TL;DR:

- Most Americans face overwhelming financial stress due to complexity, not necessarily low income.

- Financial minimalism simplifies money management through fewer accounts, automation, and intentional spending aligned with personal values.

Most people assume financial stress is an income problem. Earn more, spend less, problem solved. But 88% of U.S. adults reported financial stress entering 2026, and most of them aren’t broke. They’re overwhelmed. The connection between minimalism and money isn’t about deprivation. It’s about removing the financial noise that makes smart decisions feel impossible. When you simplify your financial system, you spend less energy managing money and more energy actually building it.

Table of Contents

- Key takeaways

- What financial minimalism actually means

- How to simplify your budget

- Cutting impulse spending and financial noise

- Building a savings system that runs itself

- My take on financial minimalism

- Take the next step with Finblog

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Minimalism isn’t deprivation | Financial minimalism focuses on intentional spending, not cutting everything you enjoy. |

| Simpler budgets stick better | Fewer categories and automated transfers reduce tracking fatigue and increase consistency. |

| Impulse spending has triggers | Reducing exposure to retail cues and using time-boxed moratoriums breaks overspending cycles. |

| Automation replaces willpower | Scheduled transfers and rules-based systems make saving automatic, not effortful. |

| Stress drops with simplicity | Pre-decided spending rules reduce anxiety, especially during high-spend periods like holidays. |

What financial minimalism actually means

Financial minimalism is not about living on rice and refusing to enjoy your money. That’s frugality taken to an extreme, and it’s not sustainable. Financial minimalism is something more specific. It’s the practice of reducing financial complexity so that every dollar you spend reflects a genuine priority.

Think about how most people manage money. Multiple bank accounts, a handful of credit cards with overlapping rewards programs, a dozen subscriptions running quietly in the background, and a budget with 20 categories to track. The system feels thorough. In practice, it creates so many decision points that most people give up tracking after a few weeks.

A minimalist approach to finances does the opposite. It cuts the system down to its load-bearing walls. Here’s what that looks like in practice:

- One checking account, one savings account, one credit card. Limiting accounts and cards prevents the budget complexity and decision fatigue that makes minimalist money management hard to sustain.

- Automated bills and savings transfers. Money moves on a schedule without requiring daily decisions. You set the rules once.

- Spending aligned with declared values. Before buying something, you ask one question: does this reflect what I actually care about?

- Regular simplification checks. A quarterly review of subscriptions, accounts, and automatic charges keeps the system lean.

The mindset shift here is real. Most financial advice asks you to track more, categorize better, and be more disciplined. Financial minimalism asks you to design a system where discipline is barely required.

How to simplify your budget

Most budgets fail not because people lack math skills but because the budget itself is too complicated to maintain. Minimalism budgeting tips almost always start with the same move: cut your categories down to three or four.

Pick a model that matches how you think

Three minimalist budgeting models work well depending on your personality. The two-bucket model separates fixed needs from everything else. Rent, utilities, insurance, and debt payments go in bucket one. Everything else goes in bucket two, and you spend freely within it. The priority-first model pays yourself first by automating savings at the top of each pay cycle, then spends whatever remains. The weekly allowance model converts your monthly discretionary spending into a single weekly number. You spend that amount however you like. When it’s gone, you wait for next week.

Start with a spending audit

Before you redesign your budget, run a 30-day spending audit to see exactly where your money goes. Most people are surprised. Subscriptions they forgot about, food delivery that adds up faster than expected, and impulse purchases that felt small individually. The audit isn’t about judgment. It’s about information. You can’t simplify what you haven’t measured.

Automate the most important transfers

Simpler budgets with automation consistently outperform detailed budgets that rely on active tracking. Set up automatic transfers to savings the day after your paycheck hits. Automate your bills so nothing slips. This approach turns your budget from a daily task into a system that runs in the background while you live your life.

Pro Tip: Set your savings transfer for one or two days after your paycheck deposits. You’ll never see the money sitting in your checking account, which means you’ll never feel tempted to spend it.

Also, consider how to budget effectively by focusing on your baseline expenses first. Know the exact minimum your life costs each month. That number becomes your anchor for every other financial decision.

