Deciding when to retire might be one of the most significant financial and lifestyle choices you’ll make, yet it’s rarely straightforward. Should you retire at 65, work into your 70s, or leave the workforce early? The answer depends on a complex mix of health, finances, personal goals, and evolving global norms. Recent research reveals surprising connections between retirement timing and longevity, while pension reforms worldwide are pushing normal retirement ages higher. This guide cuts through the confusion with expert insights and practical strategies to help you choose a retirement age that supports both your financial security and quality of life.

Table of Contents

- Key takeaways

- Understanding global trends in retirement age

- Health and longevity impacts of retirement age choices

- Financial implications of retiring earlier versus later

- Practical strategies for choosing your ideal retirement age

- Find expert retirement planning advice

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Global retirement age trend | Across developed nations the normal retirement age is rising toward the mid to late sixties as life expectancy and pension pressures push policy changes. |

| Health impacts vary by individual | The health effects of retirement depend on health status, job satisfaction, and whether work provides cognitive and social engagement. |

| Gender differences persist in timing | In Europe and elsewhere men often retire later than women due to historical pension structures and career patterns. |

| Flexible retirement adoption low | Flexible retirement paths exist but uptake remains limited, making early planning essential to adapt to policy changes. |

Understanding global trends in retirement age

Retirement age norms are shifting dramatically across developed nations. The OECD average normal retirement age for someone entering the workforce at 22 now stands at 63.9 as of 2024, with many countries planning increases to 67 or beyond. This upward trend reflects longer life expectancies, evolving pension systems, and concerns about financial sustainability as populations age.

Country-specific policies vary widely. Some nations have already implemented retirement ages of 67, while others are phasing in increases over the next decade. Within the European Union, notable gender differences persist, with men typically retiring later than women due to historical career patterns and pension structures. These variations matter because they shape social expectations and influence individual planning decisions.

| Country | Current Retirement Age | Planned Future Age |

|---|---|---|

| United States | 67 (born 1960+) | 67 |

| United Kingdom | 66 | 67 by 2028 |

| Germany | 65-67 (phasing) | 67 |

| France | 64 | 64 |

| Australia | 67 | 67 |

| Japan | 65 | Under review |

Several factors drive these increases. Longevity gains mean people live decades past traditional retirement ages, creating funding pressures on pension systems. Governments face difficult choices between raising retirement ages, cutting benefits, or increasing contributions. Labor market changes also play a role, as knowledge-based economies allow many professionals to work productively longer than previous generations could in physically demanding jobs.

When considering these global norms for your personal planning, keep several points in mind:

- Policy changes may affect your expected benefits, so stay informed about legislative updates

- International trends suggest working longer will become more common, potentially reducing stigma

- Your own health and career trajectory matter more than averages when making individual decisions

- Early planning gives you flexibility to adapt as circumstances and policies evolve

Understanding where your country fits in global trends helps set realistic expectations. If you’re planning to retire significantly earlier than your nation’s normal age, you’ll need robust personal savings to bridge the gap. Conversely, if you’re willing to work past normal retirement age, you may find why invest for retirement strategies particularly valuable for maximizing your financial position.

Health and longevity impacts of retirement age choices

The relationship between retirement timing and health outcomes is more nuanced than many assume. Contrary to the popular belief that early retirement extends life, retirement age positively impacts life expectancy, particularly in developing countries and where gender differences in retirement ages exist. Working longer appears to support longevity through continued social engagement, cognitive stimulation, and maintained routines.

Research shows particularly interesting patterns for women. Studies document cognition improvements for women and reduced physical inactivity following retirement, suggesting the transition away from work can have beneficial health effects when it occurs on favorable terms. These findings challenge assumptions that delaying retirement universally improves health outcomes.

The reality is that health impacts depend heavily on individual circumstances. Job satisfaction plays a crucial role. If you love your work and find it mentally stimulating, continuing past traditional retirement age may boost cognitive function and provide purpose. However, if your job causes chronic stress or physical strain, early retirement might relieve health-damaging pressures.

