Retirement planning sounds overwhelming, especially when figuring out where to even start. Most people are surprised to learn that only 40 percent of Americans have calculated how much they need to save for retirement. That number might seem low, but imagine having a step-by-step plan that can actually put you ahead of the curve instead of leaving you guessing.

Table of Contents

- Step 1: Assess Your Current Financial Situation

- Step 2: Set Clear Retirement Goals

- Step 3: Calculate Your Retirement Needs

- Step 4: Choose The Right Investment Options

- Step 5: Create A Comprehensive Retirement Plan

- Step 6: Review And Adjust Your Plan Regularly

Quick Summary

| Key Point | Explanation |

|---|---|

| 1. Assess Your Financial Situation | Evaluate your finances to understand your current status and net worth before planning for retirement. |

| 2. Set Clear Retirement Goals | Define specific, actionable retirement goals based on your desired lifestyle and financial needs. |

| 3. Calculate Retirement Needs | Determine the funds required for retirement by analyzing expected expenses and desired income replacement. |

| 4. Choose Diversified Investments | Select a mix of investment options that align with your risk tolerance and long-term financial goals. |

| 5. Regularly Review and Adjust Plan | Schedule consistent reviews of your retirement plan to adapt to changing circumstances and ensure financial resilience. |

Step 1: Assess Your Current Financial Situation

Retirement planning begins with a comprehensive evaluation of your current financial landscape. Understanding your financial health is the critical foundation for building a robust retirement strategy. This initial step provides a clear snapshot of where you stand financially and helps you chart a precise course toward your retirement goals.

Start by conducting a thorough financial inventory. Gather all your financial documents including bank statements, investment accounts, retirement accounts, mortgage details, outstanding loans, and credit card statements. Create a detailed spreadsheet or use a digital financial tracking tool to consolidate this information. The goal is to calculate your net worth by subtracting your total liabilities from your total assets.

According to the U.S. Department of Labor, calculating your net worth provides an essential baseline for retirement planning. This process involves carefully documenting every financial resource and obligation. Pay special attention to these key financial components:

- Current savings and investment balances

- Retirement account contributions and current values

- Annual income from all sources

- Monthly and annual expenses

- Outstanding debt amounts and interest rates

- Potential future income streams

Be brutally honest during this assessment. Many individuals underestimate their expenses or overestimate their savings. Review your spending patterns from the past 12 months to get an accurate picture of your financial habits. Look for areas where you can potentially reduce expenses and redirect funds toward retirement savings.

Consider working with a financial advisor who can provide an objective analysis of your financial situation. They can help identify potential gaps in your current financial plan and recommend strategies to optimize your retirement readiness. Some advisors offer complimentary initial consultations that can provide valuable insights without significant upfront investment.

Successful completion of this step means you have a clear, comprehensive understanding of your current financial position. Your detailed financial inventory will serve as the roadmap for subsequent retirement planning stages, helping you make informed decisions about savings, investments, and long term financial strategies.

Step 2: Set Clear Retirement Goals

Defining precise retirement goals transforms abstract dreams into actionable financial plans. After assessing your current financial situation, the next critical step is creating a vivid, realistic vision of your retirement lifestyle and the financial resources required to support it. This process goes beyond simple number crunching and involves deep personal reflection about your future aspirations.

Begin by envisioning your ideal retirement scenario. Consider the lifestyle you want to maintain, including potential travel, hobbies, living arrangements, and personal interests. Concrete visualization matters – imagine where you want to live, what activities you want to pursue, and how you want to spend your time. Some individuals dream of international travel, while others prioritize spending time with family or pursuing passion projects.

According to the U.S. Department of Labor, estimating retirement income needs requires careful calculation. Most financial experts recommend planning for 70-80% of your current annual income as a baseline retirement budget. However, this percentage can fluctuate based on individual lifestyle expectations and anticipated expenses.

