Did you know that your credit utilization ratio can make up as much as 30% of your FICO score? This single number gives lenders a quick look at how you handle borrowed money and plays a huge role in what financial opportunities you can access. Understanding this ratio and learning how it works can help you take control of your credit and set yourself up for better loan terms, higher scores, and long-term financial security.

Key Takeaways

| Point | Details |

|---|---|

| Credit Utilization Importance | Your credit utilization ratio affects approximately 30% of your FICO score, so it’s crucial to manage it effectively. Keeping this ratio below 30-40% is recommended for optimal credit health. |

| Calculation Method | Calculate your credit utilization by dividing your total credit card balances by your total credit limits and converting to a percentage. Regularly monitoring this ratio can help maintain a healthy score. |

| Common Pitfalls | Avoid maxing out credit cards and closing old accounts, as both actions can negatively impact your utilization ratio and credit score. Maintain a balance and keep old accounts open to strengthen your credit profile. |

| Improvement Strategies | Use several strategies to improve your credit utilization, such as making multiple payments each month, requesting credit limit increases, and spreading expenses across multiple cards to lower the ratio effectively. |

Table of Contents

- Defining Credit Utilization Ratio And Its Role

- Calculation Methods And Real-World Examples

- How Credit Utilization Affects Credit Scores

- Common Misconceptions And Mistakes To Avoid

- Effective Strategies For Improving Credit Utilization

Defining Credit Utilization Ratio and Its Role

When it comes to understanding your financial health, few metrics are as important as your credit utilization ratio. Think of it like a financial snapshot that shows how much of your available credit you’re actually using. According to Chase, this ratio is calculated by dividing the total amount you owe on credit cards by your total credit limit.

Why does this matter? Because credit utilization plays a massive role in determining your credit score. In fact, it accounts for approximately 30% of your FICO score and 20% of your VantageScore. Financial experts recommend keeping this ratio low – ideally below 30-40%. Here’s what that means in practical terms:

- Keep your credit card balances well below their limits

- Pay down existing balances regularly

- Avoid maxing out credit cards

- Monitor your credit utilization across all cards

Think of your credit utilization like a health meter for your financial reputation. A low ratio signals to lenders that you’re responsible with credit and can manage your finances effectively. As Investopedia points out, the lower your ratio, the better positioned you are for favorable credit terms and opportunities.

Calculation Methods and Real-World Examples

Calculating your credit utilization ratio is surprisingly straightforward. According to Chase, you simply divide your total credit card balance by your total credit limit and convert the result to a percentage. For instance, if you have a credit card with a $1,000 limit and currently owe $500, your utilization for that card would be 50%.

