TL;DR:

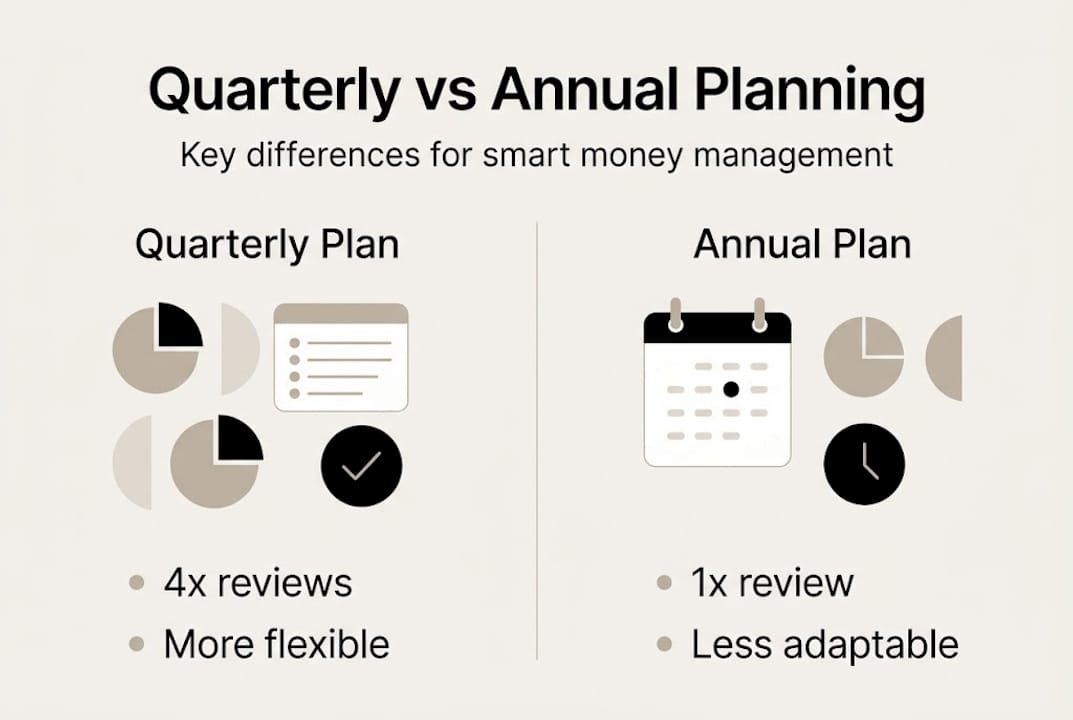

- Quarterly financial planning helps detect issues early and adjust before they become costly.

- Regular data collection and goal updates improve savings and debt management.

- Shorter planning cycles increase motivation and responsiveness compared to annual reviews.

Unexpected bills, a forgotten tax estimate, or a sudden market shift can unravel months of careful saving in days. Most people only realize something went wrong when they sit down for their annual review, and by then the damage is done. Quarterly financial planning breaks that reactive cycle. Instead of waiting 12 months to assess where you stand, you check in every three months, catch problems early, and adjust before small issues become expensive ones. This guide walks you through exactly how to prepare, execute, and verify a quarterly plan that works for both working professionals and individual investors.

Table of Contents

- What is quarterly financial planning and why does it matter?

- What you need before starting: Tools, data, and prerequisites

- Step-by-step guide: How to run your quarterly financial review

- Troubleshooting, common mistakes, and tracking progress

- A fresh perspective: Why quarterly trumps annual (and what most guides miss)

- Take the next step with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Quarterly reviews prevent surprises | Checking your finances every three months helps you adapt to changes and avoid missed goals. |

| Preparation makes reviews efficient | Gather income, expenses, and account data beforehand for a smoother, actionable review. |

| Track and adjust goals regularly | Break annual objectives into quarterly milestones for better progress and motivation. |

| Short cycles boost motivation | Frequent feedback and small victories help reinforce positive financial habits. |

What is quarterly financial planning and why does it matter?

Quarterly financial planning is a systematic process of reviewing your income, expenses, savings, debts, and goals every three months. Think of it as a scheduled tune-up for your finances. You’re not waiting for the engine light to come on. You’re checking under the hood on a regular schedule so nothing sneaks up on you.

The biggest advantage over annual planning is timing. A lot can change in 12 months: a job change, a rate hike, a new dependent, a market correction. Annual reviews catch these changes too late. Monthly reviews, on the other hand, can feel exhausting and create noise without much signal. Quarterly sits in the sweet spot, frequent enough to stay current, infrequent enough to see meaningful trends.

