Nearly 60 percent of adults say they feel anxious when thinking about their finances. Personal finance management shapes your ability to handle unexpected expenses and reach your financial goals without added stress. By grasping a few essential strategies, you can create a foundation for stability and start building confidence in your money decisions.

Table of Contents

- Defining Personal Finance Management Basics

- Types Of Financial Strategies And Tools

- Budgeting, Saving, And Investment Fundamentals

- Debt Management And Risk Mitigation Techniques

- Common Mistakes And How To Avoid Them

Key Takeaways

| Point | Details |

|---|---|

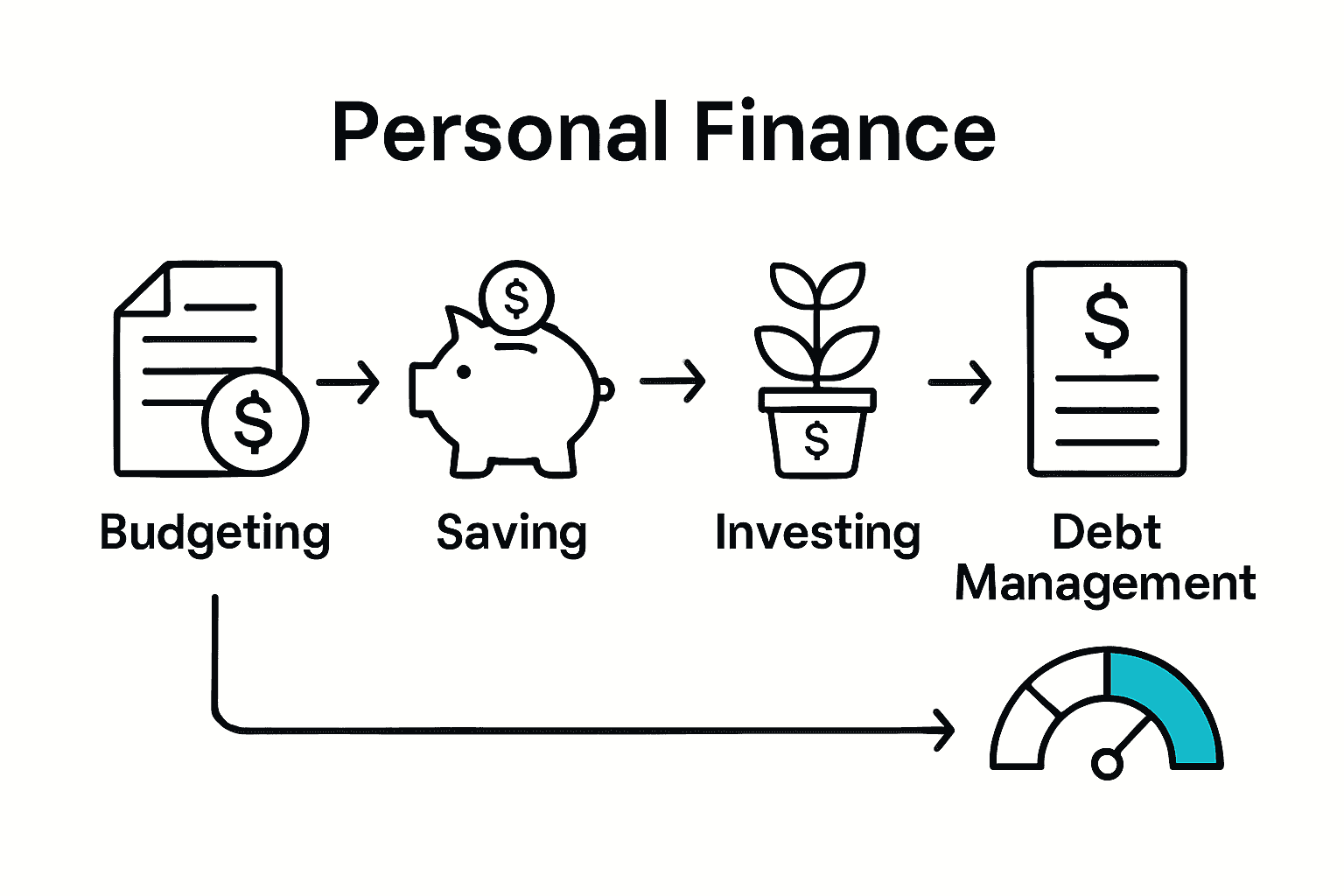

| Comprehensive Personal Finance Management | Involves budgeting, saving, investing, and debt management to achieve financial security. |

