TL;DR:

- An emergency fund is designed to cover unexpected expenses and provide financial stability.

- Most experts recommend saving three to six months of essential living costs.

- Keep your emergency fund in accessible, insured accounts like high-yield savings for quick access.

An emergency fund is one of the most misunderstood tools in personal finance. Many people see it as idle cash doing nothing while investments could be growing. That thinking is exactly why so many households end up in financial crisis when life gets unpredictable. An emergency fund is a precision tool, not a passive pile of money. It is your first line of defense against the kind of unexpected events that can derail years of careful planning. This guide explains what an emergency fund is, how much you actually need, where to keep it, and how to build one steadily without disrupting your life.

Table of Contents

- Understanding emergency funds: Purpose and definition

- How much do you really need in an emergency fund?

- Where should you keep your emergency fund?

- How to build your emergency fund: Step-by-step guide

- Why most people get emergency funds wrong—and what actually works

- Ready to boost your financial safety net?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Essential safety net | An emergency fund protects you from financial shocks like job loss or medical emergencies. |

| 3-6 months benchmark | Aim for 3-6 months of essential expenses—not total income—as your emergency fund target. |

| Keep funds accessible | Use a safe, liquid account so you can access money when you need it most. |

| Start small, stay consistent | Even small regular savings add up, so start with what you can manage and build up over time. |

Understanding emergency funds: Purpose and definition

An emergency fund is money set aside specifically for unexpected expenses or sudden financial hardship. It is not a vacation fund, a car upgrade account, or a general savings buffer. It has one job: to keep you financially stable when life throws something you did not plan for.

The scenarios where an emergency fund becomes critical are more common than people admit. Job loss is the most frequently cited example, and for good reason. Losing income suddenly, even temporarily, can create a chain reaction of missed payments, mounting debt, and lasting credit damage. Medical emergencies are another major trigger. Even with insurance, out-of-pocket costs can run into thousands of dollars very quickly. Urgent car repairs, sudden home plumbing failures, and unexpected travel for a family crisis all qualify as genuine emergencies.

What does not qualify? This part matters just as much. Holiday shopping, replacing a phone you dropped, buying new furniture, or funding a trip are not emergencies. Neither is a known annual expense like car registration or a seasonal insurance premium. Those belong in a planned savings category, not your emergency fund.

“An emergency fund is money you set aside specifically to pay for unexpected expenses or financial emergencies. Having one can keep you from having to use a credit card or take out a loan to cover bills in a difficult time.” — Consumer Financial Protection Bureau

The emotional and practical security that comes from having this fund is real and measurable. People with emergency funds report lower financial stress, better sleep, and more confidence in their overall decision-making. When your rent is covered for the next four months even if something goes wrong at work, you negotiate from a position of stability rather than desperation. That changes everything from career decisions to health choices.

Here is a quick breakdown of what counts as an emergency and what does not:

Legitimate emergencies:

- Sudden job loss or reduction in income

- Unexpected medical or dental bills

- Emergency car or home repair (not routine maintenance)

- Urgent travel due to a family crisis

- Sudden appliance failure that affects daily living

Not emergencies:

- Planned vacations or discretionary travel

- New tech purchases or upgrades

- Seasonal or predictable expenses

- Non-urgent home improvements

- Entertainment or social spending

Understanding why emergency funds matter goes beyond just having cash on hand. It is about preserving your financial foundation when circumstances shift without warning. Without it, people typically reach for credit cards, personal loans, or early retirement withdrawals, all of which carry serious long-term costs.

How much do you really need in an emergency fund?

Understanding its purpose, the next crucial question is how much you actually need to protect yourself. The widely accepted benchmark, backed by financial experts including the Consumer Financial Protection Bureau, is 3 to 6 months of essential living expenses. Notice the word “essential.” This is not about replacing your entire income or maintaining your current lifestyle at full capacity. It is about covering the non-negotiable costs that keep your life running.

Here is a table to help you map your monthly essential expenses:

| Expense category | Example monthly cost |

|---|---|

| Housing (rent or mortgage) | $1,200 |

| Utilities (electricity, gas, water) | $150 |

| Groceries and household supplies | $400 |

| Transportation (gas, transit, insurance) | $300 |

| Health insurance premiums | $200 |

| Minimum debt payments | $250 |

| Total monthly essentials | $2,500 |

Using that example, a 3-month emergency fund target would be $7,500 and a 6-month target would be $15,000. Most people find that number surprising at first. But when you break it down monthly, it becomes far more manageable to work toward.

Here is a simple step-by-step process to calculate your own target:

- List every monthly expense you cannot skip without serious consequences

- Add up only those essential categories, not subscriptions, dining out, or entertainment

- Multiply that total by three for a starter target, or by six for a more conservative cushion

- Write that number down as your specific goal, not a vague “save more” intention

Pro Tip: Adjust your target based on your personal risk profile. If you are self-employed or work in a contract-based industry, aim for at least six months. If you have a stable dual-income household with low debt, three months may be sufficient. Your target should reflect your risk, not a generic average.

