Investors love the thrill of big returns but forget that the IRS can take a huge bite out of those gains. Most people are shocked to learn that mutual funds with lower tax burdens consistently outperform others, both before and after taxes. Turns out, knowing how to play the tax game is just as important as picking the right stocks in the first place.

Table of Contents

- What Is Tax Efficient Investing And Why It Matters?

- Key Principles Of Tax Efficient Investing Explained

- Types Of Investment Accounts For Tax Efficiency

- Understanding Capital Gains And Tax Implications

- Strategies For Maximizing Tax Efficiency In Your Portfolio

Quick Summary

| Takeaway | Explanation |

|---|---|

| Optimize Investments for Tax Efficiency | Select investment vehicles that minimize tax liabilities to maximize returns. |

| Utilize Tax-Advantaged Accounts | Use IRAs, 401(k)s, and HSAs to grow investments tax-free or tax-deferred. |

| Implement Tax Loss Harvesting | Sell underperforming investments strategically to offset capital gains and reduce tax burden. |

| Emphasize Long-Term Investment Holding | Hold assets for over a year to qualify for lower capital gains tax rates. |

| Adopt a Strategic Asset Location Approach | Place investments in accounts based on their tax implications for better tax management. |

What is Tax Efficient Investing and Why It Matters?

Tax efficient investing represents a strategic approach to managing investments that minimizes tax liabilities while maximizing potential returns. Unlike traditional investment strategies that focus solely on performance, tax efficient investing considers the critical impact of taxes on overall investment growth.

Understanding the Tax Efficiency Concept

At its core, tax efficient investing aims to reduce the amount of money an investor pays in taxes by making deliberate investment choices. This approach recognizes that taxes can significantly erode investment returns over time. According to research from the University of Texas at Austin, mutual funds with lower tax burdens tend to achieve higher returns, both before and after taxes.

Key principles of tax efficient investing include:

- Strategically selecting investment vehicles with lower tax implications

- Utilizing tax advantaged accounts like IRAs and 401(k)s

- Managing investment transactions to minimize tax exposure

- Timing asset sales to optimize tax treatment

Why Tax Efficiency Matters for Investors

Investors who prioritize tax efficient strategies can potentially increase their long term wealth accumulation. The impact of taxes on investment returns can be substantial. By implementing smart tax strategies, investors can keep more of their investment gains and reduce the annual tax burden.

For example, holding investments for longer periods can qualify for lower long term capital gains tax rates, compared to short term trading which often incurs higher ordinary income tax rates. This approach not only reduces immediate tax liability but also allows for potential compound growth of invested capital.

The U.S. Securities and Exchange Commission emphasizes the importance of tax advantaged accounts, which allow investments to grow tax free or tax deferred, thereby reducing an investor’s overall tax liability and potentially enhancing long term financial outcomes. Smart investors understand that managing taxes is just as crucial as selecting high performing investments.

Key Principles of Tax Efficient Investing Explained

Tax efficient investing involves strategic financial planning designed to minimize tax liabilities while maintaining robust investment performance. Understanding these fundamental principles empowers investors to optimize their financial strategies and preserve more of their investment returns.

Strategic Asset Location

Asset location represents a critical principle in tax efficient investing. This strategy involves placing different types of investments in specific accounts to maximize tax advantages. Taxable accounts, tax deferred accounts, and tax exempt accounts each play unique roles in comprehensive tax management.

Key considerations for strategic asset location include:

- Placing high tax generating investments in tax advantaged accounts

- Keeping tax efficient investments in taxable accounts

- Balancing portfolio allocation across different account types

- Considering individual tax brackets and potential future tax implications

Tax Loss Harvesting

Tax loss harvesting is a sophisticated technique that allows investors to offset capital gains by strategically selling investments that have decreased in value. According to research from the Brookings Institution, this approach can provide significant tax management opportunities for sophisticated investors.

The process involves carefully selling underperforming investments to realize capital losses, which can then be used to reduce overall tax liability. Investors must navigate complex IRS rules, such as the wash sale regulation, which prevents claiming a loss if a substantially identical security is repurchased within 30 days.

