Your credit score is more than just three digits. The difference between a top score and a poor one can mean paying tens of thousands of dollars extra on a single mortgage. Most people think credit scores are only about qualifying for loans or credit cards. That number actually has the power to shape your job offers, your housing choices, and even your insurance rates in ways few expect.

Table of Contents

- What Is A Credit Score And How Is It Calculated?

- Why Does A Credit Score Matter In Personal Finance?

- How Credit Scores Affect Loans And Interest Rates

- Key Factors That Influence Your Credit Score

- Real-World Examples Of Credit Score Impact

Quick Summary

| Takeaway | Explanation |

|---|---|

| A high credit score saves money. | Favorable interest rates can save thousands over the life of a loan. |

| Payment history is crucial. | Timely payments impact 35% of your credit score and can significantly lower it if missed. |

| Credit utilization should be low. | Keep it below 30% to demonstrate responsible credit management and improve your score. |

| Credit scores affect employment options. | Employers may check credit scores, and a low score can restrict job opportunities. |

| Diverse credit types enhance scores. | A mix of credit accounts shows financial responsibility and can positively influence your score. |

What is a Credit Score and How is it Calculated?

A credit score is a powerful financial metric that provides lenders with a snapshot of your creditworthiness and financial reliability. Think of it as a numerical representation of your financial trustworthiness, ranging typically from 300 to 850. The higher your score, the more likely you are to be approved for loans, credit cards, and receive favorable interest rates.

Understanding Credit Score Basics

At its core, a credit score is a statistical measure that evaluates the probability of you repaying borrowed money. Credit reporting agencies compile this score by analyzing your credit history and financial behaviors. The most widely used scoring model is the FICO score, which considers multiple financial factors to create a comprehensive assessment of your credit risk.

The key components that determine your credit score include:

- Payment History: Your track record of making timely payments

- Credit Utilization: The amount of credit you’re currently using compared to your total available credit