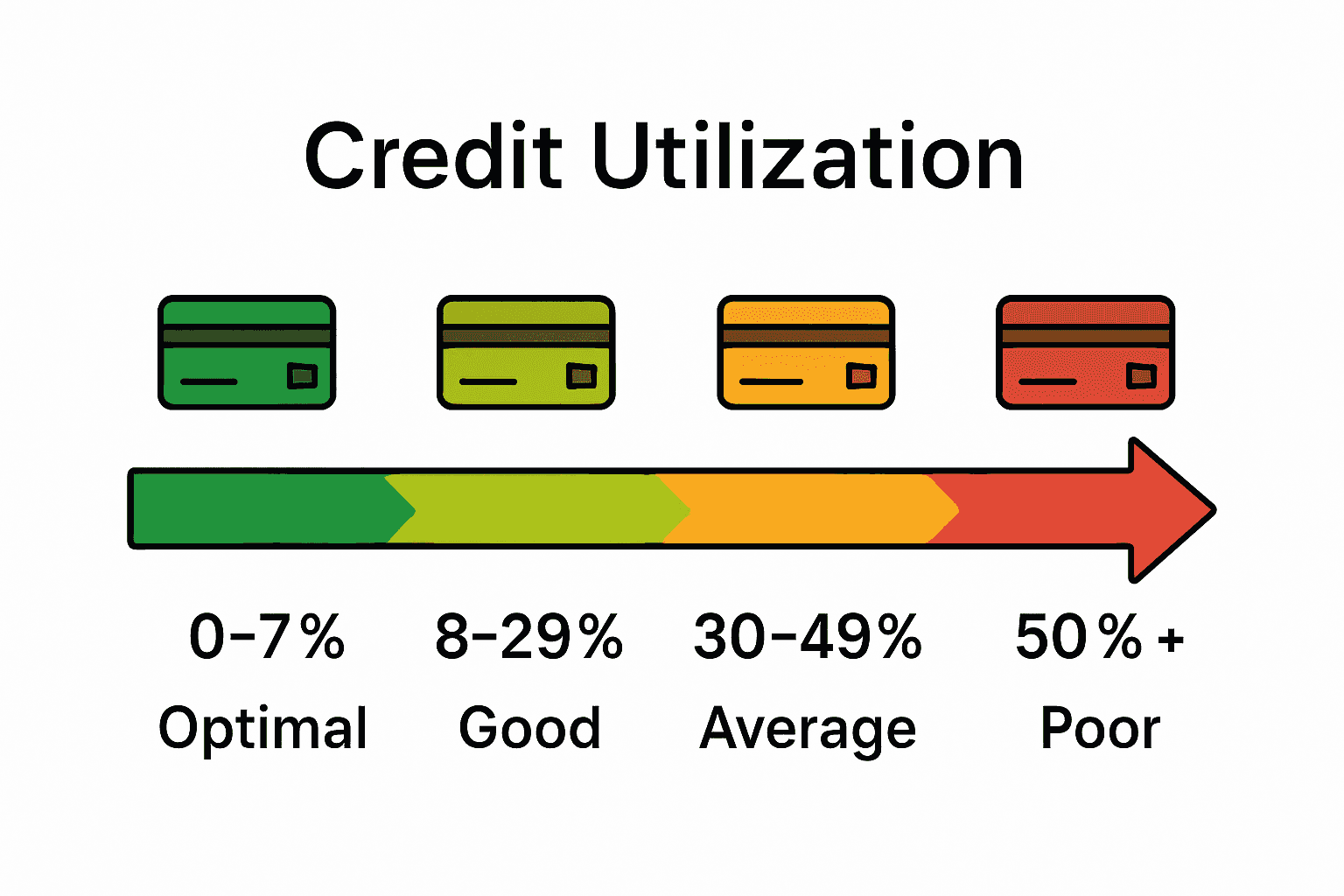

Not all utilization percentages are created equal. Credit Captain breaks down utilization ranges into helpful categories:

- 0-7%: Optimal range, yields best credit score impact

- 8-29%: Good utilization zone

- 30-49%: Average credit impact

- 50%+: Poor credit utilization

Let’s walk through a practical example. Imagine you have three credit cards:

- Card A: $300 balance on $1,000 limit (30% utilization)

- Card B: $50 balance on $2,000 limit (2.5% utilization)

- Card C: $800 balance on $1,500 limit (53% utilization)

Your overall credit utilization would be the total balance across all cards divided by total available credit. In this scenario, you’d want to focus on reducing the balance on Card C to improve your credit score.

How Credit Utilization Affects Credit Scores

Your credit utilization ratio is like a financial report card that lenders use to evaluate your creditworthiness. According to Chase, this metric represents about 30% of your FICO score and roughly 20% of your VantageScore – making it a critical factor in your overall credit health. Understand more about the importance of credit scores.

The relationship between credit utilization and credit scores is straightforward: higher utilization signals greater financial risk to lenders. According to Investopedia, maintaining high credit utilization can significantly lower your credit score. This means consistently maxing out credit cards or carrying large balances relative to your credit limits can send a red flag to potential creditors.

Here’s how different utilization levels typically impact your credit score:

Here’s a comparison of how different credit utilization ranges impact your credit score:

| Utilization Range | Score Impact | Lender Perception |

|---|---|---|

| 0-10% | Excellent | Very Low Risk |

| 11-30% | Good | Low Risk |

| 31-50% | Moderate Negative | Medium Risk |

| 51%+ | Substantial Negative | High Risk |

- 0-10%: Excellent credit score impact

- 11-30%: Good credit score performance

- 31-50%: Moderate negative impact

- 51%+: Substantial credit score reduction

To protect your credit score, financial experts recommend keeping your overall credit utilization below 30-40%. This demonstrates responsible credit management and shows lenders you’re not overly reliant on credit. Think of it like maintaining a healthy financial diet – moderation is key to long-term financial wellness.