Socioeconomic status creates significant variation in outcomes. Professionals in comfortable office environments often benefit from working longer, while those in physically demanding or high-stress roles may see health improvements from earlier exits. The voluntariness of retirement also matters tremendously. Choosing to retire feels very different from being forced out, and involuntary retirement tends to produce worse health outcomes.

“The effects of retirement timing on health and longevity are highly individual. Later retirement may boost cognitive function and longevity for those in satisfying careers, but early retirement can relieve damaging stress for others. The key factors are voluntariness, job satisfaction, and socioeconomic context.”

When evaluating health considerations for your retirement timing decision, consider:

- Your current physical and mental health status and trajectory

- Whether your job energizes or drains you on a typical day

- The physical demands of your work and whether you can sustain them

- Your social connections outside work and whether retirement would isolate you

- Family history of age-related health conditions that might affect your working capacity

Being honest about these factors helps you avoid retirement mistakes to avoid that stem from unrealistic health assumptions. Some people thrive with the structure and purpose of continued work, while others flourish when freed from workplace obligations. Neither choice is inherently superior, the right answer depends on your unique situation.

Financial implications of retiring earlier versus later

Retirement age profoundly affects your financial security. The decision to retire even a few years earlier or later can shift your lifetime wealth by hundreds of thousands of dollars through changes in pension benefits, Social Security payments, and investment growth.

| Aspect | Early Retirement (62-64) | Later Retirement (67-70) |

|---|---|---|

| Pension benefits | Reduced by 20-30% in many systems | Full or enhanced benefits |

| Social Security | Permanent reduction of 25-30% | Delayed credits increase payments 24-32% |

| Savings duration | Must last 25-35+ years | Must last 15-25 years |

| Investment growth | Shorter accumulation period | Additional years of compound growth |

| Healthcare costs | Bridge coverage until Medicare | Employer coverage may continue |

| Income flexibility | Fixed retirement income only | Option to work part-time if needed |

