TL;DR:

- Choosing the right IRA affects long-term taxes and retirement income strategy.

- Traditional IRA offers upfront deductions but taxes withdrawals, while Roth IRA provides tax-free growth.

- Your current versus future tax rate is the key factor in selecting between IRAs.

Choosing the wrong IRA type could cost you tens of thousands of dollars in unnecessary taxes over a 30-year retirement. That is not a scare tactic. It is a math problem most people never sit down to solve. The good news is that once you understand how Traditional and Roth IRAs treat your money differently, the decision becomes far less intimidating. This article walks you through the core tax differences, 2026 contribution rules, withdrawal mechanics, and the strategic factors that actually determine which account, or combination of both, makes the most sense for your retirement plan.

Table of Contents

- Understanding Traditional and Roth IRAs

- Contribution limits, income thresholds, and deadlines for 2026

- Comparing tax benefits and withdrawal rules

- Strategic considerations: Which IRA fits your long-term plan?

- Our take: The real value in choosing between Traditional and Roth IRAs

- Explore more insights and secure your retirement strategy

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Tax treatment difference | Traditional IRA provides upfront tax deductions, while Roth IRA offers tax-free withdrawals. |

| 2026 contribution rules | You can contribute up to $7,500 total to IRAs ($8,600 if 50+) by April 15, 2027. |

| Withdrawal flexibility | Roth IRAs allow penalty-free withdrawal of contributions and no required distributions for owners. |

| Strategic splitting | If unsure, diversify between both IRA types to balance tax risks and increase flexibility. |

| Estate planning advantage | Roth IRAs are more favorable for heirs, offering potential tax-free inheritance. |

Understanding Traditional and Roth IRAs

Before you can pick the right account, you need to understand what each one actually does with your money. The difference is not just a label. It changes when you pay taxes, how your money grows, and how much you keep in retirement.

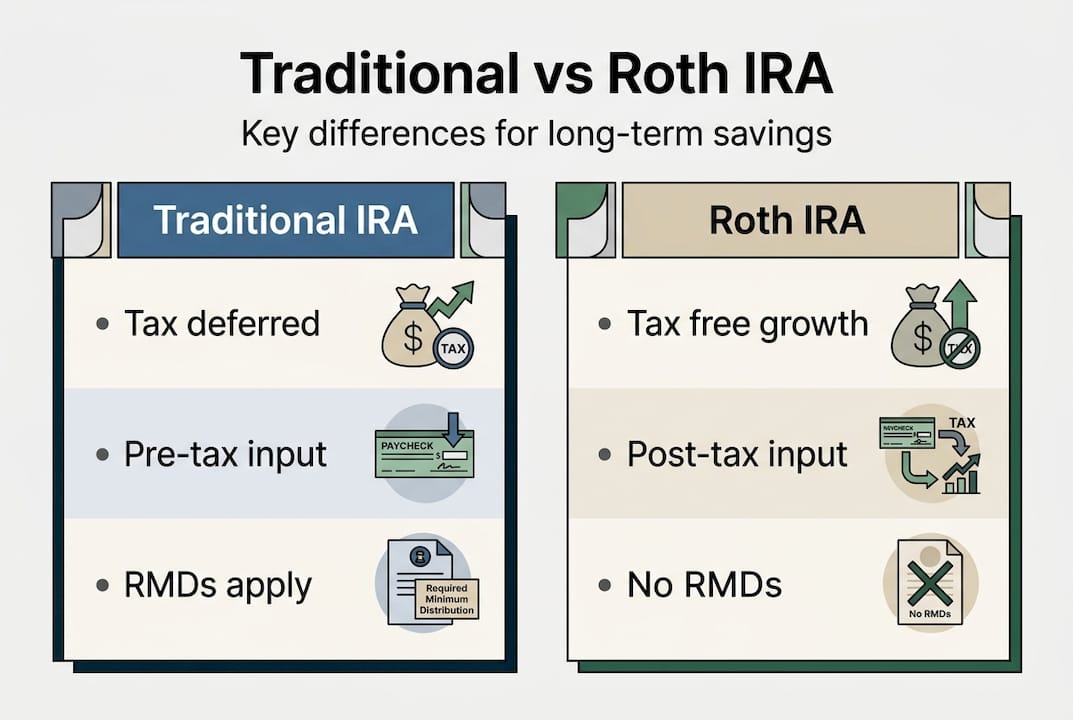

A Traditional IRA lets you contribute money before it is taxed. If you qualify for the deduction, your contribution reduces your taxable income today. Your investments then grow tax-deferred, meaning you pay nothing on gains year after year. The catch comes at retirement: every dollar you withdraw is taxed as ordinary income. You are essentially borrowing a tax break now and paying it back later.