Long Term Investment Perspective

Adopting a long term investment perspective is crucial for tax efficient investing. Investments held for extended periods typically qualify for more favorable long term capital gains tax rates. By minimizing frequent trading and focusing on sustainable growth, investors can significantly reduce their tax burden.

This approach not only provides potential tax advantages but also aligns with sound investment principles of patient capital appreciation. Short term trading often incurs higher tax rates and increased transaction costs, making a strategic long term approach more financially prudent for many investors.

Types of Investment Accounts for Tax Efficiency

Choosing the right investment accounts is fundamental to implementing a successful tax efficient investing strategy.

Different account types offer unique tax advantages that can significantly impact an investor’s long term financial growth and tax liability.

Retirement Accounts: Tax Advantaged Powerhouses

Retirement accounts provide some of the most powerful tax efficiency mechanisms for investors. These specialized accounts offer significant tax benefits designed to encourage long term saving and investment.

Key retirement account types include:

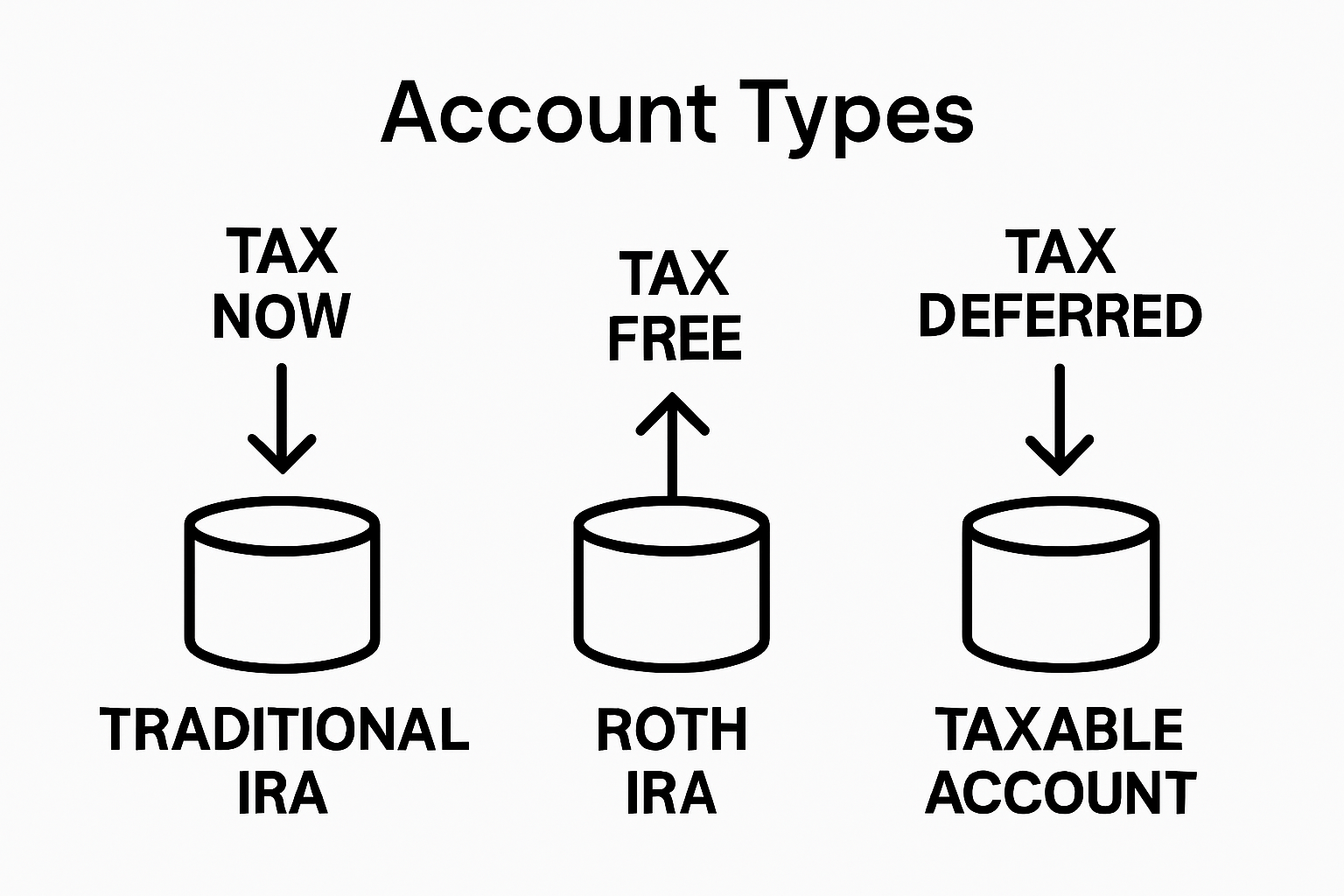

- Traditional Individual Retirement Accounts (IRAs)