Common Misconceptions and Mistakes to Avoid

When it comes to credit utilization, many people fall prey to common myths that can inadvertently damage their financial health. One widespread misconception is that completely avoiding credit is the best strategy. However, Investopedia reveals that minimal credit usage can actually be slightly negative, as creditors need data to assess your creditworthiness.

Another critical mistake many people make involves managing credit card accounts. According to Investopedia, closing old credit card accounts can unexpectedly harm your credit score through multiple mechanisms:

- Reduces total available credit

- Increases overall credit utilization ratio

- Lowers average account age

- Decreases credit mix

Instead of closing accounts, financial experts recommend more strategic approaches like requesting a credit limit increase or keeping older accounts open with minimal activity. This helps maintain a lower utilization ratio and demonstrates a longer credit history.

A few key mistakes to avoid include:

- Maxing out credit cards

- Closing long-standing credit accounts

- Never using credit at all

- Ignoring your credit utilization across multiple cards

The golden rule is balance. Use credit responsibly, keep utilization low, and maintain a mix of credit types to show financial sophistication to potential lenders.

Effective Strategies for Improving Credit Utilization

Improving your credit utilization ratio requires strategic financial planning and smart credit management. According to Experian, there are several effective methods to keep your credit utilization low and maintain a healthy credit profile. Learn more about managing credit card debt to complement these strategies.

Credello recommends multiple approaches to optimize your credit utilization. Here are some proven strategies:

- Make multiple payments each month

- Request credit limit increases

- Spread spending across multiple credit cards

- Keep older credit accounts open

- Pay purchases quickly

A practical approach involves strategic debt management. For instance, if you have multiple credit cards, consider spreading your expenses across them to maintain a lower utilization rate on each card. This technique prevents any single card from appearing maxed out. Another powerful strategy is requesting credit limit increases, which automatically lowers your utilization percentage without changing your spending habits.

Remember, the goal isn’t to avoid credit but to use it intelligently. Some additional tactics include:

- Use automatic payments to ensure timely bill settlements

- Monitor your credit report regularly

- Consider consolidating high-interest debts

- Maintain a mix of credit types

The key is consistent, responsible credit management. By implementing these strategies, you can effectively improve your credit utilization ratio and enhance your overall financial health.

Take Control of Your Credit Utilization—Secure Your Financial Future

Struggling to keep your credit utilization ratio in check can feel overwhelming, especially when you know it makes up a major portion of your credit score. High balances, overlooked credit limits, and the fear of hurting your score by making mistakes like closing old accounts can lead to anxiety and second-guessing. If you want to stop letting your credit worries keep you up at night and finally achieve the optimal credit utilization highlighted in this guide, you need practical, expert-driven strategies tailored to your unique financial goals.

Let us help you master your credit utilization and achieve real financial confidence. Visit FinBlog today to access proven tips and in-depth guides, including our popular sections on the importance of credit scores and managing credit card debt. Take the first step to improve your credit profile by connecting with our trusted advisors or signing up for exclusive guidance now. Your path to smarter credit management starts at FinBlog — act now and get on the road to prime credit health.

Frequently Asked Questions

What is a credit utilization ratio?

A credit utilization ratio is a financial metric that compares the total amount of credit you are using to your total credit limit. It is calculated by dividing your total credit card balances by your total credit limits, expressed as a percentage.

Why is credit utilization important for my credit score?

Credit utilization is a crucial factor in determining your credit score, accounting for about 30% of your FICO score and 20% of your VantageScore. A lower utilization ratio indicates responsible credit management, which can lead to better credit terms and opportunities.

How can I improve my credit utilization ratio?

To improve your credit utilization ratio, you can make multiple payments each month, request credit limit increases, spread your spending across multiple credit cards, and keep older credit accounts open, thereby maintaining a low utilization rate.

What utilization percentage is considered ideal for credit scores?

Financial experts recommend keeping your credit utilization ratio below 30-40%. An optimal range of 0-10% is considered excellent for maintaining a healthy credit score.