TL;DR:

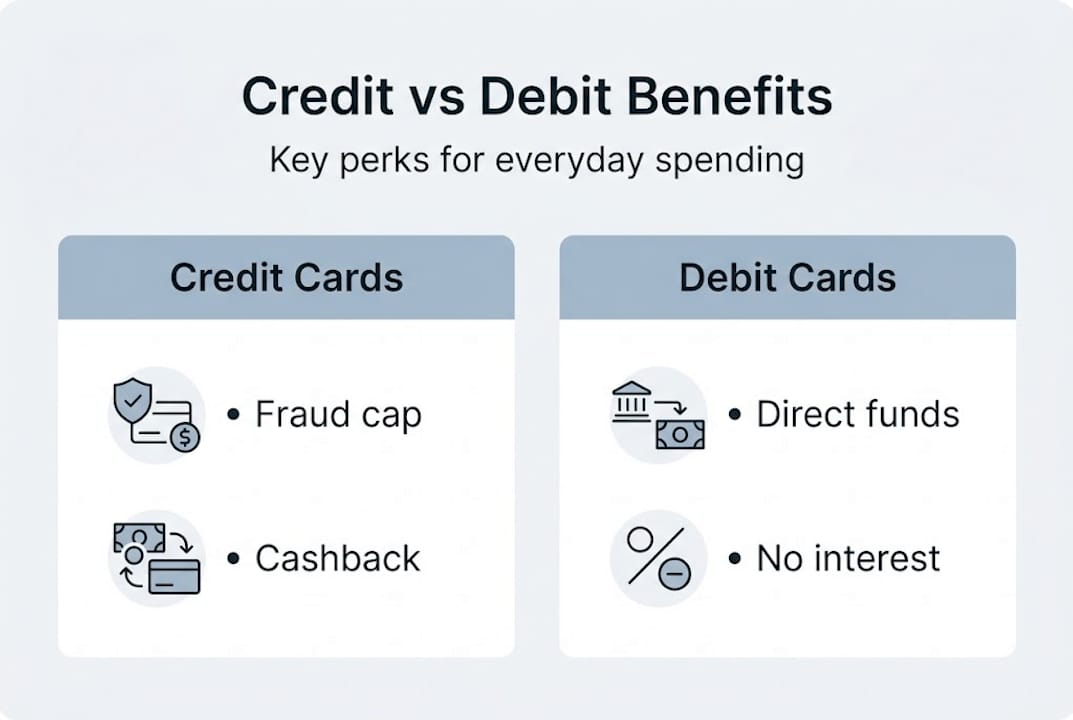

- Credit cards offer stronger fraud protection and help build credit, while debit cards have weaker protections.

- Debit cards limit spending to your checking account but do not impact your credit score.

- Choosing between credit and debit depends on your habits, needs, and financial goals.

Most people assume their credit card and debit card are basically the same tool, just with different colors. They swipe either one without a second thought, moving on with their day. But that assumption quietly costs people money, limits their legal protections, and keeps their credit score stuck in place. The choice between credit and debit affects your fraud liability, your budget discipline, your ability to build credit, and even your purchasing power during travel or emergencies. This guide breaks down exactly how each card works, where one clearly beats the other, and how to make the choice that actually fits your life.

Table of Contents

- How credit and debit cards work

- Security and fraud protection: Why it matters

- Impacts on budget and credit: Choosing what fits your goals

- When to use credit, when to use debit

- Our perspective: What most people miss about credit vs debit

- Take control of your finances with expert guidance

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Fraud protection | Credit cards cap your fraud liability much lower than debit cards if your info is stolen. |

| Budgeting impact | Debit cards help you limit spending to cash on hand, while credit cards can enable overspending but may build credit. |

| Credit score effects | Debit cards do not affect your credit score; credit cards do when used responsibly. |

| Best use cases | Credit is safer for big or online buys; debit is better for everyday expenses. |

How credit and debit cards work

At the most basic level, these two cards do something fundamentally different when you swipe them. A credit card lets you borrow money from the card issuer up to a preset spending limit. You get a monthly bill, and you choose to pay it in full or carry a balance (with interest). A debit card, by contrast, pulls money directly and immediately from your checking account. There is no borrowing. There is no bill. The money is just gone.

This difference sounds small, but its real-world effects are enormous. When you book a hotel with a debit card, many hotels place a temporary hold on your account, sometimes several hundred dollars, that can take days to clear. That hold can block rent payments or grocery purchases. Credit cards absorb that hold without touching your cash. For frequent travelers, this alone makes credit the clear winner for bookings.

Understanding the credit versus debit basics matters for more than just hotels. The mechanics of each card type determine what you can do, what you’re protected against, and what financial opportunities each one opens or closes.

Here is a quick breakdown of the key functional differences:

- Credit cards let you spend up to your approved credit limit and pay it back monthly.

- Debit cards draw directly from your bank balance, so spending is capped by what you actually have.

- Credit cards can improve your credit score when used responsibly; debit cards have zero effect on your credit history.

