Managing money can feel overwhelming, especially when the numbers never seem to add up. Nearly 60 percent of Americans report feeling anxious about their finances, even if they have a steady income. But what if the real problem is not the size of your paycheck, but the way you approach your financial stress in the first place?

Table of Contents

- Step 1: Assess Your Current Financial Situation

- Step 2: Identify Key Stressors Impacting Your Finances

- Step 3: Develop A Strategic Budget Plan

- Step 4: Implement Stress-Reduction Techniques

- Step 5: Monitor Progress And Adjust Accordingly

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Create a Financial Snapshot | Gather three months of financial documents to assess income and spending patterns effectively. |

| 2. Identify Financial Stressors | Document specific financial challenges and categorize them to understand their impact on your financial anxiety. |

| 3. Develop a Strategic Budget | Establish clear financial goals and use the 50/30/20 rule to allocate funds effectively across expenses and savings. |

| 4. Implement Stress-Reduction Techniques | Use mindfulness and technology to build resilience against financial anxiety while managing your budget and goals. |

| 5. Monitor and Adjust Your Plan | Regularly review your financial progress, making necessary adjustments with a growth mindset to stay on track. |

Step 1: Assess Your Current Financial Situation

Effective financial stress management begins with a clear understanding of your current financial landscape. This critical first step involves creating a comprehensive snapshot of your financial health, allowing you to develop targeted strategies for improvement. Think of it as a personal financial diagnostic test that reveals where you stand and highlights potential areas of concern.

To start, gather all your financial documents in one place. This includes bank statements, credit card bills, loan documents, investment account summaries, pay stubs, and any other financial records. Pull together at least the last three months of financial documentation to get an accurate representation of your income and spending patterns. Digital tools like spreadsheet software or budgeting apps can help you organize this information efficiently.

Calculate your total monthly income by adding up all sources of earnings, including your primary job, side hustles, investments, and any additional revenue streams. Next, track your monthly expenses meticulously. Categorize your spending into essential categories like housing, utilities, food, transportation, and debt payments. Pay special attention to discretionary spending such as entertainment, dining out, and shopping, which often represent hidden areas of potential financial optimization.

The goal is to create a crystal-clear picture of your financial cash flow by comparing your total income against your total expenses. This calculation will reveal whether you are living within your means or potentially overspending. If your expenses consistently exceed your income, it signals an urgent need for financial restructuring. Conversely, if you have a surplus, you can strategically allocate those funds toward savings, debt reduction, or investment opportunities.

Verify your financial assessment by checking these key indicators:

- Your monthly expenses are less than or equal to your monthly income

- You have a clear understanding of all income sources

- You can identify specific areas of unnecessary spending

- You know your total debt and monthly debt obligations

By completing this foundational step, you transform financial uncertainty into actionable knowledge. This comprehensive assessment sets the stage for developing targeted strategies to manage financial stress and create a more secure financial future.

Below is a checklist table to help you verify completion of your financial assessment and ensure all critical review points are covered.

| Verification Step | Description |

|---|---|

| Income vs. Expenses | Confirm monthly expenses are less than or equal to your monthly income. |

| Income Clarity | Ensure you understand all sources of income. |

| Spending Awareness | Identify specific areas where you spend unnecessarily. |

| Debt Clarity | Know your total debt and all monthly debt obligations. |

Step 2: Identify Key Stressors Impacting Your Finances

Building upon your initial financial assessment, the next crucial step in financial stress management involves pinpointing the specific factors creating tension in your financial life. Understanding these stressors allows you to develop targeted strategies that address root causes rather than merely treating symptoms.

Financial stress often emerges from multiple interconnected sources, making a systematic approach essential. Begin by conducting an honest self-examination of your financial pain points. This process requires vulnerability and self-reflection, recognizing that external pressures and personal financial habits both contribute to your overall financial anxiety. Common stressors typically include recurring debt, inconsistent income, excessive spending, inadequate emergency savings, and unexpected financial obligations.

Create a comprehensive stress inventory by documenting each financial challenge you currently face. Write down specific scenarios that trigger anxiety, such as credit card balances, upcoming large expenses, job instability, or significant debt repayments. Managing credit card debt represents a prime example of a focused financial stressor that many individuals struggle with systematically.

To effectively map your financial stressors, break them down into distinct categories: short-term challenges, long-term financial concerns, and potential future risks. Short-term challenges might include monthly bill payments or immediate debt obligations. Long-term concerns could involve retirement planning, investment strategies, or major life transitions. Potential future risks encompass scenarios like potential job loss, medical emergencies, or significant economic shifts.