Several common mistakes trip people up when setting their target. First, they calculate based on their total income rather than essential expenses only. That consistently inflates the goal and makes it feel unattainable. Second, they forget to include insurance premiums and minimum debt payments, which are non-negotiable outflows. Third, they never revisit the number after a major life change like a new apartment, a baby, or a pay raise.

Starting small is not a failure. It is a strategy. Even a $1,000 starter fund absorbs a significant portion of common emergencies. The important thing is to define your target through an emergency fund planning guide, start saving toward it deliberately, and build upward from there.

Where should you keep your emergency fund?

Once you know your target amount, the next step is deciding where to store your emergency fund for maximum safety and convenience. This decision is more important than most people realize, and getting it wrong can cost you either in accessibility or in opportunity.

The two best options for most people are high-yield savings accounts and money market accounts. Both offer Federal Deposit Insurance Corporation (FDIC) protection, reasonable interest rates, and easy access to your money without penalties. A high-yield savings account at an online bank often earns significantly more interest than a traditional savings account while keeping your funds just as safe.

Here is a comparison of the most common storage options:

| Account type | Access speed | Safety | Returns | Penalties |

|---|---|---|---|---|

| High-yield savings | 1 to 2 business days | FDIC insured | Moderate (4 to 5% in 2026) | None |

| Money market account | 1 to 2 business days | FDIC insured | Moderate | None |

| Traditional savings | Immediate | FDIC insured | Low (under 1%) | None |

| Certificate of deposit (CD) | Weeks to months | FDIC insured | Higher | Early withdrawal fee |

| Brokerage/investment account | 2 to 5 days | Not insured | Variable (can lose value) | Possible capital gains tax |

The key principle here is liquidity. Your emergency fund must be available quickly when you need it. A 12-month CD might earn more interest, but if your car breaks down on a Tuesday, you cannot afford to wait for a maturity date. Investments are even riskier. The stock market could be down 20% the exact week you need to pull funds, leaving you with less money than you started with.

Your emergency fund should also be kept separate from your everyday checking account. When extra money sits in the same account you use for daily spending, it tends to disappear quietly into small purchases. Separation creates a psychological barrier that protects the fund from casual spending. Explore your options for types of savings accounts to find the right fit for your specific banking preferences.

Key best practices for storing your emergency fund:

- Use an account with FDIC or NCUA (National Credit Union Administration) insurance for full protection

- Choose a bank or credit union that makes transfers straightforward but not instant enough to tempt impulse withdrawals

- Avoid mixing your emergency fund with money earmarked for other goals

- Review the interest rate on your account annually, better rates are frequently available

If you are ever tempted to put your emergency fund into the market for better returns, it is worth reading about saving vs investing to understand the key distinction. Safety and accessibility are the priorities here, not growth.

How to build your emergency fund: Step-by-step guide

With your account chosen, the main challenge becomes consistent saving and here is exactly how to make it manageable. Building an emergency fund does not require a large income or a dramatic lifestyle overhaul. It requires a clear plan and steady execution.

Follow this step-by-step approach:

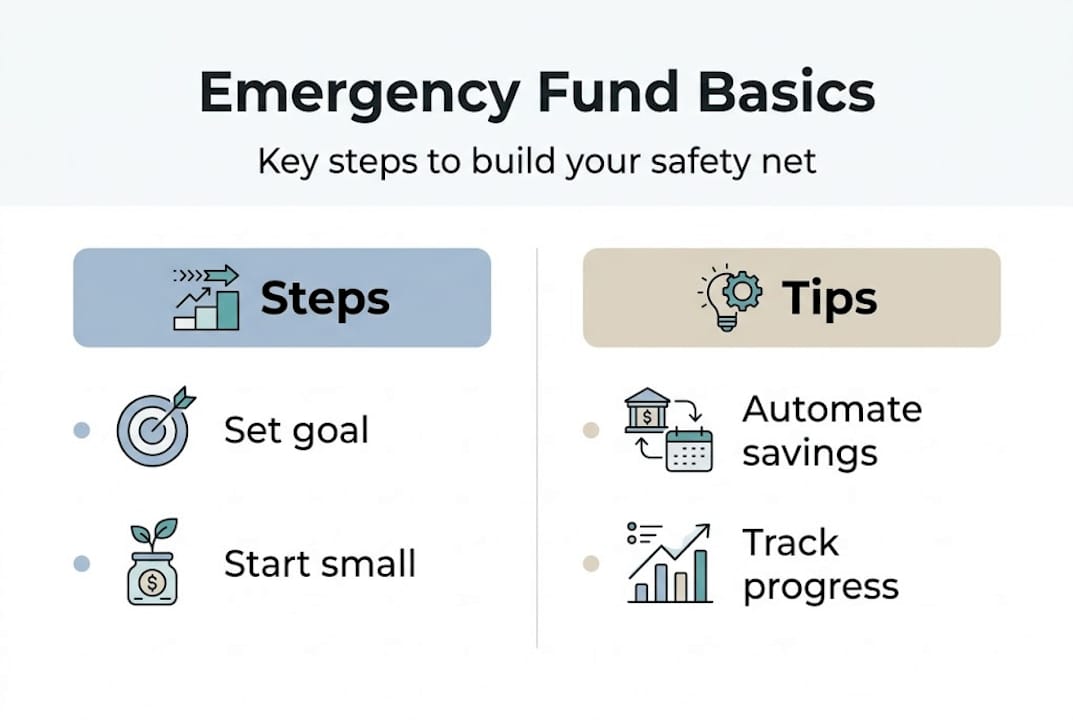

- Set a specific target. Use the calculation method from the previous section. Write your exact goal amount down somewhere you will see it regularly.

