Selling investments for a profit brings more than just a sense of accomplishment—it also means facing capital gains tax. This crucial tax affects every investor, whether your portfolio includes stocks, real estate, or collectibles. Understanding the difference between short-term and long-term gains, along with rules across countries like the United States, Canada, and the United Kingdom, can help you keep more of your returns. Get expert insight on how to turn tax knowledge into smarter investment decisions.

Table of Contents

- What Is Capital Gains Tax And How It Works

- Categories And Types Of Capital Gains Tax

- Key Rules, Rates, And Exemptions

- Global Differences And Legal Frameworks

- Compliance Steps And Common Mistakes

Key Takeaways

| Point | Details |

|---|---|

| Understanding Holding Periods | The tax rate on capital gains depends significantly on the holding period; short-term gains are taxed at ordinary income rates, while long-term gains have lower rates. |

| Impact of Asset Types | Different asset types, such as stocks, real estate, and collectibles, have varying tax implications, affecting overall tax obligations. |

| Importance of Exemptions | Awareness of exemptions, such as primary residence exclusions and specifics of inherited assets, can substantially reduce tax liabilities. |

| Tax Planning Strategy | Proactive tax planning, including loss harvesting and strategic timing of asset sales, can help minimize overall tax exposure. |

What Is Capital Gains Tax and How It Works

Capital gains tax is the tax you pay on profits from selling investments. When you buy a stock, real estate, or bond and sell it for more than you paid, that profit is subject to tax. The difference between your purchase price and your selling price is called your capital gain.

Let’s break down how this actually works in practice.

The Basic Calculation

Capital gains are straightforward to calculate. You take your sale price and subtract your original purchase price (also called your basis). Whatever remains is your gain.

Example: You buy 100 shares of a stock at $50 per share ($5,000 total). Five years later, you sell all 100 shares at $75 per share ($7,500 total). Your capital gain is $2,500.

That $2,500 is what gets taxed, not the full $7,500 sale amount. This is a critical distinction many investors miss.

Two Tax Categories Based on Holding Period

How long you hold an investment dramatically affects your tax rate. Capital gains taxation divides gains into two categories:

- Short-term capital gains: You held the asset less than one year. These are taxed as ordinary income at your regular tax rate.

- Long-term capital gains: You held the asset one year or longer. These get preferential tax rates that are significantly lower than ordinary income.

This distinction matters enormously. Short-term gains at your marginal tax rate could be 32%, 35%, or even 37%. Long-term gains typically max out at 20%.

Why This Matters for Your Portfolio

The holding period difference creates a genuine incentive to hold investments longer. A mid-career professional in a higher tax bracket could save thousands by waiting past the one-year mark before selling.

Imagine selling a $10,000 gain as short-term versus long-term. If your tax bracket is 32%, short-term costs you $3,200. Long-term? Just $2,000. That’s $1,200 in your pocket instead of the government’s.

Common Exemptions and Special Cases

Not all investment sales trigger capital gains tax. Several important exceptions exist:

- Primary residence exclusion: In the United States, you can exclude up to $250,000 of gains (or $500,000 if married filing jointly) on your primary home.

- Inherited assets: Assets you inherit often receive a “stepped-up basis,” meaning gains accumulated before your inheritance aren’t taxed.

- Charitable donations: Giving appreciated securities to charity can eliminate the capital gains tax entirely.

These exceptions can significantly reduce your tax liability if you understand them and plan accordingly.

Understanding your holding period and capital gains categories is foundational to tax-efficient investing. This single distinction can save you thousands annually.

The timing of when you realize gains can be as strategic as what you choose to invest in. Tax planning isn’t about avoiding investment opportunities—it’s about structuring them intelligently.

Pro tip: _Track your purchase dates carefully in a spreadsheet or investment platform. Knowing exactly when your one-year holding period expires lets you time sales strategically around tax planning.

Categories and Types of Capital Gains Tax

Capital gains don’t all work the same way. The type of asset you sell and how long you held it determines your tax treatment. Understanding these categories prevents costly mistakes when you’re planning to sell.

Short-Term vs. Long-Term Gains

The most fundamental distinction in capital gains taxation is holding period. Capital gains taxation classifies gains based on how long you owned the asset before selling.