Verify your financial stressor identification by checking these critical indicators:

- You can clearly articulate each financial challenge

- Each stressor is documented with specific details

- You understand the potential impact of each identified stressor

- You recognize both external and internal sources of financial pressure

By meticulously mapping your financial stressors, you transform abstract anxieties into concrete problems that can be strategically addressed. This comprehensive understanding becomes the foundation for developing precise, personalized financial stress management strategies in subsequent steps.

This table summarizes common financial stressors by category to help you organize and recognize root causes impacting your financial situation.

| Stressor Category | Example Stressors | Impact |

|---|---|---|

| Short-term Challenges | Monthly bill payments, immediate debt obligations | Immediate cash flow issues |

| Long-term Concerns | Retirement planning, major life transitions | Affects future security |

| Potential Future Risks | Job loss, medical emergency, economic shifts | Leads to instability or emergency need |

Step 3: Develop a Strategic Budget Plan

Transforming your financial stress into controlled financial planning requires creating a strategic budget that goes beyond simple expense tracking. A well-crafted budget serves as a powerful roadmap, guiding your financial decisions and providing a sense of control over your monetary ecosystem.

Start by establishing clear, realistic financial goals that align with your current income and expenses. These objectives might include debt reduction, emergency fund creation, or saving for significant life milestones. Prioritize your goals by understanding which are most critical to your immediate financial stability and long-term financial health. How to Budget Effectively can provide additional insights into structuring your financial plan.