According to NEFE’s 2026 quarterly report, 42% of Americans set aside time quarterly to review debt or financial goals. That means more than half still rely on annual or ad-hoc reviews, leaving themselves exposed to gradual financial drift. For professionals managing both personal and business finances, the gap between check-ins is where things quietly go wrong.

Finance leaders are also rethinking the traditional annual plan. As highlighted in Why CFOs are Rethinking the Annual Plan, rolling quarterly reviews give organizations and individuals alike the agility to respond to volatility instead of being blindsided by it.

Here’s a quick comparison of the three main planning frequencies:

| Approach | Frequency | Best for | Key risk |

|---|---|---|---|

| Annual | Once per year | Big-picture goal setting | Misses midyear drift |

| Monthly | 12 times per year | Cash flow management | Can feel overwhelming |

| Quarterly | 4 times per year | Balanced review and adjustment | Requires discipline |

For investors and professionals, quarterly budgeting basics provide the foundation, while setting financial goals every quarter keeps your targets realistic and current. You can also benchmark your habits against US saving rate data to see how you compare nationally.

Key benefits of quarterly planning include:

- Catches midyear problems before they compound

- Improves savings consistency by creating accountability checkpoints

- Keeps investment goals aligned with current market conditions

- Reduces financial anxiety by replacing uncertainty with a clear schedule

What you need before starting: Tools, data, and prerequisites

Before your first quarterly review, you need to gather the right data. Walking into a review without complete information is like trying to navigate without a map. You’ll make decisions based on an incomplete picture, and that leads to poor adjustments.

Start by collecting these core data points:

- All income sources: salary, freelance, dividends, rental income

- Fixed and variable expenses: rent, utilities, subscriptions, groceries

- Account balances: checking, savings, investment, retirement

- Outstanding debts: credit cards, student loans, mortgages, auto loans

- Upcoming obligations: insurance renewals, estimated taxes, tuition payments

Once you have the data, you need the right tools. A spreadsheet works well if you prefer manual control. Budgeting apps like YNAB or Mint automate tracking and generate summaries quickly. Many professionals use customized templates that combine both approaches. Explore financial planning tools to find what fits your workflow, and use planning financial milestones as a framework for structuring your review.

Your emergency fund is one of the most critical data points to assess. The NEFE 2026 report notes that average savings balances vary significantly by income level, but the standard benchmark remains 3 to 6 months of essential expenses. Here’s a simple way to assess where you stand:

| Emergency fund status | Monthly expenses covered | Action needed |

|---|---|---|

| Critical | Less than 1 month | Prioritize building immediately |

| Below standard | 1 to 2 months | Increase savings rate this quarter |

| Adequate | 3 to 6 months | Maintain and redirect surplus |

| Strong | 6 or more months | Focus on investment growth |

Your savings rate is equally important. Divide your total monthly savings by your take-home income. If the number is below 15%, that’s your first target to address.

Pro Tip: Track your essential expenses for at least three months before your first quarterly review. This gives you a reliable baseline and prevents you from making decisions based on one unusually high or low month.

Step-by-step guide: How to run your quarterly financial review

With your data assembled and tools ready, here’s exactly how to run an effective quarterly review. This process works whether you’re a solo investor or managing finances across a small business.

- Update all your financial data. Pull fresh statements for every account. Confirm your income total for the quarter, including any irregular earnings.

- Review current finances against last quarter. Compare income, spending, and savings to your previous quarter’s targets. Note where you exceeded or fell short.

- Update your projections. Adjust your annual forecast based on what actually happened this quarter. If your income grew, revise your savings targets upward.

- Check savings and debt progress. Are you on track to hit your annual savings goal? Is your debt balance decreasing at the rate you planned?

- Revise your goals. Life changes. A promotion, a new expense, or a market shift may require you to update your targets. Adjust now, not in December.

- Implement your updated budget. Use a monthly budgeting template to translate your quarterly plan into monthly action steps. If you’re new to the process, creating a budget from scratch is a logical starting point.

According to the NEFE 2026 report, 39% of Americans set budgets on a quarterly basis, and those who do tend to maintain stronger savings habits over time. The personal saving rate data from the Bureau of Economic Analysis shows how national trends shift quarter to quarter, giving you useful context for your own targets.

Expert recommendation: Aim to save at least 15 to 20% of your take-home pay each quarter. If you’re not there yet, increase your savings rate by 1 to 2% each quarter until you reach that benchmark.

