TL;DR:

- Liquidity refers to the speed and ease with which an asset can be converted into cash without significantly affecting its price. Understanding the three types—market, accounting, and personal liquidity—helps investors evaluate financial flexibility and risk. Properly structured liquidity plans enable quick access to funds, reduce hidden costs, and support strategic decision-making during market fluctuations.

Most people assume liquidity simply means having money. It doesn’t. What is liquidity, really? It’s about speed and frictionless conversion. Liquidity describes how quickly you can turn an asset into cash without moving its price in the process. A savings account is highly liquid. A rental property in a slow market is not. For investors, students, and finance professionals, understanding what liquidity actually means, and how it behaves across markets, companies, and personal portfolios, is the difference between making informed decisions and being caught off guard when it matters most.

Table of Contents

- Key Takeaways

- What is liquidity in finance: the full picture

- How to assess liquidity practically

- Why liquidity matters more than you think

- Optimizing your own liquidity plan

- My take on what most people get wrong about liquidity

- Explore deeper financial guidance on Finblog

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Liquidity means conversion speed | An asset is liquid if it can be sold quickly at or near its market value without disruption. |

| Three types of liquidity exist | Market, accounting, and personal liquidity each measure a different dimension of financial flexibility. |

| Ratios reveal company health | Current ratio, quick ratio, and cash ratio show how well a business can cover short-term obligations. |

| Bid-ask spread signals cost | Wide spreads mean illiquid markets and hidden trading costs that silently erode returns. |

| Planning beats holding | Unstructured cash creates opportunity cost. A tiered liquidity plan turns idle money into a productive system. |

What is liquidity in finance: the full picture

The liquidity definition most textbooks give you is technically correct but practically incomplete. Liquidity in finance measures how easily an asset can be converted to cash at a stable price. But the real insight is that liquidity exists on a spectrum, and where an asset sits on that spectrum determines how you should think about owning it.

Cash is the benchmark. It converts to purchasing power instantly, at no cost, with no price impact. From there, liquidity decreases. U.S. Treasury bills and money market funds are nearly as liquid as cash. Large-cap stocks traded on major exchanges are highly liquid since you can sell millions of dollars worth in seconds. Real estate, private equity, and collectibles sit at the illiquid end. Selling them takes weeks, months, or sometimes years, and rushing the process almost always means accepting a lower price.

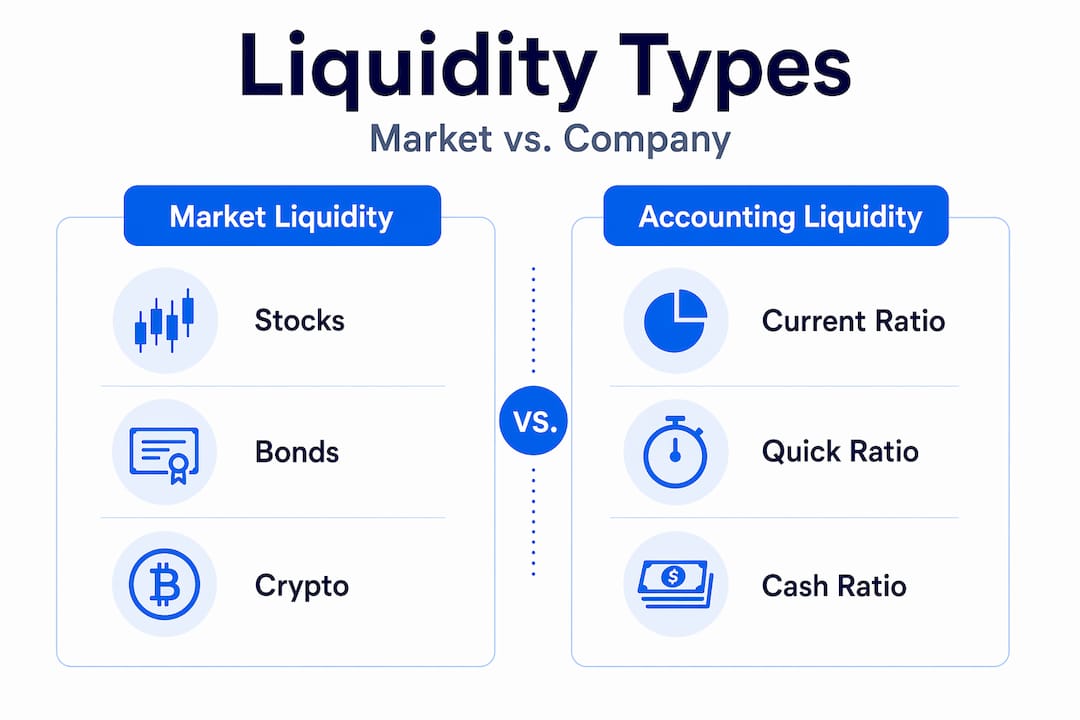

There are three distinct types of liquidity worth knowing:

- Market liquidity refers to how efficiently assets can be bought or sold in a market without causing significant price movement. Stock markets are generally highly liquid. Thinly traded small-cap stocks or exotic bonds are not.

