Choosing where to invest your hard-earned money can feel risky when technology is involved. As more working professionals seek safe investment solutions, robo-advisors have become a popular alternative to traditional portfolio management. Understanding what these platforms really offer, along with the safety myths that surround them, helps you make informed decisions about securing your financial future.

Table of Contents

- Defining Robo Advisors And Safety Myths

- Types Of Robo Advisors And How They Work

- Regulatory Oversight And Investor Protections

- Cybersecurity Measures And Data Safeguards

- Risks, Limitations, And Comparison To Traditional Advisors

Key Takeaways

| Point | Details |

|---|---|

| Understanding Robo-Advisors | Robo-advisors are automated platforms that provide financial advice and manage investments with algorithms based on user inputs. |

| Addressing Safety Myths | Modern robo-advisors implement strong security measures, while regulatory structures ensure investor protection similar to human advisors. |

| Investment Strategies | Different robo-advisors utilize various investment methodologies, including passive indexing and mean-variance optimization, catering to diverse investor needs. |

| Limitations and Risk | Robo-advisors excel in managing simple portfolios but may lack the capability to handle complex financial situations and emotional support. |

Defining Robo Advisors and Safety Myths

A robo-advisor is an automated online platform that uses algorithms to provide financial advice and manage investment portfolios based on your goals and risk tolerance. Think of it as a digital financial advisor available 24/7, making investment decisions without human emotion or bias.

These platforms have grown rapidly over the past decade, attracting millions of professionals like you who want streamlined portfolio management. They promise lower fees, accessibility, and consistent investment strategies. But myths about their safety have slowed adoption among skeptical investors.

What Robo-Advisors Actually Do

Robo-advisors handle several core functions:

- Goal-based planning: You input your financial objectives, timeline, and risk tolerance through questionnaires

- Automated portfolio construction: Algorithms select appropriate asset allocations from thousands of investment options

- Continuous rebalancing: Your portfolio automatically adjusts to maintain your target allocation

- Tax-loss harvesting: Many platforms sell losing positions to offset gains and reduce tax liability

- Low-cost execution: Minimal human oversight keeps fees significantly lower than traditional advisors

The technology behind robo-advisors relies on rules-based algorithms that follow predetermined decision frameworks. Your inputs determine your investor profile, and the algorithm matches you with a diversified portfolio based on modern portfolio theory.

The Safety Myths Holding Investors Back

Three major misconceptions discourage working professionals from using robo-advisors:

Myth #1: Algorithms can’t handle complex situations. While robo-advisors excel at standard investing, automated platforms cannot fully replace personalized human advisory services for nuanced financial planning. However, for straightforward portfolio management and regular rebalancing, they perform consistently.

