Nearly 70 percent of adults worldwide lack a basic understanding of financial concepts, according to recent OECD findings. Without this crucial knowledge, daily money choices can quickly become overwhelming or even risky. By gaining clarity on financial literacy, you set the stage for smarter budgeting, confident investing, and a stronger sense of financial security for yourself and your family.

Table of Contents

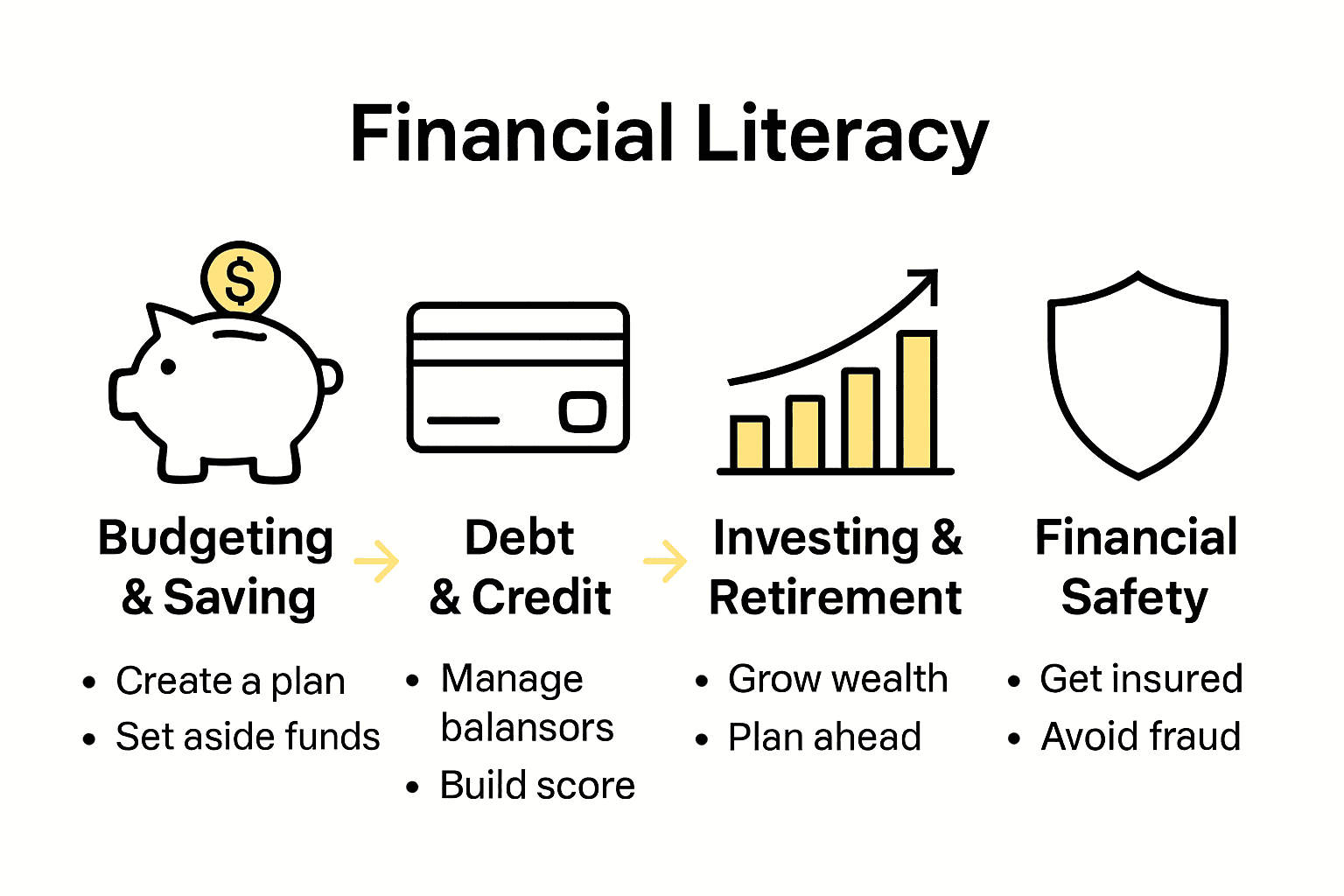

- What Is Financial Literacy Explained

- Budgeting, Saving and Emergency Funds

- Debt, Credit Scores and Responsible Borrowing

- Investing Basics and Retirement Planning

- Common Money Misconceptions Debunked

- Risks, Scams and Financial Safety

Key Takeaways

| Point | Details |

|---|---|

| Understanding Financial Literacy | Financial literacy equips individuals with the knowledge to manage finances, including budgeting, investing, and debt management. It enables strategic decision-making for long-term financial health. |

| Importance of Budgeting and Emergency Funds | Creating and maintaining a budget, alongside an emergency fund, is essential for financial stability and managing unexpected expenses effectively. |

| Responsible Borrowing Practices | Knowledge of credit scores and responsible borrowing helps individuals avoid excessive debt and maintain good credit health, which is crucial for securing loans with favorable terms. |

| Awareness of Financial Scams | Being vigilant against financial scams and understanding the risks associated with financial products is vital for personal financial safety and protection against fraud. |

What Is Financial Literacy Explained

Financial literacy represents the foundational knowledge and skills that enable individuals to understand, manage, and effectively navigate their financial world. According to the OECD, financial literacy involves comprehending financial concepts, understanding potential risks, and developing the attitudes necessary to make informed financial decisions across various economic contexts.