- Accounting liquidity measures a company’s ability to meet short-term obligations using its current assets. This is what finance teams track through liquidity ratios on the balance sheet.

- Personal liquidity is about your own financial position. How much of your net worth can you access within days, without penalty, if something unexpected happens?

Understanding the difference between these three is not academic. It shapes how you read financial statements, evaluate investment risk, and plan your own finances.

The bid-ask spread and what it reveals

One concept tied tightly to market liquidity is the bid-ask spread. The bid is the highest price a buyer will pay. The ask is the lowest price a seller will accept. The gap between them is the spread. In liquid markets, that gap is tiny. A tight spread might look like 100.00 bid / 100.02 ask. An illiquid market might show 100.00 bid / 100.50 ask.

That difference matters more than it looks. Every time you buy at the ask and eventually sell at the bid, you absorb that spread as an immediate loss. In liquid markets, that cost is negligible. In illiquid ones, it’s a meaningful drag on returns before the position has even moved.

How to assess liquidity practically

For companies, the standard approach to assessing liquidity uses three key ratios. Each one gets progressively more conservative in what it counts as available cash. Liquidity ratios such as the current ratio, quick ratio, and cash ratio measure a company’s ability to cover short-term liabilities at different levels of strictness.

| Ratio | Formula | What it measures |

|---|---|---|

| Current ratio | Current Assets / Current Liabilities | Broad short-term solvency |

| Quick ratio | (Current Assets – Inventory) / Current Liabilities | Ability to pay without selling inventory |

| Cash ratio | (Cash + Short-Term Investments) / Current Liabilities | Most conservative; pure cash coverage |

A ratio above 1.0 generally signals healthy liquidity, meaning the company can cover what it owes in the near term. A ratio well below 1.0 is a warning sign. That said, ratios alone don’t tell the full story. A retail company naturally carries more inventory than a software firm, so their current ratios aren’t directly comparable without context.

For market liquidity, the two primary indicators are bid-ask spread and average daily trading volume. High volume combined with a tight spread signals a liquid market where you can enter and exit positions efficiently. Low volume with a wide spread means the opposite. You may find yourself holding a position longer than planned simply because there aren’t enough willing buyers at a price you’d accept.

Pro Tip: When evaluating a stock for your portfolio, check its average daily volume over the past 30 days, not just its current price. A stock trading at $50 with a daily volume of 10,000 shares is far harder to exit quickly than one trading at the same price with 5 million shares of daily volume.

One common mistake when measuring liquidity is treating it as static. Liquidity conditions change. A market that trades smoothly during normal conditions can freeze during a crisis, which is exactly when you most need to sell. Build that uncertainty into your assessment.

Why liquidity matters more than you think

Liquidity shapes financial outcomes in ways that aren’t always obvious until something goes wrong. Here’s where it actually shows up in your decisions and your risk profile:

- Trading efficiency. In liquid markets, large buy or sell orders get executed near the quoted price. In illiquid markets, a large order can move the price against you, a phenomenon called market impact. You end up paying more to buy or receiving less to sell.

- Hidden transaction costs. Wide bid-ask spreads create real costs that don’t show up in brokerage commission statements. Retail investors often overlook these costs entirely, yet they can silently erode returns over time even when prices appear stable.

- Corporate survival. A profitable business can still collapse if it runs out of liquid assets to pay suppliers, employees, and debt service. The income statement might look fine while the company quietly spirals into insolvency. Understanding cash flow importance is inseparable from understanding liquidity.

- Forced selling. When investors or businesses face cash needs and hold only illiquid assets, they are forced to sell at whatever price the market offers. That is rarely a good price.

“CEOs who view cash as ‘idle’ are missing the strategic dimension of liquidity. It is not just safety. It is optionality and speed in a world where opportunities close fast.”

This framing shifts how you think about holding cash. It’s not lazy money. It’s the capacity to act decisively when others can’t.