Pro Tip: Set a recurring calendar reminder at the start of each quarter, January, April, July, and October. Treat it like a non-negotiable meeting. Consistency is the single biggest predictor of long-term success with quarterly planning.

Troubleshooting, common mistakes, and tracking progress

Even disciplined planners run into problems. Knowing the most common mistakes in advance helps you sidestep them before they derail your progress.

Common mistakes to avoid:

- Skipping a review quarter. Missing one quarter creates a six-month blind spot. If life gets in the way, do a shorter 30-minute version rather than skipping entirely.

- Focusing only on spending. Cutting expenses is only half the picture. Ignoring income growth, investment returns, or debt paydown gives you a distorted view.

- Ignoring new obligations. A new lease, insurance policy, or loan changes your financial picture significantly. Always update your obligations list at the start of each review.

- Setting goals that don’t change. Goals set in January may be irrelevant by October. Rigid goals that don’t adapt to real life lead to frustration and abandonment.

When a major life event occurs, such as a marriage, a job loss, or a new child, your quarterly review needs to expand. Revisit your emergency fund target, update your income projections, and reassess your debt strategy. As rolling planning research confirms, frequent reviews are far more effective than annual snapshots when handling life changes. Use updating your plan as a guide for restructuring after major shifts, and revisit your goal tracking tips to stay focused.

Here’s how quarterly tracking compares to other approaches:

| Tracking method | Visibility | Adaptability | Effort level |

|---|---|---|---|

| Annual review | Low | Low | Minimal |

| Rolling monthly | High | High | Significant |

| Quarterly review | Medium-high | Strong | Manageable |

Pro Tip: Celebrate small wins. Hit your savings target for the quarter? Acknowledge it. Paid off a credit card? Mark it. Positive reinforcement builds the habit faster than any spreadsheet formula.

A fresh perspective: Why quarterly trumps annual (and what most guides miss)

Most financial guides treat quarterly planning as a nice-to-have, a bonus step for the especially organized. That framing misses the point entirely. Quarterly planning is not an add-on. It’s a fundamentally different relationship with your money.

Annual plans create a false sense of security. You set targets in January, feel good about it, and then don’t look again until December. By then, six months of financial creep, small overspends, rising subscriptions, and ignored debt have quietly eroded your progress. You’re not behind because you made one big mistake. You’re behind because no one flagged the small ones.

Quarterly check-ins fix that. They create four natural moments each year to course-correct before problems compound. The rolling planning model used by forward-thinking CFOs proves that shorter planning cycles handle volatility better than rigid annual frameworks.

What most guides also miss is the emotional benefit. Shorter cycles mean shorter distances between wins. When you see progress every 90 days, motivation stays high. Annual plans often feel abstract and distant. Quarterly plans feel real and achievable. Use adapting to change as your framework for keeping each quarter responsive to what life actually brings.

Take the next step with expert support

If you’re ready to make quarterly reviews a consistent habit, Finblog offers a growing library of guides, templates, and tools built specifically for working professionals and investors. Whether you’re just starting to structure your finances or looking to sharpen an existing system, the resources here meet you where you are. Explore budgeting strategies to build a stronger foundation, or browse the full range of planning tools to find what fits your workflow. The goal is simple: turn quarterly planning from a task into a habit that pays off year after year.

Frequently asked questions

What is the main advantage of quarterly over annual financial planning?

Quarterly planning surfaces problems and opportunities four times a year instead of one, giving you far more chances to course-correct early before small issues become costly ones.

How much should I aim to save each quarter?

Target saving at least 15 to 20% of your take-home pay each quarter, and maintain an emergency fund covering 3 to 6 months of essential expenses, as recommended by the NEFE 2026 benchmarks.

What data should I collect before my financial review?

Gather all income sources, fixed and variable expenses, account balances, loan statements, and any upcoming financial obligations to ensure your review reflects your complete financial picture.

How do I stay motivated to keep up with quarterly reviews?

Set recurring calendar reminders at the start of each quarter and acknowledge every milestone you hit, no matter how small, to reinforce the habit over time.

Is quarterly planning suitable for both individuals and businesses?

Yes, though businesses often benefit from a hybrid approach that combines quarterly rolling reviews with an annual strategic plan for longer-term stability during volatile periods.

Recommended

- How to Budget Effectively: Master Your Finances in 2025 – Finblog

- 7 Smart Financial New Year Resolutions for 2025 – Finblog

- Steps to financial independence in 2026: practical guide – Finblog

- Financial literacy 2026: master investing and wealth management – Finblog

- Starting Fresh in 2025: How Bankruptcy Law Can Help You Rebuild Your Financial Future — Attorney Sean Quinlan