TL;DR:

- Effective budgeting ensures each dollar fulfills a purpose by allocating income across needs, wants, and savings.

- Choosing the right method depends on your income predictability and personality, not discipline, to avoid failure.

Good budgeting techniques are structured methods for allocating your income across needs, wants, and savings so every dollar serves a purpose. The most recognized frameworks include the 50/30/20 rule, zero-based budgeting, the envelope method, and pay-yourself-first. Each approach works differently depending on your income type, spending habits, and financial goals. Choosing the wrong method for your personality is the leading reason budgets fail, not lack of willpower. This guide breaks down how each method works, which one fits your situation, and how to build a plan that holds up over time.

What are the most effective budgeting techniques?

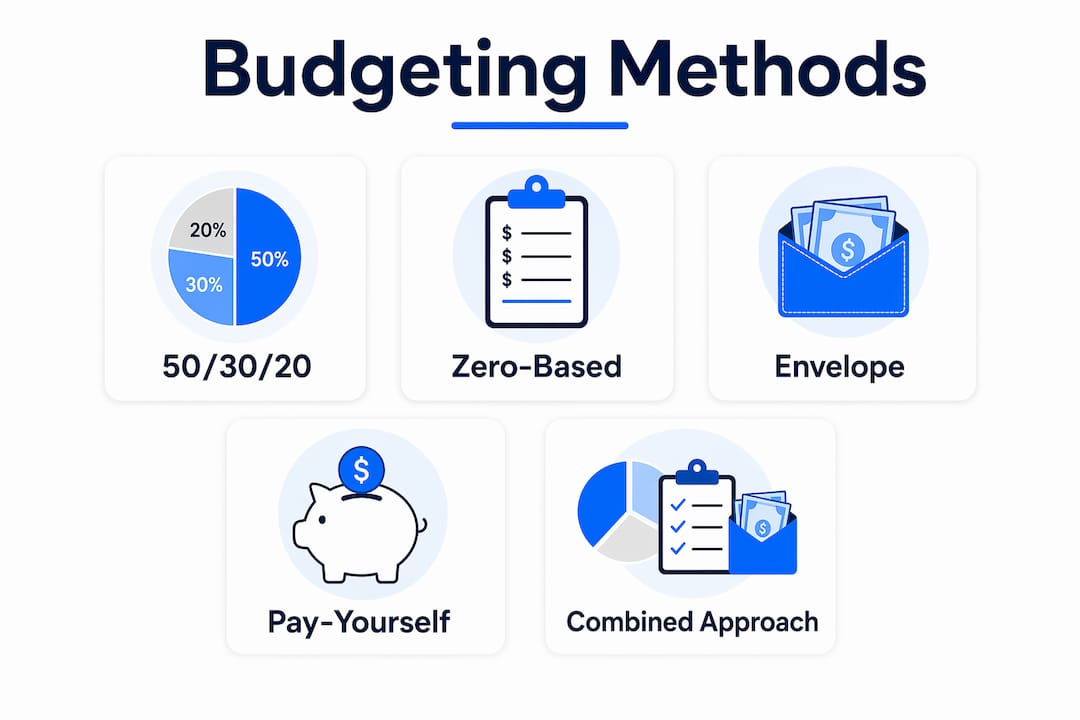

The 50/30/20 rule is the most commonly recommended starting point for personal budgeting. It divides your after-tax income into three categories: 50% for needs like rent and groceries, 30% for wants like dining out and subscriptions, and 20% for savings and debt repayment. The simplicity of this structure makes it ideal for beginners who want a clear framework without tracking every transaction.

Zero-based budgeting takes a more detailed approach. Every dollar of income gets assigned to a specific category until income minus expenses equals zero. This method requires 20–60 minutes of monthly planning and delivers the tightest control over spending. It works best for people paying down debt or those who want to know exactly where every dollar goes.

The envelope method uses physical cash divided into labeled envelopes for each spending category. When an envelope is empty, spending in that category stops for the month. This tactile approach is especially effective for people who overspend on discretionary categories like food or entertainment.

