Most working professionals face a harsh reality: median retirement savings fall short of targets, with workers aged 45 to 54 holding only 16% of what they need. This gap threatens financial security in later years. Investing for retirement isn’t optional anymore. It’s the proven path to bridge this shortfall through compound growth and strategic planning. This guide explains why investing is essential, how to approach it wisely, and what steps you can take today to secure your financial future.

Table of Contents

- Key takeaways

- Why investing is essential for a secure retirement

- Smart investment strategies: lifecycle funds, diversification, and professional advice

- Addressing risks and common misconceptions about retirement investing

- Applying investing principles to secure your retirement future

- Explore more retirement investing resources

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Compound growth power | Compound interest can turn modest savings into substantial wealth over time. |

| Inflation erodes wealth | Inflation gradually reduces purchasing power unless your investments exceed it. |

| Social Security gap | Social Security replaces only about 52 percent of preretirement income on average, leaving a gap you must fill with personal savings. |

| Tax advantaged accounts | 401k plans and IRAs boost growth by reducing taxes now and letting investments grow tax deferred or tax free. |

| Lifecycle funds automate allocation | Target date funds automatically adjust asset mix as you age to match your retirement timeline. |

Why investing is essential for a secure retirement

You’ve probably heard that saving for retirement matters. But investing transforms those savings into real wealth. Compound interest turns $1,000 into $17,000 over 30 years at 10% annual returns. Cash savings sitting in a standard account can’t compete with that growth trajectory.

Inflation quietly erodes purchasing power every year. Money that sits idle loses value, even if the number in your account stays the same. A dollar today buys less tomorrow. Investing in assets that outpace inflation protects your future spending power and ensures your retirement funds maintain their value when you need them most.

Many professionals assume Social Security will cover their needs. Reality tells a different story. Social Security replaces only 52% of preretirement income on average. That leaves a substantial gap you must fill through personal savings and investments. Without additional income sources, maintaining your current lifestyle becomes impossible.

Tax-advantaged accounts like 401(k)s and IRAs supercharge your investing power. These vehicles reduce your taxable income today while letting investments grow tax-deferred or tax-free. The combination of compound growth and tax benefits creates a powerful wealth-building engine that accelerates your path to retirement readiness.

“The best time to plant a tree was 20 years ago. The second best time is now.” This ancient wisdom applies perfectly to retirement investing. Every year you delay costs you exponential growth potential.

Consider these compelling reasons to prioritize investing:

- Growth potential far exceeds traditional savings accounts

- Protection against inflation preserves purchasing power

- Tax advantages multiply your effective returns

- Diversification spreads risk across multiple asset classes

- Automation makes consistent investing effortless

Smart investment strategies: lifecycle funds, diversification, and professional advice

Lifecycle funds, also called target date funds, remove guesswork from retirement investing. These funds automatically adjust your asset mix as you age, shifting from aggressive growth stocks to conservative bonds. Over 60% of investors now use target date funds because they align perfectly with lifecycle investing models.

Diversification protects your portfolio from catastrophic losses. Spreading investments across stocks, bonds, real estate, and other assets means poor performance in one area won’t sink your entire retirement plan. When stocks drop, bonds often rise. This balance smooths returns and reduces volatility, letting you sleep better at night.

Working with financial advisors delivers measurable benefits beyond investment selection. Clients with CFP professionals report living more comfortably in retirement and experiencing significantly less financial anxiety. Advisors help you avoid emotional decisions during market turbulence, optimize tax strategies, and adjust plans as your life circumstances change.

Pro Tip: Build an emergency fund covering three to six months of expenses before investing heavily for retirement. This safety net prevents you from raiding retirement accounts during unexpected financial challenges, protecting your long-term growth.

Effective investment strategies share common elements:

- Start with employer match in 401(k) plans for instant returns

- Increase contributions annually as income grows

- Rebalance portfolio yearly to maintain target allocations

- Avoid timing the market or chasing hot investment trends

- Review and adjust strategy with major life changes

The benefits of financial advisors extend beyond portfolio management. They provide accountability, help you stay disciplined during market downturns, and offer perspective when emotions run high. Many professionals find that advisor fees pay for themselves through better decisions and peace of mind.

Understanding sequence of returns risk becomes critical as retirement approaches. Poor market performance in the years immediately before or after retirement can devastate your savings. Advisors help structure withdrawals and asset allocations to minimize this risk, ensuring your money lasts throughout retirement.

