TL;DR:

- Cost of living adjustments (COLA) are designed to preserve purchasing power, not increase it, often leaving retirees and workers with limited real gains. The SSA calculates COLA mechanically using CPI-W data, but individual inflation experiences, such as healthcare and housing costs, often outpace official measures. Understanding how COLA impacts taxes, retirement accounts, and actual expenses enables better financial planning and salary negotiations.

Most people hear “cost of living adjustment” and assume their paycheck or benefit just got a real raise. It didn’t, necessarily. Cost of living adjustments (COLA) are designed to preserve purchasing power, not increase it. Yet millions of Americans misread COLA notices, negotiate salaries without understanding what portion is inflation-driven, and miss tax planning opportunities tied directly to annual inflation adjustments. This guide cuts through that confusion. You’ll learn exactly how COLA is calculated, what it actually does to your bottom line, and how to use it as a tool in your financial planning.

Table of Contents

- Key takeaways

- How cost of living adjustments are calculated

- How COLA affects retirement benefits and taxes

- What COLA doesn’t cover

- Using COLA in your financial planning

- COLA across sectors and programs

- My take on COLA and what most people miss

- How Finblog can help you stay ahead of COLA

- FAQ

Key takeaways

| Point | Details |

|---|---|

| COLA preserves, not grows, purchasing power | A 2.8% Social Security COLA for 2026 offsets inflation, but taxes and premiums can erase real gains. |

| CPI-W drives Social Security COLA | The SSA compares a three-month average of CPI-W across two years to set each year’s adjustment. |

| IRS limits adjust annually with inflation | For 2026, 401(k) contribution limits rise to $24,500, giving you more room for tax-advantaged savings. |

| Employers split merit and COLA raises | Average total salary increases for 2026 sit around 3.5%, but only part of that is inflation-based. |

| Personal inflation often outpaces official COLA | Healthcare and housing costs frequently rise faster than CPI-W, leaving real purchasing power behind. |

How cost of living adjustments are calculated

The Social Security Administration does not guess or negotiate COLA. The formula is mechanical. COLA equals the percentage increase between the average CPI-W (Consumer Price Index for Urban Wage Earners and Clerical Workers) for July through September of the current year versus the same three-month average from the prior year. That result gets rounded to the nearest tenth of a percent and applied to benefits beginning in January.

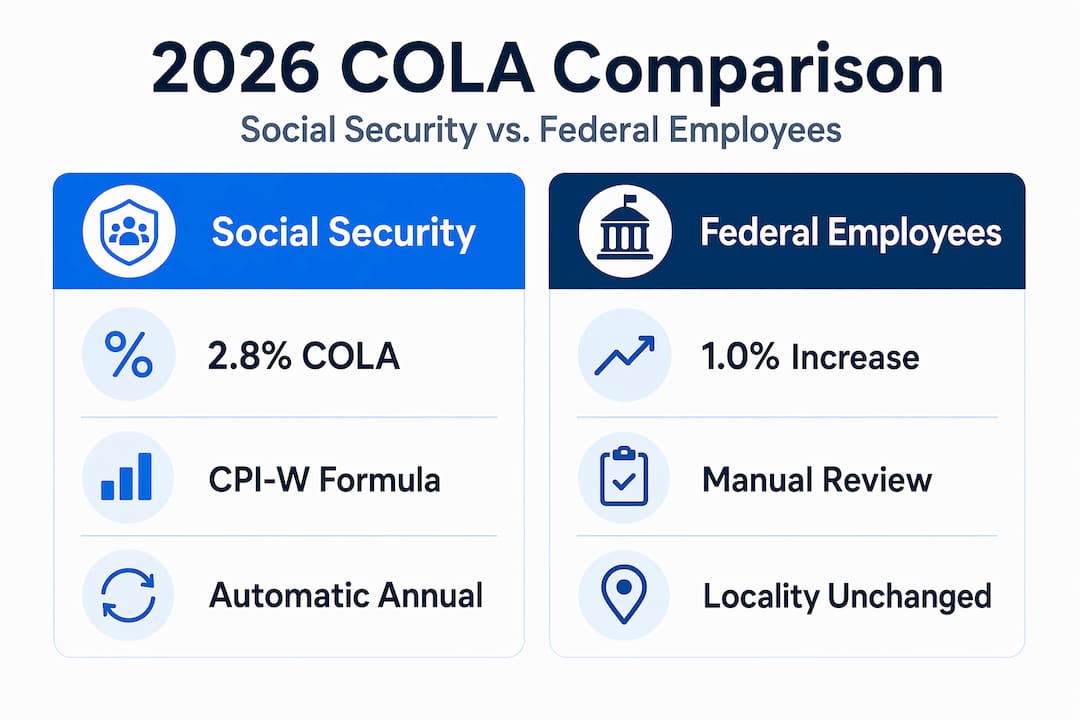

For 2026, that math produced a 2.8% COLA for Social Security and Supplemental Security Income (SSI) recipients. It’s automatic. Congress doesn’t vote on it. No one lobbies for it. It simply reflects what the index recorded.

