TL;DR:

- A Roth IRA allows after-tax contributions with tax-free growth and withdrawals in retirement, offering long-term wealth benefits. Its key features include flexible access to contributions, no required minimum distributions, and eligibility depends on income and filing status, with strategies like backdoor conversions available for high earners. The primary advantage lies in the control over retirement income and tax diversification, helping savers optimize financial flexibility and legacy planning.

Not all IRAs are created equal, and that single misconception costs thousands of savers real money every year. A Roth IRA is an individual retirement account where you contribute after-tax dollars and enjoy tax-free growth and qualified withdrawals in retirement. There’s no upfront deduction, but the payoff on the back end is enormous. This article walks you through exactly how Roth IRAs work, the 2026 rules, withdrawal mechanics, how they compare to traditional IRAs, and the strategies that actually move the needle for long-term wealth building.

Table of Contents

- How a Roth IRA works

- Contribution limits and eligibility for 2026

- Withdrawal rules: Accessing contributions and earnings

- Roth IRA vs. traditional IRA: Key differences

- Who should consider a Roth IRA?

- Our perspective: The real Roth IRA advantage

- Ready to take the next step?

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Tax-free retirement growth | Roth IRAs allow your investments to grow tax-free for your future. |

| After-tax contribution only | You contribute after-tax dollars and receive no upfront tax deduction. |

| Flexible withdrawals | You can withdraw your original contributions any time tax-free, while earnings require you to meet age and timing rules. |

| Income limits apply | There are income restrictions for making direct contributions, with alternatives for high earners. |

| No required distributions | Unlike traditional IRAs, Roth IRAs have no mandatory withdrawals for the original owner. |

How a Roth IRA works

The core mechanic is straightforward. You put money in after you’ve already paid income tax on it. That money then grows completely free from federal taxes, and when you pull it out in retirement, you owe nothing to the IRS on qualified distributions. This is the opposite of a traditional IRA, where you get the tax break upfront but pay taxes when you withdraw.

Contributions to Roth IRAs are not tax-deductible, unlike traditional IRA contributions which may reduce your taxable income today. That distinction matters enormously depending on your current tax situation. If you’re in a high bracket now and expect to drop significantly in retirement, a traditional IRA might serve you better. But if you’re in a lower bracket now, or believe taxes will rise over your lifetime, the Roth wins.

Here’s a quick summary of the core features that define a Roth IRA:

- Contributions: Made with after-tax dollars. No deduction on your return.

- Growth: All investment gains accumulate tax-free inside the account.

- Qualified withdrawals: Completely tax-free and penalty-free once you meet the rules.

- Flexibility: Your contributions (not earnings) can be withdrawn anytime without penalty.

- No forced distributions: You are never required to take money out during your lifetime.

- Broad investment options: Stocks, bonds, ETFs, mutual funds, and more are all fair game.

You can explore the full landscape of retirement account types to see how Roth IRAs fit alongside 401(k)s, SEP IRAs, and other vehicles.

“The most powerful feature of a Roth IRA isn’t just tax-free growth. It’s that your money compounds for decades and you never hand a percentage of it back to the government when you actually need it.”

Pro Tip: Think hard about your current tax bracket versus what you realistically expect in retirement. If your income is likely to be higher later, locking in tax-free status now through a Roth is one of the smartest moves you can make.

Contribution limits and eligibility for 2026

Understanding the rules is key before contributing. Here’s what you need to know for 2026.

The IRS sets annual limits on how much you can contribute. For 2026, the combined IRA contribution limit across Roth and traditional accounts is $7,500, or $8,600 if you’re age 50 or older. That higher amount for older savers is called a “catch-up contribution,” designed to help people accelerate savings as retirement approaches. Note that this limit applies to your total IRA contributions across all accounts, not per account.