Cutting impulse spending and financial noise

Impulse buying isn’t a character flaw. It’s a design problem. Environmental cues and algorithmic signals are engineered to trigger purchases before your rational brain can intervene. The minimalist solution isn’t to develop stronger willpower. It’s to change your environment.

Here are four practical steps to reduce impulsive spending:

- Unsubscribe from retail emails. Every promotional email in your inbox is a small persuasion attempt. Removing them from your environment takes the temptation off the table before it becomes a decision.

- Delete shopping apps from your phone. Friction matters. If making a purchase requires sitting at a computer rather than tapping a phone screen, you’ll make significantly fewer impulse buys.

- Use a shopping moratorium for specific categories. Time-boxed bans on purchasing within a particular category, like clothing or home goods, for 30 or 60 days break the habit loop without requiring permanent sacrifice. After the moratorium, many people find they didn’t miss those purchases at all.

- Delay purchases with a 48-hour rule. Add items to a wishlist instead of a cart. Wait two days. You’ll be surprised how often the desire fades.

Research confirms that reducing retail stimulus exposure directly lowers impulsive buying behavior. It’s not about being more disciplined. It’s about putting fewer temptations in your path.

Pro Tip: Replace the habit of browsing retail sites with a different low-cost activity. The goal is to fill the time slot, not just remove the behavior. Substitution works far better than pure elimination.

Living with less money doesn’t mean living with less. It means spending less in minimalism on things that don’t actually move the needle on your happiness or your goals.

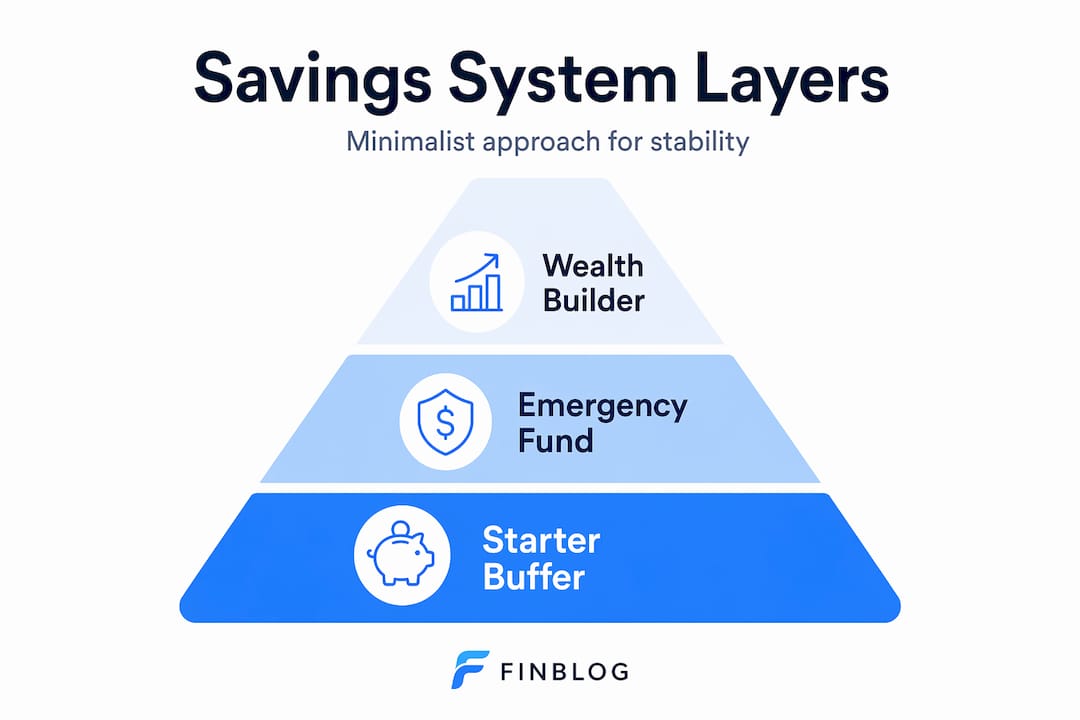

Building a savings system that runs itself

The most effective savings strategy isn’t the one with the highest return. It’s the one you actually follow. A minimalist money management approach treats your savings setup as an operating system: define the rules once, then let them run.

