TL;DR:

- Your financial plan must reflect your current circumstances to remain effective and prevent wealth erosion.

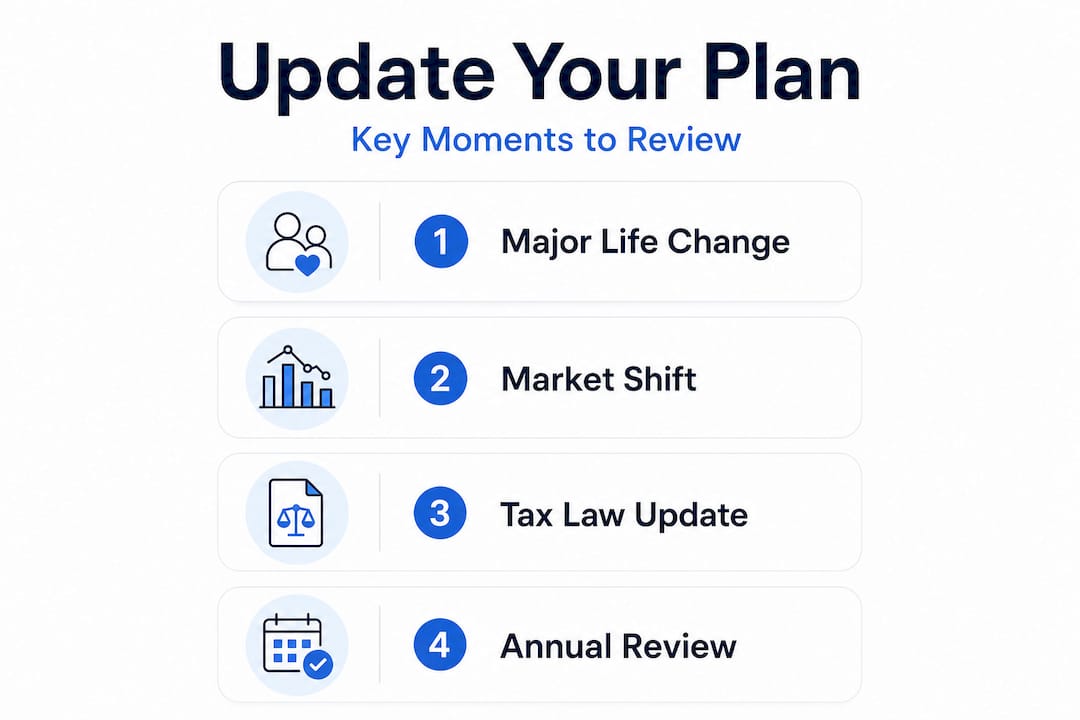

- Regular reviews triggered by life events, market shifts, or tax law changes are essential to maintain alignment and optimize outcomes.

Your financial plan is only as powerful as its ability to reflect your current reality. Many professionals and serious investors set up a solid financial plan, then let it sit untouched for years while their lives, markets, and tax laws shift around them. The cost of inaction is real: misaligned investments, missed tax efficiencies, and protection gaps that can quietly erode wealth. This guide gives you the specific triggers, practical frameworks, and review schedules you need to keep your plan working as hard as you do.

Table of Contents

- Key signs it’s time to revisit your financial plan

- How to assess your financial plan for needed updates

- Common triggers: Tax and market changes

- How often should you review your financial plan?

- What most professionals overlook about plan updates

- Take charge of your next financial review

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Triggers to update | Life changes, market shifts, and tax updates all signal it’s time to review your plan. |

| Assessment is critical | A step-by-step review ensures your goals, risks, and coverage remain aligned with your needs. |

| Schedule reviews | Set recurring annual or quarterly reviews to keep your plan agile and current. |

| Adapt proactively | Combine regular scheduling with readiness to act on new opportunities or risks. |

Key signs it’s time to revisit your financial plan

Now that you recognize the impact of outdated plans, the next step is understanding which events or signals should prompt a timely review. Most professionals know they should update their financial plan, but they rarely know exactly when.

Life events that demand immediate action

Certain life events are non-negotiable triggers. When they happen, waiting for your next scheduled review is a mistake.

- Marriage or divorce: Your household income, tax filing status, shared liabilities, and beneficiary designations all change overnight. A financial plan built for a single individual fails a married couple, and vice versa.

- Birth or adoption of a child: This introduces new costs, insurance needs, education savings goals, and updated estate planning requirements. A 529 plan or trust may become necessary.

- Death of a spouse or dependent: Survivor benefits, life insurance claims, inheritance, and revised income projections all require immediate plan adjustments.

- Career change or job loss: Income levels shift, employer-sponsored benefits like 401(k) matching or group health insurance may disappear, and spending projections need recalibration.

- Relocation to a different state: State income taxes, property taxes, cost of living, and even estate laws vary dramatically between states.