Here’s where employers work differently. Private sector companies are not bound by CPI-W. Most plan 2026 salary increases at around 3.5% total, with merit-based increases averaging 3.2% and a separate, smaller COLA component layered on top. Some employers lump both into one number without distinguishing them. Others announce them separately on your pay stub.

Key differences between COLA sources:

- Social Security COLA is formula-driven, automatic, and tied strictly to CPI-W

- Federal civilian pay received a 1.0% across-the-board increase in January 2026, far below the Social Security adjustment

- Private employer COLA varies by company, industry, and individual compensation philosophy

- CPI-U (used by the IRS for tax bracket adjustments) covers a broader population than CPI-W and often produces slightly different figures

Pro Tip: Ask your HR department to break out what percentage of your annual raise is COLA-based versus merit-based. Those are two fundamentally different signals about your value to the company.

How COLA affects retirement benefits and taxes

This is where most people leave money on the table. COLA doesn’t just change your monthly Social Security check. It ripples through retirement accounts, tax brackets, and benefit program eligibility in ways that require active attention.

The IRS adjusts dozens of tax-related thresholds every year using its own inflation measures. For 2026, 401(k) elective deferrals increase to $24,500, which means you can shelter more income from taxes if you act on it. Most people don’t update their payroll deferral elections when these limits change, effectively forfeiting tax-advantaged space they’re entitled to. Updating your retirement account contributions each January takes about ten minutes and can save meaningful money over time.

Here’s a comparison of how COLA plays out differently for two common recipient profiles:

| Factor | Social Security retiree | Working employee |

|---|---|---|

| COLA source | SSA / CPI-W formula | Employer discretion |

| 2026 increase | 2.8% | ~3.5% total (merit + COLA) |

| Tax interaction | May push income into higher bracket | Increases taxable wages |

| Medicare premium offset | Part B premium increases reduce net gain | Not applicable |

| IRS limit benefit | Higher income may affect Roth eligibility | Higher 401(k) deferral room |

The Medicare Part B premium issue deserves specific attention. In years with moderate COLA increases, rising Part B premiums can consume a significant portion of the Social Security raise before beneficiaries see a dollar of it. Inflation adjustments don’t guarantee that net income will outpace inflation once taxes and premiums are accounted for. The headline number looks good. The deposit in your account may tell a different story.

Pro Tip: Run a quick net-benefit calculation each fall when COLA is announced. Subtract expected Medicare Part B premium increases and any change in your tax bracket exposure. That’s your actual raise, not the headline percentage.

The IRS also raised the wage threshold for Roth catch-up contributions to $150,000 for 2026 under the SECURE 2.0 Act. If you earn above that threshold and are over 50, your catch-up contributions must go into a Roth account rather than a traditional pre-tax one. That’s a policy change happening alongside COLA, and it affects your retirement savings strategy whether or not you’re tracking it.

What COLA doesn’t cover

Here’s the uncomfortable truth: the index that drives your Social Security COLA does not reflect what most retirees actually spend money on. CPI-W is built around the spending patterns of urban wage earners and clerical workers, not retirees. Healthcare costs, which tend to consume a growing share of retiree budgets, are often underweighted in CPI-W relative to what individuals actually experience.

COLA tied to CPI-W may not reflect housing and healthcare inflation in ways that matter most to older Americans. If your rent went up 7% and your medical costs rose 5%, a 2.8% COLA didn’t keep you whole. It kept the government’s math whole.

Consider these gaps COLA regularly fails to close:

- Housing costs in many metro areas are rising far faster than any broad CPI measure

- Out-of-pocket healthcare including prescriptions and dental is typically undercounted in official indices

- Insurance premiums for homeowners and auto coverage have surged in recent years, well beyond general inflation

- Food inflation hits lower-income households harder because they spend a greater share of income on groceries

“Wage growth often lags inflation depending on measurement nuances, making it critical to understand COLA in the context of wages for a real purchasing power assessment.”

The honest way to evaluate whether COLA is working for you personally is to track your own monthly expenses increase over the prior twelve months and compare that to your COLA percentage. If your personal inflation rate is running at 5% and your COLA was 2.8%, you need to find the other 2.2% somewhere else, through spending cuts, additional income, or drawing down savings faster than planned. That’s not a comfortable conclusion, but it’s the right framing.

Using COLA in your financial planning

Knowing how COLA works is one thing. Putting it to work is another. Here’s a practical approach to incorporating cost of living adjustments into your annual financial routine.

-

Set a COLA calendar reminder for October. The SSA typically announces the following year’s Social Security COLA in mid-October. This is also when IRS inflation-adjusted limits for retirement accounts tend to be released. Use that data immediately, not in April.