- Credit cards often include rewards like cash back, travel miles, or purchase protection.

- Debit cards give you direct access to your cash, which can actually help you avoid overspending.

A common misconception is that using your debit card for everything is the “safer” financial move because you can’t spend what you don’t have. That logic sounds solid, but it ignores the fact that debit cards carry weaker fraud protection, earn no rewards, and do nothing to build your credit history. Understanding credit card basics reveals that responsible credit use is one of the fastest ways to strengthen your financial profile over time.

Pro Tip: Use your credit card for recurring monthly bills like streaming subscriptions and utilities. It simplifies tracking those expenses and can earn you rewards, but set up automatic full payments so you never carry a balance or pay interest.

With those basics in mind, let’s directly compare how credit and debit stack up when it comes to real-world challenges.

Security and fraud protection: Why it matters

This is where the difference between credit and debit becomes crystal clear, and where the stakes are genuinely high. Federal law sets different rules for each card type, and those rules can mean the difference between a minor inconvenience and losing hundreds of dollars.

Credit cards are governed by the Fair Credit Billing Act (FCBA). Under the FCBA, if someone fraudulently charges your credit card, your maximum liability is $50, and most major card issuers will bring that down to $0 if you report the issue promptly. The money never actually leaves your account during a dispute, because you were borrowing it, not spending your own cash.

Debit cards fall under the Electronic Fund Transfer Act (EFTA), and the rules are less forgiving. The FCBA and EFTA rules create a tiered liability system for debit that depends entirely on how quickly you report the fraud.

| Reporting timeline | Debit card liability | Credit card liability |

|---|---|---|

| Before any unauthorized charges | $0 | $0 |

| Within 2 business days | Up to $50 | Up to $50 (often $0) |

| 3 to 60 days after statement | Up to $500 | Up to $50 (often $0) |

| More than 60 days after statement | Unlimited | Up to $50 (often $0) |

That “unlimited” category in the debit column is the one that should alarm you. If you go on vacation, forget to check your bank statements for two months, and someone has been draining your account the whole time, you could lose every dollar and have no legal recourse to recover it. With a credit card, your exposure stays capped no matter how long it takes you to notice.

“Time is the critical factor in debit card fraud. The longer you wait to report unauthorized transactions, the more of your own money you stand to lose permanently. With credit cards, you’re disputing someone else’s money, not your own.”

Understanding your consumer fraud liability under these two laws is not a dry legal exercise. It is a practical skill. Make it a habit to check your statements weekly, not just monthly. Set up bank alerts for any transaction over a specific dollar amount. These small habits dramatically reduce your risk regardless of which card you carry.

Understanding how cards differ on security is crucial for protecting your money. Next, let’s see how these differences affect everyday spending and budgeting.

Impacts on budget and credit: Choosing what fits your goals

Your card choice does not just affect what happens when something goes wrong. It also shapes how you manage money day-to-day and how your financial profile looks to lenders over time.

Credit cards and your credit score: Every time you use a credit card and make on-time payments, that activity gets reported to the three major credit bureaus. Over time, this builds your credit history and improves your credit score. One of the most important factors in your score is credit utilization, which is the percentage of your available credit limit that you’re currently using. The credit utilization tips that experts consistently recommend: keep your usage below 30% of your limit for the best score impact. Using $300 on a $1,000 limit card is smart. Using $900 is not.

Debit cards, by contrast, have zero influence on your credit score. You could use your debit card perfectly for 10 years and still have no credit history, which would make it nearly impossible to qualify for a mortgage, car loan, or even a competitive credit card in the future.

Debit cards and your budget: The biggest real advantage of a debit card is its built-in spending limit. When your checking account has $800, you can spend $800. That natural ceiling prevents the debt spiral that credit cards can trigger for people who struggle with impulse spending. If you’re working on building better money habits or recovering from past debt, managing card debt is a priority, and starting with debit as your primary card is a reasonable strategy.

Here is a practical numbered list of considerations to help you decide which card fits each spending scenario:

- Do you have a credit card balance you’re already carrying? Use debit for discretionary spending until the balance is paid off.

- Are you booking travel, hotels, or rental cars? Use credit for better protection and to avoid holds on your cash.

- Are you shopping online? Use credit because disputing unauthorized charges is far easier under the FCBA.

- Are you trying to build credit from scratch? Use a credit card for one or two regular purchases and pay in full monthly.

- Are you prone to impulse spending? Use debit to keep your spending anchored to your actual bank balance.

Here is a practical look at how credit and debit play out across a typical monthly budget:

| Spending category | Credit card benefit | Debit card benefit |

|---|---|---|

| Groceries | Earn cash back rewards | No risk of overspending budget |

| Utility bills | Simplified tracking, rewards | Immediate payment, no interest risk |

| Online shopping | Stronger fraud dispute rights | Direct spending from your balance |

| Travel bookings | Avoids holds on cash, trip protection | None recommended here |

| ATM withdrawals | Usually incurs fees | Free access to your own cash |

| Discretionary spending | Risky without strong discipline | Built-in spending cap |

Pro Tip: Set up real-time transaction alerts through your bank or card app. A quick notification for every purchase keeps you aware of your spending pattern and lets you catch fraud instantly, no matter which card you use.