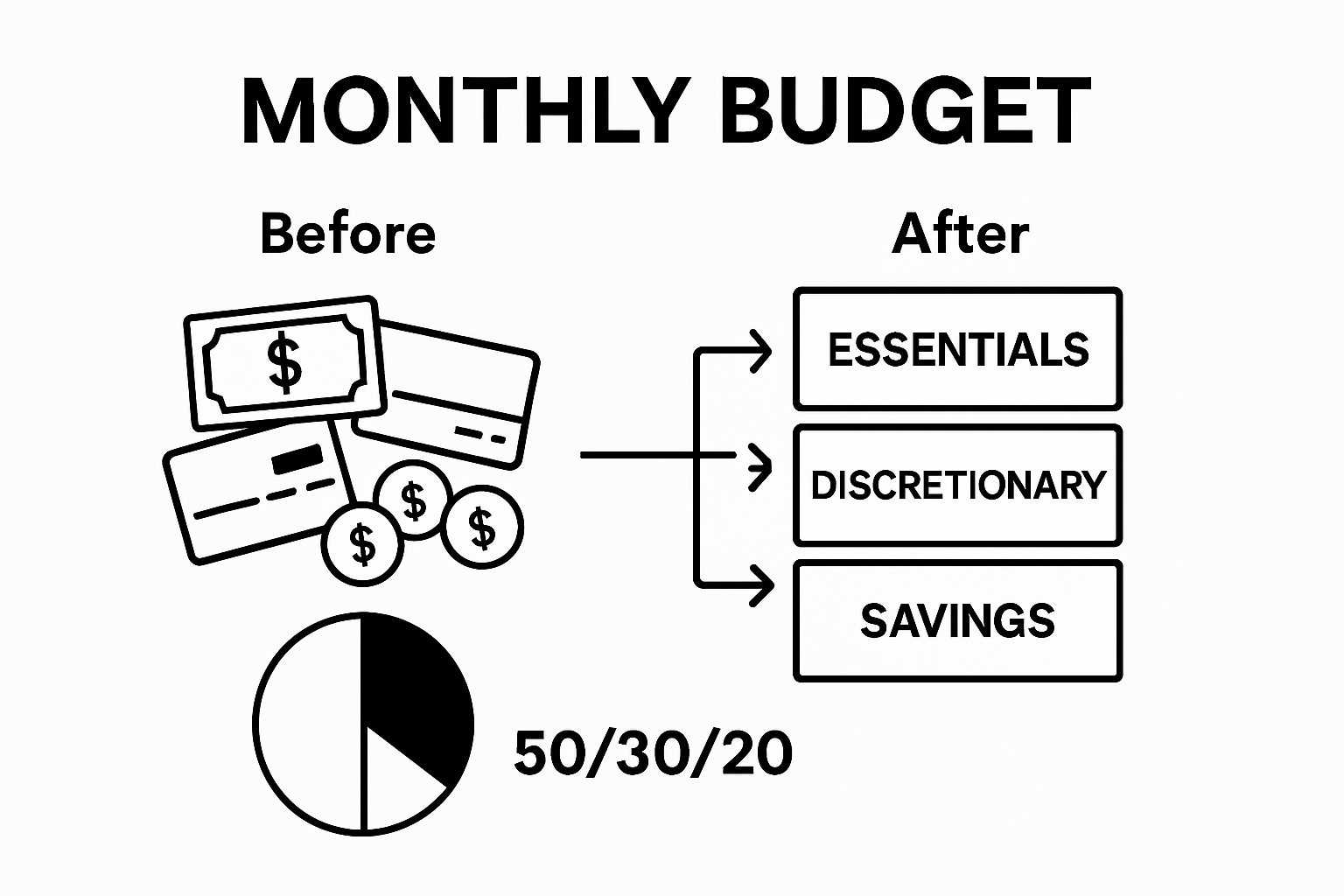

Implement the 50/30/20 budgeting framework as a foundational strategy. This approach allocates 50% of your after-tax income to essential expenses like housing, utilities, and groceries. Dedicate 30% to discretionary spending, which includes entertainment, dining out, and personal purchases. The remaining 20% goes directly toward financial goals such as debt repayment, savings, and investments. This structured method helps prevent overspending while ensuring consistent progress toward your financial objectives.

Digital tools and budgeting apps can significantly streamline your budget management process. Choose platforms that offer real-time expense tracking, automatic categorization, and visual representations of your spending patterns. These technologies provide immediate insights into your financial behavior, allowing you to make rapid adjustments and maintain budget discipline. Look for applications that sync with your bank accounts, providing comprehensive and up-to-date financial snapshots.

Verify your strategic budget plan by checking these key indicators:

- Your budget allocates funds to all essential expense categories

- You have a clear plan for managing discretionary spending

- Your financial goals are explicitly defined and measurable

- You have identified digital tools to support ongoing budget management

By developing a strategic budget plan, you transform financial uncertainty into a structured approach that reduces stress and creates a pathway to financial resilience. This methodical strategy empowers you to take control of your financial narrative, turning potential anxiety into purposeful action.

Use the following checklist table to quickly verify if your strategic budget plan covers all major requirements for long-term financial health.

| Completion Criteria | What to Check |

|---|---|

| Fund Allocation | All essential expense categories receive budgeted funds |

| Discretionary Plan | Plan exists for managing discretionary spending |

| Goal Definition | Financial goals are clear and measurable |

| Digital Support | Tools or apps identified for budget management |

Step 4: Implement Stress-Reduction Techniques

Transitioning from financial planning to stress management requires a holistic approach that addresses both psychological and practical aspects of financial anxiety. Effective stress-reduction techniques go beyond simple relaxation, creating a comprehensive strategy to build emotional resilience and maintain financial well-being.

Mindfulness and breathing exercises represent powerful tools for immediate stress relief. Develop a daily practice of deep breathing techniques that can be performed anywhere, taking five to ten minutes to focus on slow, deliberate breaths. This approach helps activate your body’s natural relaxation response, reducing cortisol levels and providing mental clarity during financially challenging moments. Practice a simple technique like the 4-7-8 method: inhale for four seconds, hold for seven seconds, and exhale for eight seconds, repeating this cycle four to five times.

Combine psychological strategies with practical financial actions to create a comprehensive stress management approach. Financial planning for freelancers often requires additional stress management techniques, but these strategies apply universally. Establish a dedicated financial self-care routine that includes regular financial check-ins, where you review your budget, track progress toward goals, and make necessary adjustments. Schedule these sessions during low-stress times, perhaps on a weekend morning with a cup of coffee, transforming potentially anxiety-inducing financial review into a calm, constructive experience.

Technology can be a powerful ally in stress reduction. Utilize meditation apps, financial tracking tools, and stress management platforms that provide guided relaxation techniques specifically designed for financial anxiety. Set up automated alerts that provide positive reinforcement when you meet budget goals or make progress on debt reduction. These digital companions can help reframe your financial journey from a source of stress to a path of empowerment and continuous improvement.

Verify your stress-reduction implementation by checking these key indicators:

- You have a consistent daily mindfulness or breathing practice

- You conduct regular, calm financial review sessions

- You use technology to support both financial and emotional well-being

- You can recognize and interrupt stress responses quickly

By implementing these targeted stress-reduction techniques, you transform financial anxiety from an overwhelming challenge into a manageable aspect of your personal growth journey. Each deliberate action builds resilience, creating a more balanced and confident approach to your financial future.

