TL;DR:

- Building simple systems like automatic transfers and separate accounts reinforces good financial habits.

- A 30-minute financial snapshot helps clarify where your money truly goes.

- Automating and regularly reviewing finances safeguards against behavioral biases and impulsive spending.

Most young professionals know they should be saving more, spending smarter, and building toward something. But knowing and doing are two completely different things. The gap between financial intention and financial action is where most people get stuck, not because they lack discipline, but because they lack a system. Building lasting money habits isn’t about willpower or deprivation. It’s about creating simple structures that make the right choices automatic. This guide walks you through a practical, step-by-step framework designed for real life, real income, and the real psychological traps that derail even the most motivated people.

Table of Contents

- Identify your starting point: The 30-minute financial snapshot

- Divide and conquer: The 3-account system for easy money management

- Automate and safeguard: Building resilience with smart systems

- Troubleshoot your habits: Tactics for debt, variable income, and common pitfalls

- Confirm your progress: Simple checkpoints for lasting success

- Why most financial advice fails (and what actually sticks)

- Build your future: More financial success resources

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Assess your finances | A quick snapshot of income, expenses, and debts gives you a powerful starting point. |

| Simplify with systems | Dividing money into essentials, lifestyle, and savings buckets makes management almost automatic. |

| Automate everything | Set up transfers and payments on autopilot so habits require less effort. |

| Troubleshoot for real life | Handle debt, variable pay, and behavioral traps with tailored tactics, not just generic advice. |

| Check in and adjust | Brief, regular reviews keep your financial habits working as your life changes. |

Identify your starting point: The 30-minute financial snapshot

You can’t navigate without knowing where you are. That sounds obvious, but most people have a vague, optimistic sense of their finances rather than an accurate one. The good news? Getting clear takes less time than you think.

A 30-minute financial snapshot is exactly what it sounds like: a fast, honest look at your numbers. No judgment, no shame. Just data. Here’s what to pull together:

- Total monthly take-home income (after taxes and deductions)

- Fixed essential expenses (rent, utilities, insurance, loan minimums)

- Variable essential expenses (groceries, transportation, prescriptions)

- Discretionary spending (dining out, subscriptions, entertainment)

- Current debt balances and interest rates

- Savings and investment account balances

Once you have these numbers, the picture becomes clear fast. Most people discover they’re spending more in one or two categories than they realized, usually subscriptions or food.

| Category | What to include | Why it matters |

|---|---|---|

| Income | Salary, side income, freelance | Sets your ceiling |

| Fixed expenses | Rent, insurance, loan payments | Non-negotiable baseline |

| Variable expenses | Groceries, gas, utilities | Controllable with effort |

| Discretionary | Dining, entertainment, shopping | Biggest opportunity for change |

| Debt | Balances, interest rates | Shapes payoff strategy |

| Savings | Emergency fund, investments | Measures progress |

The most common mistake people make here is estimating instead of actually checking. Your memory is not a reliable financial tool. Log into your bank account, pull up three months of statements, and use real numbers. A budgeting step guide can help you organize this data into a workable plan once you have it.

Pro Tip: Apps like Mint, YNAB, or your bank’s built-in tools can auto-categorize transactions, cutting your snapshot time in half. Set it up once and let it run. Building essential financial habits starts with knowing your baseline, and technology makes that easier than ever.

Divide and conquer: The 3-account system for easy money management

With a clear picture of your finances, it’s time to put your money to work for you. The single biggest mistake people make with money management is keeping everything in one account. It creates confusion, temptation, and a false sense of security.

The 3-account bucket system solves this with elegant simplicity:

- Essentials account: Covers rent, utilities, insurance, and loan payments. This is your non-negotiable bucket.

- Lifestyle account: Covers dining, entertainment, clothing, and fun. When it’s empty, you’re done spending in that category for the month.

- Savings account: Covers emergency funds, investment contributions, and future goals. This one is off-limits for daily spending.

Here’s how the allocations might look across different income levels:

| Monthly take-home | Essentials (50%) | Lifestyle (20%) | Savings (30%) |

|---|---|---|---|

| $3,000 | $1,500 | $600 | $900 |

| $4,500 | $2,250 | $900 | $1,350 |

| $6,000 | $3,000 | $1,200 | $1,800 |

These percentages aren’t rigid rules. They’re starting points. If you’re carrying significant debt, you might shift more toward essentials temporarily. The key is that each account has a job, and you always know exactly what you have available for each purpose.

