TL;DR:

- A 401(k) is a tax-advantaged retirement plan that allows pre-tax contributions from your paycheck, often with employer matching. Contributions limits in 2026 range up to $24,500, with catch-up options for those over 50, and combining traditional and Roth contributions is flexible within annual limits. Strategic timing, understanding vesting, and avoiding early withdrawals are essential for maximizing long-term growth and retirement security.

Most people think a 401(k) is just a savings account their employer manages for them. It is not. What is a 401(k), really? It is a tax-advantaged retirement plan that lets you redirect a portion of your paycheck into investments before the IRS gets involved, with your employer often adding free money on top. Understanding how a 401k retirement plan works, including the tax mechanics, contribution rules, and employer matching details, can be the difference between retiring comfortably and working longer than you planned. This guide covers everything you need to make smarter decisions starting now.

Table of Contents

- What is a 401(k) and how does it work?

- 2026 contribution limits and catch-up rules

- Tax advantages: traditional vs. Roth 401(k) explained

- Employer matching and vesting nuances

- 401(k) vs other retirement accounts: when to use what

- Smart strategies for maximizing your 401(k) benefits

- What most people miss about 401(k)s: timing and strategy

- How Finblog can help you master your 401(k) and beyond

- Frequently asked questions

What is a 401(k) and how does it work?

A 401(k) is an employer-sponsored retirement savings account that lets you contribute pre-tax wages to individual investment accounts. Those contributions are excluded from your taxable income in the year you make them, which means you pay less in taxes today. You only pay income tax when you withdraw the money in retirement.

The name comes from Section 401(k) of the Internal Revenue Code, first enacted in 1978. It was never intended to replace pensions entirely, but that is exactly what happened across most of corporate America over the past four decades.

Here is how the basic mechanics work:

- Employee salary deferral: You elect to have a percentage of each paycheck deposited directly into your 401(k) account before taxes are calculated.

- Investment options: Your plan offers a menu of funds (typically mutual funds and target-date funds) that your contributions are invested in.

- Employer contributions: Many employers match a portion of your contributions, though this is not required by law.

- Tax-deferred growth: Your investments grow without being taxed each year. You pay taxes on gains only when you withdraw.

- Roth 401(k) option: Some plans offer a Roth version where you contribute after-tax dollars, and qualified withdrawals in retirement are tax-free.

The Roth distinction matters more than most people realize. A traditional 401(k) gives you a tax break now. A Roth 401(k) gives you a tax break later. Choosing between them depends on whether you expect to be in a higher or lower tax bracket in retirement, and that is a question worth taking seriously. You can explore retirement accounts overview to see how 401(k)s fit alongside other account types.

2026 contribution limits and catch-up rules

How much can you actually put away? More than most people contribute. The 2026 IRS elective deferral limit for most employees is $24,500. If you are 50 or older, you can add an $8,000 catch-up contribution for a total of $32,500. If you are between ages 60 and 63, the Secure 2.0 Act raised that catch-up even further, to $11,250, giving you a total of $35,750.

| Contributor age | Standard limit | Catch-up contribution | Total allowed |

|---|---|---|---|

| Under 50 | $24,500 | None | $24,500 |

| 50 to 59 | $24,500 | $8,000 | $32,500 |

| 60 to 63 | $24,500 | $11,250 | $35,750 |

| 64 and older | $24,500 | $8,000 | $32,500 |

These limits apply to your contributions alone. Employer matches do not count against your employee deferral limit, though there is a separate combined limit (employee plus employer) of $70,000 in 2026 for most plans.

One thing people routinely get wrong: you can split your contributions between a traditional 401(k) and a Roth 401(k) within the same plan, as long as the combined total does not exceed the annual limit. So if you want $12,000 pre-tax and $12,500 after-tax, that is allowed. This flexibility helps you maximize tax-advantaged savings across different tax situations.

Pro Tip: If you received a raise this year, increase your 401(k) deferral percentage before you get used to the extra take-home pay. You will not miss money you never spent.

Tax advantages: traditional vs. Roth 401(k) explained

The core of how a 401(k) works is tax timing. With a traditional 401(k), your contributions reduce your taxable income now. A $24,500 contribution from someone in the 24% tax bracket saves roughly $5,880 in federal income taxes that year. But every dollar you pull out in retirement gets taxed as ordinary income.

With a Roth 401(k), you pay taxes on contributions upfront. The payoff comes later. Qualified Roth 401(k) distributions in retirement are completely tax-free, including all the growth accumulated over decades. If your investments triple over 30 years, none of that gain is taxed at withdrawal.

| Feature | Traditional 401(k) | Roth 401(k) |

|---|---|---|

| Contribution tax treatment | Pre-tax (reduces taxable income now) | After-tax (no immediate deduction) |

| Investment growth | Tax-deferred | Tax-free |

| Withdrawals in retirement | Taxed as ordinary income | Tax-free if qualified |

| Best for | Expect lower tax rate in retirement | Expect higher tax rate in retirement |

| Required minimum distributions | Yes, starting at age 73 | Yes (though Roth IRAs do not have this) |

Common misconceptions worth clearing up:

- “Tax-deferred” does not mean tax-free. You still owe taxes eventually with a traditional account.

