Most American investors think diversification solves all their financial worries, yet research shows over 65 percent still underestimate portfolio risk. Understanding what puts your money at risk is about more than just spreading investments around. With so many myths and misconceptions clouding judgment, this guide helps you separate fact from fiction so you can protect your hard-earned capital with a smarter, more realistic approach.

Table of Contents

- Portfolio Risk Defined And Common Myths

- Major Types Of Portfolio Risk Explained

- How Portfolio Risk Is Measured And Managed

- Real-World Portfolio Risk Scenarios

- Common Portfolio Risk Mistakes To Avoid

Key Takeaways

| Point | Details |

|---|---|

| Understanding Portfolio Risk | Portfolio risk includes firm-specific and market risks, affecting investment performance differently. Recognizing these distinctions aids in realistic investment strategies. |

| Importance of Diversification | Diversification reduces certain risks but does not eliminate all market risks. Investors should set realistic expectations and adapt their strategies accordingly. |

| Regular Portfolio Assessment | Conduct periodic reviews and reassess risk profiles every 6-12 months to align investments with evolving financial goals and market conditions. |

| Avoiding Common Pitfalls | Investors often misjudge risk by concentrating in high-volatility assets. A balanced approach, including low-volatility investments, can enhance overall portfolio performance. |

Portfolio Risk Defined and Common Myths

Investors frequently misunderstand portfolio risk, treating it as a monolithic concept when in reality it represents a nuanced framework of potential financial vulnerabilities. Portfolio risk management involves understanding how different types of risks interact and potentially impact investment performance.

At its core, portfolio risk encompasses two primary categories: firm-specific (diversifiable) risk and market (non-diversifiable) risk. Firm-specific risk relates to unique challenges affecting individual securities, such as management changes or company-specific financial issues. Market risk, conversely, represents broader economic factors that impact entire markets simultaneously, like economic recessions, geopolitical events, or significant interest rate shifts.

