TL;DR:

- Dollar cost averaging (DCA) helps investors avoid emotional decision-making by investing fixed amounts at regular intervals.

- It reduces risk by smoothing out market volatility and prevents timing errors, especially during downturns.

Market swings can make even confident investors second-guess every move. When prices drop sharply, the instinct is to wait for a better moment, and when prices spike, fear of buying at the top kicks in. This cycle of hesitation is one of the biggest reasons individual investors underperform over the long run. Dollar cost averaging (DCA) sidesteps that trap entirely. Instead of trying to predict the perfect moment to invest, you commit to a fixed amount on a fixed schedule, letting the math work in your favor over time.

Table of Contents

- Understanding dollar cost averaging

- How dollar cost averaging reduces risk

- Who should consider dollar cost averaging?

- How to get started with dollar cost averaging

- What most investors get wrong about dollar cost averaging

- Take your next step toward smarter investing

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Steady investment wins | Dollar cost averaging helps you build wealth without guessing market highs and lows. |

| Reduces emotional mistakes | By automating investments, you bypass the stress of market timing and emotional decision-making. |

| Best for regular savers | DCA is ideal for those investing smaller amounts consistently, not large, one-time sums. |

| Automation is easy | Most investment platforms and robo-advisors support DCA, making it simple for beginners and busy professionals. |

Understanding dollar cost averaging

Dollar cost averaging is easier to understand than most people expect. At its core, it means investing the same dollar amount at regular intervals, whether markets are up, down, or flat. You are not reacting to headlines. You are not waiting for a dip. You are just consistently putting money to work.

As defined by Finblog’s guide on the topic, “dollar cost averaging is a strategy where you invest a fixed amount at regular intervals, regardless of market conditions.” That simplicity is precisely why it works for so many people, especially those who do not have hours each week to study charts and earnings reports.

Here is a straightforward example. Say you invest $100 every month into a broad index fund:

| Month | Share price | Shares purchased |

|---|---|---|

| January | $20 | 5.00 |

| February | $10 | 10.00 |

| March | $25 | 4.00 |

| April | $15 | 6.67 |

| Total | Avg: $17.50 | 25.67 shares |

You spent $400 total and now hold 25.67 shares. Your average cost per share is about $15.58, even though the share price bounced between $10 and $25. That is the quiet power of DCA. When prices are low, your fixed dollar amount buys more shares. When prices are high, it buys fewer. Over time, this naturally lowers your average cost per share compared to buying all at once at a single price point.

The emotional benefit is just as important as the math. DCA removes the decision from the equation. You set a rule and follow it, which means fear and greed have far less influence over your portfolio.

- Reduces emotional decision-making: No more agonizing over whether today is a good day to buy.

- Builds investing habits: Regular contributions create a savings discipline that compounds over years.

- Works across account types: You can apply DCA inside a 401(k), IRA, brokerage account, or even a robo-advisor.

- Scales with your income: You can start with $50 a month and increase as your income grows.

- Accessible for everyone: You do not need a large sum to begin.

Pro Tip: Set up automatic transfers from your checking account to your investment account on payday. When the money moves before you see it, you spend less time deliberating and more time accumulating.

How dollar cost averaging reduces risk

Now that you know what DCA is, let’s explore how it actually reduces your investment risk. This is where DCA earns its reputation as a stress-reducing strategy, not just a beginner tactic.

The core risk in investing is putting a large amount of money into the market at exactly the wrong time. Imagine investing your entire $12,000 savings in February 2020, just weeks before the pandemic-driven crash wiped out nearly 34% of the S&P 500’s value. A lump-sum investor in that position would have lost roughly $4,080 almost immediately. A DCA investor spreading $1,000 per month over 12 months would have bought shares at much lower prices during the crash months, dramatically reducing the average cost basis and speeding up recovery.

As Finblog explains in their resource on investing during volatility, “DCA can help smooth out the effects of market volatility, reducing the risk of investing a lump sum at the wrong time.” This is not just theory. It plays out in every major market correction.

Here is a side-by-side comparison of lump-sum versus DCA investing over a volatile six-month period:

| Strategy | Total invested | Avg. cost per share | Shares owned | Portfolio value at recovery |

|---|---|---|---|---|

| Lump sum ($600 in month 1) | $600 | $30.00 | 20 | $700 |

| DCA ($100/month x 6) | $600 | $22.50 | 26.67 | $934 |

The DCA investor owns significantly more shares at recovery, even though both investors put in the same total amount. That gap represents real, tangible wealth.

“DCA minimizes regret and builds discipline. The investor who sticks to a schedule during a downturn is the one who benefits most when markets recover.” — Investment strategist insight shared across major financial planning communities.