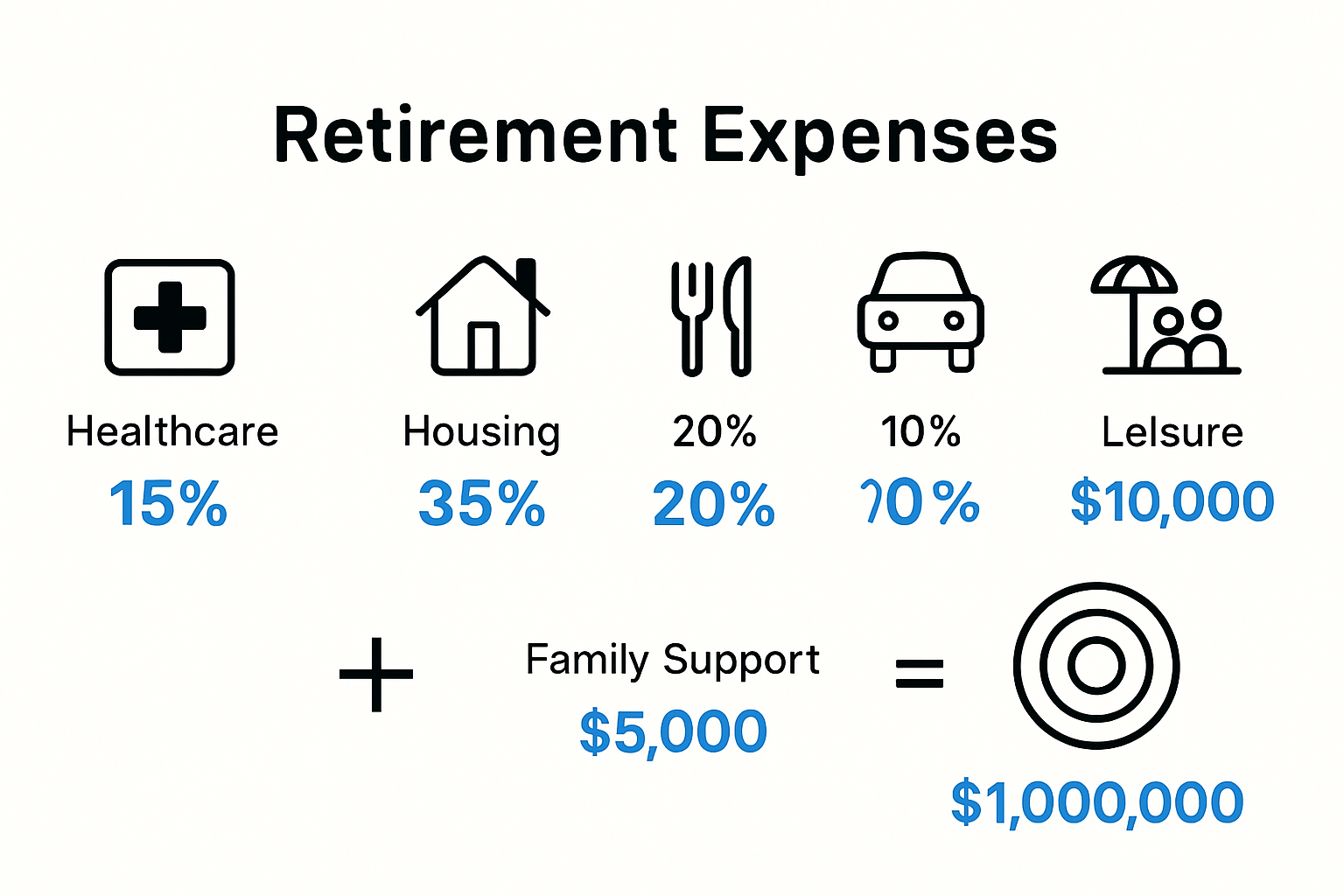

Create a detailed retirement expense projection that accounts for:

- Healthcare costs

- Housing and potential relocation expenses

- Travel and leisure activities

- Potential family support or inheritance plans

- Emergency fund requirements

Consider potential variations in your retirement journey. Some individuals might want to retire early, while others plan to work part-time or transition gradually. Your goals should remain flexible enough to accommodate unexpected life changes while maintaining a structured financial approach.

Utilize retirement calculators and financial planning tools to translate your vision into numerical targets. These resources can help you determine exactly how much money you’ll need to save monthly and annually to achieve your specific retirement objectives. Many online platforms offer free calculators that can provide immediate insights into your retirement funding requirements.

Successful goal setting means having a clear, quantifiable retirement vision supported by realistic financial projections. Your goals should feel both ambitious and achievable, providing motivation and a strategic roadmap for your financial planning journey.

Step 3: Calculate Your Retirement Needs

Calculating your retirement needs transforms abstract goals into a concrete financial blueprint. This step bridges the gap between your retirement vision and the financial resources required to make that vision a reality. The process demands precision, realistic projection, and a comprehensive understanding of your future financial landscape.

Income replacement becomes your primary calculation metric. Most financial experts recommend planning for 70-80% of your current annual income as a baseline retirement budget. However, this percentage is not a one-size-fits-all solution and requires personalized adjustment based on your specific lifestyle expectations and anticipated expenses.

According to the U.S. Department of Labor, developing an accurate retirement needs calculation involves multiple strategic considerations. Begin by creating a detailed projection of your expected retirement expenses. This means meticulously analyzing your current spending patterns and anticipating how they might change during retirement.