Addressing risks and common misconceptions about retirement investing

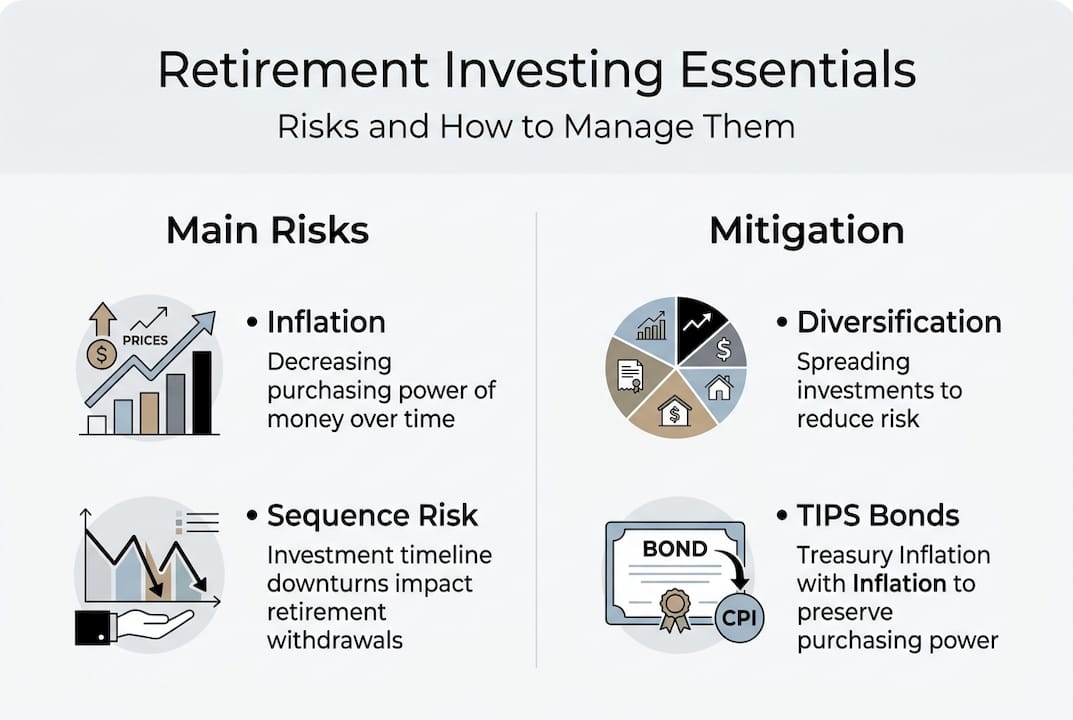

Sequence risk poses a real threat to retirement security. Market crashes early in retirement force you to sell assets at depressed prices, locking in losses and reducing future growth potential. This timing risk differs from average returns over your entire investing lifetime. Flexible spending strategies and maintaining adequate cash reserves help weather these storms without derailing your plan.

Inflation represents a silent wealth destroyer that many overlook. Even modest 3% annual inflation cuts purchasing power in half over 24 years. Unprotected cash savings lose value steadily. Strategic investing during inflation using Treasury Inflation-Protected Securities (TIPS) and diversified assets preserves your wealth’s real value.

Some voices advocate building cash-flow businesses instead of traditional retirement investing. While entrepreneurship offers rewards, data consistently shows that diversified investment portfolios outperform cash holdings over long periods. Business income can supplement retirement savings but shouldn’t replace systematic investing entirely.

| Investment Approach | Primary Advantage | Main Risk |

|---|---|---|

| Traditional portfolio investing | Proven long-term growth, liquidity | Market volatility |

| Cash-flow businesses | Active income control | Business failure, time intensive |

| Cash savings only | Safety, accessibility | Inflation erosion, minimal growth |

| Real estate investing | Tangible assets, income | Illiquidity, management burden |

Mitigation strategies protect your retirement investments from common threats. TIPS adjust principal with inflation, maintaining purchasing power automatically. Annuities provide guaranteed income streams that can’t be outlived. Flexible withdrawal strategies let you reduce spending during market downturns, preserving portfolio longevity.

Pro Tip: Maintain one to two years of living expenses in stable, liquid assets as you approach retirement. This buffer lets you avoid selling stocks during temporary market declines, protecting your sequence of returns risk exposure.