The biggest pitfall with DCA is also the most common one: stopping contributions when markets fall. This is the exact opposite of what you should do. A falling market means your fixed investment buys more shares at a discount. Pausing your DCA during a downturn is like walking away from a sale right when prices are lowest. Reviewing market history and strategy shows that investors who stayed the course through periods of geopolitical turmoil and volatility consistently outperformed those who paused or exited.

Pro Tip: During market drops, remind yourself that your next DCA contribution is about to buy shares on sale. Framing it that way makes it much easier to stay committed.

Who should consider dollar cost averaging?

With risk reduction explained, the next step is knowing whether DCA is right for you personally. The honest answer is that DCA fits a wide range of investors, but it is not universally the best choice in every scenario.

DCA works exceptionally well for working professionals who receive a regular paycheck. You already have a predictable income stream, which makes scheduling consistent investments straightforward. It also works for people who are new to investing and are still building confidence. Instead of waiting until you feel “ready” or have the perfect amount saved up, DCA lets you start immediately with whatever you can afford.

As noted in Finblog’s ETF investing guide, “DCA is especially useful for investors who want to avoid market timing and build wealth gradually.” This makes it a natural fit for ETF (exchange-traded fund) investors, since ETFs give broad market exposure and trade at low cost, pairing perfectly with a systematic contribution plan.

Here are the investor profiles that benefit most from DCA:

- New investors: Removes the paralysis of trying to pick the right moment.

- Busy professionals: Automation handles everything once it is set up.

- Risk-averse individuals: Smaller, steady contributions feel less scary than large one-time bets.

- Long-term wealth builders: Works best over five, ten, or twenty-plus years.

- Investors without a large lump sum: DCA lets you participate in the market without needing thousands upfront.

“For most investors, consistency wins over trying to time the best day. The habit of investing regularly matters far more than the precision of when you buy.”

However, DCA is not always the optimal move. If you receive an inheritance, a bonus, or proceeds from selling a property, and you have a genuinely long time horizon in a historically rising market, research suggests that investing the lump sum immediately tends to outperform DCA roughly two-thirds of the time, simply because markets rise more often than they fall. The catch is the emotional and timing risk. Most people are not emotionally prepared to invest $50,000 in a single transaction, and if timing turns against them, the psychological damage can cause them to sell at exactly the wrong moment.

For building a solid investment planning framework, DCA remains one of the most reliable tools available to everyday investors, precisely because it separates emotion from execution.

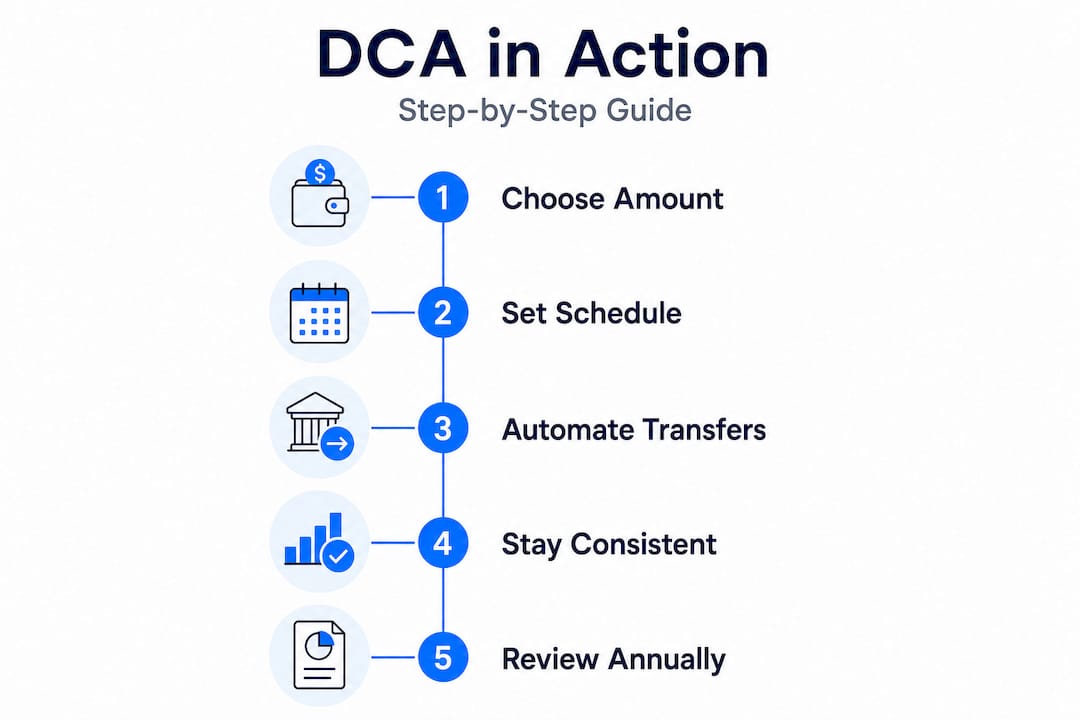

How to get started with dollar cost averaging

If you think DCA is a fit for your goals, here’s a simple way to put it to work. The barrier to entry is genuinely low, and the setup takes less time than most people expect.

