TL;DR:

- Life insurance guarantees a tax-free payout to beneficiaries upon the policyholder’s death in exchange for regular premiums. It provides financial protection by covering debts, income replacement, and future expenses like education or final costs, offering peace of mind and financial stability. The main types are term and permanent insurance, with early purchase securing lower premiums and better long-term coverage options.

Life insurance is a contract between a policyholder and an insurance company that guarantees a financial payout to named beneficiaries upon the policyholder’s death in exchange for regular premium payments. That payout, called the death benefit, arrives tax-free to beneficiaries and can cover a mortgage, replace lost income, fund a child’s education, or handle final expenses. Providers like New York Life and Liberty Mutual have built entire product lines around this core promise. For anyone between 25 and 45 building a financial life, understanding what life insurance covers and how it works is one of the most practical steps you can take toward protecting the people who depend on you.

What is life insurance and why does it matter?

Life insurance is a legally binding agreement where you pay premiums and your insurer pays a set amount to your chosen beneficiaries when you die. The policy details specify the benefit amount, premium schedule, and any conditions or exclusions. The importance of life insurance comes down to one simple reality: your income stops when you die, but your family’s financial obligations do not.

A $500,000 death benefit can replace several years of income, pay off a home loan, and still leave funds for college tuition. That kind of financial buffer gives your family time to adjust without being forced into immediate financial decisions under grief. New York Life describes this as ensuring family financial stability during transitions, which is exactly the right framing for anyone with dependents or shared debt.

Life insurance also carries a psychological value that rarely gets discussed. Knowing your family is covered changes how you approach risk, career decisions, and long-term planning. It is not just a financial product. It is a foundation.

What are the main types of life insurance?

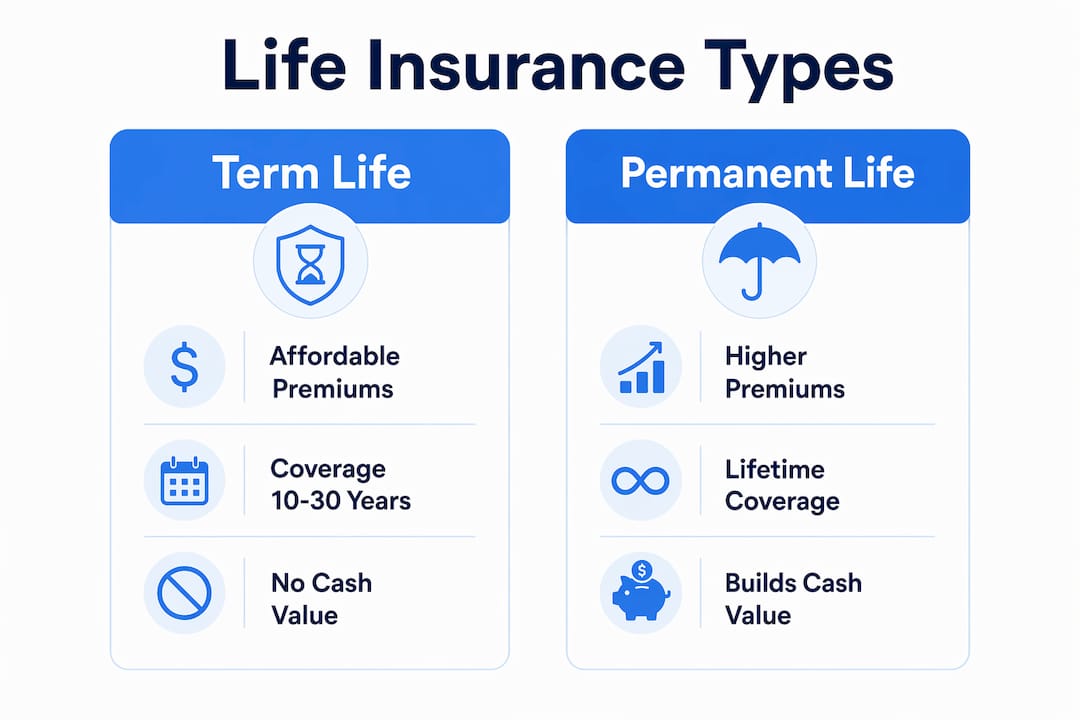

The two primary categories of life insurance are term life and permanent life insurance. Every other product you encounter is a variation of one of these two structures.

Term life insurance

Term life covers a specific period, typically 10, 20, or 30 years. If you die within that term, your beneficiaries receive the death benefit. If you outlive the term, the coverage ends with no payout. Term life is the most affordable option, which makes it the default choice for young families who need maximum coverage at the lowest cost.