At its core, financial literacy is about empowering individuals to take control of their financial future. As Wikipedia explains, this means possessing the knowledge and behaviors that allow someone to make strategic money management choices. This includes understanding critical financial concepts like:

- Compound interest mechanisms

- Inflation dynamics

- Risk diversification strategies

- Basic investment principles

- Personal budgeting techniques

Developing financial literacy isn’t just about memorizing facts—it’s about cultivating a mindset of strategic financial thinking. Financially literate individuals can:

- Create realistic and sustainable budgets

- Make informed investment decisions

- Understand and manage personal debt

- Plan for short and long-term financial goals

- Protect themselves from potential financial risks

Ultimately, financial literacy transforms money from a source of stress into a tool for achieving personal and professional aspirations. How to Budget Effectively: Master Your Finances in 2025 can provide additional insights into practical financial management strategies that complement these fundamental literacy skills.

Budgeting, Saving and Emergency Funds

Budgeting, saving, and establishing emergency funds form the core pillars of personal financial stability. According to the Library of Congress Guides, financial literacy involves learning how to manage money wisely through understanding key strategies like tracking income and expenses, establishing savings goals, and creating emergency funds to cover unexpected financial needs.

Budgeting is the foundational skill that enables individuals to take control of their financial landscape. By creating a structured plan that tracks income and allocates expenses, people can make informed decisions about spending and saving. 7 Essential Tips for Budgeting for Families can provide additional guidance on developing effective family financial strategies.

Effective financial planning involves several critical components:

- Creating a realistic monthly budget

- Tracking expenses meticulously

- Identifying areas for potential savings

- Setting clear financial goals

- Building an emergency fund

An emergency fund serves as a critical financial safety net, providing protection against unexpected expenses or income disruptions. Financial experts recommend saving 3-6 months of living expenses in an easily accessible account. This fund helps prevent individuals from falling into debt when unexpected challenges arise.

To avoid common pitfalls, it’s essential to be aware of potential budgeting mistakes. 7 Common Budgeting Mistakes to Avoid for Financial Success highlights critical errors that can derail financial planning. By understanding and proactively addressing these potential challenges, individuals can create more robust and sustainable financial strategies that support long-term economic well-being.

Here’s a comparison of the core pillars of financial literacy:

| Pillar | Primary Focus | Typical Actions | Importance |

|---|---|---|---|

| Budgeting & Saving | Manage income & expenses | Creating budgets Setting savings goals Tracking spending |

Builds financial stability |

| Debt & Credit | Borrowing and credit scores | Paying on time Managing credit use Reviewing credit reports |

Enables affordable borrowing |

| Investing & Retirement | Growing wealth & future security | Diversifying investments Early saving Periodic reviews |

Ensures long-term financial security |

| Financial Safety | Risk awareness & fraud prevention | Recognizing scams Protecting data Monitoring accounts |

Protects from losses and fraud |

Debt, Credit Scores and Responsible Borrowing

Understanding debt, credit scores, and responsible borrowing is crucial for financial health and long-term economic stability. According to Wikipedia, financial literacy encompasses comprehending how credit scores impact borrowing costs and the significance of maintaining good credit through prudent financial decisions and timely debt repayment.

Credit scores represent a critical financial metric that lenders use to assess an individual’s creditworthiness. These numerical representations reflect your financial reliability and directly influence your ability to secure loans, credit cards, and even rental agreements. Understanding the Importance of Credit Score provides deeper insights into how these scores are calculated and managed.

Responsible borrowing involves several key principles:

- Maintaining a low credit utilization ratio

- Making payments on time

- Avoiding unnecessary debt

- Understanding loan terms completely

- Monitoring your credit report regularly

As the Library of Congress Guides explain, being financially literate means knowing how to manage debt effectively and understanding the nuanced implications of borrowing. This knowledge helps individuals make informed decisions about loans and credit, ensuring they don’t become overwhelmed by financial obligations.

For those struggling with existing debt, Master Managing Credit Card Debt: Achieve Financial Freedom offers practical strategies for debt reduction.

The key is approaching borrowing as a strategic tool for financial growth, not as a means of immediate gratification, and always maintaining a clear understanding of your financial capacity and long-term goals.

Investing Basics and Retirement Planning

Investing and retirement planning are critical components of long-term financial security. According to Wikipedia, financial literacy curricula emphasize understanding different investment options, assessing risks, and recognizing the importance of early and consistent retirement savings to ensure financial stability in later years.

