Global equities climbed on Monday, with the S&P 500 and Nasdaq hitting fresh record highs, as falling bond yields, a weaker dollar, and upbeat corporate earnings helped offset lingering trade and central bank policy tensions. According to Jamie McGeever’s Reuters Trading Day column, investor confidence remains firm even in the face of tariff uncertainty and political interference chatter surrounding the Federal Reserve.

Despite the heavy fog of risk — including Donald Trump’s tariff threats, his public feud with Fed Chair Jerome Powell, and growing global political pressure on central banks — the rally appears undeterred.

Markets Surge as Risk Appetite Grows

Monday saw a broad-based rally:

- S&P 500 and Nasdaq Composite closed at record highs, lifted by strength in tech and communications services.

- Verizon ($VZ) surged 4%, leading gains after raising its annual profit forecast.

- The MSCI World Index rose 0.2%, also hitting a new high as gains in Asia offset weakness in Europe.

- Gold jumped 1.4% to a one-month high above $3,400/oz.

- US Treasury yields fell as much as 8 basis points at the long end, flattening the curve.

- The US Dollar Index dropped 0.6% — its steepest one-day fall in over a month — with a 1% decline against the yen.

Traders Shrug Off Tariff Risks — For Now

Markets appear to be brushing off Trump’s escalating trade threats, at least for the time being. As McGeever notes, the effective US tariff rate has climbed close to 20%, the highest since 1933, driven by threats of:

- 30% tariffs on EU and Mexican imports

- 20–50% tariffs on goods from Canada, Brazil, Japan, and others

- Ongoing letters from the Trump administration laying out baseline levies to over 150 countries

Still, Commerce Secretary Howard Lutnick told CBS Sunday he’s confident a deal with the EU will happen before the Aug. 1 deadline, and that negotiations are “moving along.” EU diplomats confirmed that they are preparing broader retaliation options, but still prioritise a negotiated resolution.

Investors seem to be betting on a similar outcome as in April’s “Liberation Day” volatility: a last-minute deal or watered-down tariffs.

Trump-Powell Feud Reignites Central Bank Independence Debate

Trump’s weekend tirade against Fed Chair Powell has reignited global debate around central bank independence. After the Wall Street Journal claimed Treasury Secretary Scott Bessent advised Trump not to fire Powell, both Bessent and Trump publicly denied the story.

Trump posted:

“If it weren’t for me, the Market wouldn’t be at Record Highs… People don’t explain to me. I explain to them!”

Bessent reinforced that his focus is on inflation data:

“If inflation numbers are low, we should be cutting rates. That would unlock the mortgage market.”

While Fed policy remains intact for now, Reuters’ McGeever cautions that Trump’s open pressure may puncture the veneer of independence the Fed has long operated under — an issue with global ramifications.

As former Fed Chair Janet Yellen recently told The New Yorker:

“These are the kinds of things you’d expect from a banana republic.”

Earnings, Data, and Global Watchlist

Corporate earnings remain solid, with over 83% of S&P 500 firms beating EPS forecasts so far. Strong performance has been seen from banks, tech, and telecoms, including:

- JPMorgan, Citigroup, Goldman Sachs — all beat on trading revenues

- TSMC, PepsiCo — blew past expectations on AI and consumer demand

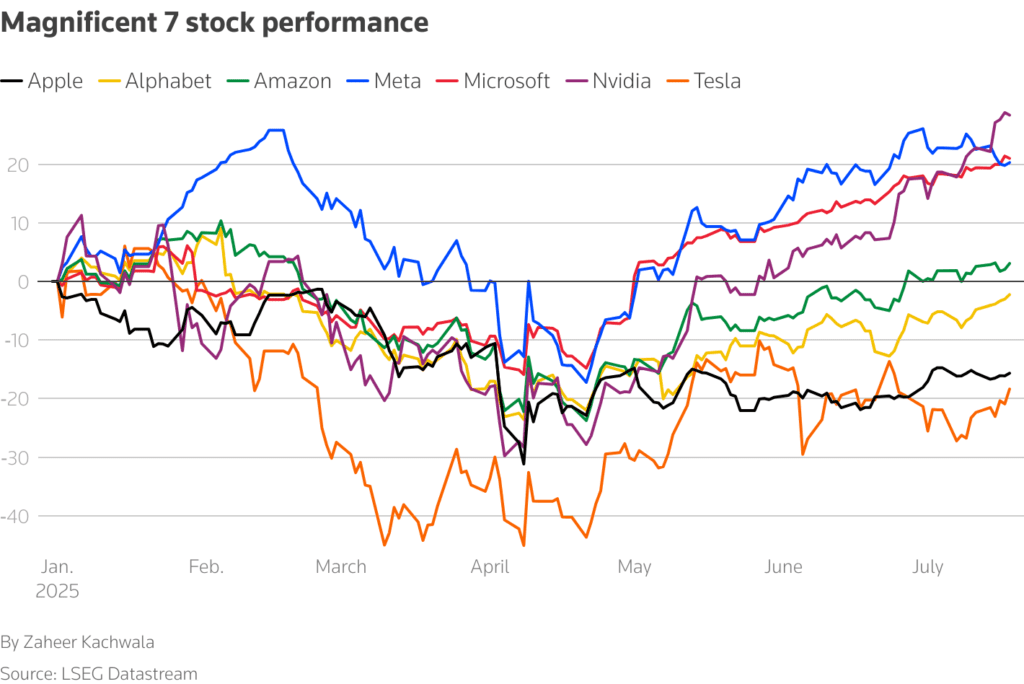

- More than 100 companies report this week, including Alphabet, Tesla, Philip Morris, and Coca-Cola

Economic data has also surprised to the upside:

- The Citi US Economic Surprise Index has been steadily rising

- Meanwhile, Europe’s equivalent is flat, and China’s is declining

Japan Reopens After Election Shock

Japanese markets reopened Tuesday after a holiday closure, giving investors their first chance to react to the upper house election, which saw Prime Minister Shigeru Ishiba’s coalition lose its majority for the first time since 1955.

Ishiba said he will stay on, citing the importance of ongoing US–Japan trade talks ahead of Trump’s tariff deadline. Nikkei futures point to a flat open.

Looking Ahead

- Tuesday’s calendar features earnings from Coca-Cola and Philip Morris, along with UK public borrowing figures and Bank of England testimony.

- Investors are watching how Japan, China, and Europe respond to shifting US trade tactics.

- The Fed’s next moves — and how political pressure shapes them — remain a key macro driver.

Disclosure: This article does not represent investment advice. The content and materials featured on this page are for educational purposes only.

Related:

Markets Brace for Tech Earnings and Trump Tariff Deadline

Indian Bank Stocks Surge as Earnings Beat Estimates

The 60/40 Portfolio Under the Microscope: 150 Years of Market Stress‑Testing

Trump To Open 401k Market To Crypto, Gold, And Private Equity

93.5 % Battery Material Tariff by US: 5 Stocks Poised to Benefit Most From It

How Nvidia Jensen Huang Persuaded Trump to Sell AI Chips to China

Stocks Inch Up as Trump Softens Tariff Talk; CPI and Bank Earnings Ahead