If you hold an investment less than one year, your gain is short-term capital gains. You pay tax at your ordinary income rate, which can reach 37% at the highest federal bracket.

Hold the same investment over one year, and it becomes long-term capital gains. The tax rate drops significantly, maxing out at 20% federally for high earners.

This difference isn’t trivial. On a $50,000 gain, short-term could cost you $18,500 in taxes while long-term costs just $10,000. That’s $8,500 in savings by waiting.

Asset-Specific Tax Rules

Different asset types carry different tax implications. Not all gains are taxed equally even after you hit the one-year mark.

Stocks and mutual funds typically receive long-term capital gains treatment if held over one year. This is the most favorable scenario for most investors.

Real estate has unique rules. Residential property gets the primary residence exclusion. Investment properties face depreciation recapture taxes, meaning you may pay a 25% rate on certain gains even if held long-term.

Collectibles (art, coins, vintage cars) face a flat 28% long-term capital gains rate, regardless of your tax bracket. This penalizes high earners the least but crushes ordinary investors.

Bonds and fixed income generate ordinary income until maturity, then capital gains treatment on the difference between purchase and sale price.

This summary distinguishes how asset types affect capital gains tax treatment:

| Asset Type | Holding Period Impact | Special Tax Rule |

|---|---|---|

| Stocks/Mutual Funds | Preferential rate after 1 year | Most favorable for investors |

| Real Estate | Exclusions, depreciation recapture | Primary residence exclusion |