Here’s a simple framework for building that system:

| Savings Layer | Purpose | Suggested Target |

|---|---|---|

| Starter buffer | Absorbs small unexpected costs without disrupting the budget | $500 |

| Core emergency fund | Covers essential expenses if income stops temporarily | 3 months of baseline expenses |

| Goal-based savings | Funds specific priorities like travel, home purchase, or education | Variable by goal |

| Automated investing | Builds long-term wealth through consistent contributions | 10-15% of gross income |

Automation with clear triggers transforms financial minimalism from an intention into an operating system. Each of these layers gets its own automatic transfer on a fixed schedule. You don’t think about it each month. The system handles it.

One critical habit that minimalism and financial freedom share: delay lifestyle inflation. When your income increases, resist immediately upgrading your spending. Direct a significant portion of any raise directly to savings or investments before you adjust your lifestyle at all. Most people do the opposite, which is why income increases rarely produce proportional improvements in financial security.

53% of adults cite inflation as their top financial concern. A minimalist system provides a buffer here because you’ve already identified your true baseline expenses and built savings layers above them. When prices rise, you know exactly where you stand.

The holiday spending problem is worth addressing specifically. 60% of Americans feel stressed approaching the holiday season, with only 26% feeling confident about managing their spending. A minimalist solution is to set a total holiday spending number in October and automate monthly transfers to a dedicated sub-account starting in January. By December, the money is already there and the decision is already made. No stress, no debt.

You can explore financial wellness routines that incorporate these automation principles to make consistency a structural feature rather than a motivational effort.

My take on financial minimalism

I’ve spent years looking at how people manage money, and the pattern I see most often isn’t recklessness. It’s complexity fatigue. People build elaborate budget systems, open accounts for every spending category, and track everything with meticulous spreadsheets. Then life gets busy and the system collapses in two weeks.

What actually works, in my experience, is something far simpler. Fewer accounts. Fewer decisions. More automation. When I shifted from a detailed category budget to a two-bucket model with automated savings, I spent less time thinking about money and actually saved more. The irony is real: less structure produced better outcomes.

The emotional side of financial minimalism gets overlooked in most articles. Money carries weight beyond numbers. Overspending is often tied to stress, boredom, or social comparison. A minimalist approach to finances doesn’t just change your system. It changes your relationship with spending. When you’ve already decided what matters to you financially, random purchases lose their appeal. You’ve pre-committed to your values, and that pre-commitment is surprisingly powerful.

My honest advice: don’t try to fix everything at once. Start with one account consolidation, one automated transfer, or one subscription cancellation. The system builds on itself, and the early wins create real momentum.

— Povilas

Take the next step with Finblog

If this article gave you a clearer picture of how minimalism and money fit together, Finblog has more to help you go further. The guides on managing financial stress and building lasting financial habits go deeper into the psychology and practice of intentional money management. For investors looking to apply these same principles to their trading and portfolio discipline, this guide to financial security for traders is a practical companion. Whether you’re starting from scratch or refining a system that already exists, Finblog’s content library is built to give you clarity, not complexity.

FAQ

What is financial minimalism?

Financial minimalism is the practice of simplifying your money system by reducing accounts, automating savings, and aligning spending with personal values rather than habits or impulses.

How do minimalism budgeting tips differ from regular budgeting?

Minimalist budgeting uses fewer categories and relies heavily on automation, reducing the daily effort required to track spending and making consistency far more achievable over time.

Can a minimalist approach really reduce financial stress?

Yes. Pre-decided spending rules and automated systems reduce the number of financial decisions you face daily, which research links directly to lower financial anxiety and better spending confidence.

How do I start living with less money stress?

Begin with a 30-day spending audit to understand your actual expenses, then consolidate accounts, cancel unused subscriptions, and set up one automatic savings transfer before changing anything else.

Does minimalism and financial freedom actually connect?

Absolutely. Fewer fixed expenses and automated saving accelerate wealth-building by reducing lifestyle inflation and eliminating financial complexity that typically erodes savings over time.