Optimizing your own liquidity plan

Knowing what liquidity means is one thing. Structuring it intentionally is another. Most individuals and even many professionals hold cash without a framework, which creates its own set of problems. Unstructured liquidity leads to hidden costs including inflation erosion, missed compounding, and tax inefficiency. Cash sitting in a low-yield checking account doesn’t feel expensive, but it is.

A practical starting point is segmenting your assets into three liquidity tiers:

- Stability tier. Three to five years of living expenses or operating costs kept in highly liquid, low-risk accounts. This covers emergencies and near-term obligations without disrupting longer-term investments.

- Growth tier. Capital deployed in stocks, bonds, or diversified funds with a medium-term horizon. Liquid enough to access within days, but not intended for short-term use.

- Legacy tier. Long-term holdings such as real estate, private equity, or illiquid alternatives. These carry the highest return potential and the lowest liquidity. They should only be funded after the first two tiers are solid.

This tiered approach prevents the most common liquidity mistake: holding too much in illiquid assets because returns look attractive, then scrambling when cash is needed.

One distinction that gets overlooked is the difference between liquidity and credit. Credit is conditional. A lender can pull a line of credit exactly when your business looks most vulnerable. Cash gives you unconditional control. Building your liquidity plan around credit availability is building on sand.

Pro Tip: Review your liquidity position quarterly, not just when markets move. Check that your stability tier remains funded, your growth tier aligns with your actual timeline, and you haven’t inadvertently concentrated too much into illiquid assets as markets have shifted.

The goal isn’t maximum liquidity. It’s intentional liquidity. A structured plan transforms cash from idle capital into an active tool that supports your financial goals rather than quietly working against them. For a deeper framework on managing this in practice, Finblog’s guide on personal finance management is worth your time.

My take on what most people get wrong about liquidity

I’ve spent years watching smart, disciplined investors make the same mistake: they treat liquidity as purely defensive. They hold cash because it feels safe. Then they watch inflation quietly chip away at its value while they wait for the “right” opportunity.

What I’ve learned is that liquidity is not about safety. It’s about speed and optionality. The investors I’ve seen generate consistently strong results aren’t the ones with the highest returns on paper. They’re the ones who had cash available when prices collapsed in 2020, when real estate deals closed fast, or when a business acquisition came up with a two-week deadline. Liquidity was the variable that let them act.

The uncomfortable truth is that most people’s liquidity isn’t actually liquid when it counts. It’s tied up in assets they can’t access quickly without loss, or it’s technically available but mentally earmarked for something else. That’s not a plan. That’s avoidance.

What actually works, in my experience, is treating liquidity as a deliberate allocation decision the same way you treat equity or fixed income. Decide how much you need in each tier, fund it before deploying into growth assets, and review it on a schedule. That discipline creates confidence. And confidence means you don’t panic-sell at the bottom when markets turn.

— Povilas

Explore deeper financial guidance on Finblog

If this article has given you a clearer sense of what liquidity means and why it matters, the next step is putting that understanding to work in your actual financial decisions. Finblog publishes in-depth, practitioner-level guides designed for investors and finance professionals who want more than surface-level explanations.

Explore how liquidity shapes investing across different asset classes and market conditions, from stocks and bonds to alternatives. If you’re building or reviewing a personal finance strategy, the resources on Finblog cover practical frameworks for capital allocation, risk management, and building financial resilience. The goal isn’t just knowledge. It’s knowledge you can act on, structured around decisions that actually matter to your financial future.

FAQ

What is the simple definition of liquidity?

Liquidity measures how quickly and easily an asset can be converted into cash without significantly affecting its price. Cash itself is the most liquid asset.

What are the main types of liquidity?

The three main types are market liquidity (ease of trading assets in a market), accounting liquidity (a company’s ability to cover short-term debts), and personal liquidity (how much of your own wealth is quickly accessible).

How do you assess a company’s liquidity?

Use the current ratio, quick ratio, and cash ratio, which measure a company’s short-term assets against its short-term liabilities. A ratio above 1.0 generally indicates the company can meet its near-term obligations.

Is credit the same as liquidity?

No. Credit is conditional and can be withdrawn by lenders at any time. Liquidity represents actual cash or assets you control unconditionally, which makes it more reliable in a financial crisis.

Why does liquidity matter for investors?

Liquidity affects how easily you can buy or sell investments, how much you pay in spread costs, and whether you can access funds when opportunities or emergencies arise without being forced to sell at a loss.