TL;DR:

- Managing investment taxes is an ongoing discipline that can significantly boost your portfolio over a lifetime.

- Understanding holding periods, account structuring, and tax-efficient strategies helps minimize taxes and maximize after-tax growth.

Most investors obsess over picking the right stocks or funds, then watch a meaningful chunk of those gains disappear at tax time. Managing investment taxes is not a once-a-year chore you hand off to your accountant in April. It is an ongoing discipline that, done right, can add tens of thousands of dollars to your portfolio over a career. This guide walks through the fundamentals of how investment income is taxed, how to structure your accounts for maximum efficiency, and how to execute specific strategies that keep more of your gains working for you.

Table of Contents

- Understanding investment taxes: the numbers that actually matter

- Preparing your portfolio for tax efficiency

- Executing tax-efficient strategies: harvesting losses and timing sales

- Verifying results and avoiding common tax pitfalls

- Why traditional tax advice on investments often misses the mark

- Start managing your investment taxes effectively today

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Long-term vs short-term gains | Holding assets over one year qualifies you for lower long-term capital gains tax rates, reducing your tax bill. |

| Strategic asset location | Placing assets into the right account types can significantly decrease annual taxes and improve after-tax returns. |

| Tax-loss harvesting benefits | Realizing losses at the right time offsets gains and lowers taxable income when done carefully to avoid wash-sale rules. |

| Mutual funds vs ETFs | ETFs typically provide better tax outcomes than mutual funds by minimizing annual capital gains distributions. |

| Measure after-tax returns | Focusing on after-tax performance rather than pre-tax results enhances wealth preservation over time. |

Understanding investment taxes: the numbers that actually matter

Before you can reduce a tax bill, you need to understand exactly what you are being taxed on and at what rate. The U.S. tax code treats different types of investment income very differently, and the gap between the best and worst outcomes is significant.

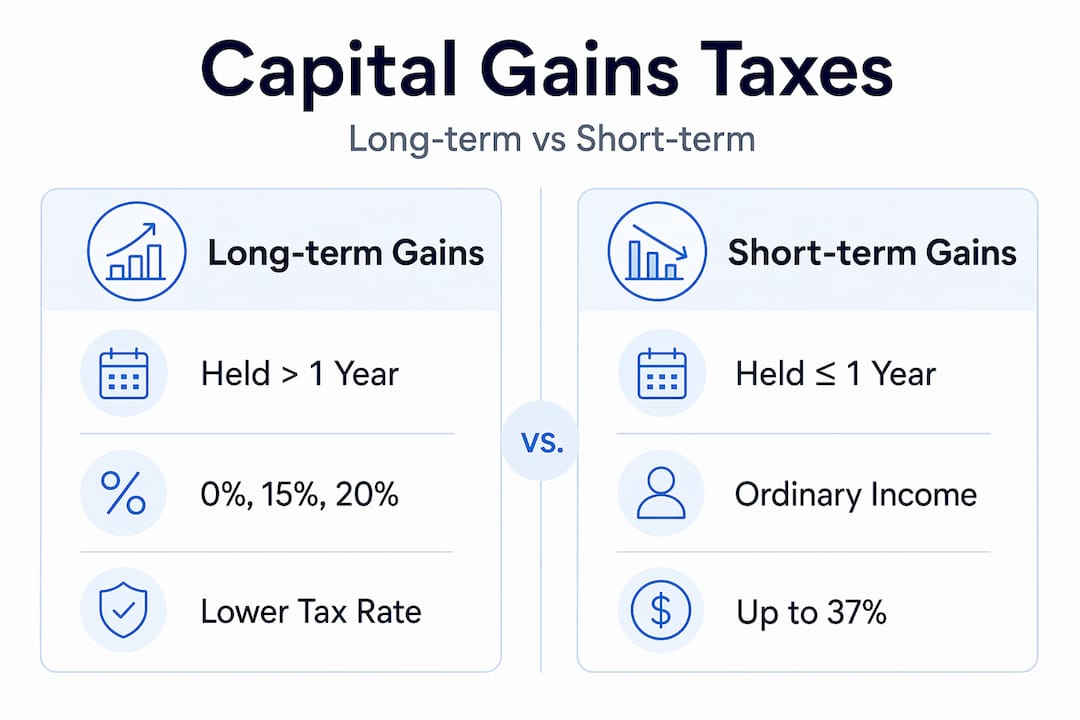

The single biggest lever in capital gains tax management is holding period. Long-term gains are taxed at 0%, 15%, or 20% on assets held more than 12 months, while short-term gains on assets sold in 12 months or less are taxed as ordinary income, up to 37%. That difference is not marginal. A $50,000 gain realized after 11 months could cost you $18,500 in federal taxes if you are in the 37% bracket. Wait one more month, and that same gain might cost you $10,000. The holding period alone is worth tracking obsessively.

Higher earners face one more layer. The Net Investment Income Tax adds 3.8% on investment income when your adjusted gross income exceeds $200,000 as a single filer or $250,000 married filing jointly. Combined with the top long-term capital gains rate, the effective federal rate on investment income can reach 23.8%, not counting state taxes.

