TL;DR:

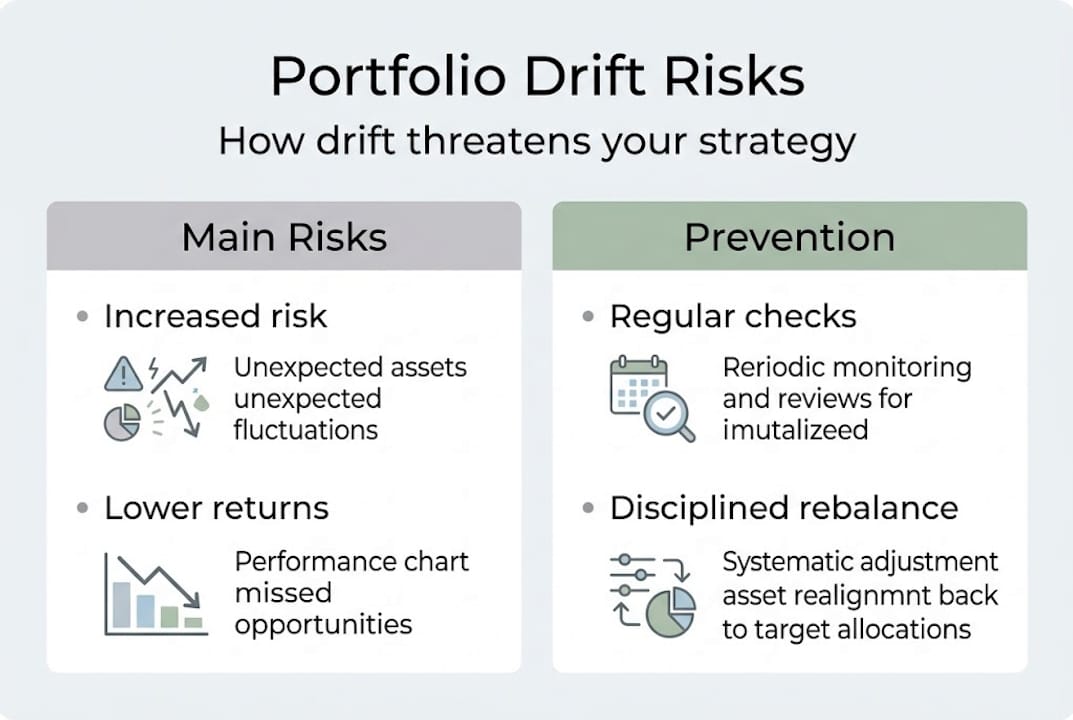

- Portfolio drift occurs quietly over time as assets grow at different rates, shifting your allocation.

- Regular rebalancing and automated tools can help maintain your original investment strategy.

- Ignoring drift increases risk, volatility, and can hinder long-term financial goals.

Most investors set an asset allocation once and assume it holds. It doesn’t. Over months and years, different assets grow at different rates, quietly pulling your portfolio away from the strategy you carefully designed. What started as a balanced 60/40 stock-to-bond mix can drift into something far riskier or far more conservative without a single deliberate change on your part. Portfolio drift is one of the most overlooked forces in long-term investing, and understanding it is the difference between staying on track and unknowingly working against your own financial goals. This guide breaks down exactly what it is, why it happens, and how to fix it.

Table of Contents

- What is portfolio drift?

- How does portfolio drift happen?

- Risks and consequences of unchecked portfolio drift

- How to identify and fix portfolio drift

- The truth about portfolio drift most investors ignore

- Take your investment strategy further

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Portfolio drift defined | Drift occurs when market shifts alter your portfolio’s asset allocation away from your original plan. |

| Risks of drift | Ignoring drift can increase risk and reduce your returns by misaligning with your investment goals. |

| Prevention and fixes | Regular monitoring and rebalancing—preferably automated—are the most effective ways to keep portfolio drift in check. |

| Expert perspective | Even seasoned investors underestimate drift’s speed and impact, but disciplined management makes a difference. |

What is portfolio drift?

Portfolio drift is the gradual shift in your asset allocation away from your original investment plan. It happens silently, without any action on your part, as individual assets appreciate or depreciate at different rates. One year your equities surge, and suddenly what was designed as a moderate-risk portfolio now carries heavy equity exposure you never intended.

As explained in our asset allocation guide, portfolio drift happens when your asset allocation changes due to market movements. The causes go beyond simple price changes, though. Compounding returns, dividend reinvestments, and differing volatility across asset classes all contribute. Over time, these small shifts stack up into meaningful structural changes.