| Continuous Learning and Adaptation | Regularly assess your financial situation, risks, and strategies to optimize personal finance. |

| Avoid Common Financial Mistakes | Plan effectively to prevent errors in budgeting, saving, and investing that impact long-term stability. |

| Utilize Effective Financial Strategies | Implement tailored budgeting techniques and investment tools suited to individual financial goals. |

Defining Personal Finance Management Basics

Personal finance management is the strategic process of understanding, organizing, and optimizing your financial resources to achieve personal economic goals. According to Library of Congress Guides, it encompasses managing an individual or household’s financial activities to establish stability and create a pathway toward long-term financial security.

At its core, personal finance management involves several critical components that work together to build a robust financial foundation. These components include:

- Budgeting: Tracking income and expenses to understand spending patterns

- Saving: Setting aside money for emergencies and future objectives

- Investing: Growing wealth through strategic financial instruments

- Debt Management: Controlling and reducing financial liabilities

Effective personal finance isn’t just about tracking numbers. As Vaia explains, it’s about creating a comprehensive strategy that reduces financial stress and enhances overall quality of life. By setting clear short-term and long-term financial goals, individuals can make informed decisions that align their daily spending with their broader financial aspirations.

Successful personal finance management requires continuous learning and adaptation. It means understanding your current financial situation, identifying potential risks, and developing strategies to mitigate them. For those looking to take their financial planning to the next level, our financial planning for beginners guide offers practical insights to jumpstart your journey toward financial empowerment.

Types Of Financial Strategies And Tools

Financial strategies are comprehensive approaches designed to help individuals achieve their monetary objectives and secure their financial future. According to Vaia, these strategies encompass key areas like budgeting, saving, investing, and debt management, each playing a crucial role in overall financial health.

The primary financial strategies and tools can be categorized into several essential domains:

-

Budgeting Strategies

- Zero-based budgeting

- 50/30/20 rule

- Envelope method

-

Saving Tools

- High-yield savings accounts

- Certificates of deposit

- Money market accounts

-

Investment Approaches

- Diversified portfolio management

- Index fund investing

- Retirement account contributions

-

Debt Management Techniques

- Debt snowball method

- Debt avalanche strategy

- Consolidation loans

As research from Florida International University Faculty indicates, successful personal financial planning involves coordinating multiple components through organized strategies and wise decision-making. Implementing these strategies requires understanding your unique financial situation and selecting tools that align with your specific goals.

For investors seeking to optimize their financial approach, understanding tax-efficient investing can provide significant advantages in building long-term wealth. By strategically selecting investment vehicles and managing tax implications, individuals can maximize their financial potential and create a more secure economic future.

Budgeting, Saving, And Investment Fundamentals

Personal financial success hinges on mastering three fundamental pillars: budgeting, saving, and investing. According to Florida International University Faculty, these activities form the cornerstone of a comprehensive financial strategy, enabling individuals to achieve future security and financial stability.

Let’s break down each fundamental component:

Here’s a summary of the core pillars of personal finance management:

| Pillar | Purpose | Key Approaches |

|---|---|---|

| Budgeting | Structured spending plan | Track income Categorize expenses Set limits |

| Saving | Build financial safety nets | Emergency fund Automate savings High-yield accounts |

| Investing | Grow long-term wealth | Diversify portfolio Assess risk tolerance Compound growth |

Budgeting Essentials

- Purpose: Create a structured spending plan

- Goal: Align expenses with financial objectives

- Key Techniques:

- Track all income sources

- Categorize essential and discretionary expenses

- Set realistic spending limits

Saving Strategies

- Purpose: Build financial safety nets

- Goal: Accumulate funds for emergencies and future needs

- Key Approaches:

- Establish emergency fund (3-6 months of expenses)

- Automate savings contributions

- Use high-yield savings accounts

Investment Principles

- Purpose: Generate long-term wealth

- Goal: Grow financial resources beyond basic savings

- Key Strategies:

- Diversify investment portfolio

- Understand risk tolerance

- Consider long-term compound growth

As Vaia explains, successfully coordinating these components requires an organized approach and consistent decision-making. By understanding the nuanced differences between spending, saving, and investing, individuals can create a robust financial framework.