Pay-yourself-first flips the traditional budgeting order. You move a set amount into savings the moment your paycheck arrives, before any bills or spending. This method removes the temptation to spend savings and works well for people who struggle to save from what is left over at month’s end.

| Method | Complexity | Time per month | Best for |

|---|---|---|---|

| 50/30/20 rule | Low | Under 30 minutes | Beginners, steady earners |

| Zero-based budgeting | High | 20–60 minutes | Debt payoff, detail-oriented |

| Envelope method | Medium | 30–45 minutes | Overspenders, cash users |

| Pay-yourself-first | Low | Under 15 minutes | Savings-focused, hands-off |

Pro Tip: Start with the 50/30/20 rule for your first two months. Once you understand your actual spending patterns, you can shift to a more detailed method like zero-based budgeting if you want tighter control.

How does your income type affect which method fits you?

Income predictability directly shapes which budgeting method works for you. A salaried worker with the same paycheck every two weeks can build a fixed budget around the 50/30/20 rule or zero-based budgeting with confidence. A freelancer or gig worker with variable monthly income needs a more flexible structure.

Freelancers and gig workers benefit most from the envelope method or pay-yourself-first. Both approaches adapt to income that changes month to month. The envelope method lets you adjust category amounts each month based on what you actually earned. Pay-yourself-first works by setting a savings percentage rather than a fixed dollar amount, so it scales with income naturally. Finblog covers freelancer financial planning in detail for anyone managing unpredictable cash flow.

Personality matters just as much as income type. Budgeting fails most often when the chosen method clashes with a person’s natural temperament, not because of a lack of discipline. Detail-oriented people who enjoy tracking numbers tend to thrive with zero-based budgeting. People who find detailed tracking exhausting do better with the 50/30/20 rule or pay-yourself-first.

Here is a quick guide to matching method to profile:

- Steady income, detail-oriented: Zero-based budgeting gives you full control and visibility.

- Steady income, hands-off: The 50/30/20 rule requires minimal tracking and still builds savings.

- Variable income, disciplined: Envelope method with monthly adjustments keeps spending in check.

- Variable income, savings-focused: Pay-yourself-first protects savings even in low-income months.

- Values-driven spender: A values-based budget, where you allocate money to what matters most to you personally, increases long-term adherence better than fixed-percentage methods alone.

Common budgeting mistakes and how to avoid them

Most budgets fail within the first 60 days. The cause is almost always a structural problem, not a motivation problem. Knowing the most common mistakes lets you build a plan that survives contact with real life.

-

Setting aspirational amounts instead of realistic ones. Your first budget must be built on actual past spending, not what you wish you spent. Pull three months of bank and credit card statements before setting any category limit. If you spent $600 on groceries last month, budgeting $250 this month will fail by week two.

-

Ignoring irregular expenses. Car repairs, annual insurance premiums, holiday gifts, and medical copays do not appear every month. Ignoring these expenses causes most budget failures within 60 days. Sinking funds solve this: divide the annual cost of each irregular expense by 12 and set that amount aside monthly.

-

Cutting all discretionary spending at once. Removing every non-essential expense creates a budget that feels like punishment. Budgets that include a small “fun money” category last longer because they do not require perfection. Even $30 to $50 per month for guilt-free spending reduces the urge to abandon the whole plan.

-

Skipping monthly reviews. A budget set in january and never revisited becomes irrelevant by march. Life changes, and your budget needs to change with it. Schedule a 20-minute review at the end of each month to compare what you planned against what you actually spent.

-

Treating a budget failure as a total failure. One overspent category does not mean the budget is broken. Adjust the category for next month and move on. Consistency over months matters far more than perfection in any single week.

Pro Tip: Create a dedicated sinking fund for car expenses, medical costs, and annual subscriptions. Add up what you spent on these in the past year, divide by 12, and transfer that amount monthly into a separate savings account.

How to implement your budget and keep it working

Setting up a budget that actually holds requires a clear starting process. Skipping steps early leads to the same problems most people hit: unrealistic numbers, missing categories, and no system for tracking. Follow these steps to build a plan that works from day one.