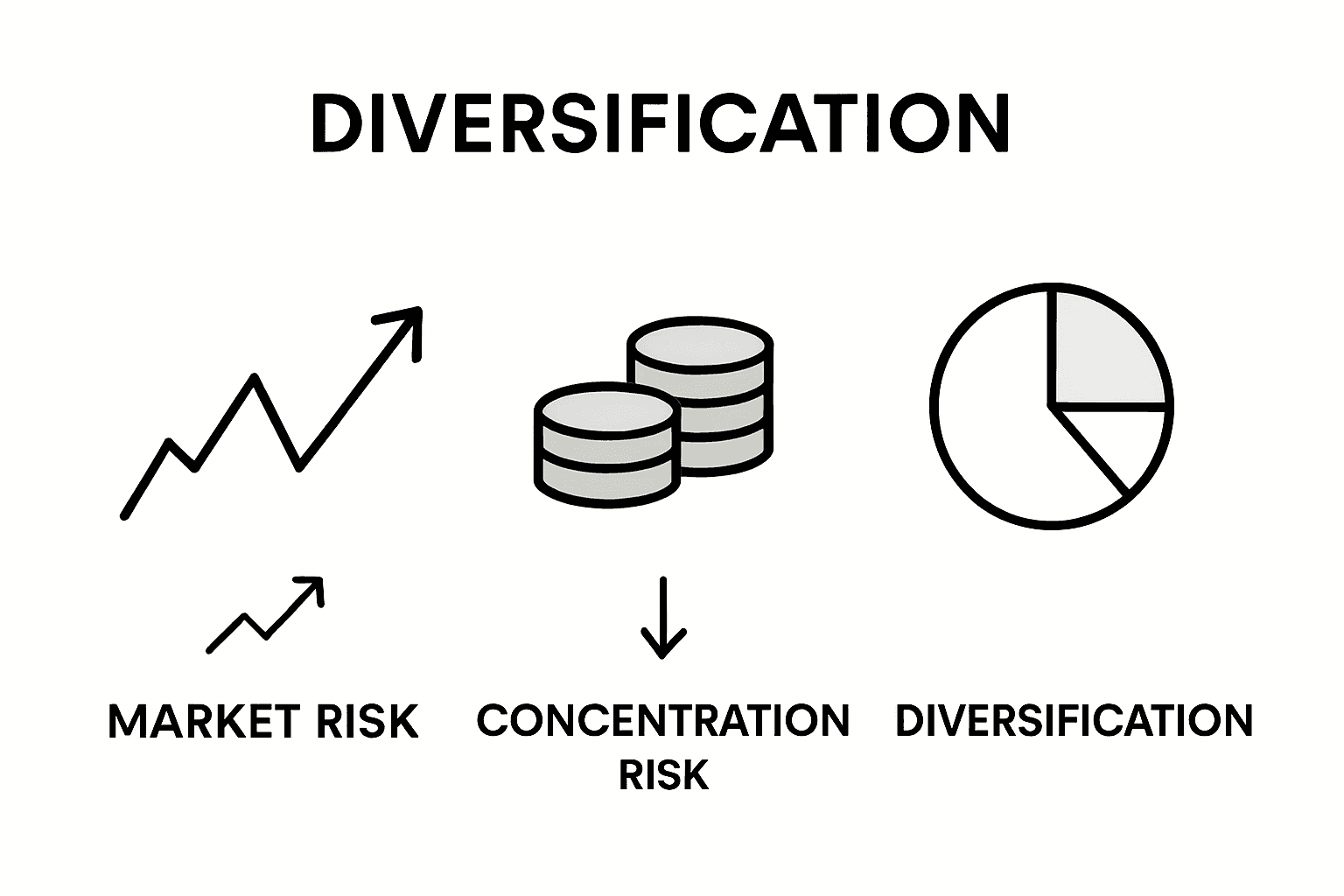

Common myths about portfolio risk can lead investors astray. Many believe that diversification automatically eliminates all investment risks. However, research demonstrates that while diversification can mitigate certain risks, it cannot completely neutralize market-wide systematic risks. Investors who understand this distinction can develop more realistic expectations and construct more robust investment strategies.

Pro Tip for Risk Management: Regularly reassess your portfolio’s risk profile every 6-12 months, paying close attention to changing market conditions and your personal financial goals. Periodic reviews help ensure your investment strategy remains aligned with your risk tolerance and evolving financial landscape.

Major Types of Portfolio Risk Explained

Investors navigating the complex financial landscape must understand the multifaceted nature of portfolio risks. Portfolio risk management encompasses several critical risk categories that can significantly impact investment performance and long-term financial strategies.

The primary types of portfolio risk include market risk, which represents potential losses due to overall market fluctuations, and credit risk, which reflects the possibility of default by investment counterparties. Additionally, investors must consider liquidity risk, which represents the potential inability to quickly convert investments into cash without substantial loss. Other significant risk types include operational risk (related to system failures or management issues), legal and regulatory risks, and business strategy risks that can unexpectedly disrupt investment performance.

Concentration risk presents another critical challenge for investors. This occurs when a portfolio becomes overly dependent on specific sectors, geographic regions, or individual securities. Research indicates that concentration risk can exponentially increase vulnerability to market shifts, making diversification a crucial risk mitigation strategy. Understanding these nuanced risk types allows investors to develop more sophisticated and resilient investment approaches that protect against potential financial downturns.

Pro Tip for Risk Assessment: Conduct a comprehensive portfolio risk audit annually, using quantitative metrics like standard deviation and Sharpe ratio to objectively evaluate your investment’s risk exposure and potential vulnerabilities.

Here’s a comparison of key portfolio risk types and their common triggers:

| Risk Type | Main Trigger | Potential Impact |

|---|---|---|

| Market Risk | Economic downturns, global crises | Broad losses across all holdings |

| Credit Risk | Counterparty default on obligations | Direct loss on affected securities |

| Liquidity Risk | Market freezes, low trading volumes | Forced sales at unfavorable prices |

| Concentration Risk | Overinvestment in one area | Amplified losses if sector declines |

| Operational Risk | System failures, fraud, poor control | Disrupted trading or value loss |

How Portfolio Risk Is Measured and Managed

Investors seeking to understand portfolio risk must leverage sophisticated measurement techniques that go beyond traditional approaches. Advanced risk analysis methodologies now incorporate big data analytics to provide more nuanced and dynamic risk assessments, enabling investors to develop more resilient investment strategies.

Traditionally, portfolio risk measurement relied on statistical models like the Mean-Variance Model, which evaluates potential returns against associated risks. Modern approaches have significantly expanded this framework, integrating complex computational techniques that analyze multiple financial variables simultaneously. Contemporary research revisiting Markowitz’s foundational work highlights the importance of understanding risk not just as a mathematical calculation, but as a dynamic, evolving concept that requires continuous monitoring and adaptive strategies.

Risk management involves several critical strategies, including diversification, asset allocation, and regular portfolio rebalancing. Investors can mitigate risks by spreading investments across different asset classes, sectors, and geographic regions. Quantitative risk measurement tools like standard deviation, beta coefficients, and Value at Risk (VaR) provide mathematical frameworks for understanding potential portfolio volatility. These metrics help investors quantify potential losses and make more informed investment decisions based on their individual risk tolerance.

Pro Tip for Risk Management: Implement a quarterly portfolio review process that systematically evaluates your investments’ performance against established risk benchmarks, allowing for proactive adjustments before potential market disruptions.

