TL;DR:

- Effective spending prioritization involves allocating income first to essentials, then for savings and debt, before discretionary expenses. Using simple frameworks like the 50/30/20 rule or reverse budgeting helps ensure core needs are met and supports financial stability. Regular weekly reviews and strategic goal ranking maintain progress and adapt to life changes confidently.

Spending prioritization is the practice of allocating income to essential obligations first, then debt and savings, and finally discretionary expenses. This sequence protects your financial foundation before anything else gets funded. Frameworks like the 50/30/20 rule from Bank of America and NerdWallet’s must-pay-first approach give you a clear structure to follow. Learning how to prioritize spending is not about perfection. It is about making sure your most critical obligations are covered every single month, no matter what.

How to prioritize spending: start with essentials

The first rule of spending prioritization is simple: fund your non-negotiable expenses before anything else. Rent or mortgage, utilities, groceries, basic transportation, and insurance are the expenses that keep your household running. Skipping any of them creates a cascade of late fees, service shutoffs, and credit damage that costs far more to fix than to prevent.

Essentials fall into two groups. The first group is predictable monthly bills: rent, electricity, water, internet, and car insurance. The second group is predictable but irregular: annual insurance premiums, school fees, and routine medical costs. Both groups belong in your must-pay category. The mistake most people make is treating irregular essentials as optional until the bill arrives.

Separating fixed obligations from flexible spending is the single most effective way to prevent late payments and avoid borrowing to cover basics. When you know exactly what your essentials cost each month, you can see immediately whether your income covers them. If it does not, that is not a discipline problem. It signals a structural income gap that requires a bigger solution than cutting coffee.

Pro Tip: List every essential expense in a single column and total them before you budget anything else. This number is your financial floor. Every other spending decision happens above it.

- Rent or mortgage payment

- Utilities: electricity, gas, water, internet

- Groceries and household supplies

- Health, auto, and renters or homeowners insurance

- Minimum debt payments

- Basic transportation costs

Which budgeting framework works best for you?

Two frameworks dominate personal finance for good reason: the 50/30/20 rule and reverse budgeting. Each works differently, and the right choice depends on your income stability and financial goals.

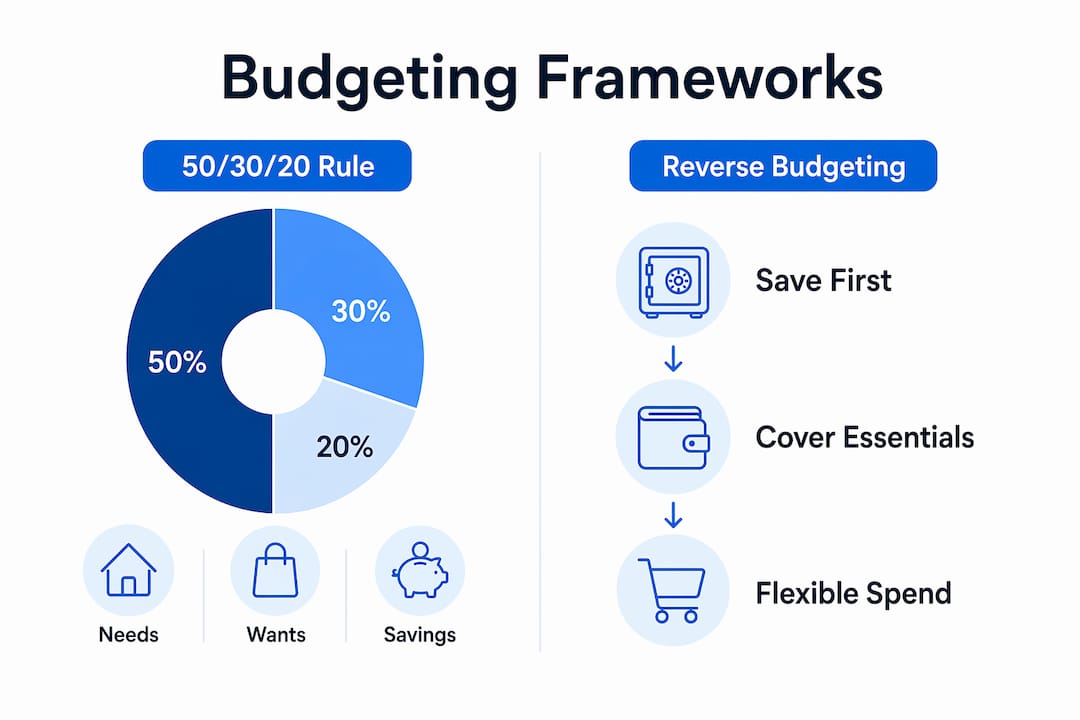

The 50/30/20 rule explained

The 50/30/20 framework allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Bank of America and NerdWallet both describe it as adjustable for high-cost-of-living areas where the 50% needs bucket may need to expand to 60% or more. The framework is useful because it gives every dollar a category without requiring you to track every purchase.