Consider these critical expense categories when calculating your retirement needs:

- Healthcare and potential medical expenses

- Housing costs, including potential downsizing or relocation

- Daily living expenses

- Transportation and mobility

- Leisure and personal interests

- Potential family support obligations

Utilize retirement calculators and financial planning tools to transform your projections into actionable numbers. Many online platforms offer sophisticated calculators that can help you determine exactly how much you’ll need to save monthly and annually. These tools typically factor in variables like inflation, expected investment returns, and potential lifestyle changes.

Dont overlook the impact of inflation and potential healthcare costs. Medical expenses tend to increase as you age, and inflation can significantly erode your purchasing power. A retirement calculation that doesnt account for these factors might leave you financially vulnerable. Consider consulting a financial advisor who can provide nuanced insights into long-term financial planning and help you develop a more comprehensive retirement strategy.

Successful completion of this step means having a clear, mathematically sound projection of your retirement financial needs. Your calculations should provide a realistic roadmap that bridges your current financial situation with your future retirement goals, offering both motivation and strategic direction for your financial journey.

Step 4: Choose the Right Investment Options

Selecting appropriate investment options represents a pivotal moment in your retirement planning journey. This step transforms your financial strategy from theoretical planning into actionable investment decisions that will shape your future financial security. Understanding the nuanced landscape of investment choices requires careful consideration of your personal risk tolerance, financial goals, and time horizon.

Diversification becomes your primary investment strategy. This principle means spreading your investments across multiple asset classes to minimize risk and maximize potential returns. Think of diversification like creating a balanced meal – you want a mix of different financial nutrients that work together to support your long-term financial health.

According to the SEC’s Investor Preparedness Checklist, understanding your personal risk tolerance is crucial. Begin by honestly assessing how comfortable you are with potential market fluctuations. Some individuals can withstand significant market volatility, while others prefer more conservative investment approaches.

Consider these fundamental investment vehicles for your retirement portfolio:

- 401(k) or employer-sponsored retirement plans

- Individual Retirement Accounts (Traditional and Roth IRAs)

- Index funds with low management fees

- Target-date retirement funds

- Diversified mutual funds

- Low-cost exchange-traded funds (ETFs)

Take time to understand each investment option’s unique characteristics. Target-date retirement funds, for example, automatically adjust their asset allocation as you approach retirement, becoming more conservative over time. Index funds offer broad market exposure with minimal management fees, making them attractive for long-term investors seeking steady growth.

Pay close attention to investment fees and expenses. Even small percentage differences in management fees can significantly impact your long-term returns. Look for investment options with low expense ratios and transparent fee structures. Many online platforms now offer robust tools that help you compare and analyze different investment options.

Remember that your investment strategy is not static. Regularly review and rebalance your portfolio, typically once or twice a year. As you move through different life stages, your investment approach should evolve to match your changing financial needs and risk tolerance.

The following table compares common retirement investment options mentioned in the guide, including core features to help you decide which options align with your strategy and risk tolerance.

| Investment Option | Key Features | Typical Risk Level |

|---|---|---|

| Employer 401(k) | Pre-tax or Roth, employer match available | Moderate |

| Traditional/Roth IRA | Tax-deferred or tax-free growth | Moderate |

| Index Funds | Broad market exposure, low management fees | Varies |

| Target-Date Retirement Funds | Auto-adjusts allocation as retirement nears | Decreasing over time |

| Diversified Mutual Funds | Professional management, varied holdings | Varies |

| Low-cost ETFs | Traded like stocks, low expense ratios | Varies |

Successful completion of this step means having a well-researched, diversified investment strategy aligned with your retirement goals. Your chosen investments should provide a balanced approach that offers growth potential while managing potential market risks.

Step 5: Create a Comprehensive Retirement Plan

Creating a comprehensive retirement plan transforms your financial aspirations into a structured, actionable roadmap. This critical step synthesizes all previous planning efforts into a cohesive strategy that addresses every aspect of your financial future. Think of this plan as a dynamic blueprint that will guide your financial decisions and provide a clear path toward retirement security.

Financial documentation becomes your foundation. Gather and organize all relevant financial documents, including tax returns, investment statements, insurance policies, and retirement account information. Create a centralized digital or physical file system that allows easy access and periodic review of your financial landscape.

According to the U.S. Department of Labor’s Retirement Toolkit, a comprehensive retirement plan should address multiple critical dimensions of financial preparedness. Begin by developing a detailed timeline that outlines specific financial milestones and savings targets for the years leading up to retirement.