Here’s what typically drives portfolio drift:

- Uneven asset returns: Stocks and bonds rarely move in lockstep, creating imbalances over time

- Market cycles: Bull runs in equities inflate their portfolio weight relative to fixed income

- Compounding: Assets with higher returns compound faster, widening allocation gaps

- Inaction: Skipping periodic reviews lets drift accumulate without correction

- Dividend reinvestment: Reinvesting into the same asset class can quietly tilt the balance

Many investors assume annual reviews are sufficient. In active markets, they often aren’t. A portfolio that looks balanced in January can drift noticeably by March after a strong equity rally or a bond selloff.

“The biggest risk isn’t always a single bad trade. Sometimes it’s the slow accumulation of misalignment between your portfolio and your actual risk tolerance.”

What makes drift especially dangerous is that it doesn’t trigger alerts. There’s no notification that your intended 60% equity allocation has crept to 72%. Your portfolio keeps working, just not the way you designed it. Unintended concentration in a volatile asset class exposes you to larger drawdowns than you planned for, while over-correction toward low-risk assets can mean your returns stall when growth is the goal.

How does portfolio drift happen?

With a solid definition in place, let’s walk through the real-world process of how drift occurs and how quickly it can take effect.

Market volatility causes asset values to change, leading to drift. The math is straightforward but the effects are easy to underestimate. Stocks and bonds respond differently to economic conditions, and even a single strong quarter in equities can tilt your allocation significantly.

Here’s a simplified example of how a portfolio drifts over one year:

| Asset class | Starting allocation | Starting value | Return | End value | End allocation |

|---|---|---|---|---|---|

| U.S. equities | 60% | $60,000 | +18% | $70,800 | 67.2% |

| Bonds | 30% | $30,000 | +2% | $30,600 | 29.0% |

| Cash/alternatives | 10% | $10,000 | +1% | $10,100 | 9.6% |

| Total | 100% | $100,000 | $111,500 | 100% |

In this scenario, equities gained more than seven percentage points of portfolio weight without a single trade. That’s meaningful drift in just twelve months. The dynamic asset allocation approach that professionals use accounts for exactly this kind of shift, adjusting proactively rather than reacting to large imbalances after the fact.

Here’s how drift typically compounds over multiple periods:

- Quarter 1: Equities outperform, slightly raising their weight

- Quarter 2: No rebalancing occurs; gains compound on a larger equity base

- Quarter 3: Bond prices dip slightly, further reducing their relative share

- Quarter 4: Equity weight is now 8 to 10 points above target without any deliberate change

Pro Tip: Set drift threshold bands around each asset class. For example, if equities drift more than 5% above their target weight, treat that as a rebalancing trigger. This keeps you responsive without overtrading.

Non-rebalancing accelerates the problem because it allows the compounding effect to widen the gap with every passing period. The longer you wait, the more significant the correction needed and the more potential tax exposure you may face when selling appreciated assets to rebalance.

Risks and consequences of unchecked portfolio drift

Understanding drift’s mechanisms, it’s vital to recognize why ignoring it could threaten your investment objectives.

Unmanaged portfolio drift increases overall portfolio risk and may lead to missed financial goals. The most common consequence is unintended equity concentration. When stocks outperform and you don’t rebalance, you end up holding more risk than your original plan anticipated. That’s fine in a bull market, but it amplifies losses when corrections arrive.

Here’s how a balanced and a drifted portfolio compare across scenarios:

| Scenario | Balanced portfolio (60/40) | Drifted portfolio (75/25) |

|---|---|---|

| Bull market return | +10.2% | +13.4% |

| Bear market loss | -12.5% | -18.7% |

| Recovery time | ~14 months | ~22 months |

| Volatility (standard deviation) | Moderate | High |

The drifted portfolio looks better during rallies, which is part of why investors resist rebalancing. But the downside is significantly steeper. And recovery from larger losses takes longer, cutting into long-term compounding.

The key risks of unchecked drift include:

- Excess volatility: Overweight equity positions swing harder in both directions

- Misaligned risk tolerance: Your portfolio no longer reflects what you actually can afford to lose

- Reduced diversification: Concentration in one asset class removes the cushion that diversification benefits are designed to provide

- Behavioral pitfalls: Watching losses mount on an overly aggressive portfolio can trigger panic selling, one of the most common financial planning mistakes investors make

53% of investors reduce risk by actively managing drift through disciplined rebalancing strategies. That’s not a marginal advantage. That’s the measurable difference between portfolios that endure market turbulence and those that get caught overexposed.