Here is how the federal capital gains tax impact stacks up by income level:

| Filing status | Taxable income range | Long-term rate | NIIT | Effective max rate |

|---|---|---|---|---|

| Single | Up to $47,025 | 0% | No | 0% |

| Single | $47,026 to $518,900 | 15% | Possibly | 18.8% |

| Single | Over $518,900 | 20% | Yes | 23.8% |

| Married filing jointly | Up to $94,050 | 0% | No | 0% |

| Married filing jointly | $94,051 to $583,750 | 15% | Possibly | 18.8% |

| Married filing jointly | Over $583,750 | 20% | Yes | 23.8% |

Key tax implications of investments to keep in mind:

- Qualified dividends are taxed at long-term capital gains rates, not as ordinary income

- Non-qualified dividends from money market funds or foreign stocks get taxed as ordinary income

- Bond interest is almost always ordinary income, making it especially tax-inefficient in taxable accounts

- Short-term gains inside mutual funds can pass through to you as ordinary income even if you never sold a share

Understanding long-term vs short-term investing consequences at the tax level changes how you approach every sell decision.

With a baseline understanding of investment taxes, the next step is preparing your portfolio structure to maximize tax efficiency.

Preparing your portfolio for tax efficiency

Asset location is one of the most underused tools in investing and tax planning. The concept is simple: different types of investments generate different types of taxable income, so placing each one in the account type where it gets the most favorable treatment saves real money.

Proper asset location can boost after-tax returns by 0.14 to 0.41 percentage points annually. That may sound small, but on a $500,000 portfolio compounded over 20 years, 0.41 points translates to well over $50,000 in extra wealth.

Here is how to think about which assets go where:

| Asset type | Best account | Reason |

|---|---|---|

| Index funds, growth stocks | Taxable | Low turnover, qualified dividends, long-term gains |

| Corporate bonds, REITs | Tax-deferred (Traditional IRA, 401k) | High ordinary income sheltered from current taxes |

| High-growth small caps | Roth IRA | Tax-free growth on highest-potential assets |

| International stocks | Taxable | Foreign tax credit can only be claimed in taxable accounts |

| Actively managed funds (high turnover) | Tax-deferred | Frequent gains distributions avoided in taxable accounts |

The goal of tax-efficient investing through asset location is not just minimizing this year’s tax bill. It is reducing tax drag compounding year after year.

Roth accounts deserve special attention here. Because withdrawals in retirement are completely tax-free, Roth IRAs are the right home for assets with the highest expected growth. If you hold a small-cap growth fund that doubles in value, a Roth account captures that entire gain tax-free. The same fund in a traditional IRA just defers the tax; the Roth eliminates it.

For higher earners who cannot contribute directly to a Roth IRA, IRA deductibility phases out in 2026 for single filers with a workplace plan at $81,000 to $91,000 modified AGI, but the backdoor Roth conversion remains available. You contribute to a non-deductible traditional IRA and convert it to Roth, though the pro-rata rule can complicate this if you hold other traditional IRA balances.

Understanding tax-advantaged accounts in full detail is worth your time before you make any major repositioning decisions.

Pro Tip: Review your asset location at least once a year. As accounts grow at different rates, your location strategy drifts and needs rebalancing to stay effective.

Now that your portfolio is prepared for tax efficiency, let us explore execution tactics to minimize taxes on transactions and income.

Executing tax-efficient strategies: harvesting losses and timing sales

This is where investing and tax planning gets specific. Knowing the rules matters less than knowing exactly how to apply them when you are sitting in front of your brokerage account.

Choosing the right cost basis method is the first decision. Most brokerages default to FIFO (first in, first out), which sells your oldest shares first. That often means selling shares with the lowest cost basis and the highest gain. A better choice is specific identification, which lets you choose exactly which tax lots to sell. The most aggressive version of this is HIFO (highest in, first out): selling the shares with the highest cost basis first to minimize your reported gain. Using specific lot identification requires discipline and monitoring, but it can meaningfully reduce taxes on every sale.

Tax-loss harvesting is the practice of selling positions at a loss to offset realized gains elsewhere in your portfolio. Done consistently, it is one of the highest-value tax-efficient investing methods available to individual investors. Here is how to do it properly:

- Identify positions in your taxable accounts that are currently sitting at a loss

- Sell the losing position and immediately purchase a similar but not identical replacement (a different S&P 500 ETF, for example)

- Book the loss, which offsets gains dollar-for-dollar and can offset up to $3,000 in ordinary income per year

- Wait at least 31 days before buying back the original security if you want to repurchase it

- Track all lots across all accounts, including your spouse’s accounts and any IRAs

That last point is critical. The wash-sale rule disallows losses if you buy a substantially identical security within 30 days before or after the sale, and it applies across ALL accounts, not just the account where the sale occurred. Many investors get caught because they sell at a loss in a taxable account, then an automatic dividend reinvestment in their IRA buys back the same fund the following week.