The biggest pitfall is mixing categories. When your fun money and your rent money live in the same account, every purchase feels like a negotiation. Separation removes that friction entirely. You can also build smart money habits faster when your system does the thinking for you.

Pro Tip: Set up automatic transfers on payday so money flows into each account before you can spend it. Pair this with setting financial priorities to make sure your allocations reflect what actually matters to you.

Automate and safeguard: Building resilience with smart systems

Setting up distinct accounts is the first step, but consistency requires more than organization. The real secret to lasting financial habits is removing willpower from the equation entirely.

Willpower is a limited resource. It gets depleted by stress, fatigue, and the hundred small decisions you make every day. Automation bypasses all of that. When your savings transfer happens automatically on payday, you never have to decide whether to save. It just happens.

Here’s how to build a resilient automated system:

- Schedule savings and investment contributions to transfer the same day your paycheck lands

- Set up automatic bill payments to avoid late fees and credit score damage

- Create calendar reminders for monthly financial reviews

- Use your bank’s alert system to flag unusual spending or low balances

One of the most underrated wealth-building habits is the 24-hour rule: before making any non-essential purchase over $30, wait a full day. This single rule eliminates a significant portion of impulse spending. The purchase either still makes sense tomorrow, or it doesn’t. Either way, you made a deliberate choice.

Here’s a stat worth sitting with: 64% of Americans overestimate their own financial capability. Overconfidence is one of the most dangerous financial traps because it makes you feel like you don’t need systems. You do. Everyone does. Consistent investment routines are what separate people who build wealth from people who intend to.

Troubleshoot your habits: Tactics for debt, variable income, and common pitfalls

Once your systems are running, you’re bound to hit a few speedbumps. Here’s how to handle them.

Dealing with debt: The instinct is to throw everything at debt immediately. But building a starter fund first before aggressively paying off high-interest debt gives you a safety net that prevents you from going back into debt the moment an unexpected expense hits. Start with $500 to $1,000 in an emergency fund, then redirect surplus to high-interest balances.

Variable income: Freelancers, contractors, and commission-based earners face a unique challenge. The strategy here is to cover fixed expenses first, then treat any surplus as savings rather than extra spending money. Lifestyle inflation, where your spending rises to match your income, is the fastest way to stay broke while earning more.

Psychological traps to watch for:

- Overconfidence bias: Believing your financial instincts are better than they are

- Resulting: Judging the quality of a financial decision by its outcome rather than the process behind it

- Action bias: Feeling like you need to constantly adjust your portfolio or strategy, even when staying the course is smarter

“Prospect theory and overconfidence disproportionately affect younger and less wealthy individuals, leading to riskier decisions and underestimating real financial vulnerability.”

These behavioral finance biases are not character flaws. They’re predictable patterns. Knowing they exist puts you ahead of most people. Pair that awareness with clear financial goal tips and you have a real edge.