- Decide on your contribution amount. Start with what you can afford to invest monthly without disrupting your emergency fund or everyday expenses. Even $50 or $100 per month builds meaningful wealth over a decade.

- Choose your investment schedule. Monthly is the most common approach because it aligns with paychecks and billing cycles. Weekly contributions work too if your platform supports fractional shares, since they smooth out price variability even further.

- Pick your account type. A tax-advantaged account like a Roth IRA or 401(k) maximizes your long-term gains. If you have maxed out those options, a standard brokerage account works fine.

- Select your investment. Broad-market index ETFs or mutual funds are the most popular choice for DCA investors because they offer instant diversification at low cost. Resources like Finblog’s guide on how to pick investments can help you narrow down the right options.

- Automate everything. This is the single most important step. Set up automatic contributions so money moves from your bank to your investment account without any manual action on your part.

- Resist the urge to monitor daily. Review your portfolio quarterly or annually. Daily checking leads to emotional reactions that undermine the whole point of DCA.

Robo-advisors have made step five almost effortless. Platforms like Betterment, Wealthfront, and Schwab Intelligent Portfolios allow you to set a contribution schedule, choose a risk level, and walk away. As Finblog notes, “setting up DCA can be automated with most investment platforms and robo-advisors,” making it one of the lowest-friction strategies available to modern investors.

Complementing your DCA plan with strong savings habits also accelerates your results. Finblog’s collection of investor saving tips offers practical guidance for finding more money to invest each month, which directly increases the power of your DCA contributions over time.

Pro Tip: Once per year, increase your monthly contribution by the same percentage as your raise or by $25 to $50. This small adjustment, made just once annually, can dramatically increase your ending portfolio value over a 20-year horizon without feeling painful in the short term.

What most investors get wrong about dollar cost averaging

Before wrapping up, it is worth acknowledging what seasoned investors have learned, often the hard way, about dollar cost averaging. And the biggest misconception is this: DCA is not a system for beating the market. It is a system for beating yourself.

Most investors who try DCA start strong. They automate contributions, they feel good about the habit, and then the market drops 20%. Suddenly, the automation feels wrong. They pause. They wait to “see what happens.” And in doing so, they miss the months when DCA delivers its most powerful returns, buying shares at prices that will look like obvious bargains in hindsight.

The volatility beneath the surface of even “calm” markets is often far more extreme than headlines suggest. Stocks that appear stable can swing wildly at the sector level. DCA works by absorbing that turbulence automatically, without requiring you to diagnose it, respond to it, or feel it.

Here is the uncomfortable truth that most financial content glosses over: DCA will not always outperform a lump sum in a bull market. A sophisticated investor with perfect timing and nerves of steel might do better going all in at the right moment. But that investor is extraordinarily rare. For the vast majority of working professionals who have jobs, families, and limited time to analyze markets, DCA is not a consolation prize. It is the smarter, more realistic choice.

The real value of DCA is not in the returns it generates. It is in the returns it protects you from destroying through impulsive decisions. Staying invested through volatility, letting compounding work over decades, and keeping your emotions out of the equation, that is where real wealth is built.

Take your next step toward smarter investing

With real-world perspective in mind, here’s where you can get support for your investment journey. At Finblog, you’ll find a growing library of practical, jargon-free resources built specifically for investors at every stage. Whether you are just starting out or looking to sharpen an existing strategy, the content is designed to move you from uncertainty to action. A great place to start is the step-by-step guide to creating an investment plan, which walks you through setting goals, choosing the right accounts, and building a strategy you can actually stick to. Learning is the first step. Putting that learning into a structured plan is where results happen.

Frequently asked questions

Does dollar cost averaging actually beat lump-sum investing?

Over long horizons, DCA can reduce risk but may not always outperform lump-sum investing in a rising market, though it smooths out volatility and reduces the danger of investing everything at the wrong time.

Is dollar cost averaging good for beginners?

Yes, it is one of the best starting strategies because it removes the pressure of timing the market and builds consistent wealth gradually, as it is especially useful for those who want to avoid market timing altogether.

How often should I invest with dollar cost averaging?

Monthly contributions are the most common and practical schedule, but weekly or quarterly contributions also work effectively as long as you stay consistent throughout market ups and downs.

Can I automate dollar cost averaging?

Yes, most brokerages and robo-advisors let you schedule recurring investments automatically, making setting up DCA one of the simplest and most hands-off strategies available today.

When is DCA not the best approach?

If you have a large lump sum and a very long investment horizon in a historically rising market, investing it all at once often captures more growth, though it requires strong emotional discipline to avoid panic-selling during downturns.