Planning your retirement withdrawals can mean the difference between decades of comfort and the risk of running out of money too soon. Most people guess or rely on old rules of thumb. But studies now show that a 3.7% withdrawal rate is the new safe starting point for modern retirees, not the outdated 4% that so many expect. Rigid formulas are fading away and the smartest strategies today are flexible, tax-aware, and tailored to your personal situation.

Table of Contents

- Understanding Key Retirement Withdrawal Strategies

- Choosing The Best Strategy For Your Needs

- Tax-Smart Withdrawal Approaches For Investors

- Tips To Make Your Money Last Longer

Quick Summary

| Takeaway | Explanation |

|---|---|

| Strategically plan withdrawals | Effective withdrawal strategies enhance sustainability and financial security during retirement. |

| Consider tax-efficient sequences | Prioritize withdrawals to minimize tax liabilities and maximize retirement portfolio longevity. |

| Evaluate personal financial circumstances | Tailor withdrawal strategies to individual needs, including income sources and expenses. |

| Maintain a flexible approach | Adjust withdrawal strategies based on market changes and personal financial situations. |

| Optimize spending and investments | Control retirement expenses and manage investments to ensure longer-lasting funds. |

Understanding Key Retirement Withdrawal Strategies

Retirement withdrawal strategies are critical financial decisions that can significantly impact your long-term financial security. Navigating the complex landscape of retirement income requires a strategic approach that balances immediate financial needs with long-term sustainability.

The Importance of Strategic Withdrawal Planning

Retirement withdrawal strategies are not one-size-fits-all solutions. According to a Financial Services Review study, tax-efficient withdrawal sequencing can dramatically impact your portfolio’s longevity and overall financial health. Retirees must carefully consider multiple factors when developing their withdrawal approach.

The core challenge lies in creating a systematic approach that addresses several key objectives:

- Tax Optimization: Minimizing tax liabilities by strategically withdrawing from different account types

- Income Sustainability: Ensuring your savings last throughout retirement

- Flexibility: Maintaining the ability to adapt to changing financial circumstances

Recommended Withdrawal Approaches

Morningstar’s research suggests a starting safe withdrawal rate of 3.7%, which reflects updated return expectations for various asset classes. This recommendation highlights the importance of a nuanced approach to retirement income.

The Financial Planning Association provides additional insights into optimal withdrawal strategies. Their research indicates that retirees with higher guaranteed income sources can potentially increase their withdrawal rates and maintain more aggressive asset allocations. This approach requires careful analysis of individual financial situations, including:

- Social Security benefit optimization

- Pension income

- Investment portfolio composition

- Individual risk tolerance

Strategic Considerations for Withdrawal Planning

Successful retirement withdrawal strategies demand a comprehensive approach. Retirees should consider multiple factors beyond simple percentage-based withdrawals. This includes:

- Tax implications of withdrawals from different account types (traditional IRAs, Roth accounts, taxable investments)

- Required minimum distributions (RMDs)

- Potential impact on Social Security benefits

- Healthcare costs and potential long-term care expenses

The most effective retirement withdrawal strategies are dynamic and personalized. They require ongoing assessment and adjustment based on changing market conditions, personal circumstances, and financial goals. While general guidelines provide a starting point, individual retirement planning demands a tailored approach that considers your unique financial landscape.

Understanding and implementing robust retirement withdrawal strategies is not just about preserving wealth. It’s about creating a sustainable income stream that provides financial security and peace of mind throughout your retirement years.

Choosing the Best Strategy for Your Needs

Selecting the most appropriate retirement withdrawal strategy requires a comprehensive understanding of your unique financial landscape. No single approach works universally, making personalized planning crucial for sustainable retirement income.