Consider incorporating these essential elements into your retirement plan:

- Detailed income projection and sources

- Comprehensive expense tracking

- Emergency fund strategy

- Healthcare and long-term care provisions

- Social Security optimization strategy

- Tax efficiency planning

- Estate planning considerations

Consult with a financial professional who can provide personalized insights and help you refine your retirement strategy. They can offer objective analysis of your current financial situation and help identify potential gaps or opportunities in your planning approach. Many financial advisors offer comprehensive retirement planning services that go beyond simple investment advice.

Remember that a retirement plan is not a static document. Schedule regular review sessions, ideally quarterly or semi-annually, to assess your progress and make necessary adjustments. Life circumstances change, and your retirement plan should remain flexible enough to accommodate shifting personal and economic conditions.

Pay special attention to potential risk management strategies. This includes evaluating insurance needs, understanding potential healthcare costs, and developing contingency plans for unexpected financial challenges. Consider exploring long-term care insurance and developing a strategy for managing potential medical expenses during retirement.

Successful completion of this step means having a holistic, detailed retirement plan that provides clear guidance and instills confidence in your financial future. Your comprehensive plan should feel like a personalized roadmap that addresses your unique financial goals and potential challenges.

Step 6: Review and Adjust Your Plan Regularly

Regular review and adjustment of your retirement plan is not just a recommended practice its a critical strategy for maintaining financial resilience. Think of your retirement plan as a living document that evolves alongside your personal and financial circumstances. The most meticulously crafted plan can quickly become obsolete without consistent monitoring and strategic modifications.

Timing becomes a crucial element of your review process. Establish a structured schedule for comprehensive plan evaluations, typically recommending quarterly reviews with a more in-depth annual assessment. These review sessions allow you to track progress, identify potential risks, and make proactive adjustments before minor deviations become significant financial challenges.

According to the U.S. Department of Labor’s Retirement Toolkit, retirement plan reviews should encompass multiple financial dimensions. Begin by comparing your current financial position against the original goals and projections established in your comprehensive retirement plan.

Consider these key areas during your regular plan review:

- Investment performance and asset allocation

- Changes in personal income or employment status

- Shifts in family circumstances

- Evolving healthcare needs

- Potential tax law modifications

- Inflation and economic market conditions

Utilize digital tools and financial tracking software to streamline your review process. Many modern platforms offer comprehensive dashboards that aggregate financial information, track investment performance, and provide visual representations of your progress toward retirement goals. These technologies can transform complex financial data into easy-to-understand insights.

Dont view plan adjustments as failures but as intelligent, strategic refinements. Life is dynamic, and your retirement plan should reflect that reality. Major life events like marriage, career changes, unexpected medical expenses, or inheritance can significantly impact your financial trajectory. Remaining flexible and responsive ensures your retirement strategy remains robust and aligned with your evolving personal circumstances.

Consider scheduling an annual consultation with a financial advisor who can provide objective insights and help you navigate complex financial adjustments. Professional guidance can be particularly valuable when addressing nuanced aspects of retirement planning, such as tax optimization or investment rebalancing.

Successful completion of this step means establishing a consistent, structured approach to monitoring and adjusting your retirement plan. Your review process should feel empowering, providing clarity and confidence in your long-term financial strategy.

Secure Your Retirement with Expert Guidance and a Personalized Approach

Struggling to turn your retirement checklist into real-world results? The article highlights key pain points like uncertainty about calculating your retirement needs, choosing the right investment options, and making sense of complex planning documents. Many people feel overwhelmed or unsure if they are truly on track for a secure future. The steps discussed—assessing your finances, setting clear goals, developing a comprehensive strategy—are only part of the journey. Moving from planning to action can be the toughest stage of all.

At finblog.com, we understand how important your financial security is. Our trusted resources and expert advisors empower you to confidently navigate retirement planning, offering guidance that transforms checklists into real progress. Ready to take the next step? Visit finblog.com, explore our proven tools, and experience our secure, user-friendly forms to get a free personalized consultation. Act now to build a retirement plan that gives you peace of mind for the years ahead.

Frequently Asked Questions

What are the first steps in retirement planning?

Retirement planning begins by assessing your current financial situation, which involves evaluating your net worth, documenting assets and liabilities, and analyzing your income and expenses.

How do I set realistic retirement goals?

Setting realistic retirement goals requires you to envision your ideal retirement lifestyle, estimate necessary expenses, and use financial tools to determine the savings required to sustain that lifestyle.

What is the recommended percentage of income to save for retirement?

Financial experts typically recommend planning for about 70-80% of your current annual income as a baseline retirement budget, though this may vary depending on your lifestyle needs and expenses.

How often should I review my retirement plan?

It is advisable to review your retirement plan at least quarterly and conduct a more comprehensive annual review to ensure your plan adapts to changes in your financial situation or family circumstances.