- Major purchase or debt: Buying a home, taking on a business loan, or liquidating a significant asset affects your balance sheet, liquidity, and investment capacity immediately.

- Inheritance or financial windfall: Sudden wealth introduces tax exposure and investment decisions that a pre-windfall plan never accounted for.

Scheduled reviews: not just when life forces you

Beyond event-driven updates, periodic reviews are essential. According to quarterly planning frequency, financial experts recommend revisiting your plan at least quarterly to catch smaller shifts before they become costly problems. Annual reviews are the baseline, but quarterly check-ins catch more issues early.

| Update Type | Trigger | Recommended Timeframe |

|---|---|---|

| Event-based | Major life or financial change | Within 30 days of event |

| Quarterly review | Portfolio drift, minor goal shifts | Every 90 days |

| Annual review | Full plan audit | Once per year, same month |

| Tax-season review | IRS changes, deductions, contributions | January through April |

Most serious investors underestimate how much a quarterly cadence improves outcomes compared to relying solely on annual financial review steps. Quarterly reviews take less time individually, but collectively keep your plan far more accurate.

How to assess your financial plan for needed updates

Once you identify it’s time to review your plan, the next stage is a thorough assessment to determine what needs to change. This is where most professionals either rush through the process or focus on just one area, like investments, while ignoring others like insurance or estate planning.

Step-by-step assessment framework

-

Revisit your financial goals and timelines. Are your retirement target date, savings milestones, and income goals still realistic? Life changes often compress or extend timelines significantly. For example, starting a business may delay retirement by three years while also changing your tax situation entirely. Reviewing your retirement plan objectives is essential during any full plan audit.

-

Evaluate your investment portfolio’s performance and risk alignment. Check whether your asset allocation still matches your stated risk tolerance. A portfolio that started at 70% equities and 30% bonds might have drifted to 85/15 after a strong market run, exposing you to more risk than you intended.

-

Review all insurance policies and coverage levels. Your needs for life, disability, long-term care, and liability insurance change over time. A policy bought when you were 35 and single may be completely inadequate at 45 with a family and a mortgage. Following sound insurance review strategies helps ensure your coverage never lags behind your actual risk.

-

Update all beneficiary designations. This is one of the most overlooked steps. Beneficiary designations on retirement accounts, life insurance policies, and transfer-on-death accounts override your will entirely. An ex-spouse listed as a beneficiary will receive those assets regardless of your wishes if you haven’t updated the designation.

-

Check alignment with current tax laws and estate plans. Contribution limits, deduction rules, and estate tax thresholds change regularly. Your plan should reflect the rules in effect now, not the ones from three years ago.

-

Document what changed and why. A retirement planning checklist helps ensure nothing falls through the cracks during the review process.

Key assessment metrics at a glance

| Area | What to assess | Red flag |

|---|---|---|

| Goals | Timeline, target amounts | More than 10% off track |

| Portfolio | Asset allocation, returns vs. benchmark | Drift beyond tolerance bands |

| Insurance | Coverage amounts, policy terms | Major life change not reflected |

| Beneficiaries | Named individuals on all accounts | Outdated or missing designations |

| Tax efficiency | Contribution limits, deductions used | Leaving tax-advantaged room unused |

| Estate plan | Will, trusts, powers of attorney | Not updated in 3+ years |

Pro Tip: Schedule your insurance and beneficiary review as a separate task from your investment review. Combining them often means one or the other gets shortchanged. Blocking 30 minutes exclusively for beneficiary checks each year can prevent significant legal and financial complications later.

Common triggers: Tax and market changes

In addition to personal circumstances, external developments can also signal it’s time to update your financial plan. These external forces are often underestimated because they don’t feel as immediate as a job change or a new baby, but they can quietly undermine a perfectly structured plan.

Tax law changes that require immediate attention

The IRS adjusts dozens of rules each year. Some changes are minor. Others can significantly affect your take-home income, retirement contributions, and estate planning strategies. Key areas to watch include:

- Contribution limits: The IRS adjusts 401(k), IRA, and HSA contribution limits almost annually for inflation. Missing the updated limits means leaving tax-deferred savings capacity on the table.

- Tax bracket thresholds: If your income stays flat but brackets adjust upward, you may fall into a lower effective rate and can plan accordingly.

- Capital gains rates: Changes in long-term capital gains tax rates can affect when you choose to sell appreciated assets.

- Estate and gift tax exemptions: These are subject to legislative change. The Tax Cuts and Jobs Act set high exemption levels, but those provisions are scheduled to sunset, which could dramatically reduce what you can transfer tax-free.

- Roth conversion rules: Changes to income limits, conversions, and backdoor strategies require you to update your retirement income distribution plan regularly.

Understanding how tax law changes affect your specific situation is not optional for serious investors. A single overlooked change can cost thousands in unnecessary taxes over time.

