TL;DR:

- IRAs offer tax-advantaged growth and investment flexibility for retirement savings.

- Choosing between Traditional and Roth IRAs depends on future tax rate expectations.

- Strategic use of contributions, rollovers, and withdrawals maximizes retirement wealth.

Most people know they should be saving for retirement, but the alphabet soup of IRA types, contribution limits, and withdrawal rules stops them cold. Traditional, Roth, SEP, SIMPLE — each comes with its own tax treatment and eligibility rules, and picking the wrong path can cost you thousands over time. The good news is that once you understand how IRAs actually work, the rules stop feeling overwhelming and start feeling like tools you can use. This guide walks you through everything: what IRAs are, how each type differs, how much you can contribute in 2026, and how advanced strategies can squeeze every dollar further.

Table of Contents

- What is an IRA and why does it matter?

- Key types of IRAs: Traditional vs Roth explained

- Contribution limits, eligibility, and income phase-outs in 2026

- Rollovers, conversions, and withdrawal rules

- Advanced IRA strategies: Maximizing your retirement success

- A fresh perspective: Why understanding IRA rules is your greatest asset

- Ready to take control of your retirement?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Tax advantages | IRAs offer either an upfront tax break or tax-free withdrawals, helping you grow more money for retirement. |

| Know your limits | Contribution limits and income phase-outs change yearly, so check them annually to maximize your input. |

| Penalty risks | Withdrawals before age 59½ may incur taxes and penalties unless you qualify for an exception. |

| Diversification strategy | Combining Traditional and Roth IRAs can provide more flexibility and tax diversity in retirement. |

| Consistent action | Regular contributions and smart withdrawal planning are key to long-term IRA success. |

What is an IRA and why does it matter?

An IRA, or Individual Retirement Arrangement, is a personal savings account with one major superpower: tax advantages. Unlike a regular brokerage account where you pay taxes on gains every year, an IRA lets your money grow in a more tax-efficient way. That difference, compounded over decades, can add up to tens of thousands of dollars.

As the IRS explains, IRAs are tax-advantaged savings plans that come in several forms: Traditional IRAs with tax-deductible contributions and taxable withdrawals, Roth IRAs with after-tax contributions and tax-free qualified withdrawals, and employer-focused options like SEP, SIMPLE, and Payroll Deduction IRAs. Each serves a different saver.

“Individual Retirement Arrangements allow ordinary Americans to build retirement wealth with meaningful tax protection — the type of account you choose shapes how and when the government takes its share.”

Understanding the difference between saving vs investing matters here too, because an IRA is technically an account wrapper, not an investment itself. You still choose what goes inside it, whether that is stocks, bonds, mutual funds, or ETFs.

Here is why IRAs matter for anyone building toward retirement:

- Tax-deferred or tax-free growth means your money compounds faster

- Flexibility to choose your own investments, unlike many employer plans

- Portability since the account belongs to you, not your employer

- Supplemental savings on top of a 401(k) or pension

- Estate planning benefits, especially with Roth IRAs

Think of an IRA as a container that changes how the government taxes what is inside it. The container matters just as much as what you put in.