Evaluating Withdrawal Strategy Options

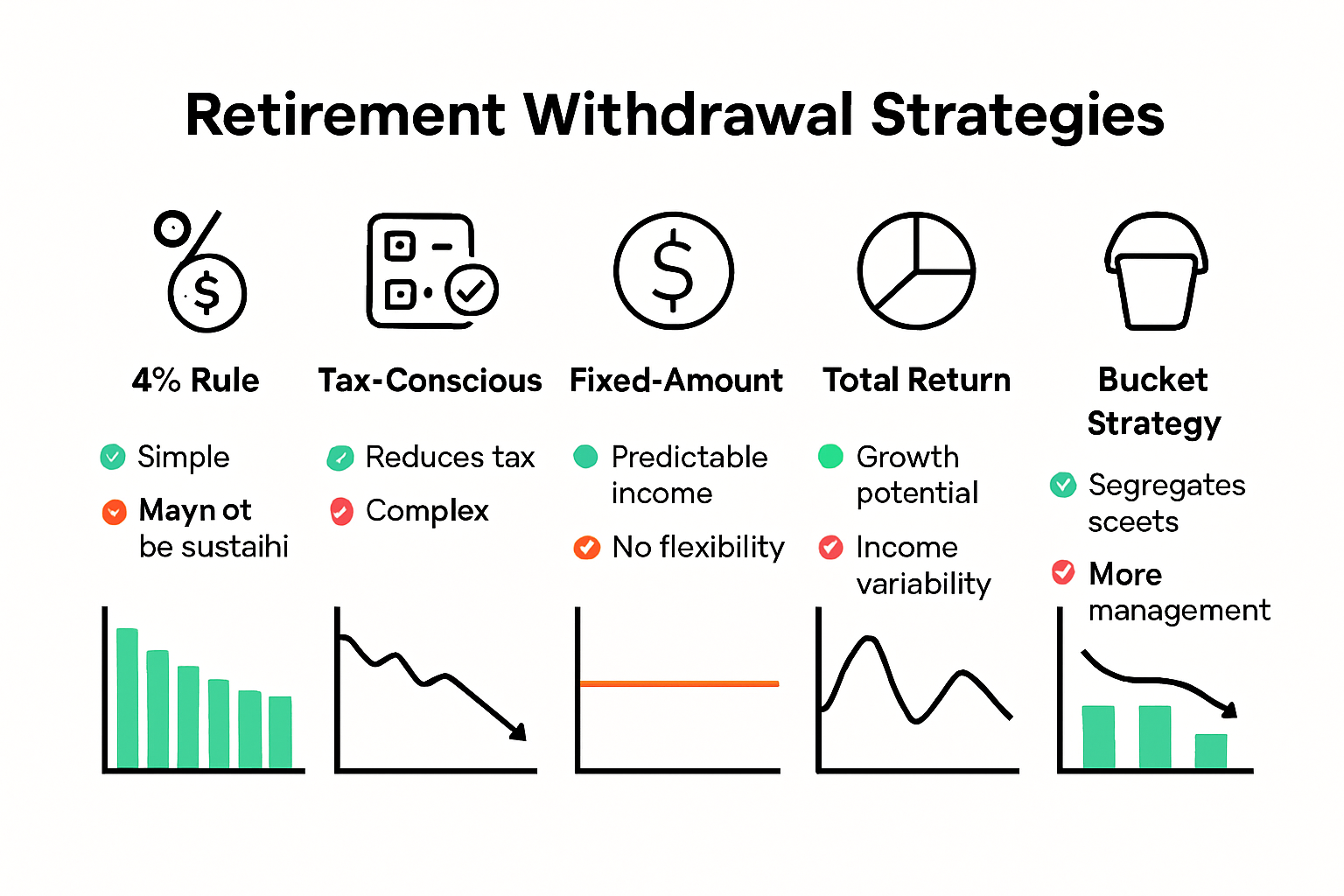

Research from the New York State Deferred Compensation Plan highlights seven distinct withdrawal strategies that retirees can consider. Each strategy presents unique advantages and potential challenges, demanding careful evaluation of individual financial circumstances.

Key strategies include:

To help you compare key retirement withdrawal strategies, the table below summarizes the main features, advantages, and considerations associated with each approach discussed in the article.

| Strategy | Key Features | Advantages | Considerations |

|---|---|---|---|

| 4% Rule | Withdraw 4% of portfolio annually | Simple, widely known | May not suit modern market returns; not flexible |

| Tax-Conscious Withdrawals | Prioritize minimizing tax liability | Can extend portfolio longevity | Requires tax knowledge and planning |

| Fixed-Amount Withdrawals | Withdraw a set dollar amount each year | Predictable income | May not adjust for inflation or market performance |

| Total Return Strategy | Adjust withdrawals based on returns | Responsive to market conditions | Income may fluctuate with performance |

| Bucket Strategy | Segment funds by time horizon | Balances short-term and long-term goals | Requires active management |

- 4% Rule: A traditional approach that suggests withdrawing 4% of your total portfolio annually

- Tax-Conscious Withdrawals: Strategically managing withdrawals to minimize tax liabilities

- Fixed-Amount Withdrawals: Maintaining consistent income regardless of market fluctuations

- Total Return Strategy: Using portfolio performance to determine withdrawal amounts

- Bucket Strategy: Segregating funds into different time-horizon investment pools

Adapting to Market Dynamics

Research from the EDHEC Climate Institute emphasizes the importance of flexible withdrawal strategies. Rigid approaches can expose retirees to significant risks associated with market volatility and changing personal circumstances.