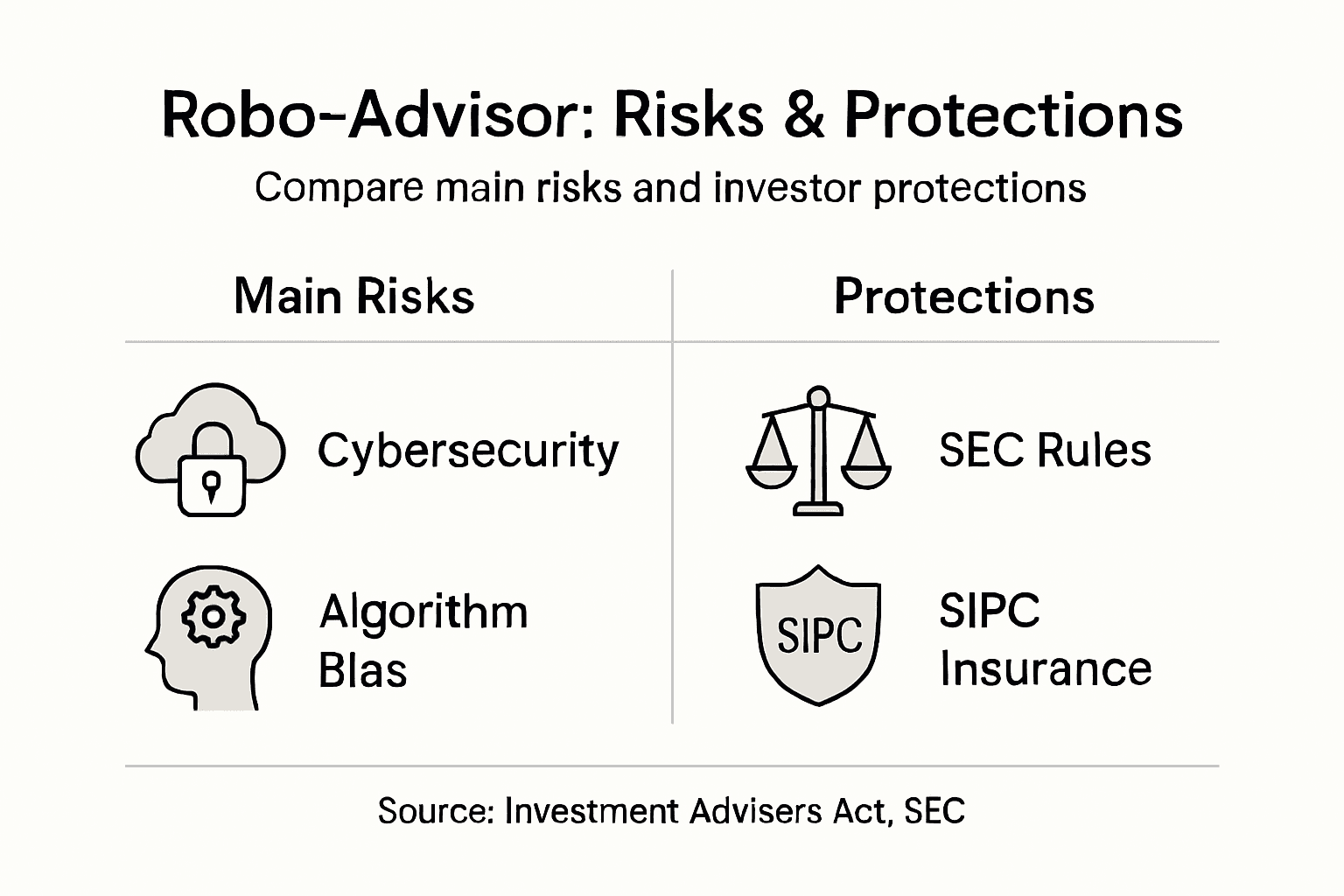

Myth #2: Your data isn’t secure. This concern is valid historically, but modern robo-advisors now employ institutional-grade security measures including encryption, two-factor authentication, and regular security audits. Banks and custodians holding assets add additional protection layers.

Myth #3: They eliminate investment bias. Robo-advisors reduce your emotional bias through mechanical execution, but algorithmic bias remains possible. Systems reflect their programming assumptions about markets and risk, which may not account for unexpected economic conditions.

Why Safety Matters More Than You Think

Your investment account represents years of earning and compound growth. Understanding regulatory oversight and transparency requirements becomes essential before trusting an algorithm with your portfolio.

Robo-advisors operate under the same regulatory framework as human advisors in most countries. They must register as investment advisers, follow fiduciary rules, and maintain adequate asset protection. This regulatory structure provides meaningful safeguards.

Real safety comes from understanding both what robo-advisors do well and where they have limitations—not avoiding them entirely.

The platforms most popular with professionals like yourself typically offer hybrid models combining algorithm-driven investing with access to human advisors for complex decisions. This blended approach addresses the legitimate concerns without sacrificing the efficiency benefits.

Pro tip: Before selecting any robo-advisor, verify it’s registered with the Securities and Exchange Commission (SEC) or your country’s equivalent financial regulator—this single check eliminates most fraudulent platforms.

Types of Robo Advisors and How They Work

Robo-advisors fall into distinct categories based on their investment approach and service model. Understanding these differences helps you choose a platform that aligns with your specific needs and comfort level with automation.

The two main investment methodologies are passive indexing and mean-variance optimization. Passive indexing tracks broad market indices like the S&P 500, keeping costs low and reducing active trading. Mean-variance optimization analyzes historical risk-return relationships to construct diversified portfolios tailored to your risk tolerance.

Pure Automation vs. Hybrid Models

Robo-advisors operate across a spectrum from fully automated to blended with human support:

- Pure robo-advisors: Algorithm-driven portfolio construction with minimal human interaction, ideal for straightforward investors

- Hybrid robo-advisors: Automated management combined with access to human financial advisors for complex questions

- White-label solutions: Banks and brokers using robo technology behind their own brands

Most platforms targeting professionals like you now offer hybrid models. You get algorithmic efficiency for routine decisions while maintaining human expert access when needed.

