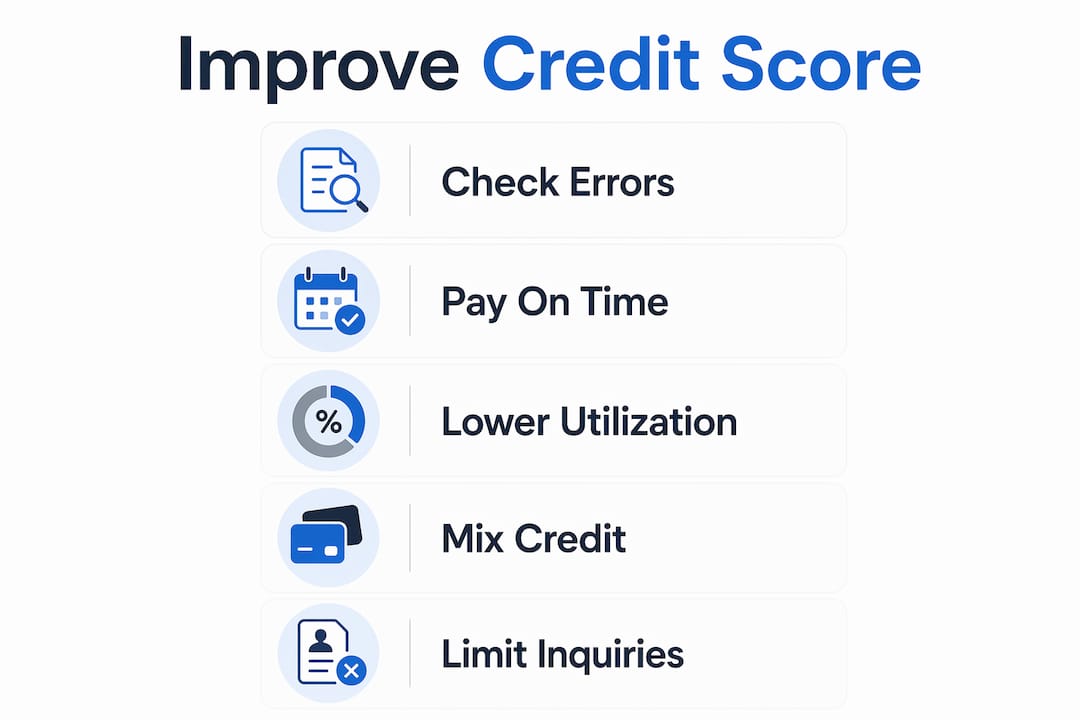

How to improve your credit score: the most effective methods

The fastest credit score gains come from targeting the two factors that carry the most weight: payment history and credit utilization. Together, they account for roughly 65% of your FICO score. Every other tactic is secondary.

On-time payments are non-negotiable. Payment history accounts for 35% of your FICO score, making it the single largest scoring component. One missed payment can drop a good score by 60 to 110 points, and that mark stays visible to lenders for seven years. Set up autopay for at least the minimum due on every account so a forgotten due date never becomes a delinquency.

Keep balances low relative to your limits. Keeping utilization under 30% of your available credit is the standard recommendation from financial regulators in the U.S. and Canada. If your total credit limit is $10,000, that means carrying no more than $3,000 across all cards. Dropping from 60% utilization to 20% can produce a meaningful score jump within a single billing cycle.

Dispute errors on your credit reports. Inaccurate accounts, wrong balances, or payments incorrectly marked late can suppress your score for years. Disputing these errors is free and legally required to be investigated by the bureaus. More on the exact process in a later section.

Maintain a healthy credit mix. A mix of credit cards, installment loans, and other credit types signals stronger credit management to scoring models. You do not need to open new accounts just to diversify, but if you only have credit cards, a small personal loan or a credit-builder loan can add dimension to your profile.

Limit new credit applications. Too many recent inquiries signal financial stress to lenders. Each hard inquiry can shave a few points off your score. If you are shopping for a mortgage or auto loan, bundle all applications within a 14 to 45-day window so scoring models treat them as a single inquiry.

