TL;DR:

- A debt repayment plan is a structured approach to paying down debts by organizing balances, prioritizing payments, and directing extra cash toward specific debts. Using tools like the snowball, avalanche, or hybrid methods, combined with automation and accurate data, can speed up the process and reduce interest costs. Outside options like debt consolidation and balance transfers may help but require careful consideration to avoid extending debt or incurring higher costs.

A debt repayment plan is a structured system for paying down what you owe by organizing balances, prioritizing payments, and directing extra cash toward specific debts in a deliberate order. Done right, it reduces total interest paid, improves your credit score, and gives you a clear finish line. This guide covers every step: gathering your debt data, choosing between the snowball, avalanche, or hybrid method, automating payments so you never miss a beat, and knowing when tools like debt consolidation or balance transfers make sense. Follow these steps and you will have a working debt reduction plan before the end of the day.

What information and tools do you need to start your debt repayment plan?

The first step in any debt management strategy is a complete debt inventory. Listing all debts with balances, APR, minimum payments, and due dates in one place is the foundation of realistic planning. Without this snapshot, you are guessing at timelines and interest costs.

Collect the following for every debt you carry: creditor name, current balance, interest rate (APR), minimum monthly payment, and due date. Pull this from your most recent statements or log into each account directly. Do not estimate. A $200 difference in a balance can shift your payoff date by months.

Once you have your debt list, calculate your monthly take-home income and subtract fixed essential expenses like rent, utilities, groceries, and insurance. What remains is your discretionary cash. Even $100 per month applied consistently to a single debt accelerates payoff dramatically.

Here is a simple example of how to organize your data:

| Creditor | Balance | APR | Min. Payment | Due Date |

|---|---|---|---|---|

| Chase Visa | $4,200 | 22.99% | $84 | 15th |

| Sallie Mae | $11,500 | 6.8% | $130 | 1st |

| Capital One | $1,800 | 26.99% | $45 | 22nd |

| Personal loan | $6,000 | 14.5% | $145 | 10th |

Tools like Tiller Money, YNAB (You Need a Budget), or a simple Google Sheets template work well for this. Free debt payoff calculators from sites like Bankrate let you model different payment scenarios before you commit.

Pro Tip: Assign each debt a stress score from 1 to 5 based on how much it bothers you emotionally. A high-balance student loan at low interest might score a 2, while a credit card you share with a family member might score a 5. This score helps you balance emotional relief with financial logic when choosing your payoff order.

Which debt repayment strategies work best: snowball, avalanche, or hybrid?