Timing sales around your 12-month holding period is often overlooked but directly impacts your holding periods and taxes outcome. If you are 11 months into a position with a significant gain, waiting another month to clear the long-term threshold is almost always worth it.

Pro Tip: Set a standing loss threshold (for example, 10% below cost basis) that triggers an automatic review for harvesting. This removes emotion from the decision and keeps you from missing opportunities during volatile markets.

Verifying results and avoiding common tax pitfalls

Executing good strategies is only half the job. The other half is reviewing your outcomes, catching surprises early, and refining your approach.

“Annual tax planning that estimates full-year income and gains helps avoid panic selling and allows you to use low-bracket years effectively, which is one of the highest-leverage moves in investing and tax planning.”

Here is what an annual tax review for an investor should cover:

- Realized gains and losses year to date, broken down by short-term and long-term

- Projected ordinary income from wages, interest, and non-qualified dividends to gauge which bracket you will land in

- Upcoming mutual fund distribution dates so you do not buy into a fund the week before it pays out a large capital gains distribution

- Estimated NIIT exposure based on AGI trajectory

- Asset location drift caused by different accounts growing at different rates

That third point deserves a full stop. Mutual funds distribute capital gains annually even if you never sold a single share. If you buy into a fund in November and it distributes a large gain in December, you will owe taxes on that gain for the full year even though you held the fund for six weeks. ETFs and tax-managed funds are specifically designed to minimize these surprise distributions.

Panic selling at year-end is another trap. When markets drop and anxiety spikes, many investors sell without considering tax consequences, turning unrealized losses into poorly timed realized events, or worse, triggering gains by selling winners to lock in profits they fear losing. Reviewing tax planning strategies at a calm moment early in Q4 gives you a clear action plan before emotional pressure kicks in.

Why traditional tax advice on investments often misses the mark

Here is the uncomfortable truth most financial content avoids: the conventional focus on gross returns makes investors substantially poorer over time.

Ask most people about their portfolio performance and they will quote you a pre-tax number. Ask their advisor, and the answer is usually the same. But taxes drag compounded wealth by 1 to 2 percentage points annually, making after-tax returns the most important measure by a wide margin. A strategy that earns 9% gross but generates 2 points of annual tax drag is genuinely worse than a 7.5% gross strategy with 0.3 points of drag. That math holds up even before compounding. After 30 years, it is not even close.

Most investors also treat tax efficiency as a year-end conversation rather than an embedded part of every portfolio decision. Asset location gets set up once and then forgotten. Lot-level tracking gets ignored until a sale happens and the brokerage default produces a painful result. Wash-sale violations get discovered after the fact on a 1099 that removes a deduction you counted on.

The best practice for investment taxes is not a checklist. It is a mindset shift toward after-tax performance as the only number that actually matters. Every buy decision, every sell, every account contribution should be filtered through one question: what is the after-tax outcome?

The investors who compound wealth most efficiently are not necessarily the ones with the best stock picks. They are the ones who obsessively protect their gains from tax drag through tax-efficient investing habits applied consistently across decades.

Start managing your investment taxes effectively today

Understanding the tax implications of investments is the first step. Applying best practices for investment taxes across your actual portfolio is where the real gains happen. At Finblog, you will find detailed guides on every topic covered here, from comparing ETFs and mutual funds to structuring retirement contributions for maximum after-tax benefit. Our resources are built for investors who want to move from general awareness to specific, actionable strategies. Whether you are looking to refine your asset location, understand the mechanics of a backdoor Roth, or build a disciplined loss-harvesting routine, the next step is having the right information when you need it.

Frequently asked questions

What is the difference between short-term and long-term capital gains taxes?

Short-term capital gains on assets held 12 months or less are taxed as ordinary income at rates up to 37%, while long-term gains on assets held more than 12 months are taxed at 0%, 15%, or 20% based on your taxable income.

How does the Net Investment Income Tax affect my investment returns?

The Net Investment Income Tax adds an additional 3.8% on certain investment income when your modified adjusted gross income exceeds $200,000 for single filers or $250,000 for married couples, meaning your effective rate on gains can reach 23.8% at the federal level before state taxes.

What is tax-loss harvesting and how can I use it without triggering the wash-sale rule?

Tax-loss harvesting means selling a position at a loss to offset realized gains, and to keep the deduction valid, you must avoid buying the same or substantially identical security within 30 days before or after the sale across all of your accounts.

How important is asset location in managing investment taxes?

Very important. Placing tax-inefficient assets like bonds in tax-deferred accounts and tax-efficient assets like index funds in taxable accounts can boost after-tax returns by up to 0.41 percentage points annually, which compounds into significant savings over time.

Are mutual funds or ETFs better for tax efficiency?

ETFs are generally more tax-efficient because they have lower portfolio turnover and rarely distribute capital gains annually, while mutual funds distribute gains each year regardless of whether you sold shares, creating taxable events you did not choose.