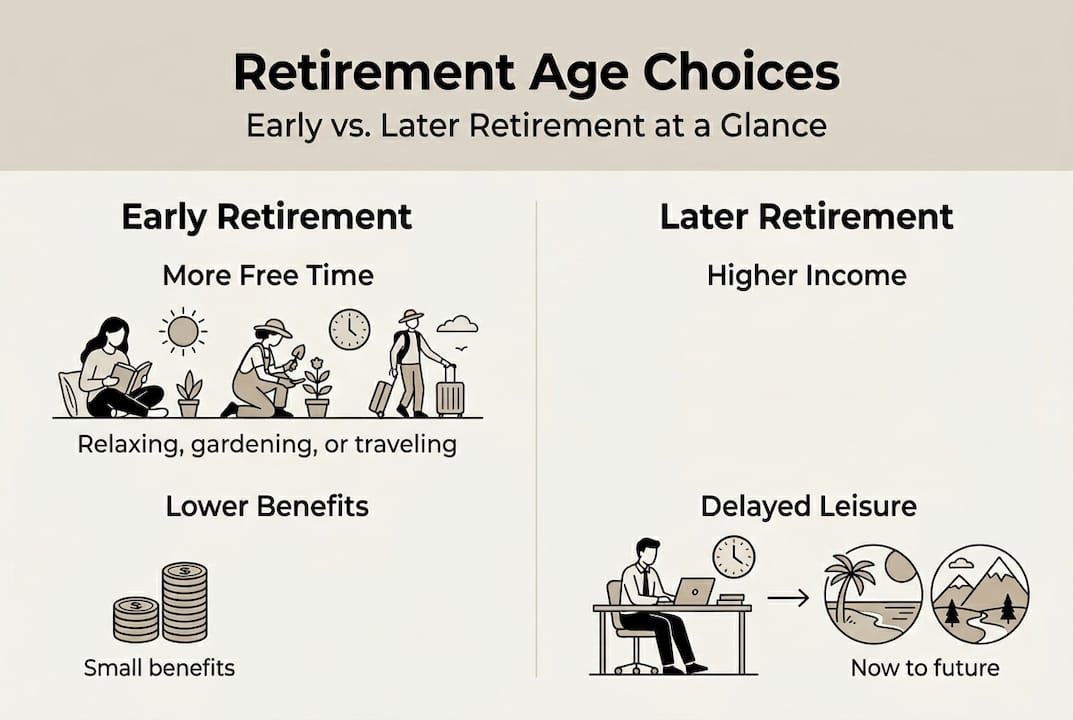

Retiring later delivers clear financial advantages. Your pension and Social Security benefits grow substantially with each year of delay, often by 6-8% annually. Your retirement savings have more time to compound, and you need them to last fewer years. You also avoid the expensive gap between early retirement and Medicare eligibility, when private health insurance can cost $1,000-$2,000 monthly.

However, early retirement offers benefits beyond the purely financial. Reduced stress, more time with family, and the ability to pursue passions while you’re healthy enough to enjoy them all have real value. The challenge is ensuring you can afford these benefits without compromising long-term security.

To evaluate your financial readiness for different retirement ages, follow these steps:

- Calculate your projected pension and Social Security benefits at ages 62, 65, 67, and 70 using official calculators

- Estimate your retirement expenses, including healthcare, housing, and discretionary spending

- Project your investment portfolio value at each potential retirement age using realistic return assumptions

- Model withdrawal rates to ensure your savings last through age 95 or beyond

- Identify gaps between income and expenses at each age and determine if they’re sustainable

- Consult with a financial advisor to stress-test your plans against market downturns and unexpected expenses

Flexible retirement pathways offer middle ground options. EU flexible retirement pathways show rising effective retirement ages with men retiring later than women, yet take-up rates for deferral and phased options remain surprisingly low. Phased retirement lets you reduce hours gradually, maintaining some income while transitioning to full retirement. This approach can optimize your financial position while testing whether you’re ready for complete workforce exit.

Pro Tip: Coordinate your retirement age decision with tax-efficient retirement withdrawal strategies to maximize after-tax income. Working a few extra years while converting traditional IRA funds to Roth accounts can dramatically reduce lifetime tax bills and required minimum distributions.

For those considering leaving the workforce ahead of traditional timelines, exploring early retirement strategies and understanding different retirement accounts comparison options can reveal paths to financial independence that don’t require working into your late 60s.

Practical strategies for choosing your ideal retirement age

Choosing your retirement age requires balancing multiple competing factors. No single formula works for everyone, but a systematic evaluation process helps you reach a decision aligned with your priorities and circumstances.

Start by assessing the key dimensions that should influence your choice. Your physical and mental health set boundaries on how long you can realistically work. Job satisfaction determines whether continuing work enhances or diminishes your quality of life. Financial resources establish whether early retirement is feasible or if working longer is necessary. Family needs, including caregiving responsibilities or desires to spend time with grandchildren, add another layer of consideration.

Your willingness to work longer differs from your ability to do so. You might be physically capable of working to 70 but unwilling to sacrifice additional years of freedom. Conversely, you might desperately want to retire early but lack the financial resources to make it viable. Honest assessment of both dimensions prevents unrealistic planning.

The voluntariness of your retirement timing significantly affects outcomes. Contrasting research shows that later retirement may boost longevity and health, but early retirement can relieve damaging stress, with effects varying by voluntariness, job satisfaction, and socioeconomic status. Forced early retirement due to health problems or job loss produces very different results than a planned, financially secure early exit.