Investment strategies form the foundation of successful financial planning. Diversification is key to managing risk and maximizing potential returns. Master Building an Investment Portfolio for Profits offers insights into creating a balanced approach to investing that aligns with individual financial goals and risk tolerance.

Crucial investment principles include:

- Starting to invest early

- Diversifying across different asset classes

- Understanding your risk tolerance

- Regularly reviewing and rebalancing investments

- Minimizing investment fees

Retirement planning requires a strategic approach. The Library of Congress Guides highlight the importance of developing a comprehensive strategy that considers various investment vehicles and aligns with long-term financial objectives. This means looking beyond simple savings and understanding how different investment options can work together to build a robust retirement fund.

For those looking to take their retirement planning to the next level, 7 Must-Know Retirement Planning Tips for Smart Investors provides valuable guidance. The most successful investors understand that retirement planning is not a one-time event, but an ongoing process that requires consistent attention, education, and strategic decision-making.

Common Money Misconceptions Debunked

Financial myths can significantly hinder personal economic growth and financial well-being. According to Wikipedia, financial literacy is fundamentally about dispelling common money misconceptions that can lead individuals astray. One prevalent myth is the belief that carrying a credit card balance improves credit scores, when in reality, paying off balances in full and on time is far more beneficial for credit health.

Money misconceptions often stem from outdated advice or incomplete understanding of financial principles. These myths can prevent individuals from making smart financial decisions and building long-term wealth. Common misconceptions include:

- Believing that budgeting means restricting your lifestyle

- Thinking that investing is only for wealthy people

- Assuming that credit cards are always bad

- Believing you’re too young to start saving

- Thinking that your income determines your financial success

The Library of Congress Guides emphasize that budgeting is not a restrictive practice, but an empowering tool that gives individuals control over their financial destiny. Contrary to popular belief, budgeting actually provides freedom by helping you understand and optimize your spending patterns.

Understanding these misconceptions is crucial for financial growth. Learning to question conventional wisdom and seek accurate, up-to-date financial information can transform your approach to money management. By challenging these myths, you open yourself to more strategic and informed financial decision-making that can significantly impact your long-term economic well-being.

Risks, Scams and Financial Safety

Financial safety is a critical component of personal financial management that requires constant vigilance and awareness. According to the OECD, financial literacy encompasses the ability to recognize and avoid financial scams while understanding the risks associated with various financial products, ultimately protecting individuals from potential fraud.

Financial scams have become increasingly sophisticated, targeting individuals through multiple channels including digital platforms, phone calls, and email communications. Common Financial Scams: Complete Guide for Investors provides critical insights into identifying and avoiding these increasingly complex fraudulent schemes.

Key warning signs of potential financial scams include:

- Promises of guaranteed high returns

- Pressure to make immediate decisions

- Requests for personal financial information

- Unsolicited investment opportunities

- Communications from unverified sources

- Demands for upfront payments

- Complex or intentionally confusing explanations

As Wikipedia emphasizes, being financially literate means developing a keen awareness of potential financial risks and understanding the importance of safeguarding personal financial information. This involves not just recognizing scams, but also implementing proactive protection strategies such as:

- Using strong, unique passwords

- Monitoring financial statements regularly

- Being skeptical of unsolicited communications

- Verifying the legitimacy of financial institutions

- Protecting personal identification information

By cultivating a strategic approach to financial safety, individuals can significantly reduce their vulnerability to potential scams and protect their hard-earned financial resources.

Take Control of Your Financial Future Today

Feeling overwhelmed by budgeting, debt management, and investing basics is completely normal when you are just starting out on your financial literacy journey. This article highlights key challenges like understanding credit scores, building emergency funds, and avoiding common money misconceptions that often cause confusion and hold many back from reaching their goals. If you want to stop feeling stuck and start making confident financial decisions that lead to real stability and growth, it is time to take action now.

Explore expert strategies tailored for beginners on how to master your finances by visiting finblog.com. You can also deepen your skills and protect yourself from pitfalls with resources like 7 Common Budgeting Mistakes to Avoid for Financial Success and discover how to Master Managing Credit Card Debt. Don’t wait to secure your financial future. Visit finblog.com to get personalized guidance that turns knowledge into power.

Frequently Asked Questions

What is financial literacy?

Financial literacy refers to the skills and knowledge that enable individuals to understand and manage their financial resources effectively. It involves understanding concepts such as budgeting, saving, investing, and managing debt.

Why is budgeting important in financial literacy?

Budgeting is a critical component of financial literacy as it helps individuals track their income and expenses, enabling them to make informed decisions about spending and saving. It is essential for achieving financial stability and reaching long-term financial goals.

How can I improve my financial literacy skills?

Improving financial literacy can be achieved through education, such as reading books, taking online courses, using financial management tools, and seeking advice from financial professionals. Regularly reviewing personal finances and staying informed about financial concepts also helps.

What common financial myths should I be aware of?

Common financial myths include the belief that budgeting is restrictive, that investing is only for wealthy individuals, and that carrying a credit card balance improves credit scores. Understanding these misconceptions is crucial for building a strong financial future.