Pro Tip: Pay your credit card balance before the statement closing date, not just before the due date. Bureaus typically receive your reported balance at statement close, so paying early means a lower balance gets reported, which directly lowers your utilization ratio that month.

Most people see measurable improvement within one to three billing cycles when they address utilization and payment consistency simultaneously. Negative items like late payments take longer to fade, but their impact diminishes over time even before they drop off your report.

How does credit utilization affect your score?

Credit utilization is the ratio of your current revolving balances to your total revolving credit limits. It accounts for approximately 30% of your FICO score, making it the second most influential factor. Unlike payment history, utilization has no memory. Pay down a balance today and your score can reflect that improvement within weeks.

Here is a practical breakdown of utilization ranges and their general scoring impact:

| Utilization range | Scoring impact |

|---|---|

| 0% to 10% | Optimal. Associated with the highest scores. |

| 11% to 29% | Good. Minimal negative effect on most scoring models. |

| 30% to 49% | Moderate drag. Score improvement possible by reducing balances. |

| 50% and above | Significant negative impact. Prioritize paying down balances immediately. |

Three strategies lower your utilization quickly:

- Pay your full balance before the statement closing date. Paying before statement close means the lower balance is what gets reported to the bureaus, not the higher mid-cycle balance. This is the fastest legal way to reduce reported utilization.

- Request a credit limit increase on existing cards. If your income has grown and your payment history is solid, many issuers will approve a limit increase with a soft pull. A higher limit on the same balance immediately lowers your ratio.

- Spread balances across multiple cards rather than maxing one. A single card at 80% utilization hurts more than four cards each at 20%, even if the total dollar amount is identical. Scoring models penalize high utilization on individual accounts, not just the aggregate.

For a deeper look at how to calculate and manage your ratio, Finblog’s credit utilization ratio guide covers the math and card-by-card strategy in detail.

What steps should you take to fix credit report errors?

One in five Americans has an error on at least one credit report, according to Federal Trade Commission research. Those errors can cost you loan approvals or push you into higher interest rate tiers. The fix is straightforward, but it requires documentation and persistence.

Follow these steps to identify and correct inaccuracies:

- Pull your free reports from all three bureaus. Visit AnnualCreditReport.com to download your Equifax, Experian, and TransUnion reports at no cost. Review each one separately because errors often appear on only one bureau’s file.

- Flag specific errors. Common problems include accounts that are not yours (often from identity theft or mixed files), payments marked late that were actually on time, incorrect balances or credit limits, and accounts that should have been removed after seven years.

- Gather documentation before you dispute. Bank statements, payment confirmations, and account correspondence are your evidence. Disputes work best when you match exact trade line details and include all supporting documentation.

- Submit a separate dispute to each bureau that shows the error. File online through Equifax’s, Experian’s, or TransUnion’s dispute portals, or send a certified letter with copies of your documentation. Credit bureaus must investigate and correct inaccurate information for free, typically within 30 days.

- Follow up and document everything. Keep records of every submission, confirmation number, and response. If a bureau does not correct a legitimate error, you can escalate to the Consumer Financial Protection Bureau.

Pro Tip: Never send original documents to a bureau. Send certified copies and keep the originals. If you mail a dispute, use certified mail with return receipt so you have proof of delivery.

The urgency here is real. Negative accurate information stays on your report for up to 7 years. An error that goes unchallenged can suppress your score for the entire duration. Correcting even one significant error can produce a score jump of 20 to 100 points, depending on the severity of the inaccuracy.

Why payment history and consistent credit behavior matter most

Payment history is the single biggest factor in your credit score, and it is also the most unforgiving. A single 30-day late payment can drag down an otherwise excellent score, and the damage compounds with each additional missed payment. The good news is that consistent on-time behavior going forward steadily reduces the impact of past mistakes.

Here is what consistent credit behavior looks like in practice:

- Set up autopay for every account. Even if you pay the full balance manually each month, autopay for the minimum due acts as a safety net. It prevents a missed payment from turning into a delinquency if you travel, get sick, or simply forget.

- Get current immediately after a missed payment. Staying current after a missed payment is the fastest way to begin score recovery. Lenders report your status monthly, so one month of current status starts rebuilding your history right away.