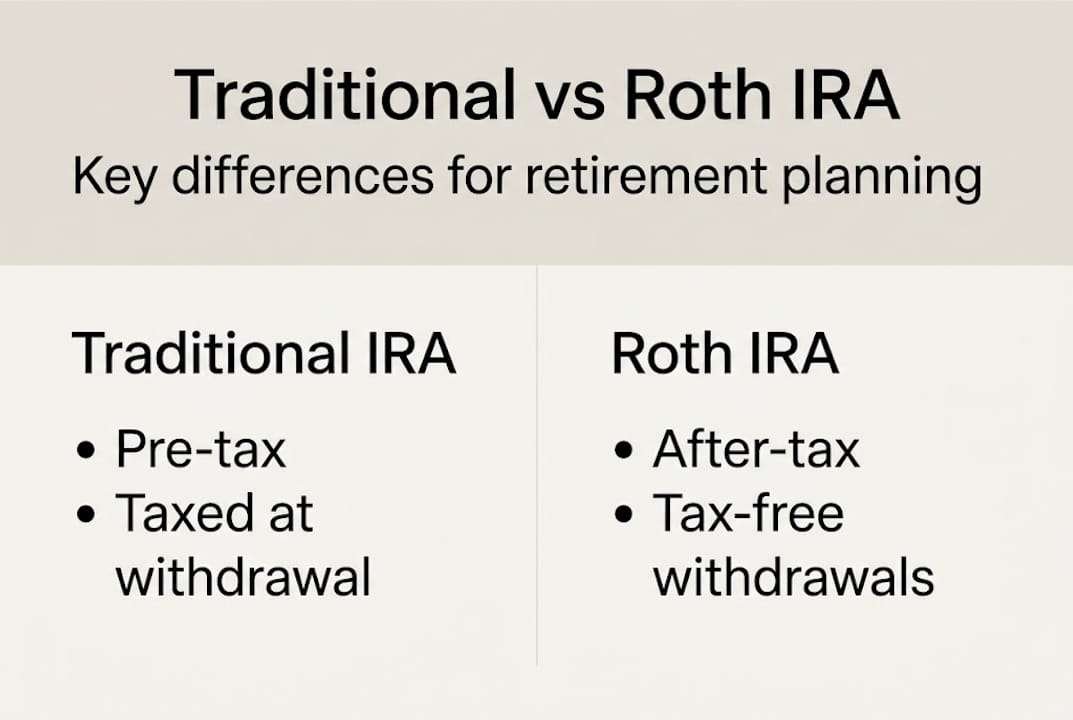

Key types of IRAs: Traditional vs Roth explained

Now that you know what IRAs are, let us see how each type works so you can choose the right fit for your situation.

The two most common types are the Traditional IRA and the Roth IRA. Both let your investments grow without annual taxes on dividends or capital gains. The key difference is when you get the tax break. Traditional IRAs offer tax-deductible contributions and taxable withdrawals in retirement, while Roth IRAs take after-tax money now and offer tax-free qualified withdrawals later.

| Feature | Traditional IRA | Roth IRA |

|---|---|---|

| Contribution type | Pre-tax (deductible) | After-tax |

| Tax on growth | Deferred | Tax-free |

| Withdrawals | Taxed as income | Tax-free if qualified |

| Required minimum distributions | Yes, starting at 73 or 75 | No RMDs during owner’s life |

| Income limits to contribute | None (deduction may be limited) | Yes, phase-outs apply |

| Early withdrawal penalty | 10% before age 59½ | Contributions can be withdrawn anytime |

Choosing between them comes down to one key question: will your tax rate be higher now or in retirement? If you expect to be in a lower bracket later, a Traditional IRA saves you money today. If you expect higher taxes in retirement, a Roth wins. You can read a deeper breakdown in our guide to choosing an IRA type.

Beyond these two, there are other types worth knowing:

- SEP IRA: Designed for self-employed people and small business owners, with much higher contribution limits

- SIMPLE IRA: For small businesses with 100 or fewer employees, includes employer matching

- Payroll Deduction IRA: Employees contribute directly from their paycheck to a Traditional or Roth IRA

For a broader look at how these stack up against 401(k)s and other vehicles, our retirement accounts comparison covers the full picture.

Pro Tip: If you are unsure which to pick, consider contributing to both. Using a Traditional IRA now and a Roth IRA later (or vice versa) gives you tax diversification, meaning flexibility to draw from different buckets in retirement based on your tax situation that year.

Contribution limits, eligibility, and income phase-outs in 2026

Understanding the differences is important, but knowing how much you can contribute and who is eligible is crucial for effective planning.

For 2026, the annual IRA contribution limit is $7,500 for most savers, or $8,600 if you are age 50 or older. That higher amount is called the catch-up contribution, and it exists specifically to help people who started saving later in life accelerate their progress. These limits apply combined across all your Traditional and Roth IRAs.

| Age group | 2026 contribution limit |

|---|---|

| Under 50 | $7,500 |

| Age 50 and older | $8,600 |

| SEP IRA (self-employed) | Up to 25% of compensation |

Key deadline: You have until April 15, 2027 to make your 2026 IRA contribution. That gives you extra time if cash flow is tight early in the year.

You must have earned income (wages, salary, self-employment income) to contribute. You cannot fund an IRA with investment income or Social Security payments alone. Also, your contribution cannot exceed your earned income for the year.

Income phase-outs matter for Roth IRA eligibility and Traditional IRA deductibility. Here is how to check your eligibility:

- Calculate your modified adjusted gross income (MAGI) for 2026

- Check if you or your spouse are covered by a workplace retirement plan

- Compare your MAGI to the IRS phase-out ranges for your filing status

- Determine whether your Roth contribution or Traditional deduction is reduced or eliminated

For 2026, Roth IRA contributions phase out for single filers between $150,000 and $165,000 MAGI, and for married filing jointly between $236,000 and $246,000. Traditional IRA deductibility phases out at lower thresholds if you have a workplace plan. Pairing your IRA with other tax-smart moves is covered in our guide to IRA deduction limits in 2026 and strategies for maximizing 2026 retirement contributions.

Rollovers, conversions, and withdrawal rules

Once you are clear on how much you can put in, you need to know how and when you can move or withdraw your money.

A rollover moves money from one retirement account to another, like from a 401(k) to a Traditional IRA when you leave a job. Done correctly, a rollover is not taxable. A conversion moves money from a Traditional IRA to a Roth IRA. You pay income tax on the converted amount now, but future growth is tax-free.

One popular advanced move is the backdoor Roth. High earners who exceed Roth income limits can contribute to a non-deductible Traditional IRA and then convert it to a Roth. The pro-rata rule applies if you have other pre-tax IRA balances, which can make part of the conversion taxable, so planning matters.