- Roth Individual Retirement Accounts (Roth IRAs)

- 401(k) and 403(b) employer sponsored retirement plans

- Self employed retirement accounts like SEP IRAs and Solo 401(k)s

Traditional retirement accounts typically provide immediate tax deductions on contributions, with taxes deferred until withdrawal. Roth accounts, conversely, allow tax free withdrawals in retirement after contributions are made with after tax dollars.

Taxable Brokerage Accounts

Taxable brokerage accounts offer flexibility without the strict contribution limits of retirement accounts. While these accounts do not provide upfront tax deductions, investors can implement strategic tax management techniques. According to research from the SEC, understanding the tax implications of these accounts is crucial for effective investment planning.

Investors can minimize tax impacts in taxable accounts through strategies like:

- Holding investments for over one year to qualify for lower long term capital gains rates

- Selecting tax efficient mutual funds and exchange traded funds

- Utilizing tax loss harvesting techniques

- Focusing on investments with qualified dividend income

Health Savings Accounts: Triple Tax Advantage

Health Savings Accounts (HSAs) represent a unique investment vehicle with extraordinary tax benefits. These accounts offer a triple tax advantage: contributions are tax deductible, investments grow tax free, and withdrawals for qualified medical expenses are also tax free.

HSAs can function not just as medical expense accounts but as additional retirement savings vehicles. By treating HSAs as long term investment accounts, investors can maximize their tax efficiency while maintaining flexibility for healthcare related expenses.

The following table highlights and compares the main types of investment accounts discussed in the article, focusing on their tax benefits and key characteristics.

| Account Type | Tax Advantages | Key Features |

|---|---|---|

| Traditional IRA / 401(k) | Tax-deferred growth; pre-tax contributions | Taxes paid at withdrawal; contribution limits apply |

| Roth IRA / Roth 401(k) | Tax-free growth and withdrawals; post-tax contributions | No taxes at withdrawal; income limits may affect eligibility |

| Taxable Brokerage Account | No upfront or withdrawal tax advantages | Flexible; subject to capital gains/dividends taxes |

| Health Savings Account (HSA) | Triple tax advantage: deductible contributions, tax-free growth, tax-free withdrawals for qualified expenses | Used for medical expenses; can be used for retirement savings |

Understanding Capital Gains and Tax Implications

Capital gains represent the financial profits realized from selling investments or assets, and understanding their tax implications is crucial for effective tax efficient investing. These gains are not just numbers on a spreadsheet but represent significant opportunities for strategic financial planning.

Defining Capital Gains

Capital gains occur when an investor sells an asset for more than its original purchase price. The difference between the selling price and the original cost basis represents the taxable gain. Assets can include stocks, bonds, real estate, and other investment vehicles.

Key characteristics of capital gains include:

- Profits generated from selling investment assets

- Calculated by subtracting the original purchase price from the sale price

- Subject to different tax rates based on holding period

- Applicable to various types of investment assets

Short Term vs Long Term Capital Gains

The duration an investor holds an asset significantly impacts its tax treatment. According to research from the Legal Information Institute at Cornell Law School, assets held for different periods are taxed at varying rates.

Short term capital gains apply to assets held for one year or less and are taxed at ordinary income tax rates. Long term capital gains, conversely, apply to assets held for more than one year and typically receive preferential tax treatment. These long term gains are taxed at lower rates, often 0%, 15%, or 20%, depending on the investor’s income level.