| Collectibles | Flat 28% regardless of bracket | Art, coins, vintage cars |

| Bonds | Ordinary income until maturity | Capital gains after maturity |

Global Variations for International Investors

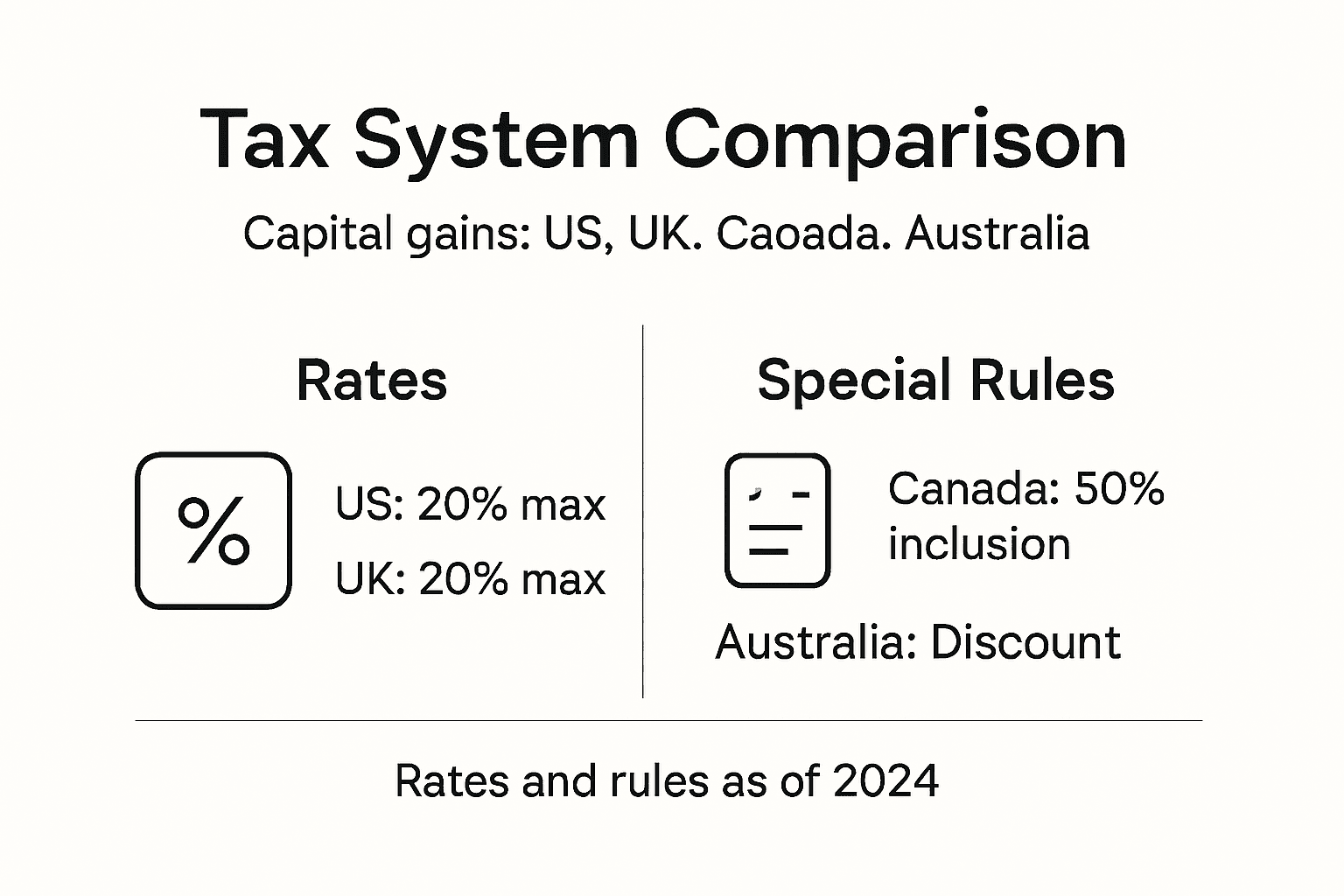

If you invest internationally or live abroad, capital gains taxation changes dramatically by country. Canada taxes only 50% of capital gains. The United Kingdom exempts the first £3,000 annually. Australia indexes gains for inflation before applying tax.

This matters enormously if you’re a global investor. A $100,000 gain taxed at 20% in the United States costs $20,000. The same gain in Canada costs roughly $10,000 due to the 50% inclusion rate.

Asset type and holding location determine your actual tax bill, not just your gain amount. Plan accordingly.

Many mid-career professionals work internationally or have holdings across borders without fully understanding tax implications. This oversight costs real money.

Pro tip: Identify your longest-held positions first when planning sales. Prioritize selling short-term holdings before long-term ones to minimize your overall tax bill in a single year.

Key Rules, Rates, and Exemptions

Capital gains tax isn’t one-size-fits-all. Rules, rates, and exemptions vary dramatically by location and asset type. Getting these details right saves thousands annually.

Understanding Tax Rates by Jurisdiction

Your tax rate depends entirely on where you’re taxed. The United States applies federal rates ranging from 0% to 20% on long-term gains, depending on income level. But that’s just federal—state and local taxes add another layer.

In the United Kingdom, capital gains tax rates vary by income bracket and asset type. Residential property faces steeper rates than stocks. Australia taxes gains at your marginal income tax rate with inflation indexing. Canada taxes only half of gains.

This matters profoundly. A $100,000 gain taxed at 20% in the United States costs $20,000. The same gain in Canada costs roughly $10,000 due to the 50% inclusion rate.

Here’s how capital gains tax rates and rules compare across several major countries:

| Country | Tax Rate (Long-Term) | Annual Exemption | Unique Features |

|---|---|---|---|

| United States | 0%-20% federal, plus state | $250,000/$500,000 (homes) | State taxes vary, stepped-up basis |

| Canada | Taxed on 50% of gains | None | 50% inclusion rate, no annual exemption |

| United Kingdom | 10%-20% (after £3,000) | £3,000 | Higher property rates, business relief |

| Australia | Marginal income tax rate | None | Inflation indexing, no annual exemption |

Annual Exemptions and Thresholds

Most countries allow you to exclude a certain amount of gains annually before taxation applies. The United Kingdom permits £3,000 of capital gains tax-free annually. The United States allows married couples to exclude up to $500,000 on primary residence sales.

These exemptions reset yearly, so timing matters. If you’re planning multiple sales across years, spacing them strategically around exemption thresholds reduces your total tax liability.

Key exemptions by type:

- Primary residence: $250,000 (single) or $500,000 (married) in the US

- Annual exclusion: £3,000 in the UK, AU$0 in Australia (no annual exemption)

- Qualified dividends: Often taxed at capital gains rates, not ordinary income

- Small business stock: Special treatment under Section 1202 in the US (up to $10 million exclusion)

Special Reliefs and Exclusions

Beyond basic exemptions, specific reliefs apply to certain situations. Business Asset Disposal Relief in the UK reduces rates on qualifying business sales. Private Residence Relief protects gains on your primary home from taxation entirely.