- Length of Credit History: How long you’ve maintained credit accounts

- Credit Mix: The variety of credit types you manage

- New Credit Inquiries: Recent applications for new credit

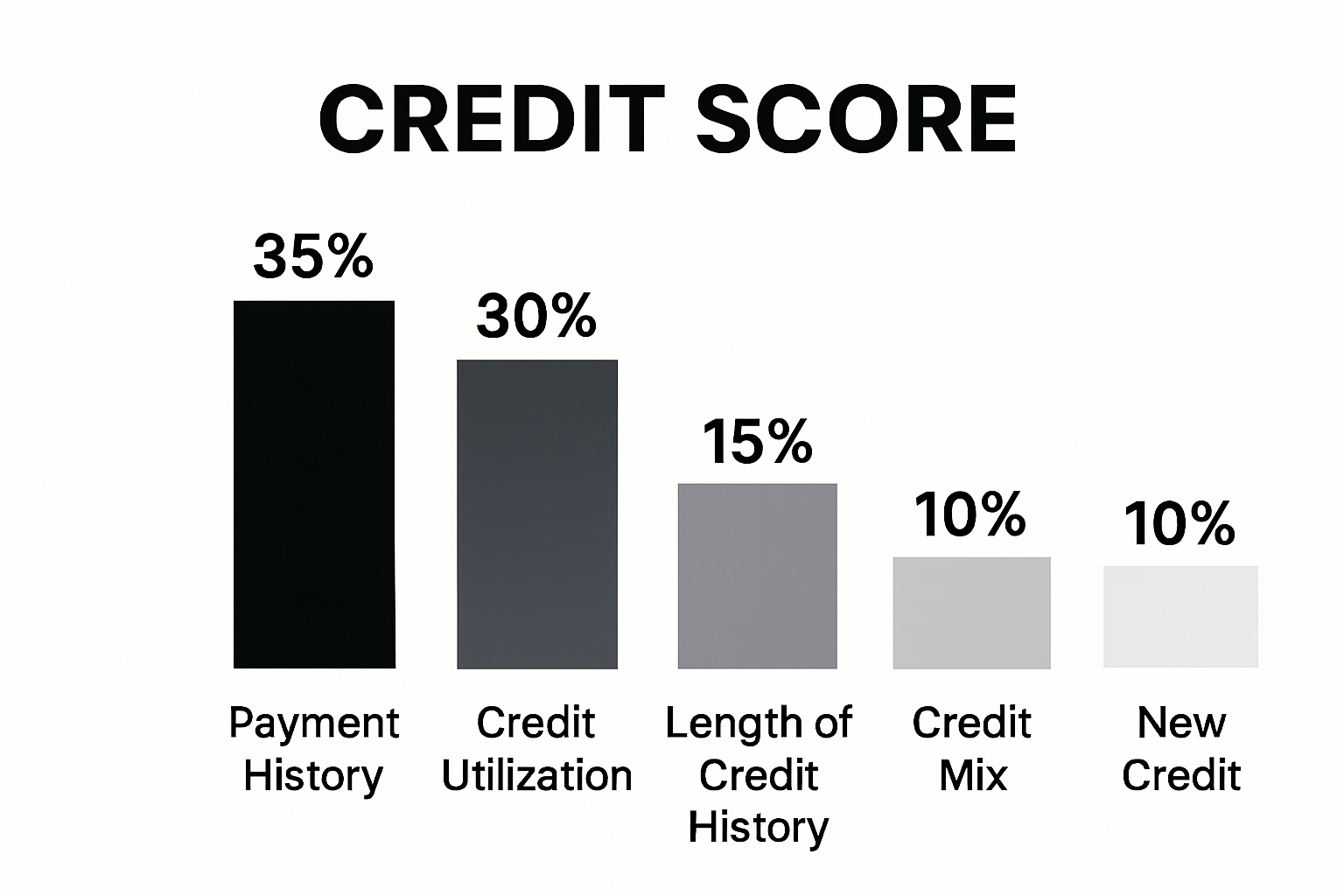

Calculating Your Credit Score

Each component of your credit score carries a different weight. According to research from the Federal Reserve, the breakdown typically looks like this:

- Payment History: 35%

- Credit Utilization: 30%

- Length of Credit History: 15%

- Credit Mix: 10%

- New Credit: 10%

For instance, consistently paying bills on time will positively impact your score, while missed payments or high credit card balances can significantly lower your rating.

The table below summarizes the main components of a credit score and their respective weightings, providing a clear reference for understanding what impacts your score most.

| Credit Score Component | Description | Weight in Score |

|---|---|---|

| Payment History | Record of on-time and missed payments across accounts | 35% |

| Credit Utilization | Ratio of used credit to available credit limit | 30% |

| Length of Credit History | How long you have maintained credit accounts | 15% |

| Credit Mix | Variety of credit types managed (credit cards, loans, etc.) | 10% |

| New Credit | Number of recent credit inquiries and newly opened accounts | 10% |

Why Does a Credit Score Matter in Personal Finance?

Your credit score is more than just a number. It is a critical financial passport that can unlock or restrict opportunities across multiple aspects of your financial life. Whether you are planning to buy a home, start a business, or simply manage your financial health, your credit score plays a pivotal role in determining your economic potential.

Financial Opportunities and Access

A strong credit score directly influences your ability to access financial resources. Lenders, landlords, and even potential employers use this score as a key indicator of your financial responsibility. According to research from Experian, a high credit score can translate into substantial financial advantages:

- Lower interest rates on loans and credit cards

- Higher approval chances for mortgages and rental applications

- Better terms for insurance policies

- Increased negotiating power with financial institutions

Consider a scenario where two individuals apply for a mortgage. The person with an excellent credit score might secure an interest rate 1-2% lower than someone with a poor score. Over a 30-year mortgage, this difference could mean saving tens of thousands of dollars.

