TL;DR:

- Inflation causes a sustained rise in prices that diminishes the purchasing power of money. It primarily results from demand-pull, cost-push factors, and monetary expansion, all influenced by inflation expectations. Central banks, especially the Federal Reserve, manage inflation through interest rate adjustments, which take months to impact the economy.

Inflation is defined as a sustained rise in the general price level of goods and services, which directly reduces the purchasing power of money. Understanding how inflation works is not just an academic exercise. It shapes your mortgage rate, your grocery bill, your retirement savings, and the interest you earn on a checking account. The Federal Reserve targets roughly 2% annual inflation as a healthy benchmark. The U.S. annual inflation rate hit 2.4% in January 2026, sitting just above that target. That single number ripples through every corner of the economy.

How does inflation work: causes and mechanisms

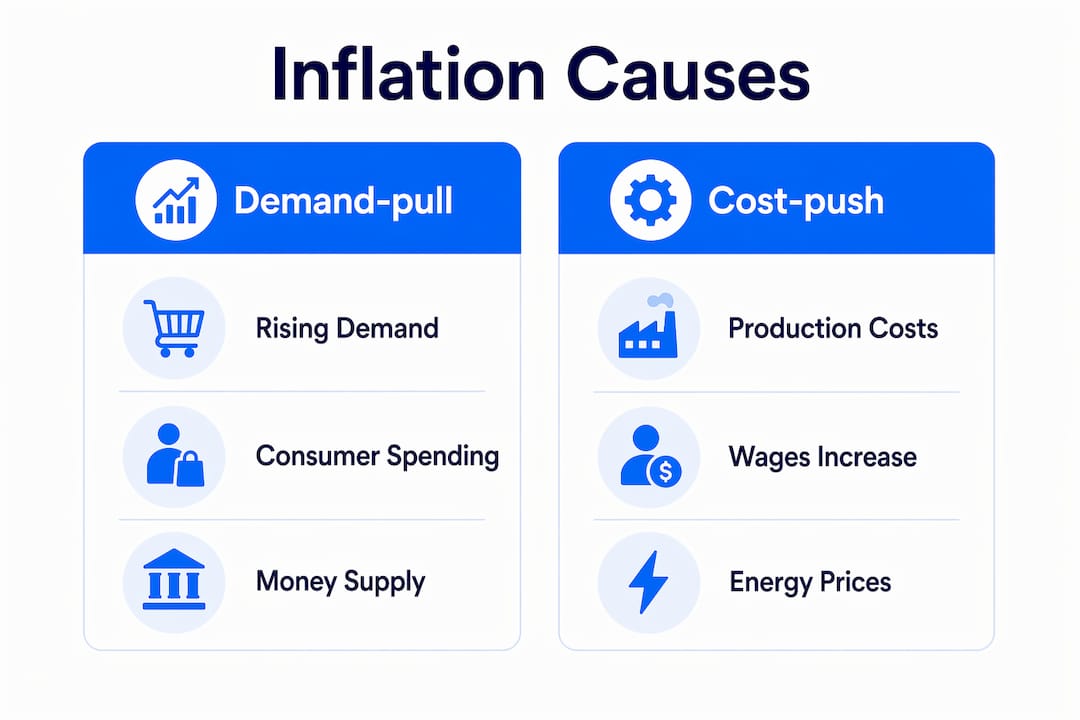

Inflation does not appear randomly. It follows two primary mechanisms: demand-pull and cost-push. Understanding both tells you why prices rise and how long that rise is likely to last.

Demand-pull inflation occurs when aggregate demand in an economy grows faster than supply. Think of the post-pandemic period in the U.S., when stimulus checks and pent-up consumer spending collided with supply chains that could not keep pace. Too many dollars chasing too few goods pushes prices up. This is the textbook definition of demand-pull in action.

Cost-push inflation works from the supply side. When production costs rise, such as wages, raw materials, or energy, businesses pass those costs on to consumers. The 1970s oil shocks are the clearest historical example. OPEC’s embargo sent energy prices soaring, which raised the cost of producing almost everything, from plastics to food.

The money supply also plays a direct role. When central banks like the Federal Reserve expand the money supply faster than economic output grows, each dollar in circulation buys less. Milton Friedman’s famous observation that “inflation is always and everywhere a monetary phenomenon” captures this relationship precisely.

External shocks accelerate both mechanisms. Supply chain disruptions, geopolitical conflicts, and commodity price spikes can trigger cost-push inflation almost overnight. The 2021–2023 U.S. inflation surge combined all three forces at once: demand stimulus, supply chain collapse, and energy price volatility.

One underappreciated driver is inflation expectations. When workers expect prices to rise 5% next year, they demand 5% wage increases. Businesses then raise prices to cover those wages. The expectation becomes self-fulfilling. This wage-price spiral is why central banks work hard to keep expectations anchored near their 2% target.