Behavioral inertia kills more retirement plans than market crashes. Many professionals know they should invest more but never take action. Analysis paralysis and fear of making wrong choices lead to dangerous delays. Starting with simple, automated investments beats perfect planning that never happens. Imperfect action today outperforms perfect inaction every time.

Applying investing principles to secure your retirement future

Only a small fraction of US workers reach recommended retirement savings targets. This statistic should motivate immediate action, not despair. You can change your trajectory starting today with disciplined execution of proven principles.

Follow these steps to build retirement security:

- Maximize employer 401(k) match immediately for free money

- Open an IRA to supplement workplace retirement accounts

- Automate monthly contributions to remove willpower from the equation

- Increase savings rate by 1% annually until reaching 15% or more

- Review asset allocation yearly and rebalance as needed

- Consult a financial advisor for personalized guidance

Prioritizing tax-advantaged accounts accelerates wealth building substantially. Understanding the nuances of 401(k) versus IRA accounts helps you optimize contributions and minimize tax burdens. Many professionals can contribute to both, maximizing annual savings limits and diversifying account types for retirement flexibility.

Disciplined, regular investing beats market timing attempts consistently. Dollar-cost averaging smooths purchase prices over time, buying more shares when prices drop and fewer when prices rise. This mechanical approach removes emotion and builds wealth steadily regardless of market conditions. Set it, forget it, and let compound interest work its magic.

Risk management requires ongoing attention as circumstances change. Young professionals can tolerate more volatility with decades until retirement. Those approaching retirement need greater stability and income focus. Adjusting your strategy over time aligns investments with your evolving needs and risk capacity.

Professional advice keeps you accountable and on track. Markets will test your resolve with inevitable downturns. Advisors provide perspective during chaos, preventing panic selling that destroys long-term returns. They also identify opportunities you might miss and optimize strategies as tax laws and personal situations evolve.

Key implementation principles:

- Start immediately, even with small amounts

- Increase contributions with raises and bonuses

- Avoid withdrawing funds before retirement

- Stay invested through market volatility

- Diversify across asset classes and accounts

- Review progress quarterly, adjust annually

Exploring early retirement strategies can inspire aggressive saving and investing. While not everyone wants to retire early, the principles of maximizing savings rates and optimizing investments benefit all retirement timelines. Higher savings rates create flexibility and security regardless of your target retirement age.

Explore more retirement investing resources

Building retirement security requires ongoing education and strategic action. The principles covered here provide a strong foundation, but deeper exploration helps you optimize your personal situation. Finblog offers comprehensive resources covering retirement accounts, investment strategies, risk management techniques, and financial planning guidance.

You’ll find expert articles explaining complex topics in accessible language, helping you make informed decisions about your financial future. From understanding different account types to navigating market volatility, these resources empower you to take control of your retirement planning with confidence.

Whether you’re just starting your career or approaching retirement, the right information at the right time makes all the difference. Explore our library of retirement investing content to discover strategies tailored to your stage of life and financial goals. Your future self will thank you for the time invested in financial education today.

FAQ

What is the best age to start investing for retirement?

The best age is right now, regardless of your current age. Starting in your twenties maximizes compound growth potential, turning modest contributions into substantial wealth over four decades. Even starting at 40 or 50 provides significant benefits compared to relying solely on Social Security. Every year of compound growth matters exponentially.

How do target date funds simplify retirement investing?

Target date funds automatically adjust your stock and bond allocation based on your expected retirement year. They start aggressive with higher stock exposure when you’re young, then gradually shift to conservative bonds as retirement approaches. This hands-off approach eliminates the need for manual rebalancing while following proven lifecycle investing principles that over 60% of investors now embrace.

Why is working with a financial advisor beneficial for retirement planning?

Financial advisors tailor strategies to your specific goals, risk tolerance, and life circumstances. They provide objective guidance during market volatility when emotions tempt poor decisions. Research shows clients working with CFP professionals report higher rates of comfortable retirement and significantly reduced financial stress compared to those managing investments alone.

Can investing during inflation protect my retirement savings?

Yes, strategic investing during inflation preserves purchasing power through TIPS and diversified assets that typically rise with prices. Stocks of companies that can pass costs to customers often maintain real value during inflationary periods. Combining inflation-protected securities with flexible spending strategies and diversified portfolios helps your retirement income maintain its buying power across decades.