The weakness of 50/30/20 is that it assumes your income is large enough to cover all three buckets. For lower incomes, needs alone can consume 70% or more of take-home pay. In that case, the framework still works as a target, not a current reality.

Reverse budgeting: pay yourself first

Reverse budgeting sets aside savings the moment income arrives, before bills or lifestyle spending. The remainder covers everything else. This method reduces decision fatigue because you never have to decide whether to save this month. The transfer happens automatically. NerdWallet notes that pay-yourself-first budgeting is especially effective for people who find category-by-category tracking exhausting.

The tradeoff is that reverse budgeting requires enough income to cover essentials after the savings transfer. If your margins are tight, you may need to start with a small savings amount and scale up over time.

| Framework | Best For | Main Advantage | Main Limitation |

|---|---|---|---|

| 50/30/20 Rule | Stable income earners | Clear category structure | Fails at low income levels |

| Reverse Budgeting | Savings-focused individuals | Automates saving first | Requires income buffer |

| Cash Envelope Method | Overspenders on discretionary | Tactile spending control | Inconvenient for digital payments |

| Zero-Based Budgeting | Detail-oriented planners | Every dollar assigned | Time-intensive to maintain |

The best budgeting system is the one you will actually use month after month. Complexity is the enemy of consistency. Start with the simplest framework that covers your essentials and savings, then add detail only where overspending keeps happening.

Step-by-step guide to ranking your financial goals

Goal-based prioritization works as a ladder. You climb one rung before moving to the next. This sequence, validated by NerdWallet and Finhelp, prevents the common mistake of investing for retirement while carrying high-interest credit card debt.

-

Build a starter emergency fund. Save $500–$1,000 before anything else. This small buffer stops a car repair or medical bill from becoming credit card debt. Without it, every unexpected expense resets your financial progress.

-

Capture your full employer 401(k) match. Employer match contributions are an immediate 50–100% return on your contribution. No investment beats that. Fund this before paying extra on any debt.

-

Pay down high-interest debt. The goal prioritization framework from Finhelp targets debts above roughly 10–15% APR first. Credit cards typically charge 20–29% APR. Paying them off is the equivalent of earning that rate risk-free.

-

Grow your emergency fund to 3–6 months of essential expenses. Once high-interest debt is gone, build a full emergency fund covering your financial floor for three to six months. This is the buffer that keeps a job loss from becoming a financial crisis.

-

Increase retirement savings. After your emergency fund is solid and high-interest debt is cleared, direct more income toward a Roth IRA, traditional IRA, or additional 401(k) contributions. Compound growth rewards consistency over time.

-

Fund flexible lifestyle expenses last. Travel, dining out, subscriptions, and hobbies belong at the bottom of the ladder. They are the first category to reduce when income falls short.

Pro Tip: Automate steps 2 and 4 with direct deposit splits or automatic transfers. Automation removes the monthly decision and makes the behavior default rather than deliberate.

The ladder works because it ranks expenses by urgency and risk. Missing an employer match costs you free money. Carrying high-interest debt costs you compounding interest. Skipping a vacation costs you nothing financially. The sequence reflects that logic exactly.

When income falls short of covering all rungs, adjust flexible spending first. Must-pay-first budgeting protects essentials and minimum debt payments. Lifestyle spending absorbs the shortfall. This approach also reveals quickly whether the shortfall is temporary or structural, which determines whether you need to cut spending, increase income, or both.

How do you monitor and adjust spending priorities over time?

Tracking spending is not a one-time setup. It is a weekly practice that takes 15–30 minutes and prevents small overruns from becoming large problems. Investopedia recommends treating budget reviews like short training sessions: brief, regular, and focused on incremental improvement rather than perfection.