- Demand-pull: excess consumer demand outpaces supply

- Cost-push: rising input costs passed through to consumers

- Monetary expansion: more money in circulation relative to output

- External shocks: oil spikes, supply chain failures, geopolitical events

- Inflation expectations: anticipated price rises that embed themselves into wages and contracts

Pro Tip: Watch the University of Michigan Consumer Sentiment Survey each month. Its inflation expectations component is one of the earliest signals that a wage-price spiral may be forming, often before official CPI data catches up.

How is inflation measured using CPI and other indices?

Inflation measurement relies on price indices, and the two most important in the U.S. are the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index. Each tracks a different basket of goods and uses different weighting methods.

The Bureau of Labor Statistics calculates CPI by tracking the prices of a fixed basket of goods and services that a typical urban household buys. That basket includes housing, food, transportation, medical care, and education. Each category carries a weight based on how much consumers actually spend on it. Housing, for example, accounts for roughly one-third of the total CPI weight. US CPI inflation is projected at 2.7% for 2026, while UK CPI rose 3.3% over the 12 months to March 2026. That gap reflects different energy policies, wage dynamics, and fiscal responses on each side of the Atlantic.

The PCE index, published by the Bureau of Economic Analysis, uses a broader basket and adjusts weights more frequently to reflect actual spending shifts. If beef prices spike and consumers switch to chicken, PCE captures that substitution. CPI does not adjust as quickly. The Federal Reserve prefers PCE, and specifically core PCE, as its primary inflation gauge.

| Index | Published By | Basket Type | Fed Preferred? |

|---|---|---|---|

| CPI | Bureau of Labor Statistics | Fixed basket, urban households | No |

| Core CPI | Bureau of Labor Statistics | Excludes food and energy | Partial |

| PCE | Bureau of Economic Analysis | Broader, adjusts for substitution | Yes |

| Core PCE | Bureau of Economic Analysis | Excludes food and energy | Primary target |

Headline inflation includes every item in the basket, including volatile food and energy prices. Core inflation strips those out to reveal the underlying trend. A cold winter that spikes natural gas prices will push headline inflation up sharply, but core inflation may barely move. Core PCE is considered a better predictor of long-term inflation trends precisely because it filters out that noise.

Pro Tip: Track both headline and core inflation each month. If headline is rising but core stays flat, the spike is likely temporary. If core starts climbing alongside headline, the inflation is structural and more persistent.

What is the real impact of inflation on your finances?

Inflation’s most direct effect is the erosion of purchasing power. If your salary rises 2% but inflation runs at 4%, you are effectively taking a pay cut. That gap between wage growth and price growth is where household financial stress originates.

The impact is not evenly distributed. Low-income households spend a larger share of their income on essentials like food, rent, and utilities. Those categories tend to inflate faster than discretionary goods. In the UK during 2024/25, 21% of working-age adults could not afford basic items, even as real median incomes grew 4.6%. For low-income households, that real income growth was only 1.7%. Inflation acts as a regressive force, hitting those with the least the hardest.

Borrowing costs rise with inflation because central banks raise interest rates to cool demand. A household carrying a variable-rate mortgage or credit card debt feels this immediately. A 1% rate increase on a $300,000 mortgage adds roughly $180 per month to the payment. That is money that cannot go toward savings or investment.

Savings accounts and fixed-income investments lose real value when inflation outpaces their returns. A savings account earning 1% while inflation runs at 3% is losing purchasing power at 2% per year. This is why financial advisors consistently recommend holding assets that historically outpace inflation, such as equities, Treasury Inflation-Protected Securities (TIPS), or real estate.

- Purchasing power falls when wages do not keep pace with prices

- Variable-rate debt becomes more expensive as central banks raise rates

- Low-income households face disproportionate strain on food and housing costs

- Cash savings lose real value in high-inflation environments

- Investment returns must exceed the inflation rate to build real wealth

Finblog’s guide on inflation and your savings covers specific strategies for protecting cash holdings. For investors, the impact on investment returns deserves its own analysis, particularly for bond portfolios and dividend stocks.

How do central banks control inflation?

Central banks are the primary line of defense against runaway inflation. The Federal Reserve uses the federal funds rate as its main tool. Raising that rate makes borrowing more expensive for banks, which in turn raises rates for consumers and businesses. Higher borrowing costs reduce spending and investment, which cools demand and slows price growth.

The transmission of monetary policy tools to the real economy follows a sequence:

- The Federal Reserve raises the federal funds rate target.

- Commercial banks raise their prime lending rates within days.

- Mortgage rates, auto loan rates, and credit card rates follow within weeks.

- Businesses reduce capital investment due to higher financing costs.