Retired professionals can benefit from special provisions. Retirement accounts offer tax-deferred growth, meaning you don’t pay capital gains on portfolio trades within the account itself.

Inherited assets often receive stepped-up basis, eliminating taxes on gains accumulated before inheritance. Charitable donations of appreciated securities avoid capital gains tax entirely while generating a deduction.

Annual exemptions reset yearly. Spacing sales strategically across multiple years can double your tax-free gains.

Many investors miss these opportunities because they don’t track exemption thresholds or plan sales with timing in mind.

Pro tip: Document your purchase dates and cost basis immediately for every investment. Create a simple spreadsheet tracking when you hit one-year holding periods and which gains would fall within annual exemptions.

Global Differences and Legal Frameworks

Capital gains tax systems vary wildly across countries. What’s taxed in one jurisdiction might be exempt in another. For global investors, this creates both complications and opportunities.

Comparing Major Tax Systems

The United States taxes long-term gains at 0%, 15%, or 20% depending on income. But you also face state taxes ranging from 0% to 13.3% in California.

Canada uses a 50% inclusion rate, meaning you only pay tax on half your gains. This effectively cuts your tax bill compared to the United States.

The United Kingdom applies rates from 10% to 20% after a £3,000 annual exemption. Australia taxes gains at your marginal rate with inflation indexing built in.

These differences compound over time. An investor moving from the US to Canada could cut their effective tax rate by 40% on the same portfolio gains.

Integration Into Income Tax Frameworks

Most developed countries integrate capital gains into their broader income tax systems differently. A global framework for capital gains taxes highlights how New Zealand, the Netherlands, and others debate whether gains should be taxed at ordinary rates or preferentially.

New Zealand eliminated capital gains tax entirely on most assets before reintroducing it selectively. The Netherlands taxes gains as income only under specific circumstances. Germany taxes gains at ordinary rates after a one-year holding period.

Each approach reflects different policy priorities around fairness, revenue generation, and economic growth.

OECD Perspectives and Policy Evolution

The OECD coordinates tax policy across developed nations. Capital gains taxation analysis from the organization shows most members apply lower rates than ordinary income rates, creating incentives for investment.

However, the OECD also identifies tensions in current systems:

- Lower rates on capital gains versus wages create inequity

- Revenue potential is lost through preferential treatment

- Economic distortions occur when gains are taxed differently by asset type

- Timing manipulation becomes possible when rules are complex

Many countries are reconsidering their approaches. The OECD suggests targeted reliefs and reformed timing rules could improve fairness without sacrificing economic growth.

Practical Implications for Cross-Border Investors

If you work internationally or hold assets across borders, you face multiple tax systems simultaneously. Tax treaties between countries prevent double taxation, but compliance becomes complex.

Your residency status determines which country taxes your gains. Non-residents often face different rates. This creates planning opportunities if you structure residency strategically.

Tax system differences across borders create both risks and opportunities. Understanding your specific situation prevents costly mistakes.

Many professionals don’t realize their country of residency or citizenship affects taxation significantly.

Pro tip: If you’re considering relocation, model capital gains taxes in your current and prospective countries before moving. A move could permanently reduce your tax rate on investment income.

Compliance Steps and Common Mistakes

Capital gains tax compliance isn’t optional. Miss deadlines or misreport gains, and penalties compound quickly. Understanding the process prevents costly errors and audit triggers.

Essential Documentation Requirements

Accurate records form the foundation of compliance. You need clear documentation of every investment transaction. This includes purchase dates, purchase prices, sale dates, sale prices, and any adjustments for splits or dividends.

Capital gains tax reporting requires accurate records of asset purchase and sale dates, values, costs, and reliefs. Without this documentation, you can’t calculate gains accurately or prove your basis to tax authorities.

Create a simple tracking system immediately:

- Purchase details: Date, price per share, total cost, broker name

- Sale details: Date, price per share, total proceeds, broker fees

- Cost basis adjustments: Stock splits, dividend reinvestments, gifts received

- Reliefs claimed: Primary residence exclusion, stepped-up basis, charitable donations

Digital records beat paper. Use a spreadsheet or investment software that generates reports automatically.

Reporting Deadlines and Procedures

Deadlines vary by country and asset type. In the United States, you report gains on Form 8949 and Schedule D by April 15. The United Kingdom requires residential property gains reported within 60 days of sale.