Permanent life insurance

Permanent life insurance covers you for your entire lifetime and includes a cash value component that grows over time. The three most common subtypes are whole life, universal life, and final expense insurance. Whole life offers fixed premiums and guaranteed cash value growth. Universal life allows flexible premiums but requires active monitoring because universal life premiums can fluctuate, and a drop in cash value can put the policy at risk. Final expense insurance is a smaller permanent policy designed to cover burial and end-of-life costs.

Cost differences between these types are significant. Monthly premiums range from $30–$100 for final expense policies, $150–$400 for universal life, and up to $600 for variable life. Term life for a healthy 30-year-old typically runs well under $50 per month for a $500,000 policy. That gap reflects the added features and lifelong coverage permanent policies provide.

| Type | Coverage Period | Monthly Cost Range | Cash Value |

|---|---|---|---|

| Term Life | 10–30 years | $20–$50 | No |

| Whole Life | Lifetime | $200–$500 | Yes, fixed growth |

| Universal Life | Lifetime | $150–$400 | Yes, flexible |

| Final Expense | Lifetime | $30–$100 | Yes, minimal |

| Variable Life | Lifetime | Up to $600 | Yes, market-linked |

Pro Tip: Match your policy type to your life stage. A 28-year-old with a new mortgage and two kids needs affordable term coverage now. A 42-year-old with a paid-off home and estate planning goals benefits more from a permanent policy.

How does life insurance work in practice?

Life insurance works through a straightforward exchange: you pay premiums, and your insurer accepts the financial risk of your death. The mechanics behind that exchange are worth understanding before you sign anything.

Premiums and underwriting. Your premium is calculated based on your age, health, lifestyle, and the coverage amount you select. A 30-year-old nonsmoker in good health pays far less than a 50-year-old with a chronic condition. Buying earlier secures lower premiums and locks in long-term savings. Even a five-year delay can meaningfully increase your monthly cost for the same coverage.

The claims process. When the insured person dies, beneficiaries file a claim with the insurer and provide a death certificate. The insurer reviews the claim and, if approved, issues the death benefit. Most claims are paid within 30 to 60 days. The payout is not subject to federal income tax in most cases, which means your beneficiaries receive the full amount.

Living benefits. Modern policies now include living benefits that allow you to access part of your death benefit while still alive if you are diagnosed with a terminal, chronic, or critical illness. Liberty Mutual, for example, offers accelerated death benefit riders that let policyholders draw funds for medical care or living expenses. This feature transforms life insurance from a purely posthumous tool into one that can support you during a serious health crisis.

Cash value access. Permanent policies build cash value that grows tax-deferred and can be borrowed against. You can take a policy loan or make a partial withdrawal to fund a home purchase, business investment, or emergency. The catch: unpaid loans reduce your death benefit, and mismanagement can trigger taxes or cause the policy to lapse.

Pro Tip: If your only coverage is through your employer, you are more exposed than you think. Employer-provided life insurance typically ends when you leave the job. A personal policy travels with you regardless of where you work.

What are the key benefits of life insurance for financial planning?

The benefits of life insurance extend well beyond the death benefit. For anyone in the 25–45 age range building wealth and managing obligations, a policy can serve multiple financial planning functions at once.

- Income replacement. If you earn $80,000 per year and die unexpectedly, your family loses that income stream. A properly sized death benefit replaces years of earnings, giving your household time to stabilize.

- Debt coverage. Mortgages, car loans, student debt, and credit card balances do not disappear when you die. Your estate or co-signers may be responsible. A death benefit can clear those obligations immediately.

- Education funding. Parents with young children often size their death benefit to include projected college costs. A $1 million policy for a 32-year-old parent is not excessive when you factor in a 20-year mortgage, two kids, and a spouse who would need to rebuild financially.

- Estate planning and wealth transfer. Permanent life insurance integrates directly into estate planning strategies because the death benefit passes outside of probate. That means faster, private transfer of wealth to your heirs. Guardian Life notes that permanent policies can serve as tax-efficient estate assets when structured correctly.

- Tax advantages. The cash value in a permanent policy grows tax-deferred. You can access it through loans without triggering income tax in most scenarios. This makes permanent life insurance a complement to other tax-efficient investing strategies for high earners.

- Peace of mind. This one is underrated. Knowing your family is financially protected changes your relationship with risk. You make clearer career and investment decisions when you are not operating from financial anxiety.

How do you choose the right life insurance coverage?

Choosing the right policy starts with an honest assessment of what your family would need if your income disappeared tomorrow. The right coverage amount and type depend on your specific obligations, not a generic rule of thumb.