A practical workflow is to allocate income into broad categories first: needs, savings, and wants. Then drill down only into the categories where overspending occurs. This approach gives you a clear signal without micromanaging every purchase. Apps like Mint, YNAB (You Need a Budget), and Copilot Money connect directly to bank accounts and categorize transactions automatically, which cuts the manual work significantly.

Monthly reviews should answer three questions. Did essentials stay within budget? Did savings transfers happen as planned? Where did flexible spending exceed the target? Answering these three questions takes less time than most people expect and reveals patterns that are invisible when you only check your balance.

Overspending is part of learning, not a reason to abandon the budget. When a category runs over, adjust the next month rather than scrapping the system. Budgets that survive imperfect months are more valuable than perfect budgets that get abandoned after the first slip.

Common mistakes that derail spending priorities over time:

- Treating irregular expenses as surprises instead of planning for them monthly

- Reviewing spending only when something goes wrong instead of on a fixed schedule

- Cutting savings before cutting discretionary spending when income drops

- Setting a budget based on ideal income rather than actual take-home pay

- Ignoring common budgeting mistakes that quietly erode financial progress month after month

Adjusting your budget after a life change, such as a raise, a new expense, or a paid-off debt, is not a failure. It is the system working correctly. Finblog’s guide on when to update your financial plan covers the specific triggers that should prompt a full budget review.

Key takeaways

Effective spending prioritization means funding essentials and savings before any discretionary expense, using a consistent framework and regular reviews to stay on track.

| Point | Details |

|---|---|

| Essentials come first | Fund rent, utilities, groceries, and insurance before any other category. |

| Use a proven framework | The 50/30/20 rule or reverse budgeting gives every dollar a clear purpose. |

| Follow the priority ladder | Build an emergency fund, capture employer match, then tackle high-interest debt. |

| Review spending weekly | Spend 15–30 minutes per week tracking categories and adjusting where needed. |

| Adjust flexible spending first | When income falls short, cut discretionary expenses before touching savings. |

The uncomfortable truth about budgeting consistency

After years of watching people work through their finances, the pattern I see most often is not a lack of knowledge. Most people know they should save before they spend. The real problem is that budgets get built during a motivated moment and then ignored when life gets complicated.

The fix is not a better spreadsheet. It is a simpler system. I have found that people who separate their must-pay expenses into a dedicated account the day income arrives almost never miss an essential payment. The money is already gone from the spendable pool. That single habit does more for financial stability than any sophisticated budgeting app.

The other thing I would push back on is the idea that a budget needs to be perfect to be useful. A budget that covers essentials and moves some money to savings, even if the discretionary categories are rough estimates, beats a detailed budget that gets abandoned in week two. Understanding your personal priorities beyond what society expects you to spend on gives your budget a purpose that keeps you committed when motivation fades.

Start with the financial floor. Automate savings. Review once a week. Everything else is refinement.

— Povilas

Take control of your finances with Finblog

Finblog provides financial education and tools designed for people who want to build real stability, not just follow generic advice. Whether you are working through your first budget or refining a system that has stalled, the resources here cover the full range of effective spending habits and budgeting strategies. Explore Finblog’s guides on setting financial priorities and the best budgeting techniques to find the approach that fits your income and goals. If you are ready to connect with expert guidance tailored to your situation, Finblog is the starting point.

FAQ

What does it mean to prioritize spending?

Prioritizing spending means funding essential obligations like rent, utilities, and groceries first, then savings and debt, and finally discretionary expenses. This sequence protects financial stability before lifestyle spending gets any budget room.

What is the 50/30/20 rule for budgeting?

The 50/30/20 rule allocates 50% of after-tax income to needs, 30% to wants, and 20% to savings and debt repayment. Bank of America and NerdWallet both recommend adjusting the percentages for high-cost-of-living situations.

How much should i save in an emergency fund?

Start with $500–$1,000 as a starter fund, then build to 3–6 months of essential expenses. This range covers most job losses or medical emergencies without forcing you to take on new debt.

What should i cut first when money is tight?

Cut discretionary expenses first: dining out, subscriptions, entertainment, and travel. Essentials and minimum debt payments stay funded. Savings transfers can be reduced temporarily but should not be eliminated entirely.

How often should i review my budget?

Investopedia recommends 15–30 minutes per week for budget reviews. Monthly check-ins on category totals and a quarterly review of larger financial goals keep the system aligned with your actual income and priorities.