Flexible strategies offer several critical advantages:

- Dynamic adjustment of withdrawal rates based on market performance

- Enhanced ability to manage unexpected financial challenges

- Reduced risk of portfolio depletion during market downturns

Advanced Considerations for Retirement Income

A comprehensive study by Milevsky and Young explores sophisticated retirement income strategies, particularly focusing on annuitization. Their research suggests that strategic integration of life annuities can provide additional financial security.

Key factors to consider when choosing your withdrawal strategy include:

- Current age and expected longevity

- Total retirement savings

- Anticipated expenses

- Risk tolerance

- Existing income sources like Social Security or pensions

The optimal retirement withdrawal strategy is not static. It requires periodic review and adjustment as your financial situation evolves. Consulting with a financial professional can help you develop a personalized approach that balances your immediate income needs with long-term financial sustainability.

Ultimately, the best strategy is one that provides consistent income, manages tax efficiency, and adapts to your changing life circumstances. By understanding the nuances of different withdrawal approaches, you can create a robust financial plan that supports your retirement goals.

Tax-Smart Withdrawal Approaches for Investors

Tax efficiency is a critical component of successful retirement withdrawal strategies. Minimizing tax liabilities can significantly extend the longevity of your retirement portfolio and maximize your available income during retirement years.

Understanding Tax-Efficient Withdrawal Sequencing

Research from the National Bureau of Economic Research reveals a strategic approach to withdrawing retirement funds that can optimize tax efficiency. The study suggests a specific order of withdrawals that can help investors minimize their tax burden and preserve more of their retirement savings.

The recommended withdrawal sequence typically follows this order:

For retirees aiming to minimize taxes and extend their retirement savings, the table below outlines the standard withdrawal order and why each step is recommended.

| Withdrawal Order | Account Type | Rationale |

|---|---|---|

| 1st | Taxable Accounts | Reduces ongoing taxable income and capital gains early |

| 2nd | Tax-Deferred Accounts | Defers taxes until withdrawals are required |

| 3rd | Roth Accounts | Preserves tax-free growth for the longest period |

- Taxable Accounts First: Begin by withdrawing from standard investment accounts

- Tax-Deferred Accounts Next: Utilize traditional IRAs and 401(k) accounts

- Roth Accounts Last: Preserve tax-free Roth accounts for later stages of retirement

Navigating Required Minimum Distributions

According to IRS guidelines, understanding required minimum distributions (RMDs) is crucial for tax-smart retirement planning. RMDs are mandatory withdrawals that begin at a specific age, typically 72, and can significantly impact your tax liability if not managed strategically.

Key considerations for RMD management include:

- Calculating precise RMD amounts based on account balance and life expectancy

- Timing withdrawals to minimize tax impact

- Exploring options for reducing RMD tax liability

Advanced Tax Optimization Strategies

Sophisticated investors can implement several advanced techniques to minimize tax exposure during retirement:

- Partial Roth conversions to manage annual tax liability

- Strategic charitable giving using qualified charitable distributions

- Timing withdrawals to stay within lower tax brackets

- Leveraging tax-loss harvesting in taxable accounts

Tax-smart withdrawal approaches require ongoing attention and periodic review. The tax landscape changes frequently, and individual financial situations evolve. What works best in one year may not be optimal in the next. This dynamic nature underscores the importance of flexible, personalized retirement withdrawal strategies.

Consulting with a tax professional or financial advisor can provide personalized insights tailored to your specific financial situation. They can help you navigate the complex landscape of retirement account withdrawals, ensuring you maximize tax efficiency while maintaining a sustainable income stream.

Remember that effective tax management is not about completely eliminating tax obligations, but about strategically minimizing them. By understanding the nuanced approaches to retirement account withdrawals, you can create a more robust and tax-efficient retirement income plan.