2026 Roth IRA income phase-out ranges

| Filing status | Phase-out begins | Phase-out ends |

|---|---|---|

| Single / head of household | $153,000 MAGI | $168,000 MAGI |

| Married filing jointly | $242,000 MAGI | $252,000 MAGI |

| Married filing separately | $0 MAGI | $10,000 MAGI |

MAGI stands for modified adjusted gross income. If your income falls within the phase-out range, your contribution limit is reduced proportionally. Once you exceed the upper threshold, direct Roth IRA contributions are completely phased out for single filers above $168,000 and married filers above $252,000 in 2026.

To make any contribution, you need eligible compensation. That includes:

- Wages, salaries, and tips

- Self-employment income

- Commissions and bonuses

- Taxable alimony received under pre-2019 divorce agreements

- Non-taxable combat pay (for military members)

Investment income, rental income, and Social Security payments do not count as eligible compensation for IRA purposes.

If your income is above the phase-out limit, you’re not necessarily locked out. The backdoor Roth strategy involves making a non-deductible contribution to a traditional IRA, then converting that balance to a Roth IRA. It’s a legal workaround that high earners use routinely. Pair this with tax-advantaged account strategies for a full picture of how to minimize your lifetime tax bill.

Withdrawal rules: Accessing contributions and earnings

Once you start saving, knowing the rules for accessing your money is just as important as knowing how to put it in.

![]()

Roth IRAs have two distinct buckets: your contributions and your earnings. The rules are very different for each. Understanding this split can save you a significant amount in penalties.

Here’s how withdrawals break down:

- Contributions first: The IRS considers withdrawals to come from contributions before earnings. This means you can pull out what you put in at any time, for any reason, with zero tax or penalty.

- Age 59½ requirement: To withdraw earnings tax- and penalty-free, you must be at least 59½ years old at the time of the distribution.

- The 5-year rule: Your Roth IRA must have been open for at least five tax years before earnings can be withdrawn tax-free. The clock starts January 1 of the year you made your first contribution.

- Qualified distributions: A distribution is “qualified” when both the age and 5-year requirements are met. These withdrawals are fully tax-free.

- Early withdrawal exceptions: Penalties on earnings may be waived for first-time home purchases (up to $10,000), qualified education expenses, disability, and a handful of other IRS-approved situations.

Contributions can be withdrawn anytime tax-free and penalty-free. It’s only the earnings portion that requires both age 59½ and the 5-year rule for a tax-free qualified distribution. Many people don’t realize this distinction, which is one reason Roth IRAs are genuinely flexible in a way traditional IRAs are not.

“Your Roth IRA contributions are yours to access whenever you need them. The government already got its tax cut. That flexibility is built-in financial protection you should never take for granted.”

Pro Tip: Keep a simple log of every annual Roth contribution and any conversions. If you ever need to access funds, that record proves exactly which portion is contribution-based and penalty-free. Your brokerage should have this history, but having your own copy is a smart habit.

Thinking ahead about how you’ll actually draw down your accounts is part of any good plan. Exploring withdrawal strategies for lasting income can help you sequence distributions across taxable, traditional, and Roth accounts in the most efficient order.