Long-Term Financial Implications

Your credit score is not just about immediate financial transactions. It is a long-term financial health indicator that can impact your life trajectory. Research from the Federal Reserve reveals that credit scores influence:

- Employment opportunities in certain industries

- Potential business partnerships

- Personal and professional credibility

- Financial flexibility during economic uncertainties

Moreover, a good credit score can help you develop a robust financial plan by providing access to better financial products and lower-cost borrowing options. It serves as a foundation for building wealth and achieving long-term financial goals.

In essence, your credit score is a powerful financial tool. It reflects your financial discipline, provides access to opportunities, and can significantly impact your economic potential. Treating it with care and understanding its importance is crucial for anyone seeking financial stability and growth.

How Credit Scores Affect Loans and Interest Rates

Your credit score is not just a number. It is a powerful financial metric that directly influences the cost and accessibility of borrowing money. Lenders use this score as a critical tool to assess risk, determine loan terms, and set interest rates that reflect your financial reliability.

Loan Approval and Risk Assessment

According to Investopedia, credit scores serve as a comprehensive risk profile for financial institutions. Higher scores signal lower lending risk, which translates into more favorable financial opportunities. Lenders evaluate your creditworthiness through several key perspectives:

- Probability of Repayment: Higher scores indicate a stronger likelihood of timely loan repayment

- Financial Stability: Consistent credit management demonstrates responsible financial behavior

- Risk Mitigation: Lower scores suggest potential challenges in meeting financial obligations

For example, a borrower with a credit score above 750 might qualify for a mortgage with an interest rate of 4%, while someone with a score below 650 could face rates closer to 6% or higher. This seemingly small difference can result in tens of thousands of dollars in additional interest payments over the loan’s lifetime.

Below is a comparison table that shows how different credit score ranges correspond to typical interest rates and the impact on loan costs as described in the article.

| Credit Score Range | Typical Interest Rate | Lending Category | Impact on Loan Cost |

|---|---|---|---|

| 750-850 | Lowest (e.g., 4%) | Excellent Credit | Save tens of thousands in interest |

| 700-749 | Competitive | Good Credit | Lower rates, better terms |

| 650-699 | Moderate | Fair Credit | Higher rates, fewer options |

| 300-649 | Highest (e.g., 6%+) | Poor Credit | Much higher total loan cost |

Interest Rate Calculations

Research from the Consumer Financial Protection Bureau demonstrates that credit scores directly impact interest rate calculations. Lenders typically segment credit scores into distinct risk categories:

- Excellent Credit (750-850): Lowest interest rates

- Good Credit (700-749): Competitive interest rates

- Fair Credit (650-699): Moderate interest rates

- Poor Credit (300-649): Highest interest rates

Each credit score range represents a different level of perceived financial risk. The lower your score, the more expensive borrowing becomes. A poor credit score can mean paying significantly higher interest rates on personal loans, credit cards, mortgages, and auto financing.

Understanding how credit scores influence loans empowers you to make strategic financial decisions. By maintaining a strong credit profile, you can unlock more affordable borrowing options and save substantial money over time.

Key Factors That Influence Your Credit Score

Your credit score is a dynamic financial indicator that reflects your financial behavior and reliability. Understanding the key factors that shape this critical number can help you strategically manage and improve your financial health.

Payment History: The Most Critical Component

According to FICO, payment history represents the most significant factor in determining your credit score. This component accounts for approximately 35% of your total score and examines your track record of making timely payments across various financial obligations:

- Consistency in paying credit card bills

- Mortgage payment punctuality

- Personal loan repayment patterns

- Student loan payment records

- Frequency of late or missed payments

Every late payment can potentially lower your credit score, with more recent missed payments carrying a more substantial negative impact. A single 30-day late payment could reduce your score by 50-100 points, underscoring the critical importance of consistent, on-time payments.