To evaluate and decide on your ideal retirement age, take these practical steps:

- Schedule a comprehensive financial review with a qualified advisor to model different retirement age scenarios

- Assess your health trajectory honestly, consulting your physician about whether your work is sustainable long-term

- Evaluate your job satisfaction on a scale of 1-10 and consider whether changes could improve it if you’re undecided

- Survey your social connections and plan how you’ll maintain community and purpose in retirement

- Discuss timing preferences and financial realities with your spouse or partner to ensure alignment

- Test a trial retirement scenario by taking an extended vacation or sabbatical to experience non-working life

- Review your decision annually as health, finances, and preferences evolve rather than treating it as permanent

Pro Tip: Leverage phased retirement options if your employer offers them. Reducing to 60-80% time for a few years before full retirement lets you test the lifestyle, ease the psychological transition, and continue building savings while enjoying more personal time. This approach often produces better outcomes than abrupt cold-turkey retirement.

Regular reassessment is essential because circumstances change. A health diagnosis might make early retirement necessary. Strong market returns might make it financially feasible years sooner than expected. Conversely, a market downturn might require working longer than planned. Building flexibility into your thinking prevents you from feeling locked into a decision made years earlier under different conditions.

The most successful retirement transitions happen when people have clearly defined what they’re retiring to, not just what they’re retiring from. Before finalizing your timeline, develop a vision for how you’ll spend your time, maintain social connections, and find purpose. Explore retirement planning tips to ensure you’re considering all dimensions of a successful transition, not just the financial aspects.

Find expert retirement planning advice

Retirement age decisions carry lifelong consequences for your financial security and quality of life. While this guide provides foundational insights, your unique circumstances deserve personalized analysis from qualified professionals who can model scenarios specific to your situation.

Expert financial advisors help you navigate complex tradeoffs between retiring earlier for lifestyle benefits versus working longer for financial security. They stress-test your plans against market volatility, inflation, and unexpected expenses that could derail inadequately prepared retirements. Professional guidance is particularly valuable when coordinating multiple income sources, optimizing Social Security claiming strategies, and managing tax-efficient withdrawals.

Finblog offers comprehensive resources to support your retirement planning journey. Our tools and educational content help you understand the implications of different retirement ages, compare financial scenarios, and make informed decisions aligned with your goals.

Pro Tip: Use online retirement calculators to simulate multiple scenarios before meeting with an advisor. Running projections for retiring at 62, 65, 67, and 70 helps you understand the financial implications and arrive at consultations with informed questions.

FAQ

What is the average retirement age internationally?

The OECD average normal retirement age for someone who entered the workforce at 22 is approximately 64 as of 2024, with many developed countries raising their official retirement ages to 67 or beyond over the next decade. Significant variations exist by country due to different pension policies and demographic pressures. Gender differences also persist, particularly in European Union nations where men typically retire later than women due to historical career patterns and pension structures.

How does retiring early affect health outcomes?

Early retirement may relieve chronic workplace stress, but its effects on cognitive function and physical health are mixed and highly dependent on individual circumstances. Research shows that outcomes vary significantly based on whether retirement is voluntary, your level of job satisfaction, and your socioeconomic status. Women may experience cognitive improvements following retirement, while involuntary early retirement tends to produce worse health outcomes than planned transitions.

What financial factors should I consider when planning retirement age?

You should carefully evaluate pension benefits, Social Security payments, personal savings adequacy, investment growth potential, and tax-efficient retirement withdrawal strategies when planning your retirement age. Later retirement generally improves financial security through enhanced benefits and shorter drawdown periods, but requires good health and reasonable job satisfaction. Model your projected income and expenses at different retirement ages to identify potential gaps and ensure your savings will last through age 95 or beyond.

Are flexible retirement pathways widely used?

Despite their availability in many countries, flexible retirement options like phased retirement and benefit deferral have surprisingly low adoption rates, with typically fewer than 40% of eligible workers choosing these pathways. Low take-up may result from lack of awareness about available options, employer policies that don’t accommodate gradual transitions, or financial pressures that make partial retirement unaffordable. However, those who do use phased approaches often report smoother psychological transitions and better financial outcomes than abrupt retirement.