The opportunity cost is equally real. A portfolio that drifts too conservative, perhaps after a period of bond outperformance, may miss equity growth that was essential to meeting a retirement timeline. Drift cuts both ways.

How to identify and fix portfolio drift

Having detailed the risks, let’s move to practical strategies for keeping your portfolio in alignment and staying ahead of drift.

Regular rebalancing restores your intended asset allocation and manages drift. Here’s a step-by-step approach to detecting and correcting it:

- Pull your current allocation: Log into your brokerage or use an aggregator tool to see the real-time weight of each asset class

- Compare to your target: Side-by-side comparison reveals any drift beyond your acceptable threshold

- Identify the trigger: Determine whether drift is driven by equity gains, bond losses, or both, as the cause shapes your correction strategy

- Plan your rebalancing trades: Decide whether to sell overweight assets, redirect new contributions, or use a combination

- Execute and document: Record the rebalancing date, the trades made, and the resulting allocation for future reference

- Schedule the next review: Set a calendar reminder, quarterly at minimum

For tools, robo-advisors like Betterment and Wealthfront offer automatic rebalancing built into their platforms. Portfolio tracking software, including Personal Capital and Morningstar Portfolio Manager, lets you set drift alerts tied to your target allocation.

Pro Tip: Automate rebalancing wherever possible. Automation removes the emotional friction that causes most investors to delay corrections, especially when overweight assets are still performing well.

Professionals managing institutional portfolios often combine hedging strategies with routine rebalancing, using options or futures to limit downside during volatile periods while maintaining target allocations. For individual investors, the simpler approach of threshold-based rebalancing, informed by solid asset management explained principles, delivers strong results without complexity.

The truth about portfolio drift most investors ignore

Here’s something the standard advice rarely says out loud: most investors don’t rebalance because they don’t want to. Selling winners to buy underperformers feels psychologically wrong, even when it’s the rational move. This behavioral friction is why drift accumulates far faster in real portfolios than in theoretical models.

Manual rebalancing schedules fail more often than they succeed. Life intervenes, markets seem unsettled, and the task gets postponed. Automation isn’t a convenience, it’s the correction to a deeply human bias toward inertia.

There’s also a subtler issue: over-diversification. Some investors respond to drift concerns by adding more asset classes, believing broader holdings solve the alignment problem. They don’t. As explored in our analysis of when diversification backfires, spreading assets too thin can mask drift rather than address it. You can hold 40 positions and still be structurally overweight in one sector without realizing it.

The professionals who manage drift most effectively treat it as a systems problem, not a discipline problem. They build rules, automate triggers, and remove discretion from the rebalancing decision. That’s the framework worth adopting.

Take your investment strategy further

Portfolio drift is the kind of challenge that rewards the investors who stay informed and take a structured approach to management. At Finblog resource hub, you’ll find practical guides covering asset allocation, rebalancing strategies, risk management, and more, all built for investors who want expert-level insight without the jargon. Whether you’re refining your current strategy or building from the ground up, the tools and perspectives available here can help you keep your portfolio aligned with your actual goals. Explore the resources, apply the frameworks, and stay ahead of the drift that quietly undermines so many long-term investment plans.

Frequently asked questions

How often should I monitor for portfolio drift?

Regular monitoring is key to preventing significant drift; most experts recommend quarterly reviews or checks after major market events, though automated systems can handle this continuously.

Can portfolio drift increase my investment risk?

Yes. Portfolio drift increases risk and can impact financial performance by pushing your allocation beyond your intended risk tolerance without any deliberate action on your part.

What’s the best way to correct portfolio drift?

Rebalancing is the most effective fix. Regular rebalancing fixes drift and realigns your portfolio with your objectives; automated rebalancing tools make this process consistent and emotionally neutral.

Does market volatility affect portfolio drift?

Absolutely. Volatile markets create more drift, causing faster and more pronounced shifts in asset mix that require more frequent monitoring and potentially more aggressive correction strategies.

Recommended

- Why Portfolio Diversification Has Paid Off—but More Isn’t Always Better

- Investors Turn to New Strategy as Stocks and Bonds Fall Together

- Master Investing During Market Volatility for Lasting Results – Finblog

- Dynamic Asset Allocation Strategies for Volatile Markets – Finblog

- Is Your KiwiSaver Dropping, Or Are You Protected?