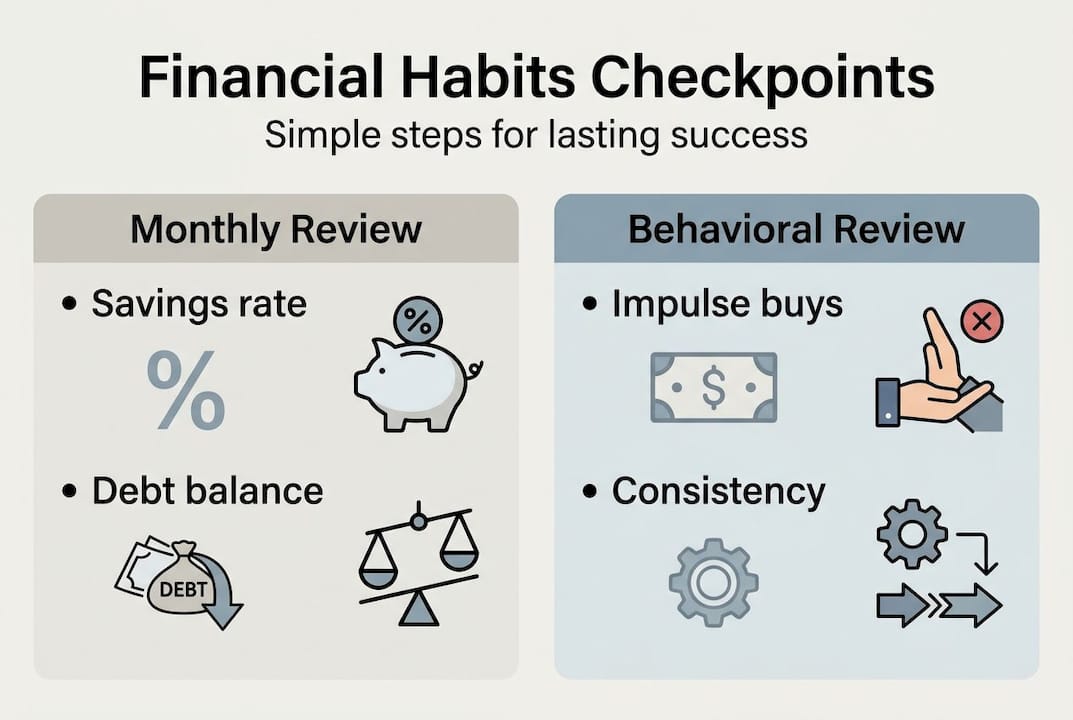

Confirm your progress: Simple checkpoints for lasting success

With systems and troubleshooting in place, it’s time to ensure your habits keep delivering results. A 10-minute monthly audit is all it takes to stay on track and catch small problems before they become big ones.

Here’s a simple numbered checkpoint routine:

- Check your savings rate: Are you hitting your target percentage each month?

- Review account balances: Is each bucket where it should be?

- Track debt progress: Are balances moving in the right direction?

- Assess goal milestones: Are you on pace for your 3, 6, and 12-month targets?

- Flag behavioral patterns: Did you dip into savings for non-emergencies?

Routine check-ins and behavioral review are what separate people who maintain habits from people who restart them every January. The goal isn’t perfection. It’s consistency over time.

| Checkpoint | Frequency | What to look for |

|---|---|---|

| Savings rate | Monthly | Meeting your target % |

| Debt balances | Monthly | Consistent reduction |

| Emergency fund | Quarterly | 3-6 months of expenses |

| Investment growth | Quarterly | Contributions + returns |

| Full financial review | Annually | Realign goals and allocations |

When you miss a month or overspend, don’t catastrophize. Adjust and move forward. Celebrate the fact that you have a system at all. Most people don’t. Learning how to budget effectively is an ongoing skill, not a one-time setup.

Why most financial advice fails (and what actually sticks)

Here’s something most financial content won’t tell you: the advice isn’t the problem. The delivery mechanism is.

Conventional financial advice assumes you’ll remember to save, remember to check your accounts, and remember to pause before spending. It treats financial success as a knowledge problem when it’s actually a design problem. You don’t need more information. You need better architecture.

The people who build real wealth over time aren’t necessarily the most disciplined. They’re the ones who built environments where the right choice is the easy choice. Automatic transfers. Separate accounts. Friction before impulse purchases. These aren’t hacks. They’re the actual mechanism.

Small, consistent actions also beat large, irregular ones every single time. Saving $200 every month for three years outperforms saving $1,000 twice a year, not just mathematically but psychologically. Consistency builds identity. And identity drives behavior far more reliably than motivation does.

The habits from wealthy people worth copying aren’t about sacrifice. They’re about systems that make the right behavior the default. Build the system first. The discipline follows naturally.

Build your future: More financial success resources

Want to keep leveling up your financial game? You now have the foundation: a clear snapshot of your finances, a three-account structure, automated systems, troubleshooting strategies, and a monthly review process. That’s more than most people ever put in place.

At FinBlog, we publish practical, no-fluff guides built specifically for professionals who are serious about building real wealth. Whether you’re just getting started or ready to go deeper, our library covers everything from behavioral finance to advanced investment strategy. Explore our smart money strategies to take your next step with confidence. The best financial decision you can make today is to keep going.

Frequently asked questions

What is the most important first step to start good financial habits?

The best first step is to track your income and spending so you know exactly where your money goes. A 30-minute financial snapshot gives you the real numbers you need to make informed decisions.

How do I stay consistent with savings?

Automate transfers into savings each payday to make saving effortless and consistent. When the transfer happens before you can spend the money, saving becomes automatic rather than optional.

What should I do first—pay off debt or save?

Build a starter emergency fund first, then pay off high-interest debt for the best balance of security and growth. Building a starter fund prevents you from cycling back into debt when unexpected costs arise.

What’s a practical system for handling impulsive spending?

Use a 24-hour rule for non-essential purchases over $30 to give yourself time to reconsider. This simple pause before purchasing eliminates a large portion of regret spending without requiring strict budgeting.

How can I avoid common behavioral traps with money?

Rely on automation instead of willpower and regularly review your decisions so biases don’t take over. Automating to remove willpower is one of the most effective defenses against overconfidence and impulse-driven financial mistakes.