Once you know how your card choices affect your finances, it helps to apply that knowledge to daily life. Let’s look at where each card shines.

When to use credit, when to use debit

Now that you understand the mechanics, protection rules, and budgeting implications, the practical question becomes: when should you actually reach for each card?

Use a credit card when:

The scenario involves risk, distance, or a purchase you may need to dispute. Credit’s stronger legal protection under the FCBA makes it the right tool for purchases where something could go wrong and you’d want a clear path to recovering your money.

- Booking travel: Airlines, hotels, and car rental agencies frequently issue refunds slowly or dispute them entirely. Credit card issuers will fight on your behalf through chargebacks, which debit does not handle as cleanly or quickly.

- Online purchases: Any time you’re buying from a website, especially a new or unfamiliar retailer, you want the FCBA in your corner. If the product never arrives or is counterfeit, a credit card dispute is your fastest resolution.

- Recurring subscriptions: Streaming services, software plans, and membership fees are easy to track and pay automatically on credit. You earn rewards and keep your cash in your account earning interest until the bill is due.

- Large purchases: For appliances, electronics, or furniture, many credit cards offer extended warranty protection or purchase insurance that debit cards simply do not include.

Use a debit card when:

The situation calls for simplicity, direct cash access, or strict spending control.

- ATM withdrawals: Using your own bank’s debit card at its ATMs is usually free. A credit card cash advance, by contrast, starts charging interest immediately with no grace period, which makes it one of the most expensive financial moves you can make.

- Daily cash-based budgeting: Some people use the envelope method, physically allocating cash for each budget category. A debit card supports this mindset by keeping spending tied to real dollars in your account.

- Small, everyday purchases: Coffee, lunch, and quick errands where fraud risk is low and you want to stay within a tight weekly budget are good fits for debit.

- Situations where you’re rebuilding financial discipline: If credit card spending has caused problems before, sticking to debit while you review your card strategies and rebuild habits is a legitimate and practical approach.

Quick reference:

- Credit wins for: fraud protection, online shopping, travel, building credit, and earning rewards.

- Debit wins for: staying on budget, ATM access, avoiding debt, and disciplined everyday spending.

Finally, putting all this into action will sharpen your financial decisions. Let’s wrap up with some perspective you may not hear elsewhere.

Our perspective: What most people miss about credit vs debit

At finblog.com, we’ve noticed a pattern: most financial guides treat this as a features debate. Credit has better fraud protection, debit keeps you on budget, and you should use the right tool for the right job. That advice is technically correct, but it skips the most important variable: you.

The best card isn’t the one with superior features. It’s the one that works with your actual habits, not the habits you plan to have someday. Many people tell themselves they’ll pay the credit card balance in full every month and then quietly carry a balance for years. Others avoid credit entirely out of fear and end up with no credit history when they actually need a loan.

Credit card overspending often has an emotional trigger: stress shopping, social comparison, or treating a bonus as permission to splurge. Debit card overdrafts have their own traps too, especially if you’re not tracking your balance in real time. Neither card fixes a budgeting mindset problem on its own.

Our advice: before you focus on which card has better perks, spend one month reviewing your long-term card strategies and writing down what actually triggers your biggest spending mistakes. Awareness and intention are the only features that work on every purchase.

Pro Tip: Schedule a 10-minute monthly statement review on your calendar. Catching a fraudulent charge, a forgotten subscription, or a spending pattern that’s drifting out of control is worth far more than any reward points you could earn.

Take control of your finances with expert guidance

Understanding the difference between credit and debit is just the starting point. Smart card use, fraud protection, debt management, and building a credit profile that works in your favor all require ongoing attention and the right information. At Finblog, we publish clear and actionable guides designed to help you make confident financial decisions at every stage. Whether you’re working to pay down debt, improve your credit score, or simply get more from the money you already have, Finblog’s financial insights give you the practical knowledge to move forward.

Explore our full library of guides on credit strategy, budgeting, and fraud protection. Your financial goals are specific to you, and the right guidance should be too.

Frequently asked questions

What is the biggest advantage of credit cards over debit cards?

The biggest advantage is stronger fraud protection, limiting your liability to $50 or less under the FCBA if your card is used fraudulently, often reduced to $0 by most issuers.

Will using a debit card help improve my credit score?

No, debit card use is never reported to credit bureaus, so it has no effect on your credit score regardless of how consistently you use it.

What should I do if my debit card is lost or stolen?

Report it to your bank immediately, because your liability under EFTA can rise from $50 to unlimited the longer you wait to report the loss.

Are there situations where using debit is better than credit?

Yes, debit is the smarter choice for ATM withdrawals, strict cash-based budgeting, and any situation where avoiding potential debt and interest charges is your top priority.

Can I avoid credit card interest completely?

You can avoid interest entirely by paying your full statement balance before the due date every single month, which also helps your credit utilization stay low.