For those looking to refine their budgeting skills, our guide on how to budget effectively provides practical insights to help transform financial management from a challenge into a structured, achievable process.

Debt Management And Risk Mitigation Techniques

Financial resilience requires a strategic approach to managing debt and mitigating potential risks. According to Florida International University Faculty, successful financial management involves carefully planning borrowing strategies and protecting against unforeseen events through comprehensive risk management techniques.

Debt management strategies can be categorized into key approaches:

Debt Reduction Techniques

- Prioritize High-Interest Debt

- List all debts with interest rates

- Focus on highest-interest obligations first

- Consider debt consolidation options

Debt Repayment Strategies

- Systematic Debt Elimination

- Snowball method (smallest balance first)

- Avalanche method (highest interest first)

- Negotiate lower interest rates

Risk Mitigation Approaches

- Financial Protection Strategies

- Emergency fund development

- Comprehensive insurance coverage

- Diversified investment portfolio

Vaia emphasizes that effective risk mitigation involves a proactive approach to protecting financial resources, including obtaining appropriate insurance and strategically diversifying investments to minimize potential losses.

For individuals struggling with credit challenges, our guide to managing credit card debt offers practical insights into breaking free from financial constraints and building a more stable financial future.

Common Mistakes And How To Avoid Them

Financial success is often derailed by preventable errors that can significantly impact long-term economic stability. According to Vaia, common personal finance mistakes frequently stem from lack of planning, insufficient savings, and poor debt management.

Key financial mistakes to watch out for include:

Budgeting Blunders

- Overlooking Small Expenses

- Ignore daily coffee purchases

- Neglect subscription services

- Underestimate impulse buying

Savings Pitfalls

- Failing to Protect Financial Future

- No emergency fund

- Inadequate retirement planning

- Avoiding automatic savings contributions

Investment Errors

- Common Investment Mistakes

- Emotional investing

- Lack of diversification

- Trying to time the market

Research from Florida International University Faculty highlights that avoiding these financial mistakes requires coordinated planning and wise decision-making. The key is developing a proactive approach to personal finance that anticipates potential challenges and creates robust strategies to address them.

For those seeking to identify and overcome financial missteps, our guide to common budgeting mistakes provides practical insights to help you steer clear of typical financial pitfalls and build a more secure financial foundation.

Take Control of Your Financial Future Today

Managing your personal finances can feel overwhelming when faced with budgeting struggles, debt worries, and investment uncertainties. This complete guide showed you how critical it is to align spending with your goals, build savings cushions, and invest wisely to protect against risk and avoid common pitfalls. If you find yourself wanting a clearer path or dedicated support to turn these concepts into actionable plans, you are not alone.

At finblog.com, we specialize in empowering individuals like you with expert advice and practical tools tailored to personal finance management basics. Explore resources such as our financial planning for beginners guide or learn the essentials with our guide on how to budget effectively. Don’t wait to create financial resilience. Visit finblog.com now and take the next step toward mastering your money with confidence.

Frequently Asked Questions

What are the essential components of personal finance management?

Personal finance management includes budgeting, saving, investing, and debt management. These components work together to create a stable financial foundation and help achieve economic goals.

How can I effectively budget my finances?

To budget effectively, track all income sources, categorize essential and discretionary expenses, and set realistic spending limits. Techniques like the zero-based budgeting method or the 50/30/20 rule can be helpful.

What strategies can I use to manage debt?

You can use debt reduction techniques such as focusing on high-interest debt first, utilizing the debt snowball or avalanche methods, and considering debt consolidation options to manage and reduce debt effectively.

Why is it important to have an emergency fund?

An emergency fund is crucial for financial resilience as it provides a safety net during unexpected expenses or emergencies. It is recommended to save 3-6 months’ worth of expenses to cover unforeseen events.