- Avoid opening multiple new accounts in a short period. Each new account lowers the average age of your credit history and adds a hard inquiry. Both factors pull your score down temporarily. Open new credit only when you have a clear purpose.

- Monitor your accounts weekly, not monthly. Fraudulent charges or billing errors can trigger missed payments you do not know about. Apps like Credit Karma or the monitoring tools built into Experian and Discover give you real-time alerts.

The timeline for payment history improvements is longer than for utilization changes. Reducing utilization can show results in one billing cycle. Rebuilding a payment history pattern takes six to twelve months of consistent behavior to produce meaningful score gains. The two-track approach of staying current while also lowering utilization addresses different scoring components on different timelines, which is why both matter simultaneously.

Key takeaways

Improving your credit score requires consistent on-time payments, low credit utilization, and accurate credit report data working together over time.

| Point | Details |

|---|---|

| Payment history is foundational | At 35% of your FICO score, one missed payment can drop a good score by over 60 points. |

| Keep utilization below 30% | Paying balances before statement close lowers what bureaus see and speeds up score gains. |

| Dispute errors immediately | Inaccurate negative items can stay on your report for 7 years if left unchallenged. |

| Limit new credit applications | Bundle mortgage or auto inquiries within 45 days so models treat them as one inquiry. |

| Consistency beats quick fixes | Six to twelve months of on-time payments produces lasting improvement no single tactic can match. |

What I have learned after years of watching people fix their credit

The biggest misconception I see is that credit repair is a mystery that requires a paid service or a loophole. It does not. No secret formula exists. The path is consistent payment behavior and balanced credit use, repeated month after month. Most people who hire credit repair companies are paying for things they could do themselves for free in an afternoon.

What actually trips people up is impatience. They pay down a card, check their score two days later, see no change, and conclude the strategy is not working. Credit bureaus update on their own schedule, tied to your statement dates. You need to give changes at least one full billing cycle before drawing conclusions.

The second trap is chasing score points through tactics that backfire. Closing old credit cards to “simplify” your finances reduces your total available credit and raises your utilization ratio instantly. Applying for a new card to get a higher limit adds a hard inquiry and lowers your average account age. Both moves can drop your score in the short term even when the intention is to improve it.

My honest recommendation: use a free tool like Credit Karma or Experian’s free monitoring to track your score weekly, set every account to autopay, and check your reports from all three bureaus at least twice a year. If you have debt spread across multiple cards, Finblog’s guide on credit card debt strategies lays out a clear repayment sequence that also protects your utilization ratio while you pay down balances.

Patience and documentation are the real tools. Everything else is noise.

— Povilas

Take the next step with Finblog’s financial guides

Finblog publishes regularly updated guides on every major credit and debt topic, written for people who want real answers without the jargon. If you are working through a credit recovery plan, the debt repayment strategies guide walks through structured payoff methods that protect your score while reducing what you owe. For professionals managing credit alongside career and investment goals, the credit score improvement tips for professionals resource covers advanced tactics suited to higher-income credit profiles. Visit Finblog to explore the full library of guides and get the financial clarity you need to make your next move with confidence.

FAQ

How long does it take to improve your credit score?

Utilization changes can show results within one billing cycle. Rebuilding payment history typically takes six to twelve months of consistent on-time payments to produce meaningful score gains.

What is the fastest way to raise your credit score?

Paying down credit card balances before your statement closing date lowers your reported utilization immediately, which is the fastest single action most people can take to see a score increase.

Does checking your own credit score lower it?

No. Checking your own score is a soft inquiry and has no effect on your credit score. Only hard inquiries from lenders when you apply for credit can temporarily lower your score.

How many points can disputing a credit report error add?

The impact depends on the severity of the error. Removing a falsely reported late payment or a fraudulent account can add anywhere from 20 to 100 points, depending on how much that item was dragging down your score.

What credit utilization ratio should you aim for?

Aim for below 10% for the highest scoring benefit, and stay under 30% at a minimum. Utilization above 30% begins to have a measurable negative effect on most FICO-based scoring models.