This table summarizes the distinctions between short-term and long-term capital gains taxation, as described in the article, to clarify their tax implications for investors.

| Capital Gains Type | Holding Period | Tax Rate Basis | Typical Tax Rate Range |

|---|---|---|---|

| Short-Term Gains | One year or less | Ordinary income tax rates | 10% – 37% (based on income) |

| Long-Term Gains | More than one year | Preferential tax rates | 0%, 15%, or 20% (based on income) |

Tax Loss Harvesting Strategies

Investors can strategically manage capital gains through tax loss harvesting. This technique involves selling investments that have decreased in value to offset capital gains from other profitable investments. By carefully timing asset sales and understanding tax regulations, investors can minimize their overall tax liability.

Important considerations for tax loss harvesting include:

- Offsetting capital gains with capital losses

- Adhering to IRS wash sale rules

- Maintaining overall investment portfolio strategy

- Consulting with tax professionals for personalized guidance

Understanding capital gains and their tax implications allows investors to make more informed decisions, potentially reducing tax burdens and maximizing investment returns.

Strategies for Maximizing Tax Efficiency in Your Portfolio

Maximizing tax efficiency requires a comprehensive approach that goes beyond simple investment selection. Sophisticated investors understand that strategic planning and deliberate asset management can significantly reduce tax liabilities and enhance long term investment returns.

Asset Location and Strategic Placement

Asset location represents a critical strategy for minimizing tax impacts. This approach involves carefully placing different types of investments in specific accounts to optimize tax treatment. By understanding the unique tax characteristics of various investment vehicles, investors can create a more tax efficient portfolio.

Key principles of strategic asset placement include:

- Holding high yield investments in tax advantaged accounts

- Placing tax efficient index funds in taxable accounts

- Minimizing tax generating assets in accounts with immediate tax implications

- Balancing investment types across different account structures

Investment Vehicle Selection

Choosing the right investment vehicles plays a crucial role in tax efficient investing. According to research from the TIAA Institute, maximizing contributions to tax favored accounts can significantly reduce overall tax burden.

Tax efficient investment vehicles include:

- Index funds with low turnover rates

- Exchange traded funds (ETFs)

- Municipal bonds

- Low dividend growth stocks

- Qualified dividend paying investments

Active Tax Management Techniques

Proactive tax management involves continuously monitoring and adjusting investment strategies to minimize tax liabilities. This dynamic approach requires ongoing attention and strategic decision making.

Effective tax management techniques encompass:

- Implementing tax loss harvesting strategies

- Timing investment sales to optimize capital gains treatment

- Utilizing tax loss carryforwards

- Considering asset holding periods to qualify for long term capital gains rates

Successful tax efficient investing demands a holistic approach that integrates careful planning, strategic asset selection, and continuous portfolio optimization.

Take Control of Your Taxes and Maximize Every Dollar

Reading about tax efficient investing can open your eyes to how much taxes actually eat into your returns. Navigating concepts like strategic asset location and tax loss harvesting can feel overwhelming if you are trying to do it all on your own. Maybe you want to protect more of your hard earned money but you are not certain which accounts will help you most. Or perhaps you have experienced the sting of higher tax bills from short term trades and want to finally start benefiting from long term strategies.

You do not have to manage these tough decisions alone. finblog.com is designed exactly for investors like you who need clear, expert guidance on tax efficient investing. Whether you are ready to optimize your portfolio or just starting to explore your options, our team can help simplify every step. Visit our main page now to connect, ask questions, and see how small changes in your approach can lead to bigger long term rewards. Act now to protect your financial future and start building a strategy that truly works for you.

Frequently Asked Questions

What is tax efficient investing?

Tax efficient investing is a strategy aimed at minimizing tax liabilities while maximizing investment returns by making deliberate investment choices that consider tax implications.

How can tax efficiency impact my investment returns?

Tax efficiency can significantly enhance your investment returns by reducing taxes on capital gains and other earnings, allowing you to retain more of your gains and compound growth over time.

What are some strategies for achieving tax efficient investing?

Key strategies include strategic asset location, tax loss harvesting, and holding investments in tax-advantaged accounts like IRAs or 401(k)s to minimize tax exposure and optimize tax treatment.

What types of accounts are best for tax efficient investing?

Tax efficient investing often utilizes various account types, including tax-advantaged retirement accounts (like IRAs and 401(k)s), taxable brokerage accounts for flexibility, and Health Savings Accounts (HSAs) for their triple tax advantage.