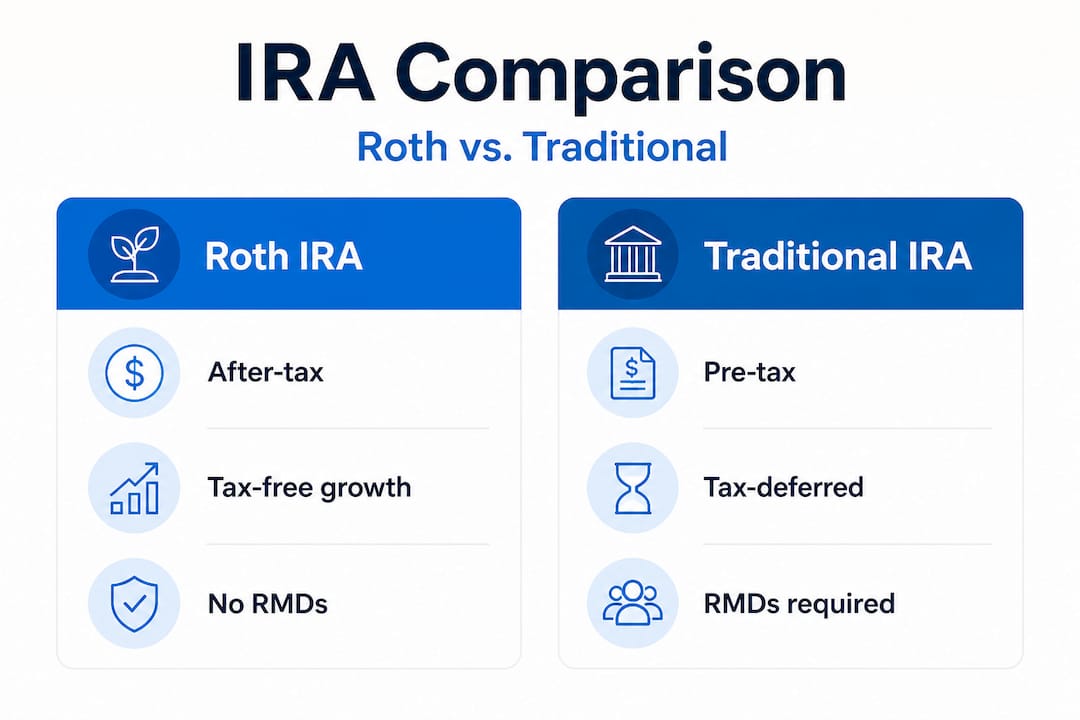

Roth IRA vs. traditional IRA: Key differences

To decide if a Roth IRA fits your situation, compare it against the most common alternative.

| Feature | Roth IRA | Traditional IRA |

|---|---|---|

| Tax treatment of contributions | After-tax (no deduction) | Pre-tax (may be deductible) |

| Tax treatment of withdrawals | Tax-free (qualified) | Taxed as ordinary income |

| Required minimum distributions (RMDs) | None for original owner | Starting at age 73 |

| Income limits for contributions | Yes (phase-outs apply) | No income limit (deduction may phase out) |

| Early withdrawal of contributions | Tax-free and penalty-free | Taxed and penalized |

| Best for | Lower bracket now, higher later | Higher bracket now, lower later |

One of the most significant and underappreciated differences is the RMD rule. No required minimum distributions apply to Roth IRAs during the original owner’s lifetime, unlike traditional IRAs which force withdrawals starting at age 73. This gives Roth account holders far more control over their income in retirement and makes the Roth a powerful legacy-building tool.

Reasons to lean toward a Roth IRA:

- You’re in a low or moderate tax bracket today

- You want tax-free income in retirement without worrying about bracket changes

- You value the ability to leave a tax-advantaged inheritance

- You want the flexibility to access contributions if needed

Reasons to lean toward a traditional IRA:

- You need the tax deduction now to reduce a high current income

- You expect to be in a much lower bracket after you retire

- Reducing your taxable income this year is a pressing financial priority

“For those who care about leaving wealth to heirs, the Roth IRA’s lack of RMDs means assets can continue to compound untouched. The traditional IRA forces you to start spending your own money at 73, whether you want to or not.”

Deciding between these two account types is genuinely one of the most consequential retirement decisions you’ll make. A deeper look at choosing traditional or Roth IRA walks through side-by-side scenarios with real dollar figures. You might also want to explore the 401k vs IRA comparison if you have access to a workplace plan and want to optimize your entire savings strategy.

Who should consider a Roth IRA?

Equipped with a comparison, let’s zero in on who stands to benefit most from opening and funding a Roth IRA.

The Roth is a particularly strong fit if you expect a higher tax bracket in retirement or want the strategic advantage of tax diversification across your portfolio. But it also works well in several specific real-life scenarios that mainstream advice tends to undervalue.

Strong candidates for a Roth IRA:

- Young professionals early in their careers: You’re likely in one of the lowest tax brackets you’ll ever see. Locking in tax-free status now on decades of future growth is extremely valuable.

- Mid-career earners who want tax diversification: Having both a traditional 401(k) and a Roth IRA means you can choose in retirement which account to draw from based on your income that year.