- Audit your income and expenses honestly. List every income source and every expense from the past three months. Include subscriptions, annual fees, and irregular costs. This audit is the foundation of any effective budgeting method.

- Choose a method that matches your profile. Use the income type and personality guide above. Do not pick a method because it sounds impressive. Pick the one you will actually use.

- Set category amounts based on your audit. Start with what you actually spend, then make small, realistic reductions where you want to cut back. Aim for changes of 10–15% in any category, not 50%.

- Track spending weekly, not monthly. Weekly check-ins catch overspending before it compounds. A simple spreadsheet, a notes app, or a financial planning tool all work. The tool matters less than the habit.

- Automate savings transfers. Set up an automatic transfer to savings on payday. Automation removes the decision entirely and makes pay-yourself-first work even for people who forget to save manually.

- Review and adjust every month. Treat your budget as a living document. Adjust category amounts when your life changes, not just when the budget breaks.

Combining methods is also a legitimate strategy. Many people use pay-yourself-first to protect savings, then apply the 50/30/20 rule to the remainder. Others use zero-based budgeting for three months to understand their spending, then switch to a simpler method once patterns are clear. The goal is a system you will maintain, not a system that looks perfect on paper. Finblog’s guide on how to create a budget walks through each setup step in detail.

Key Takeaways

The most effective budgeting technique is the one that matches your income type, personality, and spending habits, not the one that sounds most disciplined.

| Point | Details |

|---|---|

| Match method to personality | Detail-oriented people succeed with zero-based budgeting; hands-off spenders do better with 50/30/20. |

| Build from real spending data | Base your first budget on three months of actual expenses, not aspirational targets. |

| Use sinking funds for irregular costs | Set aside monthly amounts for car repairs, gifts, and annual bills to prevent budget failure. |

| Automate savings first | Transfer savings on payday before spending to remove reliance on leftover funds. |

| Review monthly and adjust | A budget that is never updated becomes irrelevant within weeks. |

The method matters less than the fit

I have reviewed dozens of personal budgeting frameworks over the years, and the pattern is always the same. People do not fail at budgeting because they lack discipline. They fail because they picked a method that fights their natural behavior instead of working with it.

Zero-based budgeting gets the most praise in financial media. It is genuinely powerful for debt payoff. But I have watched detail-averse people try it, burn out in six weeks, and conclude they are “bad with money.” They are not. They just used the wrong tool. A hands-off person who automates savings with pay-yourself-first and loosely follows the 50/30/20 rule will outperform a detail-averse person grinding through zero-based budgeting every single time.

The other thing most articles skip: your budget should reflect your values, not a generic template. If travel is your priority, your budget should show that. If you are paying down debt aggressively, every category should reflect that urgency. A budget that ignores what you actually care about will not hold your attention past the first month.

Start simple. Track honestly. Adjust without guilt. That is the real framework behind every method that works.

— Povilas

Finblog’s resources for building your budget

Finblog offers a range of personal finance guides built for people who want practical, no-nonsense budgeting advice. Whether you are setting up your first budget or refining a plan that has not been working, the resources cover every stage of the process. From personal finance fundamentals to method-specific walkthroughs, the content is designed for real-world application. Visit Finblog to access budgeting guides, financial planning tools, and expert advice tailored to your goals.

FAQ

What is the best budgeting method for beginners?

The 50/30/20 rule is the best starting point for beginners. It divides income into needs, wants, and savings with minimal tracking required.

How long does it take to set up a zero-based budget?

Zero-based budgeting requires 20–60 minutes of planning per month. It is the most time-intensive method but delivers the tightest spending control.

Why do most budgets fail?

Budgets fail most often because the chosen method does not match the person’s temperament or income type, not because of a lack of effort. Starting with unrealistic spending targets also causes early burnout.

What is a sinking fund and why does it matter?

A sinking fund is a monthly savings amount set aside for irregular expenses like car repairs or annual subscriptions. Without sinking funds, unexpected costs break most budgets within 60 days.

Can you combine different budgeting methods?

Combining methods is a practical strategy. Many people use pay-yourself-first to protect savings, then apply the 50/30/20 rule to the remaining income for day-to-day spending.