The table below offers a summary of quantitative methods used to measure portfolio risk:

| Method | What It Measures | Key Use Case |

|---|---|---|

| Standard Deviation | Portfolio return volatility | Assess potential performance swings |

| Beta Coefficient | Sensitivity to market movements | Identify risk relative to index |

| Sharpe Ratio | Risk-adjusted return efficiency | Compare portfolio performance |

| Value at Risk (VaR) | Potential maximum loss estimate | Simulate expected worst-case loss |

Real-World Portfolio Risk Scenarios

Investors face numerous complex risk scenarios that challenge traditional investment strategies and demand sophisticated risk management approaches. One particularly revealing example involves international investment patterns and regional investment biases, where investors tend to concentrate their portfolios within their home country, inadvertently increasing their overall financial vulnerability.

Consider a scenario where an investor allocates 80% of their portfolio to domestic stocks, believing local markets represent the safest investment strategy. This approach exposes the portfolio to significant concentration risk, making it vulnerable to country-specific economic downturns, regulatory changes, or localized market disruptions. Such myopic investment strategies can dramatically amplify potential losses, demonstrating how psychological biases like familiarity can lead to suboptimal risk management.

Another critical real-world risk scenario emerges during economic transitions or unexpected global events. The COVID-19 pandemic illustrated how quickly seemingly stable investment sectors could experience profound disruption. Technology stocks that appeared recession-proof experienced sudden volatility, while traditional industries like travel and hospitality faced unprecedented challenges. These scenarios underscore the importance of dynamic risk management, which requires continuous portfolio reassessment, sector diversification, and maintaining flexibility in investment allocations.

Pro Tip for Risk Navigation: Implement a 20-30% allocation to international and emerging market securities to naturally diversify your portfolio and reduce country-specific investment risks.

Common Portfolio Risk Mistakes to Avoid

Investors frequently fall prey to systemic risk management errors that can significantly undermine their long-term financial objectives. Understanding counterintuitive investment principles reveals that traditional assumptions about risk and return often fail to capture the complex realities of financial markets.

One critical mistake involves blindly pursuing high-risk investments under the misguided belief that greater risk automatically translates to higher returns. Contrary to popular perception, low-volatility securities can sometimes outperform their high-volatility counterparts. This phenomenon challenges the conventional wisdom that investors must accept substantial risk to generate meaningful investment gains. Many individuals mistakenly concentrate their portfolios in aggressive, high-risk assets without conducting comprehensive risk assessments or understanding the nuanced dynamics of market performance.

Tail risk scenarios represent another significant area where investors frequently miscalculate potential portfolio vulnerabilities. These rare but potentially catastrophic events can cause dramatic portfolio losses that standard risk models often fail to predict. Investors who neglect comprehensive risk analysis may find themselves exposed to extreme market conditions that can rapidly erode investment value. Common mistakes include overlooking systemic risks, failing to diversify adequately, and maintaining rigid investment strategies that cannot adapt to unexpected market disruptions.

Pro Tip for Risk Mitigation: Conduct an annual comprehensive portfolio stress test that simulates multiple market scenarios, including extreme events, to identify and address potential vulnerabilities before they can impact your investment performance.

Take Control of Your Portfolio Risk Today

Understanding the complex nature of portfolio risk is the first step toward protecting your investments from unexpected market shifts and concentration pitfalls. This article highlights critical challenges like market risk, concentration risk, and tail risk that many investors overlook. If you find yourself uncertain about how to regularly assess and adapt your portfolio’s risk profile, you are not alone. Many struggle with aligning their investment strategy to personal risk tolerance while navigating economic changes and diverse risk types.

At finblog.com, we specialize in helping serious investors like you transform these challenges into structured opportunities. Our expert insights and custom advisory services focus on practical risk management techniques including portfolio diversification, quantitative risk measurement, and dynamic rebalancing. Don’t leave your portfolio vulnerable to avoidable losses or missed growth potential. Start your journey with a personalized consultation today to implement resilient strategies based on the latest research and proven principles discussed throughout this article.

Explore our resources further and secure your financial future by visiting finblog.com. Let us help you master your portfolio risk before the next market change impacts your wealth.

Frequently Asked Questions

What is portfolio risk?

Portfolio risk refers to the potential financial vulnerabilities within an investment portfolio, encompassing both firm-specific (diversifiable) risk and market (non-diversifiable) risk that can impact investment performance.

How is portfolio risk measured?

Portfolio risk is measured using various quantitative methods such as standard deviation, beta coefficients, and Value at Risk (VaR). These metrics help assess potential volatility and losses in investment performance.

What are the major types of portfolio risk?

The major types of portfolio risk include market risk, credit risk, liquidity risk, operational risk, and concentration risk. Each type has distinct triggers and potential impacts on portfolio performance.

Why is diversification important in managing portfolio risk?

Diversification is important because it helps mitigate firm-specific risks by spreading investments across different asset classes, sectors, and geographic regions. However, it cannot eliminate market-wide risks entirely.