Missing deadlines triggers penalties automatically. Late filing penalties can reach 5-25% of unpaid tax. Interest compounds daily on overdue amounts.

Key deadlines to track:

- Identify all sales during the tax year

- Calculate gains using accurate cost basis

- Classify as short-term or long-term

- Report on appropriate tax forms by deadline

- Pay taxes owed on or before payment date

Set calendar reminders 30 days before deadlines. Don’t rely on memory.

Common Mistakes That Trigger Audits

Tax authorities scrutinize certain patterns. Understanding what triggers audits helps you avoid red flags.

The biggest mistake: forgetting about cost basis adjustments. Many investors don’t track stock splits or reinvested dividends, inflating their gains artificially. This instantly signals audit risk.

Second mistake: mixing up holding periods. Selling at day 365 instead of day 366 costs thousands in additional tax. Date accuracy matters.

Third mistake: inconsistent reporting across years. If you report different basis amounts for inherited assets or adjusted holdings, auditors notice immediately.

Common patterns that trigger scrutiny:

- Frequent trading with minimal documentation

- Large gains with no supporting records

- Basis different from broker statements

- Missing transactions on returns

- Loss harvesting without clear investment rationale

Incomplete records cause more audits than intentional underreporting. Document everything systematically.

Mid-career professionals often manage investments casually without formal tracking, then scramble at tax time. This disorganization creates audit risk.

Tax Planning Opportunities Before Year-End

Don’t wait until April to think about compliance. Strategic planning in November and December reduces your tax bill legally.

Loss harvesting offsets gains before year-end. Selling losing positions eliminates gains dollar-for-dollar. Repurchase after 30 days to maintain exposure.

Timing large sales across years reduces tax impact. If you’re close to a higher tax bracket threshold, delaying gains to the next year could save significantly.

Proactive planning beats reactive scrambling. December moves compound year over year.

Pro tip: Set up a quarterly review in January, April, July, and October to track realized gains, identify loss harvesting opportunities, and adjust year-end planning. This prevents last-minute audit risk and ensures accurate compliance.

Take Control of Your Capital Gains Tax Strategy Today

Navigating the complexities of capital gains tax can feel overwhelming, especially for global investors facing varying rates, exemptions, and holding period rules. This article highlights crucial concepts like long-term versus short-term gains, stepped-up basis, and international tax differences that directly impact your portfolio’s performance and tax liability. Without informed planning, you risk paying more taxes than necessary, losing thousands in avoidable costs.

At finblog.com, we understand these challenges and specialize in helping professionals and serious investors uncover smart tax strategies. From tracking your holding periods to leveraging exemptions and managing international investments, our expert guidance empowers you to make confident decisions that maximize your after-tax returns. Don’t let missed deadlines or overlooked exemptions eat into your wealth. Visit finblog.com now to learn more and secure personalized advice tailored to your unique situation. Take action today to protect your gains and build lasting financial security.

Frequently Asked Questions

What is capital gains tax?

Capital gains tax is the tax you pay on profits made from selling investments, such as stocks or real estate, when the selling price exceeds the purchase price.

How does the holding period affect capital gains tax rates?

The holding period significantly impacts tax rates. Short-term capital gains, from assets held for less than one year, are taxed as ordinary income at your regular tax rate. Long-term capital gains, from assets held for at least one year, typically benefit from lower tax rates.

Are there any exemptions to capital gains tax?

Yes, there are several exemptions, including the primary residence exclusion, which allows you to exclude up to $250,000 (or $500,000 for married couples) on gains from the sale of your primary home, and stepped-up basis for inherited assets, which may reduce tax liability.

How do different asset types affect capital gains tax treatment?

Different asset types have varying tax implications. For example, stocks generally receive long-term capital gains treatment when held over one year, while collectibles are taxed at a flat rate of 28%. Understanding these distinctions helps investors plan better.

Recommended

- Capital Gains Tax – Impact on High-Net-Worth Investors – Finblog

- Understanding the Tax Implications of Investing – Finblog

- Understanding Tax Efficient Investing: How It Works – Finblog

- Missed the 2025 Global Rally? Why International Stocks Still Offer Opportunity in 2026

- International Bank Transfer: Impact on Expats’ Money

- Buying Investment Property Guide for Auckland Investors