Consider these factors when sizing your coverage:

- Income replacement: Most financial planners suggest a death benefit equal to 10–12 times your annual income. A $90,000 earner would target $900,000–$1,080,000 in coverage.

- Outstanding debts: Add your mortgage balance, car loans, and any co-signed debt to your coverage calculation.

- Future costs: Factor in projected childcare, college tuition, and any planned major expenses your family would still face.

- Your life stage: Term life suits young families needing affordable income replacement. Permanent life fits those with estate planning and legacy goals. Many people hold both simultaneously.

- Affordability: The best policy is one you can sustain. A $1 million term policy you keep for 20 years beats a $500,000 permanent policy you lapse after five years because the premiums became unmanageable.

A practical scenario: a 33-year-old couple with a $350,000 mortgage, two young children, and a combined income of $160,000 should carry at minimum $1.5 million in combined coverage. A 20-year term policy for each partner accomplishes this affordably. As they pay down debt and build assets over time, they can add a smaller permanent policy for estate planning purposes.

Combining term and permanent policies often best meets evolving financial needs. This approach gives you high coverage now at low cost, with a permanent foundation that builds cash value for the future. It is not a one-size-fits-all product category, and the right mix changes as your life does.

Key takeaways

Life insurance is the most direct tool available for protecting your family’s financial stability, and the type and amount you choose should match your current obligations and long-term goals.

| Point | Details |

|---|---|

| Core definition | Life insurance pays a tax-free death benefit to named beneficiaries in exchange for regular premiums. |

| Two main types | Term life covers a set period at low cost; permanent life covers your lifetime and builds cash value. |

| Living benefits matter | Modern policies let you access part of the death benefit during a terminal or critical illness. |

| Buy early, pay less | Premiums rise significantly with age, so locking in coverage in your 30s saves money long-term. |

| Employer coverage is not enough | Workplace policies end when you leave the job; a personal policy provides continuous protection. |

Why i think most people get life insurance backwards

Most people treat life insurance as something to buy after a major life event: a marriage, a baby, a mortgage. That instinct is understandable, but it is also expensive. By the time those events arrive, you are already older, possibly less healthy, and paying more for the same coverage you could have locked in years earlier.

I have seen this pattern repeatedly. Someone in their late 30s finally buys a term policy after their second child is born and pays 40% more per month than they would have at 29. The coverage is the same. The cost is not.

The other mistake I see is treating employer-provided life insurance as a real safety net. It is not. It is a benefit that disappears the moment you change jobs, get laid off, or retire. Personal policies are the only kind that follow you through every chapter of your financial life.

My actual recommendation: buy a 20-year term policy in your late 20s or early 30s to cover your peak earning and obligation years. Then, as your income grows and your estate planning needs become clearer, layer in a smaller permanent policy. This combination gives you coverage depth now and a tax-efficient asset for later. For anyone thinking about how this fits into a broader wealth transfer strategy, life insurance is often the most underused tool in the plan.

Do not wait for the perfect moment. The perfect moment was five years ago. The second-best moment is now.

— Povilas

Explore life insurance options with Finblog

Finblog covers the full range of personal finance decisions that matter to professionals in their 30s and 40s, including how to evaluate, compare, and integrate life insurance into a broader financial plan. If you are ready to move from understanding the basics to making a real decision, Finblog’s insurance planning resources walk you through coverage sizing, policy comparisons, and how life insurance fits alongside your investment and tax strategy. You can also explore how insurance integrates with property investment planning for a complete picture of asset protection. Start with your current obligations, run the numbers, and use Finblog to compare your options before you commit to any policy.

FAQ

What does life insurance actually cover?

Life insurance covers the financial needs of your beneficiaries after your death, including mortgage payoff, income replacement, childcare costs, and final expenses. Some modern policies also include living benefits for terminal or critical illness.

How much life insurance do i need?

Most financial planners recommend a death benefit equal to 10–12 times your annual income, plus any outstanding debts and projected future costs like college tuition.

What is the difference between term and whole life insurance?

Term life covers a specific period (typically 10–30 years) at a lower cost with no cash value. Whole life covers your entire lifetime, builds cash value, and costs significantly more per month.

Can i access my life insurance money while i am still alive?

Yes. Permanent policies build cash value you can borrow against, and many policies include living benefit riders that let you access part of the death benefit during a serious illness.

When is the best time to buy life insurance?

The best time to buy is as early as possible. Life insurance costs increase with age, and locking in coverage in your late 20s or early 30s secures the lowest available premiums for the same benefit amount.