- High earners using the backdoor Roth: Above the income limits but still want tax-free growth? The conversion strategy remains one of the best legal tools available.

- Anyone concerned about future tax increases: Federal debt levels and long-term fiscal projections make it entirely reasonable to assume taxes could be higher in 20 to 30 years. A Roth hedges against that uncertainty.

- Those who value flexible access: Because contributions can be withdrawn anytime without penalty, the Roth doubles as a secondary emergency fund for disciplined savers.

- Estate planning-focused individuals: With no RMDs and tax-free inherited distributions for beneficiaries, the Roth is one of the most efficient assets to pass on.

Pro Tip: If you think you might need occasional access to your savings before retirement, a Roth IRA’s contribution flexibility makes it significantly more useful than most retirement accounts. Just be careful not to treat it as a regular savings account, since touching earnings early can trigger taxes and penalties.

For practical steps on making the most of every available account, the guide on optimizing retirement savings covers contribution sequencing, Roth conversions, and how to build a tax-efficient portfolio over time.

Our perspective: The real Roth IRA advantage

Most conversations about Roth IRAs get stuck on the contribution limit or the income phase-out. Those numbers matter, but they’re not where the real value lives.

The deeper advantage of a Roth is what it does to your decision-making power in retirement. When you have a mix of taxable accounts, traditional retirement accounts, and a Roth IRA, you gain something most retirees never have: genuine flexibility to control your taxable income each year. That flexibility can mean the difference between paying 12% and 22% on a large distribution, or qualifying for subsidized health insurance before Medicare kicks in.

We’ve seen too many savers dismiss the Roth because they’re in a “high tax bracket now.” That logic misses the point. Tax diversification isn’t about optimizing one year. It’s about having options across a 20 or 30-year retirement. The traditional account handles today’s deduction. The Roth handles tomorrow’s uncertainty.

The backdoor Roth conversion is also more accessible than people realize. If your income is above the phase-out limit, a non-deductible traditional IRA contribution followed by a conversion is a straightforward annual strategy used by plenty of high earners. It requires attention to the “pro-rata rule” (which averages out pre-tax and after-tax IRA balances for tax purposes), but a good tax advisor can walk you through it cleanly.

Legacy planning is perhaps the most overlooked Roth benefit. Because original owners face no RMDs, a well-funded Roth can sit untouched for decades, compounding entirely tax-free. Heirs who inherit Roth accounts still must take distributions over 10 years under current rules, but those distributions remain tax-free. That’s a meaningful difference from the taxable inherited traditional IRA. Exploring advanced Roth strategies can help you integrate these concepts into a complete long-term financial plan.

Ready to take the next step?

Understanding a Roth IRA is one thing. Actually building a strategy around it, one that accounts for your tax bracket, income trajectory, employer plans, and estate goals, is where the real work begins. At finblog.com, we’ve built a library of practical retirement guides designed for people who are serious about making their money work harder over the long term. Whether you’re still deciding between account types or ready to explore conversions and contribution sequencing, our resources give you clear, actionable direction without the jargon. Start by reading through all your options and understand all retirement options available to you before making any contribution decisions this year.

Frequently asked questions

Can I withdraw contributions from a Roth IRA at any time?

Yes, you can withdraw your contributions from a Roth IRA at any time tax-free and penalty-free, since you already paid taxes on that money before contributing.

What happens if I earn too much for a direct Roth IRA contribution in 2026?

You may be able to use a backdoor Roth IRA strategy, where you contribute to a traditional IRA and then convert it to a Roth. High earners can use this workaround legally regardless of income.

Are Roth IRA withdrawals ever required?

No, no required minimum distributions apply to Roth IRAs during the original owner’s lifetime, giving you complete control over when and how much you withdraw.

Can I contribute to both a Roth and traditional IRA in the same year?

Yes, but your combined contributions across both accounts cannot exceed $7,500 in 2026, or $8,600 if you are age 50 or older.

What is the five-year rule for Roth IRAs?

Earnings require both age 59½ and a five-year holding period before they can be withdrawn as a qualified, completely tax-free distribution.