- Consumer spending slows as credit becomes more expensive.

- Demand falls, reducing upward pressure on prices over the following months.

The critical word in that sequence is “months.” Rate hikes take time to work through the economy. Households with variable-rate debt feel the payment increase immediately, but goods prices may not stabilize for six to eighteen months after the initial rate change. This lag creates a painful window where borrowing costs are high but inflation has not yet fallen.

Governments also use fiscal policy to manage inflation. Tax increases reduce disposable income, which cuts consumer demand. Spending cuts reduce government’s own contribution to aggregate demand. Both tools are politically difficult to deploy, which is why monetary policy carries most of the burden in practice.

The trade-off between controlling inflation and maintaining employment is real. The Phillips Curve relationship describes the historical inverse link between inflation and unemployment. Aggressive rate hikes that crush inflation often push unemployment higher in the short term. The Federal Reserve’s dual mandate, price stability and maximum employment, reflects exactly this tension.

Key takeaways

Inflation reduces purchasing power through demand-pull and cost-push mechanisms, measured by CPI and PCE, and controlled primarily through Federal Reserve interest rate policy.

| Point | Details |

|---|---|

| Inflation definition | A sustained rise in the general price level that reduces what money can buy. |

| Two core causes | Demand-pull (excess demand) and cost-push (rising production costs) drive most inflation cycles. |

| Measurement tools | CPI and PCE track price changes; core versions exclude food and energy for trend analysis. |

| Household impact | Low-income households face the steepest burden as essentials inflate faster than wages. |

| Policy response | Federal Reserve rate hikes slow inflation but take months to affect consumer prices. |

Why most people misread inflation until it hits their wallet

I have spent years reading economic data, and the pattern I see most often is this: people treat inflation as an abstract news story right up until their grocery bill jumps $80 in a single month. Then it becomes very personal, very fast.

The most common misconception I encounter is that inflation is simply “prices going up.” That framing misses the mechanism entirely. Inflation is a relationship between money supply, demand, supply capacity, and expectations. When you understand that relationship, you stop being surprised by inflation and start anticipating it.

What I find genuinely underappreciated is the role of expectations. When inflation expectations become unanchored, wage-price spirals can persist long after the original shock has passed. The 1970s U.S. inflation did not end because oil prices fell. It ended because Paul Volcker at the Federal Reserve was willing to push the federal funds rate above 20% and accept a deep recession to break those expectations. That is how powerful the psychology of inflation is.

My practical advice: stop watching headline CPI as your primary signal. Watch core PCE, watch wage growth data from the Bureau of Labor Statistics, and watch the University of Michigan inflation expectations survey. Those three together give you a far clearer picture of where inflation is heading than any single monthly print.

For your own finances, the question is not whether inflation will affect you. It will. The question is whether your income, savings, and investments are positioned to outpace it. If your savings are sitting in a low-yield account while inflation runs above 2%, you are losing ground every month. That is not a crisis, but it is a slow leak worth fixing.

— Povilas

Protect your finances with finblog’s inflation resources

Inflation does not wait for you to feel ready. The gap between understanding inflation and acting on that understanding is where real financial damage accumulates. Finblog has built a set of practical guides specifically for investors and savers navigating inflationary periods. Whether you want to understand how rising prices affect your savings account or you are looking for proven wealth protection strategies during high-inflation cycles, the resources are there. For a broader view of how the Bank of England is responding to current conditions, Finblog’s analysis of UK inflation trends provides useful context. Start with the guides most relevant to your situation and build from there.

FAQ

What is the simplest definition of inflation?

Inflation is a sustained increase in the general price level of goods and services that reduces the purchasing power of money over time. The Federal Reserve targets approximately 2% annual inflation as a stable benchmark.

What causes inflation to rise suddenly?

Sudden inflation spikes are typically caused by demand surges, supply chain disruptions, or sharp increases in energy prices. All three forces combined during the 2021–2023 U.S. inflation cycle, producing the highest inflation rates in four decades.

How is inflation measured in the united states?

The U.S. measures inflation primarily through the Consumer Price Index (CPI) and the Personal Consumption Expenditures (PCE) index. The Federal Reserve focuses on core PCE, which excludes volatile food and energy prices, as its preferred long-term inflation indicator.

Is inflation good or bad for the economy?

Low, stable inflation around 2% supports economic growth by encouraging spending and investment. Inflation above that level erodes purchasing power, raises borrowing costs, and disproportionately harms low-income households who spend more of their income on essentials.

How does inflation affect investment returns?

Inflation reduces the real return on any investment that does not outpace it. A bond yielding 3% during a 4% inflation period delivers a negative real return. Assets like equities, real estate, and Treasury Inflation-Protected Securities (TIPS) historically offer better protection against inflation over the long term.