Withdrawals before age 59½ generally trigger a 10% early withdrawal penalty plus ordinary income taxes. But there are exceptions:

- First-time home purchase (up to $10,000 lifetime)

- Qualified higher education expenses

- Unreimbursed medical expenses above a threshold

- Disability or death

- Substantially equal periodic payments (SEPP)

For Required Minimum Distributions (RMDs), Traditional IRA owners must begin withdrawals at age 73 if born between 1951 and 1959, or age 75 if born in 1960 or later. RMDs are calculated using your prior December 31 account balance divided by an IRS life expectancy factor. Roth IRA owners face no RMDs during their lifetime, which is a powerful planning advantage.

“Roth IRAs have no required minimum distributions during the account owner’s lifetime, making them an exceptional tool for both retirement income flexibility and estate planning.”

Pro Tip: Plan your withdrawals to avoid stacking income into a higher tax bracket. Drawing from a Roth IRA in a high-income year, and a Traditional IRA in a low-income year, can save you real money. Our guide to IRA withdrawal strategies walks through this in detail.

Advanced IRA strategies: Maximizing your retirement success

With the basics covered, let us take it to the next level: how savvy retirees maximize every IRA advantage.

One often-overlooked area is asset location. Not all investments belong in the same account. High-growth assets like small-cap stocks or REITs are often better placed inside a Roth IRA, where gains are never taxed. Bonds or dividend-heavy funds may work better in a Traditional IRA or taxable account, depending on your overall picture.

Inherited IRA rules changed significantly after 2019. Non-spouse beneficiaries must now empty inherited IRAs within 10 years of the original owner’s death. Exceptions apply for surviving spouses, minor children, disabled individuals, and those not more than 10 years younger than the deceased. This rule has major tax implications if you inherit a large IRA.

Withdrawal coordination is another powerful tool. By timing withdrawals to stay within lower tax brackets, you can reduce your lifetime tax bill significantly. This often means drawing down Traditional IRA balances before RMDs kick in, especially in years when your income is lower. Coordinating this with Social Security timing adds another layer of optimization.

Here are key strategies worth building into your plan:

- Contribute consistently, even in small amounts, and let compounding do the work

- Use Roth conversions in low-income years to reduce future RMD burdens

- Place tax-inefficient assets in tax-sheltered accounts

- Coordinate IRA withdrawals with Social Security to minimize taxes on benefits

- Review beneficiary designations annually

Choosing Traditional if you expect a lower tax bracket in retirement, Roth if you expect a higher one, or both for tax diversification, is the core framework most financial planners use.

Pro Tip: Consistency beats everything. Missing even one year of contributions can cost you more than a decade of subpar returns. Automate your IRA contributions so they happen without you having to think about it. For more depth, see our guide on optimizing retirement savings.

A fresh perspective: Why understanding IRA rules is your greatest asset

Here is something most retirement articles will not tell you: the biggest returns in your IRA will not come from picking the right stock. They will come from understanding the rules well enough to use them strategically.

Most people spend enormous energy worrying about market performance, chasing returns, or waiting for the “perfect” time to invest. That energy is largely wasted. The best retirement accounts are not the ones with the highest-performing funds. They are the ones used consistently, with smart tax decisions made along the way.

The real edge comes from knowing when to convert, when to withdraw, how to layer accounts, and how to keep more of what you earn by minimizing unnecessary taxes. A person who contributes $7,500 every year to a Roth IRA starting at 35 will almost certainly outperform someone who contributes sporadically but picks “better” funds.

“Discipline and tax awareness compound just like interest. The investor who understands the rules wins more often than the investor who chases performance.”

Simple, consistent action beats complex schemes. Start now, contribute regularly, and revisit your strategy as your income and tax situation change.

Ready to take control of your retirement?

Armed with practical knowledge, you are ready to make confident moves toward a more secure retirement. Understanding how IRAs work is just the beginning. The next step is putting that knowledge into a plan that fits your income, your goals, and your timeline.

At Finblog, we publish practical, no-fluff guides designed to help you make smarter decisions with your money. Whether you are just opening your first IRA or looking to fine-tune an existing strategy, our resources meet you where you are. Start by exploring our full guide to optimizing your retirement strategy and take the next step toward building the retirement you actually want.

Frequently asked questions

Can I have both a Traditional and a Roth IRA?

Yes, you can own both types, but your combined contributions cannot exceed the annual limit ($7,500 or $8,600 if 50 or older) across both accounts in a single year.

What is the penalty for withdrawing from an IRA before age 59½?

Generally, early withdrawals trigger a 10% penalty plus ordinary income taxes, though exceptions exist for first-time home purchases, qualified education expenses, and certain medical costs.

How do required minimum distributions (RMDs) work for IRAs?

Traditional IRA owners must begin RMDs at age 73 or 75 depending on birth year, while Roth IRA owners face no RMDs during their lifetime, giving Roth accounts a significant flexibility advantage.

Who can contribute to an IRA in 2026?

Anyone with earned income up to the contribution limit can contribute, though income phase-outs may reduce or eliminate Roth IRA eligibility or Traditional IRA deductibility for higher earners.