Pro Tip: Set up automated alerts through your financial advisor or a tax-focused news service. Rather than waiting to hear about major IRS updates, have the information delivered to you so your plan stays current without extra research effort.

Market cycles and economic volatility

A sustained bull market can push your portfolio well beyond your target asset allocation. A sharp correction can do the opposite. Neither outcome is inherently bad, but both demand a response if they move you outside your planned risk parameters.

One important statistic worth noting: surveys consistently show that fewer than half of investors make formal updates to their financial plan after significant market disruptions, even when their portfolio value changes by 20% or more. That inaction is precisely what separates reactive investors from proactive ones.

Market changes also affect your underlying assumptions. If your plan assumed a 7% average annual return but market conditions shift the realistic expectation to 5%, your projected retirement date and savings targets need to be recalculated. Sticking to old assumptions in a changed environment is not discipline. It is denial.

How often should you review your financial plan?

Now that you know the triggers, it’s important to establish a routine schedule that keeps your plan in top shape. The most effective professionals don’t treat financial reviews as a reactive emergency. They build review habits into their calendar before a crisis forces them to act.

Recommended review schedule

- Quarterly (every 90 days): Check portfolio drift, confirm you’re on track with savings contributions, and scan for any tax or market changes that occurred in the past quarter.

- Annually (full audit): Conduct a thorough annual review process covering goals, insurance, beneficiaries, estate plans, tax positioning, and investment strategy simultaneously.

- After any major life event: Don’t wait for your scheduled review. Address changes within 30 days of a significant event.

- When tax law changes take effect: Budget time in Q1 of each year specifically to respond to any IRS updates from the prior legislative session.

Pro Tip: Treat your annual financial review like a performance review at work. Block an entire day, prepare documentation in advance, and use a structured checklist so nothing gets skipped. Professionals who treat their review casually tend to miss the details that matter most.

“A financial plan that isn’t regularly updated isn’t really a plan at all. It’s a historical document. The best investors I’ve worked with treat their plan as a living system, not a static report they filed away after their initial meeting.” This reflects the standard of practice among top wealth managers who consistently outperform their peers not through stock-picking, but through disciplined, consistent plan maintenance.

What most professionals overlook about plan updates

Having set the practical steps, let’s dig into what separates the truly effective planners from the rest.

The conventional wisdom says: set up your financial plan, review it once a year, and you’ll be fine. That advice sounds reasonable, but it misses something critical. The most damaging financial mistakes rarely announce themselves with a major life event. They sneak in through small, unchecked drifts.

A portfolio that drifts 5% beyond your risk tolerance over 18 months doesn’t feel dangerous. Until a market correction hits and the loss is 30% instead of the 20% you modeled. A life insurance policy that hasn’t been updated after a salary increase leaves your family underinsured. Not dramatically, just enough to cause real hardship if something happens.

True financial agility means combining your scheduled reviews with a constant low-level awareness of what’s happening in your life and the markets. Think of it as the difference between a scheduled car inspection and paying attention to how your car drives every day. You need both.

The professionals who consistently build and preserve wealth are not just disciplined about their annual review. They stay curious and responsive year-round. They notice when something changes and ask whether their plan still fits. They use proactive quarterly updates to course-correct early, before small misalignments become expensive problems.

A calendar reminder is not a strategy. Awareness combined with a structured system is a strategy. That combination is what most people miss, and it’s what the highest-performing investors consistently get right.

Take charge of your next financial review

Ready to apply what you’ve learned? Your financial plan is one of the most powerful tools you have for building long-term wealth and security, but only if it reflects where you actually are today. At finblog.com, we provide in-depth planning guides, structured review frameworks, and expert-backed resources designed specifically for professionals and serious investors who want more than generic advice. Whether you’re starting your first full plan audit or refining a strategy you’ve maintained for years, explore our financial planning resources to find practical tools that help you stay ahead of every trigger, change, and opportunity your financial life will bring.

Frequently asked questions

What are the biggest risks of not updating my financial plan?

Failing to update your financial plan can expose you to unnecessary investment risk, missed tax-saving opportunities, and outdated insurance coverage that leaves critical gaps in your protection strategy.

How do market changes impact my financial plan?

Market changes can rapidly shift your portfolio’s asset allocation and risk exposure, and as quarterly planning guidance confirms, regular rebalancing is essential to stay aligned with your goals after significant market moves.

Should I update my plan if there are changes in tax law?

Yes, because tax law changes can affect contribution limits, deduction eligibility, and retirement distribution rules in ways that make your current strategy less efficient or even noncompliant.

How often should I schedule a thorough review of my financial plan?

Most professionals should conduct a detailed review at least once a year, as outlined in the annual review framework, and additionally after any major life or financial event.

Is it better to review my plan quarterly or annually?

Quarterly reviews offer greater agility and catch smaller issues before they compound, but as quarterly planning guidance recommends, an annual review remains the minimum standard for most investors with moderate to complex financial situations.