- Roth is not always better. If you are currently in a high tax bracket and expect to be in a lower one at retirement, traditional 401(k) contributions can save you more overall.

- Employer matches are always pre-tax. Even in a Roth 401(k), your employer’s matching contributions sit in a traditional (pre-tax) portion of your account.

Pro Tip: If you cannot confidently predict your future tax rate (and most people cannot), splitting contributions between traditional and Roth is a legitimate hedging strategy, not indecision.

When thinking through comparing traditional and Roth tax options, consider where your income will likely land in your peak earning years versus your retirement years.

Employer matching and vesting nuances

An employer match is exactly what it sounds like: your employer contributes money to your 401(k) based on how much you put in. A common formula is a 50% match on the first 6% of your salary you contribute. If you earn $80,000 and contribute 6% ($4,800), your employer adds $2,400. That is a guaranteed 50% return on those dollars before any market gains.

But there is a critical catch. Employer match contributions may be subject to a vesting schedule, meaning you do not fully own those matched dollars until you have worked at the company long enough. Your own contributions are always 100% yours immediately.

Here is how vesting schedules typically work:

- Immediate vesting: You own 100% of employer contributions right away. Rare but it exists.

- Cliff vesting: You own 0% until a specific date, then 100% all at once (for example, after three years).

- Graded vesting: You gain ownership gradually, such as 20% per year over five years.

To maximize your employer match, follow these steps:

- Find out exactly what your employer’s match formula is. Read the plan summary document or ask HR.

- Confirm the vesting schedule and note your vesting milestones.

- Contribute at least enough to capture the full match before directing money elsewhere.

- Do not leave a job with unvested match dollars on the table unless there is a compelling reason to.

Think of unvested employer match as deferred compensation. Leaving too early costs you real money. You can dig deeper into optimizing retirement savings strategies that account for vesting timing.

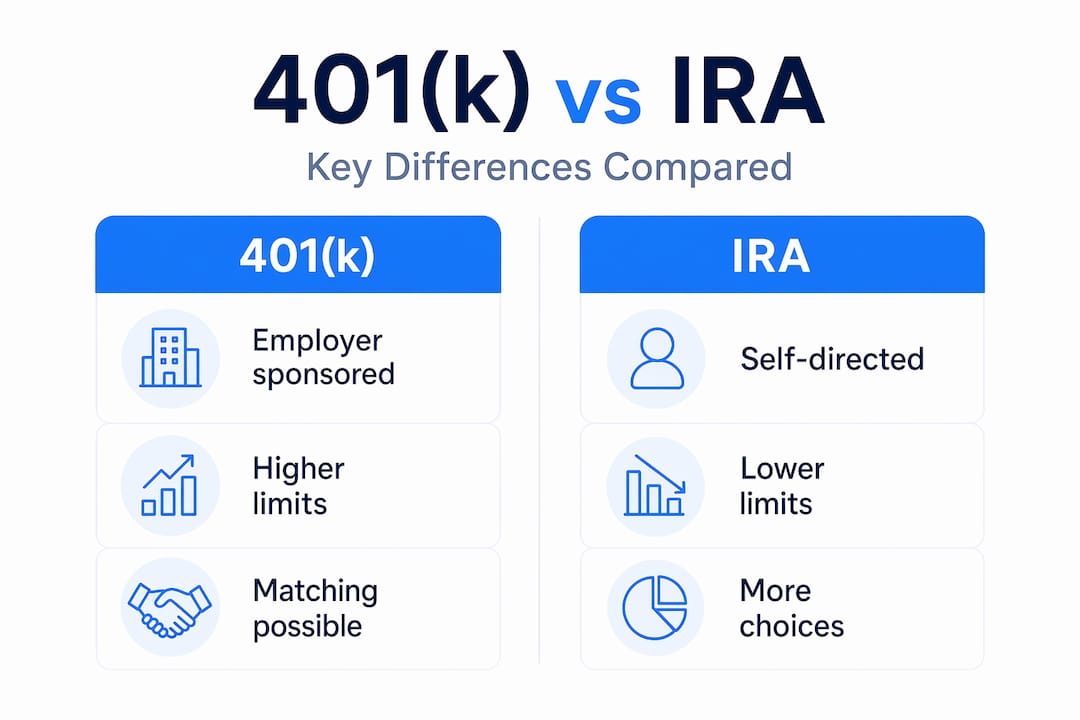

401(k) vs other retirement accounts: when to use what

Understanding the difference between 401(k) and IRA is essential if you are trying to build a complete retirement picture. These accounts are not competitors. They are designed to work together.