Here’s a quick comparison of pure robo-advisors, hybrid models, and traditional advisors for investment management:

| Service Type | Human Interaction | Customization Level | Best Use Case |

|---|---|---|---|

| Pure Robo-Advisor | Minimal, mostly automated | Standardized based on questionnaire | Routine investing and rebalancing |

| Hybrid Robo-Advisor | Occasional expert access | Tailored, with algorithm and advisor input | Complex situations and personalized needs |

| Traditional Advisor | High, face-to-face or remote | Deeply personalized, ongoing advice | Multifaceted financial planning and coaching |

How Robo-Advisors Process Your Information

Every robo-advisor follows a similar operational flow. First, you complete a detailed questionnaire covering your financial goals, investment timeline, income level, existing assets, and risk tolerance.

The platform then uses algorithmic asset allocation to build a personalized portfolio. This involves determining what percentage of your money goes to stocks, bonds, real estate, and other asset classes based on your profile.

Once deployed, your portfolio enters the rebalancing phase. Your robo-advisor continuously monitors performance and automatically sells winners and buys losers to maintain your target allocation. This mechanical approach removes emotional decision-making.

Key Operational Differences Between Platforms

While the basic structure mirrors across providers, real differences emerge in execution:

- Asset selection: Some platforms use primarily index funds for low costs, while others incorporate individual stocks or alternative investments

- Rebalancing frequency: Ranging from quarterly to event-triggered (when allocations drift beyond thresholds)

- Tax optimization: Advanced platforms employ tax-loss harvesting automatically; basic ones don’t

- Fee structures: Typically 0.25% to 0.50% annually, but some charge flat fees or wrap commissions

- Minimum investment requirements: From zero to $500,000, depending on platform tier

The real value of robo-advisors lies not in outperforming markets, but in providing consistent execution of sound investment principles without emotional interference.

Personalized portfolio assignments based on your risk profile represent the core innovation. Rather than offering generic portfolios, modern robo-advisors create customized allocations reflecting your unique situation.

Your choice depends on two factors: how much hand-holding you prefer and what investment strategy resonates with you. Some professionals value maximum automation; others prefer hybrid models where they can consult advisors about life changes affecting their strategy.

Pro tip: Request a “before and after” rebalancing report from any platform you’re considering—seeing actual examples of how they manage your money during market volatility reveals whether their approach matches your comfort level.

Regulatory Oversight and Investor Protections

Robo-advisors operate within established regulatory frameworks designed to protect your money and ensure fair treatment. Understanding these protections gives you confidence that your automated advisor meets rigorous legal standards.

In the United States, robo-advisors fall under the Investment Advisers Act of 1940. This means registered platforms must comply with fiduciary duties, maintain client confidentiality, and disclose conflicts of interest. Similar regulatory structures exist in Canada, the United Kingdom, and most developed markets.

Fiduciary Standards and Robo-Advisor Compliance

A fiduciary is legally required to act in your best interest, prioritizing your needs over their profits. The critical question: can algorithms meet fiduciary standards? The answer is yes.

Robo-advisors can meet fiduciary standards with proper programming and oversight. Regulators focus on transparency and conflict-of-interest management rather than questioning algorithmic capability. This distinction matters because it means your robo-advisor provider must disclose any conflicts—such as pushing their own investment products over competitors’ options.

The key protection: registered robo-advisors must document their decision-making logic and justify their recommendations based on your profile.

Key Investor Protections You Have

Multiple layers of protection safeguard your investments when using regulated robo-advisors:

- SEC or FINRA registration: Verified on official regulatory databases; fraudulent platforms fail this check immediately

- Custody requirements: Your assets held by independent custodians (banks or brokers), not the robo-advisor company itself

- Net worth verification: Ensures advisors are stable and properly capitalized

- Insurance coverage: Many custodians carry SIPC insurance (up to $500,000 per account) protecting against firm insolvency

- Audit requirements: Regular compliance reviews of algorithmic processes and client suitability assessments

Regulatory oversight doesn’t prevent market losses, but it prevents fraud and ensures your robo-advisor operates with transparent, conflict-managed processes.