Credit Utilization and Account Management

Research from Experian reveals that credit utilization and account management are equally crucial in credit score calculations. This factor focuses on how much credit you are using compared to your total available credit:

- Recommended credit utilization below 30%

- Lower utilization rates signal responsible credit management

- Maintaining low balances across credit accounts

- Avoiding maxing out credit cards

- Keeping older credit accounts open to demonstrate long-term stability

Credit scoring models look favorably upon consumers who demonstrate disciplined credit use. By keeping your credit utilization low and maintaining a diverse mix of credit accounts, you signal financial responsibility to potential lenders.

Understanding these factors empowers you to take proactive steps in managing your credit score. Consistent, strategic financial behavior can help you build and maintain a strong credit profile that opens doors to better financial opportunities.

Real-World Examples of Credit Score Impact

Credit scores are not abstract concepts but powerful financial tools that directly influence real-life opportunities and financial outcomes. Understanding these practical implications can help you appreciate the profound significance of maintaining a strong credit profile.

Employment and Professional Opportunities

Research from the Society for Human Resource Management reveals that many employers now include credit checks as part of their hiring process. A low credit score can potentially impact your professional prospects:

- Reduced chances in financial sector jobs

- Limited opportunities in management positions

- Potential barriers in roles requiring financial responsibility

- Higher scrutiny during background checks

- Potential disqualification for sensitive positions

Imagine two equally qualified candidates applying for a financial analyst position. The candidate with a higher credit score might have a significant advantage, as employers often view credit history as an indicator of personal reliability and professional discipline.

Housing and Rental Implications

According to TransUnion, credit scores play a crucial role in housing and rental decisions. Landlords and property managers use credit scores to assess potential tenants:

- Higher scores increase rental application approval rates

- Lower scores might require additional security deposits

- Potential requirement for a co-signer with excellent credit

- Negotiating power for rental terms

- Access to more desirable housing options

A person with an excellent credit score might secure an apartment with lower upfront costs and more favorable lease terms, while someone with a poor credit score could face significant barriers in finding suitable housing.

Your credit score is a powerful financial passport that extends far beyond simple loan approvals. It influences professional opportunities, housing options, and overall financial flexibility. By understanding and actively managing your credit score, you can unlock numerous personal and professional advantages.

Take Control of Your Financial Future with Expert Credit Score Guidance

Are you worried about how your credit score might limit your financial opportunities? Many people, just like you, face the stress of loan rejections, high interest rates, or missed housing options because of a number that may not reflect their real potential. Your credit score plays a crucial role in shaping your financial experiences, from loan approvals to job prospects. Ignoring it can cost you valuable chances and real money.

Now is the time to take proactive steps. At finblog.com, you will discover trusted strategies to build, repair, and protect your credit score. Gain insights into proven credit management methods and stay informed with expert-led educational content. Ready to reshape your financial path? Visit finblog.com and fill out our secure consultation form to get personalized advice tailored to your goals. Start your journey toward better credit and greater financial confidence today.

Frequently Asked Questions

What is a credit score?

A credit score is a numerical representation of your creditworthiness, typically ranging from 300 to 850. It indicates how likely you are to repay borrowed money and is used by lenders to assess your financial reliability.

How is a credit score calculated?

A credit score is calculated using several key components: payment history (35%), credit utilization (30%), length of credit history (15%), credit mix (10%), and new credit inquiries (10%). Each of these factors contributes to your overall credit risk assessment.

Why is a credit score important?

A credit score is important because it directly affects your ability to obtain loans, the interest rates you’ll receive, and access to other financial products. A high credit score can lead to lower rates and better terms from lenders, which can save you money in the long run.

How can I improve my credit score?

To improve your credit score, focus on making timely payments, keeping your credit utilization under 30%, maintaining a mix of credit types, and minimizing new credit inquiries. Regularly reviewing your credit report for errors and addressing them can also positively impact your score.