A Roth IRA works in reverse. You contribute money you have already paid taxes on, so there is no upfront deduction. But your investments grow completely tax-free, and qualified withdrawals are tax-free in retirement. You pay the tax bill now so you never see it again.

Here is a quick breakdown of the key differences:

- Traditional IRA: Pre-tax contributions, possible deduction, tax-deferred growth, taxed withdrawals

- Roth IRA: After-tax contributions, no deduction, tax-free growth, tax-free qualified withdrawals

- Early withdrawal: Both charge a 10% penalty before age 59½ on earnings, but Roth lets you pull out your contributions (not earnings) anytime without penalty

- Flexibility: Roth wins here because you are not locked into a rigid withdrawal schedule

If you are also weighing whether an IRA is better than a workplace plan, the 401k vs IRA differences guide breaks that down clearly. And if you are still deciding whether to save or invest first, saving vs investing is worth reading before you commit.

Pro Tip: The question is not just “which IRA is better?” It is “which one is better for my tax situation?” Your current tax rate versus your expected retirement tax rate is the single most important variable in this decision.

Contribution limits, income thresholds, and deadlines for 2026

Knowing the rules is not optional. Contributing too much or missing an income threshold can trigger IRS penalties that wipe out any tax benefit you were trying to capture.

For 2026, the IRA contribution limit is $7,500 per year, or $8,600 if you are age 50 or older. That catch-up provision matters a lot if you are in your 50s and trying to accelerate savings. The deadline to make 2026 contributions is April 15, 2027, which gives you extra time even after the calendar year ends.

Here is what the income thresholds look like for 2026:

| Account type | Filing status | Phaseout range |

|---|---|---|

| Roth IRA eligibility | Single / Head of Household | $153,000 to $168,000 |

| Roth IRA eligibility | Married Filing Jointly | $242,000 to $252,000 |

| Traditional IRA deduction | Single (covered by workplace plan) | $81,000 to $91,000 |

| Traditional IRA deduction | Married Filing Jointly (covered) | $129,000 to $149,000 |

These income eligibility ranges phase out your ability to contribute to a Roth or deduct a Traditional IRA contribution. Once you exceed the top of the range, you lose the benefit entirely for that account type.

Key checkpoints to keep in mind:

- The $7,500 limit is a combined cap across all your IRAs, not per account

- You must have earned income equal to or greater than your contribution amount

- Roth phaseout starts at $153,000 MAGI for single filers in 2026

- Contributions can be made up to the tax filing deadline, not just December 31

- If you are covered by a workplace retirement plan, your Traditional IRA deduction may be limited even at moderate incomes

For more detail on what qualifies as a deductible contribution, the IRA deduction rules for 2026 page covers that alongside other common tax deductions worth knowing.

Comparing tax benefits and withdrawal rules

Eligibility is only one side. Let’s see how taxes and withdrawal rules play out for each account over time.

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contribution tax treatment | Pre-tax (deductible if eligible) | After-tax (no deduction) |

| Investment growth | Tax-deferred | Tax-free |

| Withdrawals in retirement | Taxed as ordinary income | Tax-free (if qualified) |

| Required Minimum Distributions | Yes, starting at age 73 | No lifetime RMDs for owner |

| Early withdrawal penalty | 10% on all withdrawals before 59½ | 10% on earnings only; contributions anytime |

| Inheritance tax treatment | Heirs pay taxes on distributions | Tax-free to heirs if 5-year rule met |

The RMD and withdrawal rules are where Traditional IRAs can create unexpected problems. Starting at age 73, you are required to withdraw a minimum amount each year whether you need the money or not. Those withdrawals are taxable, and they can push you into a higher bracket, trigger Medicare surcharges, or increase the portion of Social Security that gets taxed.

“Roth IRA has no lifetime RMDs for the owner, offering more flexibility in managing retirement income and taxes.”

Key withdrawal rules to know:

- Traditional IRA withdrawals before age 59½ face a 10% penalty plus income tax

- Roth contribution withdrawals are always penalty-free and tax-free at any age

- Roth earnings require the account to be at least 5 years old and the owner to be 59½ for tax-free status

- Conversions from Traditional to Roth have their own 5-year clock for penalty-free access

- Traditional IRA heirs pay income tax on every distribution they take

- Roth IRA heirs receive distributions tax-free if the 5-year rule is satisfied

Pro Tip: If leaving wealth to your children or grandchildren is part of your plan, a Roth IRA is a significantly more efficient vehicle. Tax-free inheritance is a real and often overlooked advantage.

For a broader look at how different retirement account features compare, or to think through withdrawal strategies that make your savings last, both are worth bookmarking.