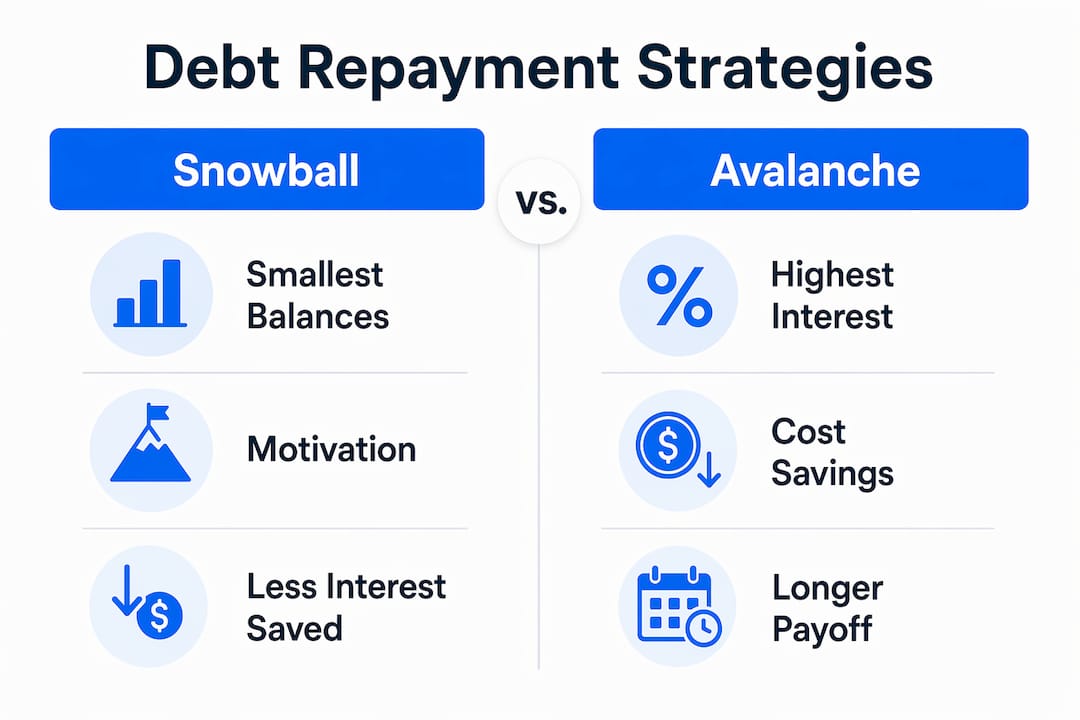

The three most proven debt repayment strategies are the debt snowball, the debt avalanche, and a hybrid of both. Each has a distinct logic, and the right choice depends on your psychology as much as your numbers.

The debt snowball method

The debt snowball method directs every extra dollar toward your smallest balance first, regardless of interest rate. Once that balance hits zero, you roll its payment into the next smallest debt. The debt snowball builds momentum through quick wins. Behavioral research consistently shows that eliminating accounts, even small ones, triggers a motivation boost that keeps people on track for months.

The debt avalanche method

The debt avalanche targets your highest-interest debt first. You pay minimums on everything else and throw all extra cash at the account with the worst APR. Mathematically, this saves the most money. Credit card debt at 26.99% costs you far more per dollar than a student loan at 6.8%, so attacking it first is the financially optimal move. Investopedia recommends prioritizing high-interest consumer debt before tax-deductible debts like mortgages or student loans.

The hybrid approach

The hybrid approach lets you mix both methods. You might knock out one or two small balances first for a psychological win, then shift to the highest-interest account. This is not a compromise. It is a deliberate strategy that acknowledges both math and motivation. Research shows the difference between snowball and avalanche in total interest paid is often measured in months, not years. That means emotional sustainability can matter more than picking the “perfect” method.

Here is a side-by-side comparison to help you choose:

| Method | Payoff order | Motivation style | Interest savings | Best for |

|---|---|---|---|---|

| Snowball | Smallest balance first | Quick wins, momentum | Lower | People who need early victories |

| Avalanche | Highest APR first | Long-term discipline | Higher | People motivated by total cost |

| Hybrid | Mixed, flexible | Balanced | Moderate | People who need both wins and savings |

The best debt repayment method is the one you will actually follow for 12, 24, or 36 months. Analysis paralysis over choosing the perfect strategy causes more failed plans than any math error. Pick one, start this week, and adjust later if needed.

How can automation and consistent payment routines improve your debt repayment plan?

Automation is the single most reliable way to follow through on a debt reduction plan. Behavioral economics research confirms that automated payments dramatically increase goal adherence. When money moves without you having to decide each month, you remove the friction that derails most plans.

Set up automation in this order:

- Automate all minimum payments on every debt immediately. Missing a minimum triggers late fees and can raise your APR, both of which work against your plan.

- Schedule your extra payment to transfer on payday, before you see the money in your checking account. Paying yourself out of debt first prevents the cash from disappearing into discretionary spending.

- Use named transfers when your bank allows it. Named automated transfers like “Friday Freedom Payment” reduce the temptation to redirect that money. Naming a transfer makes it feel committed, not optional.

- Set calendar reminders two days before each due date as a backup check. Automation fails occasionally due to bank errors or account changes. A reminder catches problems before they become late payments.

- Freeze cards you are paying down. Literally placing a credit card in a container of water in your freezer creates a physical pause before impulse spending. It sounds extreme. It works.

Pro Tip: Review your automation setup once per quarter. Life changes, income changes, and your plan should reflect that. A quarterly check-in also lets you redirect any raise or bonus directly to your target debt before lifestyle inflation absorbs it.

Burnout is the most common reason people abandon a working plan. Build in one small monthly reward, a dinner out or a streaming subscription, that you keep regardless of progress. Removing all discretionary spending creates a deprivation mindset that leads to binge spending and abandoned plans.

What financing options can support your debt repayment plan?

Debt consolidation and balance transfers are tools, not solutions. Used correctly, they lower your interest costs and simplify your repayment. Used carelessly, they extend your debt timeline and cost more in the long run.