A 401(k) is a defined contribution plan, distinct from defined benefit pensions. In a pension, your employer promises a specific monthly income in retirement. In a 401(k), your retirement income depends on how much you saved and how your investments performed. Pensions are rare in the private sector today.

| Feature | 401(k) | Traditional IRA | Roth IRA |

|---|---|---|---|

| Who sets it up | Employer | Individual | Individual |

| 2026 contribution limit | $24,500 (employee) | $7,000 | $7,000 |

| Employer match available | Yes | No | No |

| Tax on contributions | Pre-tax or Roth | Pre-tax (if eligible) | After-tax |

| Investment choices | Plan menu only | Open brokerage options | Open brokerage options |

| Income limits | None | Deduction phases out | Contribution phases out |

Key reasons to use multiple account types:

- A 401(k) captures employer matching, which an IRA cannot replicate.

- An IRA gives you broader investment choices than most 401(k) plan menus.

- A Roth IRA has no required minimum distributions, unlike a 401(k) or traditional IRA.

- Combining accounts spreads your tax exposure across pre-tax and after-tax buckets.

Explore the 401k vs IRA comparison to see how these accounts work together for long-term planning.

Smart strategies for maximizing your 401(k) benefits

Knowing the mechanics is step one. Using them effectively is step two. Record 401(k) balances show that consistent investing pays off, but hardship withdrawals are rising and eroding those gains for many savers.

Follow these steps to get the most out of your 401(k):

- Automate your contributions. Set a percentage, not a dollar amount, so your savings scale automatically when your salary increases.

- Capture the full employer match first. Before funding any other account, get every dollar of free money your employer offers.

- Increase your deferral by 1% each year. Most people do not feel a 1% change in take-home pay. Over 10 years, this compounds significantly.

- Avoid hardship withdrawals at almost any cost. You lose the principal, the growth on that principal, and you may owe taxes plus a 10% penalty if under age 59½.

- Use catch-up contributions aggressively after 50. The enhanced contribution window between ages 60 and 63 is especially powerful for closing any savings gap.

- Review your investment allocation annually. Default fund selections are not always optimal. Check that your mix of stocks and bonds matches your time horizon.

Pro Tip: If you are behind on retirement savings, the enhanced catch-up limits for ages 60 to 63 are one of the most underused tools available. Running the numbers with a financial advisor at this stage can show you exactly how much ground you can recover.

What most people miss about 401(k)s: timing and strategy

Here is a perspective most retirement articles skip: the biggest 401(k) mistakes are not about choosing the wrong fund. They are about timing decisions made without full information.

Vesting schedules are a prime example. Workers often leave jobs just months before their employer match vests, walking away from thousands of dollars. The vesting timeline on employer contributions is not buried in fine print because it is unimportant. It is buried there because most employees never look. Knowing your vesting date should factor into every job change decision.

The Roth vs. traditional choice deserves the same scrutiny. Most financial content defaults to “Roth is great” without acknowledging that someone in the 32% or 35% federal bracket paying taxes today on Roth contributions could be paying significantly more than they would in retirement if their income drops. Tax strategy is not one-size-fits-all, and the assumptions you make today about future tax rates will shape the actual value of your retirement account.

Early hardship withdrawals are the silent killer of compounding. Pulling $20,000 at age 40 does not cost you $20,000. Assuming 7% average annual growth over 25 years, that withdrawal costs you closer to $108,000 in future value, before accounting for taxes and penalties. That context changes the conversation entirely.

Long-term discipline beats short-term optimization every time. The professionals who retire comfortably are rarely the ones who picked the best funds. They are the ones who contributed consistently, captured every employer match, and never touched the account early. Understanding retirement age planning insights helps you build a timeline that makes those consistent habits sustainable.

How Finblog can help you master your 401(k) and beyond

Your 401(k) is one piece of a larger retirement picture, and the decisions you make now carry consequences for decades. At Finblog, we publish regularly updated guides on 401(k) plans, traditional and Roth IRAs, tax-advantaged strategies, and retirement withdrawals, written specifically for adult professionals who want clarity, not jargon. Whether you are just starting to think about retirement or trying to catch up in your 50s and 60s, you will find practical, no-fluff resources to match your situation. With the right information at your fingertips, you can approach your retirement savings with confidence and make empowered decisions for your future.

Frequently asked questions

What is the difference between a traditional and Roth 401(k)?

A traditional 401(k) uses pre-tax contributions that reduce your taxable income today but are taxed as ordinary income upon withdrawal. A Roth 401(k) uses after-tax contributions, making qualified withdrawals in retirement completely tax-free.

How much can I contribute to my 401(k) in 2026?

Most employees can contribute up to $24,500 in 2026, with a $8,000 catch-up for those 50 and older, and up to $11,250 catch-up for those aged 60 to 63 under the Secure 2.0 Act rules.

What is a vesting schedule on employer matches?

A vesting schedule determines how long you must stay employed before employer match dollars fully belong to you. Your own contributions are always 100% yours from day one.

Can I contribute to both a 401(k) and an IRA?

Yes. You can contribute to both in the same year since 401(k)s and IRAs have separate contribution limits. Combining both accounts is one of the most effective ways to build diversified retirement savings.

What happens if I take a hardship withdrawal from my 401(k)?

You will owe income tax on the full amount plus a 10% early withdrawal penalty if you are under 59½, and you permanently lose the compounding growth that money would have generated over decades.