Tips to Make Your Money Last Longer

Extending the longevity of your retirement savings requires strategic planning, disciplined financial management, and proactive decision-making. Making your money last throughout retirement involves more than just careful withdrawals it demands a comprehensive approach to financial sustainability.

Strategic Portfolio Management

Managing your investment portfolio is crucial for ensuring long-term financial stability. Diversification remains a key strategy for protecting your retirement funds against market volatility. By spreading investments across different asset classes, you can potentially reduce risk and create more consistent returns.

Consider these portfolio management techniques:

- Asset Allocation: Balance stocks, bonds, and other investments based on your risk tolerance

- Regular Rebalancing: Periodically adjust your portfolio to maintain desired risk levels

- Low-Cost Investment Options: Minimize fees to preserve more of your retirement savings

Lifestyle and Spending Optimization

Controlling expenses plays a critical role in extending your retirement funds. Creating a sustainable spending plan that aligns with your available resources can significantly impact your financial longevity.

Key strategies for managing retirement expenses include:

- Developing a comprehensive budget

- Identifying and eliminating unnecessary expenses

- Exploring cost-effective living arrangements

- Considering part-time work or consulting opportunities

- Leveraging senior discounts and cost-saving programs

Advanced Financial Protection Strategies

Additional approaches can help protect and extend your retirement savings:

- Maintaining an emergency fund to cover unexpected expenses

- Considering supplemental income streams

- Exploring healthcare cost management options

- Investigating long-term care insurance

- Implementing tax-efficient withdrawal strategies

Delaying Social Security benefits can also provide a significant financial advantage. Each year you wait to claim benefits beyond your full retirement age increases your monthly payment, potentially providing a more robust income stream in later years.

Technology and financial tools can help you track and manage your retirement finances more effectively. Budgeting apps, investment tracking platforms, and retirement calculators offer valuable insights into your financial health and can help you make more informed decisions.

The key to making your money last longer is remaining flexible and adaptable. Your retirement strategy should evolve with changing personal circumstances, market conditions, and economic landscapes. Regular financial check-ups with a professional can help you stay on track and make necessary adjustments.

Remember that preserving your retirement funds is not about extreme frugality but about smart, intentional financial management. By implementing a holistic approach that combines strategic investments, careful spending, and proactive planning, you can create a more secure and sustainable retirement experience.

Frequently Asked Questions

What are the best withdrawal strategies for retirement?

Effective withdrawal strategies for retirement include the 4% rule, tax-conscious withdrawals, fixed-amount withdrawals, total return strategy, and the bucket strategy. Each has its own advantages and considerations that should align with your individual financial situation.

How can I optimize my retirement withdrawals for tax efficiency?

To optimize retirement withdrawals for tax efficiency, consider the order of withdrawals: start with taxable accounts, then tax-deferred accounts, and reserve Roth accounts for later. This approach helps minimize tax liabilities and prolong the longevity of your retirement portfolio.

What factors should I consider when choosing a retirement withdrawal strategy?

When selecting a retirement withdrawal strategy, consider factors such as your age, expected longevity, total retirement savings, anticipated expenses, risk tolerance, and existing income sources like Social Security or pensions. Personalizing your strategy is crucial for sustainability.

How often should I review my withdrawal strategy during retirement?

It’s advisable to review your withdrawal strategy at least annually or anytime there’s a significant change in your financial situation or market conditions. Regular assessments ensure that your approach remains aligned with your goals and can adapt to any changes in your circumstances.

Take Control of Your Retirement Income Strategy Today

Are you worried your savings might not last, or unsure how much you can safely withdraw without running out? Retirement planning is one of life’s biggest financial challenges. As explained in our article, the right withdrawal approach is crucial for balancing reliable income and tax efficiency. Many retirees feel anxious about unpredictable market changes, rising healthcare costs, and whether the old 4 percent rule still applies. If you want confidence in your financial future, you need a flexible strategy built for your unique circumstances.

Get actionable guidance tailored to your needs at finblog.com. Our secure platform provides expert tips, practical tools, and easy-to-understand resources drawn from the latest research on retirement withdrawal strategies. Take the next step by connecting with our trusted professionals through our streamlined, user-friendly consultation forms. Maximize your income and minimize your risks starting today. Visit finblog.com and gain the clarity and support you deserve for every stage of your retirement journey.