These protections apply universally to registered platforms. Before opening an account, verify your chosen robo-advisor is registered by checking the SEC’s Investment Adviser Public Disclosure database or your country’s equivalent.

Below is a summary of common investor protections you receive with regulated robo-advisors:

| Protection Type | What It Provides | Who Enforces It |

|---|---|---|

| Independent Custody | Assets held by third-party bank or broker | Financial regulators (e.g., SEC, FINRA) |

| Insurance Coverage | Up to $500,000 SIPC per account | SIPC and partnering custodians |

| Regulatory Registration | Verifies legitimacy and compliance | SEC, your country’s financial regulator |

| Regular Audits | Ensures suitable advice and process transparency | Independent auditors and regulators |

Emerging Regulatory Challenges

Regulators continue evolving frameworks to address robo-specific risks. Regulatory frameworks must address scale, competence, and honesty concerns as algorithms make millions of decisions across millions of accounts.

Key areas receiving regulatory attention include algorithmic suitability testing, cybersecurity standards, and data privacy protocols. This ongoing evolution protects you by closing gaps as technology advances.

Your role involves verifying registration status and understanding what conflicts your platform discloses. Don’t assume all robo-advisors are equally regulated—registration status and disclosure practices vary significantly.

Pro tip: Before funding your account, request the robo-advisor’s Form ADV Part 2A (their disclosure document) and review the “conflicts of interest” section—this five-minute read reveals what the platform profits from and how they manage those conflicts.

Cybersecurity Measures and Data Safeguards

Your personal financial data—income, assets, investment history, Social Security number—represents a high-value target for cybercriminals. Understanding how robo-advisors protect this information provides peace of mind when automating your investments.

Reputable robo-advisors implement multi-layered security architecture designed to prevent unauthorized access and data breaches. These aren’t casual protections; they’re institutional-grade systems protecting millions of dollars across millions of accounts.

Security Technologies Protecting Your Account

Modern robo-advisors employ several defense mechanisms working in parallel:

- Encryption in transit: Data traveling between your device and the platform’s servers uses military-grade encryption (TLS 1.2 or higher)

- Encryption at rest: Information stored on company servers remains encrypted, making stolen data unreadable

- Multi-factor authentication: Login requires both your password and a second verification method (app, SMS, or security key)

- Zero-trust architecture: Systems assume every access request is potentially hostile, requiring continuous verification rather than trusting established connections

- Regular security audits: Third-party firms conduct penetration testing and vulnerability assessments

These technologies work together rather than independently. Even if hackers breach one layer, others prevent data exposure.

Industry Standards and Compliance

Robo-advisors must align with financial industry security standards that exceed typical internet companies. Advanced cybersecurity frameworks establish baselines for protecting client data across financial institutions.

Most regulated platforms comply with PCI DSS (Payment Card Industry Data Security Standard) for handling payment information and GLBA (Gramm-Leach-Bliley Act) requiring financial institutions to protect customer privacy. These regulatory requirements create enforceable security standards.

Additionally, platforms must establish incident response teams trained to detect and contain security breaches within minutes of discovery. This rapid response capability prevents widespread data exposure.

What You Control in Your Security

Technology alone doesn’t guarantee account safety. Your behavior matters significantly. Best practices include using strong passwords and enabling multi-factor authentication to prevent account takeovers even if platform defenses are compromised.

Many robo-advisor breaches succeed not because of weak platform security but because users reuse passwords across multiple websites or click malicious links. Your vigilance complements institutional protections.

Security is a partnership: platforms build the vault, but you control who holds the key.

Start by creating unique, 16-character passwords combining uppercase, lowercase, numbers, and symbols. Avoid password managers unless they use military-grade encryption. Enable two-factor authentication on your account and your linked bank accounts.

Never access your robo-advisor account from public WiFi without a VPN. Hackers monitoring public networks can intercept unprotected connections even with platform encryption.

Pro tip: Check your robo-advisor’s security page or request their SOC 2 Type II report—this third-party audit confirms they maintain appropriate safeguards and log all security incidents, giving you independent verification beyond marketing claims.

Risks, Limitations, and Comparison to Traditional Advisors

Robo-advisors aren’t perfect solutions for every investor. Understanding their genuine limitations helps you decide whether automation serves your needs or whether you require human expertise for complex situations.