Debt consolidation loans combine multiple debts into a single loan with one monthly payment. In 2026, consolidation loan rates range from 7% to 36% APR with repayment terms up to 7 years. If your current credit card rates average 24% and you qualify for a consolidation loan at 12%, the math is straightforward. The risk is extending your term so long that you pay more total interest despite the lower rate.

Balance transfer credit cards move high-interest balances to a card with a 0% promotional APR, typically for 12–21 months. To qualify for a competitive offer, you generally need a FICO score of 670 or higher. Most cards charge a transfer fee of 3%–5% of the balance. Always calculate transfer fees against the interest you would save during the promotional period before committing.

Consider these factors before using either option:

- Do not consolidate if you cannot qualify for a rate meaningfully lower than your current average APR.

- Do not use a balance transfer card if you cannot pay off the transferred balance before the promotional period ends. The revert rate is often 27% or higher.

- If your unsecured debt exceeds 50% of your gross income or your repayment timeline stretches beyond 5 years, debt relief programs through a nonprofit credit counselor may be worth exploring.

The goal of any financing option is to reduce the cost of your debt, not to create breathing room for new spending. Use these tools as part of your plan, not as a reason to delay starting one.

Key takeaways

A structured debt repayment plan built on accurate data, a sustainable payoff method, and automated payments is the most reliable path to becoming debt-free.

| Point | Details |

|---|---|

| Start with a full debt inventory | List every balance, APR, minimum payment, and due date before choosing a strategy. |

| Match your method to your mindset | Snowball builds momentum; avalanche saves more interest; hybrid balances both. |

| Automate payments on payday | Scheduling transfers before you see the money removes the decision and keeps you consistent. |

| Evaluate consolidation carefully | Only consolidate or transfer balances if the new rate is meaningfully lower than your current average. |

| Know when to seek outside help | If unsecured debt tops 50% of gross income or payoff exceeds 5 years, explore nonprofit debt relief. |

What I have learned from watching debt plans succeed and fail

Most debt plans fail in the middle, not at the start. People begin with energy, knock out a balance or two, and then hit a long stretch where progress feels invisible. That is where I have seen the most abandonment, and it is almost never a math problem.

The plans that survive that middle stretch share one trait: they are built around the person’s actual life, not an ideal version of it. I have seen people choose the avalanche method because it is “smarter,” then quit after six months because they had not closed a single account. I have seen others use the snowball on debts that were mathematically trivial and stay motivated for three years straight. The NFCC research on progress tracking backs this up. Visual progress and social accountability, whether that is a spreadsheet on your fridge or a friend who checks in monthly, are more predictive of success than the interest rate you are targeting.

My honest advice: start with whatever method gets you moving this week. Use smart financial goals to anchor your plan to a specific date and dollar amount. Then automate everything you can and review quarterly. If you hit a wall, switch methods. Switching from avalanche to snowball is not failure. It is adaptation. The only plan that does not work is the one sitting in a spreadsheet you stopped opening.

— Povilas

How Finblog can help you build and track your plan

Finblog offers free calculators, budgeting tools, and expert articles designed specifically for people working through debt repayment. Whether you are comparing payoff methods, modeling consolidation scenarios, or tracking monthly progress, Finblog’s resources give you the data you need to make confident decisions. The guides on managing debt effectively walk you through each stage of the process with clear, step-by-step explanations. Explore the full resource library at Finblog and start building a plan that fits your numbers and your life today.

FAQ

What is a debt repayment plan?

A debt repayment plan is an organized system for paying down debt by listing all balances, choosing a payoff order, and directing extra payments consistently until each account reaches zero.

What is the fastest way to pay off debt?

The debt avalanche method, which targets the highest-interest balance first, eliminates debt at the lowest total cost. Combining it with automated extra payments on payday accelerates results further.

How do I choose between the snowball and avalanche methods?

Choose the snowball if you need early wins to stay motivated. Choose the avalanche if you are disciplined enough to focus on long-term interest savings. The difference in total interest is often just months, so pick the method you will actually sustain.

When does debt consolidation make sense?

Debt consolidation makes sense when you can qualify for a loan rate meaningfully lower than your current average APR and you commit to not accumulating new balances during repayment.

How much of my income should go toward debt repayment?

Financial counselors generally recommend allocating at least 15%–20% of take-home income to debt repayment beyond minimum payments. If unsecured debt exceeds 50% of gross income, consider speaking with a nonprofit credit counselor about structured relief options.