Here is a checklist table summarizing the key steps for implementing effective stress-reduction techniques to manage financial anxiety.

| Implementation Step | Indicator of Completion |

|---|---|

| Mindfulness Practice | Daily breathing or mindfulness exercise established |

| Financial Check-Ins | Regular, low-stress financial review sessions occur |

| Tech Support | Technology or apps used for emotional and financial wellbeing |

| Stress Interruption | Can recognize and disrupt stress responses quickly |

Step 5: Monitor Progress and Adjust Accordingly

The final stage of financial stress management involves creating a dynamic, responsive system that evolves with your changing financial landscape. Monitoring progress is not a one-time activity but an ongoing process of evaluation, reflection, and strategic adaptation that transforms your financial planning from static to strategic.

Establish a consistent financial review schedule that allows you to track your progress systematically. Choose a frequency that works for your lifestyle monthly or quarterly works best for most individuals. During these review sessions, compare your current financial situation against the goals and budget you established in previous steps. Look beyond simple number tracking analyze the emotional and practical aspects of your financial journey. Are you feeling more confident? Have your stress levels decreased? These qualitative measurements are just as important as quantitative metrics.

Building an investment portfolio requires similar principles of regular monitoring and adjustment. Use digital tools and spreadsheet applications to create visual representations of your financial progress. Graphs and charts can help you quickly understand trends, identify potential issues, and celebrate your achievements. Automated tracking apps can provide real-time insights, sending alerts when you deviate from your budget or when unexpected expenses arise.

Develop a flexible mindset that views financial adjustments as opportunities for growth rather than failures. If you discover that certain strategies aren’t working, approach these moments with curiosity and compassion. Perhaps your initial budget allocations were unrealistic, or unexpected life changes have impacted your financial landscape. The key is to remain adaptable, making incremental modifications that align with your evolving financial goals and personal circumstances.

Verify your progress monitoring by checking these key indicators:

- You have a regular, scheduled financial review process

- You use digital tools to track financial progress

- You can identify and explain changes in your financial situation

- You approach financial adjustments with a positive, growth-oriented mindset

By implementing a robust monitoring and adjustment strategy, you transform financial stress management from a reactive process to a proactive journey of continuous improvement. Each review becomes an opportunity to refine your approach, build resilience, and move closer to your ultimate financial objectives.

This checklist table helps verify you are consistently monitoring your financial progress and maintaining a flexible, growth-oriented approach.

| Monitoring Step | Confirm This is True |

|---|---|

| Review Schedule | Regular financial review sessions are scheduled |

| Digital Tools | Apps or spreadsheets help track progress |

| Change Awareness | Can explain significant changes in finances |

| Growth Mindset | Approach adjustments with positivity and flexibility |

Take Charge of Your Financial Confidence Today

You have just explored practical strategies to assess your finances, identify stressors, and create a resilient budget. If you are feeling overwhelmed by financial uncertainty or struggling to break out of the cycle of stress and reactive decision-making, you are not alone. Many people discover through honest financial assessment that constant anxiety, hidden debt, and a lack of clear direction can easily stall progress toward a secure future. Recognizing issues like unmanaged debt, inconsistent budgeting, or a missing support system is the first step toward real change—finblog.com gives you the tools and expert guidance to turn that knowledge into action.

Why wait to secure your financial future? With instant access to actionable resources and personalized consultation, you can move beyond surface-level advice. Visit finblog.com today to find proven guides on how to budget effectively, master stress-reduction techniques for your financial routine, and connect with experts who understand your unique challenges. Act now to receive thoughtful updates, guidance, and strategies that will keep you on track month after month. Start your journey to financial peace of mind and lasting confidence—take your next step with finblog.com.

Frequently Asked Questions

What is the first step in effective financial stress management?

Effective financial stress management begins with assessing your current financial situation. This involves gathering financial documents, calculating total income and expenses, and creating a comprehensive view of your financial health.

How can I identify the key stressors impacting my finances?

You can identify financial stressors by conducting a self-examination of your financial situation. Document specific challenges such as debt, inconsistent income, or unexpected expenses, and categorize them into short-term, long-term, and potential future risks.

What budgeting strategy should I consider for better financial management?

The 50/30/20 budgeting framework is a recommended strategy. Allocate 50% of your after-tax income to essentials, 30% to discretionary spending, and 20% to savings and debt repayment to create a balanced financial plan.

How do I monitor my progress in managing financial stress?

Establish a regular financial review schedule, such as monthly or quarterly. During these sessions, track your progress against your budget and goals, evaluate both quantitative and qualitative changes, and adjust your strategies as needed.