- Open a dedicated account. Choose a high-yield savings or money market account that is separate from your checking account. Name it “Emergency Fund” if your bank allows custom labels.

- Set up automatic transfers. Schedule a fixed amount to move from your checking account to your emergency fund on payday. Even $50 per paycheck adds up to $1,300 in a year.

- Track your progress monthly. Check the balance once a month to stay motivated and adjust contributions when your income changes.

- Celebrate milestones. Reaching $500, then $1,000, then your first month of expenses covered are all worth acknowledging.

Pro Tip: Treat your emergency fund contribution exactly like a bill. “Paying yourself first” before discretionary spending ensures it actually happens. If it is automatic, it is not a decision you have to make every month.

Finding extra cash to accelerate your savings is often easier than it seems. Selling items you no longer use can generate a fast one-time boost. Cutting one subscription you barely use, even temporarily, frees up recurring cash. A small side gig, freelancing on weekends or driving for a delivery app, can add hundreds of dollars per month toward your goal. Read saving money best practices for detailed strategies tailored to investors and professionals building their financial foundation.

After an emergency happens and you draw from the fund, rebuild it as soon as possible. Return to your automatic contributions immediately, even if the amount is small. Do not let the fund sit depleted. The period right after using it is when you are most vulnerable to a second unexpected event.

Pitfalls to watch for:

- Raiding the fund for non-emergencies. Treat a clear personal definition of “emergency” as a rule, not a guideline.

- Skipping small deposits. Small, regular contributions beat large, inconsistent ones every time.

- Waiting until you earn more. Start with whatever you can manage today. $25 a week still builds a meaningful cushion over six months.

Progress over perfection is the right mindset. According to the CFPB’s emergency fund guidance, starting with a small goal and working up is not a compromise. It is the approach most likely to succeed long term.

Why most people get emergency funds wrong—and what actually works

Most financial advice tells you to save three to six months of expenses and leaves it there. That benchmark is useful, but the deeper story is almost always missing from mainstream guides.

The biggest mistake is thinking an untouched emergency fund is wasted money. That thinking comes from the same logic that says insurance is only valuable when you make a claim. In reality, the security itself has genuine value. Knowing the money is there changes how you make decisions every single day. It reduces the impulse to stay in a bad job out of fear, or to avoid a necessary medical visit because the cost feels impossible. That peace of mind is not abstract. It is financially consequential.

What most guides also miss is the importance of tailoring your fund to your actual risk factors rather than copying a generic number. A freelance graphic designer with inconsistent monthly income has a fundamentally different risk profile than a federal employee with tenure and full benefits. Common financial planning mistakes frequently include applying one-size-fits-all rules to situations that demand individual analysis.

A smaller “mini” fund, even just $500 to $1,000, still covers the majority of the most common financial emergencies Americans face. It is not ideal, but it provides real, meaningful protection. Waiting until you can save six months of expenses before starting means you are unprotected for months or years unnecessarily.

The uncomfortable truth is that perfection is not the standard here. A partially funded emergency account is dramatically better than none. Start where you are, build steadily, and adjust the target as your life changes. That is the approach that actually works in the real world, not the clean theoretical version.

Ready to boost your financial safety net?

Building an emergency fund is one of the most impactful financial moves you can make, and the good news is that you do not need to figure it out alone. At finblog.com, we offer in-depth guides, practical calculators, and expert resources designed specifically for adults who want to build genuine financial security. Whether you are just starting your fund or looking to optimize what you already have, our content is built to give you clear, actionable direction. Explore our full library of personal finance guides, connect with our advisory resources, and take the next step toward a financial foundation that holds up when it matters most.

Frequently asked questions

Can I use my emergency fund for planned expenses?

No. Emergency funds are strictly for unexpected expenses like sudden job loss, unplanned medical bills, or urgent repairs. Planned purchases should be saved for separately in a dedicated account.

Is it better to invest my emergency fund for higher returns?

Keep your emergency fund in a safe, easily accessible account rather than investing it. Investments can lose value or take days to liquidate, both of which defeat the purpose of an emergency fund.

What if I can’t save three months’ expenses right now?

Start with a smaller goal like $500 or $1,000. Starting small and building gradually is far more effective than waiting until you can save a full three-month target at once.

How often should I review or update my emergency fund?

Review your emergency fund target whenever your life circumstances change significantly, such as after a job change, a move to a higher-cost area, a new family member, or a major shift in monthly expenses.