Strategic considerations: Which IRA fits your long-term plan?

Understanding the differences is step one. Applying them to your actual situation is where most people get stuck.

The core question is simple: will your tax rate be higher now or in retirement? If you expect to be in a higher bracket later, paying taxes now with a Roth makes sense. If you expect a lower bracket in retirement, deferring with a Traditional IRA saves you money. When you genuinely do not know, diversifying with both is a legitimate and widely recommended strategy.

Key decision factors to weigh:

- Current vs. future tax rate: The single biggest driver of which account wins mathematically

- Income level: High earners may lose Roth eligibility and need to consider the backdoor approach

- Time horizon: Longer timelines favor Roth because tax-free compounding has more years to work

- Medicare and Social Security: Traditional withdrawals raise your Modified Adjusted Gross Income, which can increase Medicare premiums and the taxable portion of Social Security

- Flexibility needs: Roth wins if you want access to contributions before retirement without penalties

- Estate planning goals: Roth is more efficient for passing wealth to heirs

For high earners above the Roth income limit, the backdoor Roth strategy is a legal workaround. You contribute to a Traditional IRA on a non-deductible basis, then convert it to a Roth. The catch is the pro-rata rule: if you have other pre-tax IRA balances, the IRS aggregates all your non-Roth IRAs when calculating the taxable portion of your conversion. This can create an unexpected tax bill if not planned carefully.

According to T. Rowe Price research, the best approach for most people aged 30 to 55 is to choose based on current versus expected retirement tax rate, and when uncertain, split contributions between both.

Pro Tip: If you are paralyzed by the choice, just start saving. Both IRAs outperform a taxable brokerage account. Explore tax-advantaged strategies and portfolio diversification to build a well-rounded retirement approach.

Our take: The real value in choosing between Traditional and Roth IRAs

Here is the uncomfortable truth most financial content skips: the IRA you pick matters far less than whether you actually save consistently. People spend months researching the “optimal” account while leaving money in a checking account earning nothing. That indecision has a real cost.

The long-term advantage of consistent saving beats the marginal tax optimization of picking the “right” IRA by a wide margin in most scenarios. Both accounts are dramatically better than a taxable brokerage account. If you are saving in either one, you are already ahead of most people.

That said, diversifying between Traditional and Roth is genuinely smart. Tax laws change. Your income changes. Your health, family situation, and spending needs in retirement are impossible to predict perfectly today. Holding both types gives you flexibility to draw from whichever account is more tax-efficient in any given year of retirement.

“Both IRAs are superior to taxable accounts. The best move is to save consistently and adjust your strategy as your situation evolves.”

Do not wait for perfect clarity. Start with what you can contribute now, and revisit your investment diversification strategy annually. Small decisions made early compound into large advantages over time.

Explore more insights and secure your retirement strategy

If this article helped clarify your thinking, you are just getting started. The real work is building a retirement strategy that accounts for your income, tax situation, timeline, and goals, not just picking an account type. At finblog.com, you will find in-depth guides, comparison tools, and practical frameworks designed specifically for people serious about long-term financial planning. Whether you want to go deeper on IRA account comparisons, explore tax-efficient withdrawal strategies, or understand how to layer multiple retirement accounts together, the resources are there. Take the next step and put your retirement savings on a track that actually matches where you want to end up.

Frequently asked questions

Can I contribute to both a Traditional and a Roth IRA in 2026?

Yes, you can split contributions between both IRAs as long as your total does not exceed the combined annual limit of $7,500, or $8,600 if you are age 50 or older.

What happens if my income exceeds the Roth IRA phaseout limit?

You cannot contribute directly to a Roth IRA, but you can use a backdoor Roth conversion by contributing to a Traditional IRA first and then converting it to a Roth.

Do Roth IRAs have required minimum distributions?

No. Roth IRAs have no RMDs for the original account owner, while Traditional IRAs require you to start taking distributions at age 73.

Which IRA is better for estate planning?

Roth IRAs are generally more efficient for heirs because they can receive tax-free distributions as long as the 5-year rule has been satisfied, while Traditional IRA heirs pay ordinary income tax on every withdrawal.

How do my withdrawals impact Medicare premiums or Social Security taxation?

Traditional IRA withdrawals count as taxable income and can raise your MAGI, which increases Medicare premiums and the taxable share of Social Security benefits. Roth withdrawals do not count toward that calculation.

Recommended

- 401k vs IRA: Maximizing Retirement Savings Potential – Finblog

- Tax-advantaged accounts: maximize your savings in 2026 – Finblog

- Expert Retirement Accounts Comparison – Best Choices 2025 – Finblog

- Why invest for retirement: build lasting financial security – Finblog

- Financial Planning | Thrive Benefits