The core trade-off is simple: robo-advisors excel at efficient, low-cost portfolio management for straightforward goals. They struggle with nuanced life changes, behavioral coaching, and complex tax situations requiring judgment calls.

Key Limitations of Robo-Advisors

While robo-advisors offer significant advantages, real constraints exist:

- Limited nuanced judgment: Algorithms follow predetermined rules and cannot adapt to unexpected personal circumstances like job loss, inheritance, or family emergencies

- Algorithmic bias risks: Systems reflect their programming assumptions and historical data, potentially missing emerging market conditions or unconventional strategies

- Reduced behavioral coaching: Robo-advisors cannot provide emotional support during market downturns or help you resist panic-selling urges

- Complex situation gaps: Tax-loss harvesting, charitable giving strategies, and estate planning require human expertise

- Digital platform reliance: Investors uncomfortable with technology or lacking internet access face barriers

Robo-advisors are best suited for straightforward investment objectives rather than multifaceted financial planning addressing major life transitions.

Robo-Advisors vs. Traditional Advisors

The choice between automation and human guidance depends on your situation. Here’s how they compare:

Robo-Advisors Advantages:

- Lower fees (typically 0.25%-0.50% versus 1%-2% for human advisors)

- 24/7 accessibility and instant portfolio adjustments

- No emotional bias in decision-making

- Ideal for investors with simple goals and substantial assets ($10,000+)

Traditional Advisors Advantages:

- Deep client relationships and personalized advice tailored to unique situations

- Comprehensive financial planning beyond investing (insurance, estate planning, tax strategy)

- Behavioral coaching preventing emotional mistakes

- Face-to-face accountability and customized guidance

- Better suited for complex situations, major life events, or wealth management

The best choice isn’t robo versus human—it’s matching your complexity level to the right service type.

Many working professionals benefit from hybrid approaches. You might use a robo-advisor for core retirement savings while consulting a human advisor annually about major changes affecting your overall financial picture.

Real Risks You Should Monitor

Beyond limitations, actual risks exist when using robo-advisors:

- Market downturns test your conviction: Without human advisors reminding you why you chose your allocation, panic-selling becomes tempting

- Algorithmic errors happen: Software bugs or unintended consequences from algorithm updates occasionally cause problems

- Platform concentration risk: If your robo-advisor fails, your assets need protecting through custodian insurance (typically $500,000 coverage)

- Regulatory gaps remain: As technology outpaces regulation, some edge-case scenarios lack clear protection

These risks are manageable but real. Verify your platform has SIPC insurance and independent asset custody before investing significant money.

Pro tip: Consider a “barbell” strategy: automate your straightforward core holdings with a robo-advisor, then consult a human advisor annually about major life changes, tax-loss harvesting opportunities, or strategic portfolio adjustments affecting your overall wealth plan.

Secure Your Investment Journey with Expert Guidance

Are you concerned about the safety and risks of robo-advisors after reading about algorithmic biases, cybersecurity measures, and regulatory protections? These challenges highlight the importance of making informed decisions when automating your investments. At Finblog, we understand the need for clarity and confidence in managing your portfolio with cutting-edge technology and trusted financial principles.

Take control of your financial future with insights tailored to working professionals like you. Discover how combining automation with expert advice can help you navigate market volatility, protect your personal data, and leverage fiduciary standards effectively. Visit Finblog now to explore practical strategies, and start with our easy-to-use forms that ensure a secure and personalized consultation experience.

Get started today and transform uncertainty into opportunity by visiting Finblog. Your safest investment step is just one click away.

Frequently Asked Questions

Are robo-advisors safe for my investments?

Robo-advisors are generally safe as they operate under strict regulatory frameworks, ensuring fiduciary responsibilities and asset protection through independent custody and insurance coverage.

What cybersecurity measures do robo-advisors use to protect my data?

Robo-advisors implement advanced security technologies, including encryption, multi-factor authentication, and regular security audits to safeguard your personal and financial data.

What are the limitations of using a robo-advisor?

Robo-advisors may struggle with complex financial situations, lack the nuanced judgment offered by human advisors, and cannot provide behavioral coaching during market downturns.

How do robo-advisors compare to traditional financial advisors?

Robo-advisors typically offer lower fees and automated portfolio management for straightforward goals, while traditional advisors provide personalized, comprehensive advice tailored to complex financial situations.