-

Update your 401(k) contribution rate. When the IRS raises the deferral limit, increase your contribution to capture the extra room. Updating contribution limits annually aligned with IRS COLA adjustments maximizes your tax-advantaged savings over time. If your employer uses a flat dollar amount rather than a percentage of salary, recalculate accordingly.

-

Separate your salary raise components. Employers vary in how they implement COLA, with some applying across-the-board inflation raises and others combining merit and COLA increases. Ask explicitly: “How much of this raise is COLA-based, and how much reflects my individual performance?” Knowing this shapes how you position yourself for next year’s review.

-

Benchmark your raise against actual inflation. If your employer offers a 2.5% raise in a year where your personal living costs rose 4%, you took a real pay cut. The Finblog guide on inflation and your savings walks through how to measure this properly.

-

Reassess your budget with realistic COLA expectations. Build your household budget assuming COLA covers roughly 60 to 70 percent of your actual cost of living increase. That conservative assumption motivates you to find savings or income elsewhere rather than assuming a government formula has you covered.

Pro Tip: If you’re within ten years of retirement, track both the Social Security COLA trend and the CPI-E (a separate index designed to reflect elderly spending patterns). Some policy proposals use CPI-E as the COLA basis, and the difference matters for long-range income projections.

COLA across sectors and programs

Not all cost of living adjustments are created equal, and the gap between programs is wider than most people realize.

| Program / Sector | 2026 COLA | Formula basis | Timing |

|---|---|---|---|

| Social Security / SSI | 2.8% | CPI-W Q3 average | January |

| Federal civilian pay | 1.0% across-the-board | Presidential / Congress | January |

| Private sector wages | ~3.5% total (varies) | Employer discretion | Varies |

| IRS tax brackets | Inflation-adjusted | CPI-U | Tax year start |

| Civil monetary penalties | CPI-U multiplier | Federal Register formula | January |

Federal civilian employees received a 1.0% across-the-board pay increase in January 2026, with locality pay levels unchanged. That’s less than a third of the Social Security COLA for the same year. The formula for civil monetary penalties uses a different index (CPI-U October data) with specific multipliers, showing just how fragmented the inflation adjustment system really is.

Social Security and SSI are the only programs with a fully automatic, formula-driven COLA. Everything else involves some degree of policy discretion, budget constraints, or employer judgment. That distinction matters because it makes Social Security one of the few genuinely inflation-linked income sources available to retirees.

My take on COLA and what most people miss

I’ve spent years watching people make the same mistake: they see the COLA announcement, feel relieved, and move on. That passive reaction is the problem.

In my experience, the most financially resilient people treat COLA not as a conclusion but as a starting point. They calculate their personal inflation rate, compare it to the official index, and identify the gap. Then they make deliberate decisions to close it, whether through higher retirement contributions, spending adjustments, or salary conversations grounded in data.

The contrarian view worth hearing: don’t expect your employer’s COLA component to reflect your actual cost of living increase. Employers use pay transparency laws and budget constraints, not your rent increase, as their primary inputs. I’ve found that employees who come to salary reviews with their own inflation data, not just company-provided figures, consistently negotiate better outcomes.

The deeper issue is the difference between nominal and real. Distinguishing nominal pay increases from real purchasing power requires using the same inflation index as the official COLA calculation, and most people never do this math. When you do, it often reveals that your real income has been flat or declining for years, even while the nominal number went up every January.

Understanding that clearly is not depressing. It’s clarifying. It tells you exactly what you need to do next.

— Povilas

How Finblog can help you stay ahead of COLA

Finblog publishes detailed, jargon-free guides built for people who want to act on financial information, not just understand it. If this article raised questions about how COLA interacts with your retirement accounts, the Finblog guide on IRA savings strategies breaks down how to maximize contributions as IRS limits shift. For tax planning around inflation adjustments, the resource on maximizing 2026 deductions covers bracket shifts and IRS changes in plain language. And if you’re a Social Security beneficiary figuring out how the 2026 COLA affects your overall income picture, the Social Security basics guide at Finblog is worth bookmarking for ongoing reference.

FAQ

What is a cost of living adjustment?

A cost of living adjustment is a change to wages, benefits, or income designed to offset inflation. It is typically calculated using a government price index like CPI-W or CPI-U.

How is the 2026 Social Security COLA calculated?

The SSA compares the average CPI-W for July through September 2025 against the same period in 2024. The resulting percentage increase, 2.8% for 2026, applies to benefits starting in January.

Does a COLA increase mean more spending power?

Not necessarily. After accounting for Medicare Part B premium increases and potential tax bracket creep, many beneficiaries see little to no real gain in actual purchasing power.

How does COLA affect my 401(k) contributions?

The IRS adjusts 401(k) contribution limits annually for inflation. For 2026, the elective deferral limit rises to $24,500, giving you more room to reduce taxable income through retirement savings.

How do I use COLA in a salary negotiation?

Ask your employer to separate the COLA and merit components of any raise offer. If the COLA portion is below actual inflation, use your own expense data to negotiate a higher merit-based increase on top of it.