TL;DR:

- Over 30% of long-term stock returns come from dividends, yet many investors are unclear on their function.

- Dividends are periodic payments from company profits, paid as cash or stock, with key dates influencing payouts.

- Focusing on dividend quality, payout ratios, and growth prospects is essential, as high yields can be misleading.

Over 30% of long-term stock market returns come from dividends, yet many smart professionals admit they’re unclear on how dividends actually work. Specifically, dividends contributed ~31% of S&P 500 total return since 1926. That’s a massive slice of wealth-building that gets overlooked in everyday investing conversations. Most people focus on stock prices going up or down, but the steady income stream from dividends quietly does a lot of heavy lifting in a long-term portfolio. This guide breaks down exactly what dividends are, how the payment process works, which numbers actually matter, and how to use dividends as a real income strategy without falling into common traps.

Table of Contents

- What are dividends and how do they work?

- The dividend timeline: Key dates and what they mean

- Dividend yield and payout ratio: Measuring dividend value

- Types of dividends and why strategies differ

- Risks, rewards, and common dividend myths

- A fresh take: What most guides get wrong about dividends

- Ready to learn more? Your next step

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Dividends explained simply | Dividends are profit payouts companies make to shareholders, usually as cash or extra stock. |

| Check the timeline | Know the key dividend dates so you qualify and understand when payouts arrive. |

| Measure value smartly | Look at both dividend yield and payout ratio to gauge reliability, not just size. |

| Balance risk and reward | High dividend yields can mean higher risk; steady, well-covered payouts are usually safer. |

| Strategy matters | Use dividends to grow wealth and consider total return, not just income. |

What are dividends and how do they work?

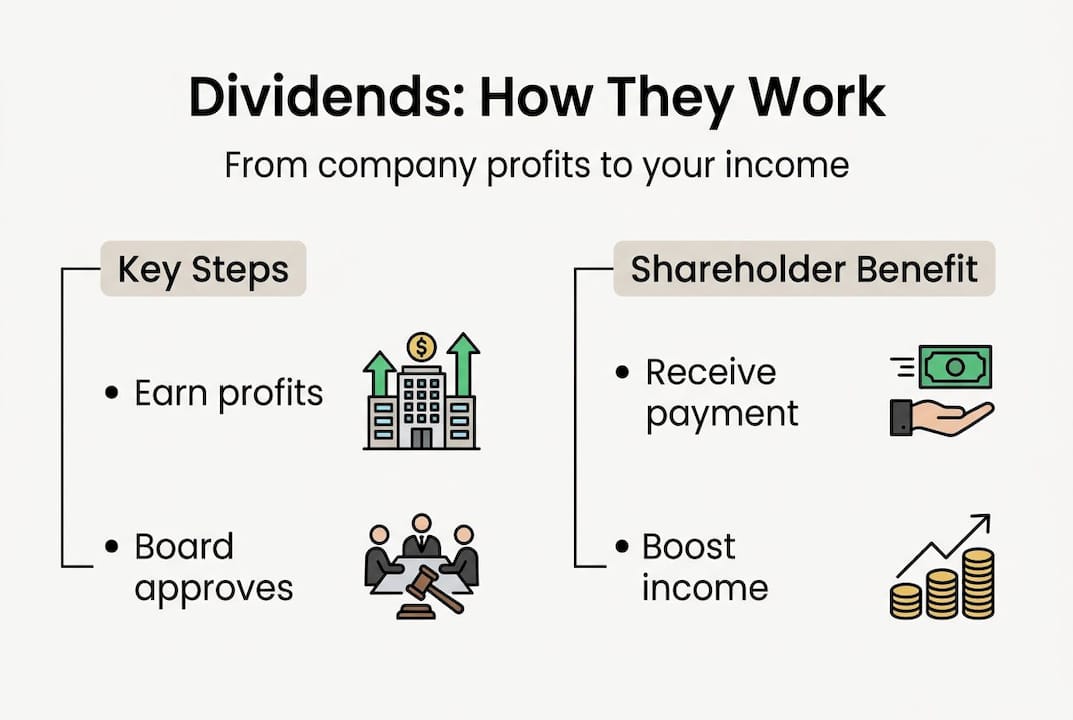

Let’s start simple. A dividend is a payment a company makes to its shareholders, usually from the profits it earns. Think of it like this: you own a small slice of a business, and when that business does well, it shares some of the profits with you. That’s a dividend.

Dividends are periodic payments made to shareholders from profits, authorized by the company’s board of directors. The board decides whether to pay a dividend, how much to pay, and how often. Most large, established companies pay dividends quarterly, though some pay monthly or annually.

When you invest in stocks and ownership of a company, you become a shareholder. If that company decides to pay a dividend, you receive a proportional payout based on how many shares you own. Own 100 shares and the company pays $1 per share? You get $100.

Dividends come in two main forms:

- Cash dividends: The most common type. Money is deposited directly into your brokerage account.

- Stock dividends: Instead of cash, the company gives you additional shares. This increases your ownership stake without you spending more money.

Some companies also issue special dividends, which are one-time payments made when the company has extra cash from an asset sale or an unusually profitable period.

“Dividends represent one of the clearest signals a company can send: we are profitable, financially healthy, and committed to rewarding our investors.” — Common principle among dividend-focused analysts

Not every company pays dividends. Young, fast-growing companies often reinvest all their profits back into the business to fuel expansion. That’s why tech startups rarely pay dividends, while mature companies like utilities, consumer staples, and financial firms tend to pay them consistently.

The process is straightforward: company earns profits, board approves a dividend, shareholders receive payment. Simple in concept, but the timing details matter a lot.

The dividend timeline: Key dates and what they mean

Knowing what dividends are leads to the next key question: who actually gets paid and when? This is where four specific dates come into play, and missing even one of them can mean missing your payout entirely.

Here’s how the dividend payment process works, step by step:

- Declaration date: The company’s board officially announces the dividend. They state the amount, the record date, and the payment date. This is when the dividend becomes public knowledge.

- Ex-dividend date: This is the critical cutoff. To qualify for the dividend, you must own the shares before this date. If you buy shares on or after the ex-dividend date, you will not receive the upcoming payment.

- Record date: The company checks its records to confirm which shareholders are eligible. This date is typically one business day after the ex-dividend date.

- Payment date: The actual day the dividend money hits your account. This can be days or even weeks after the record date.

Here’s something interesting about the ex-dividend date that surprises many new investors: stock prices often drop by roughly the dividend amount on the ex-dividend date. Why? Because the value of the upcoming dividend is no longer included in the stock price once that cutoff passes. It’s not a loss, it’s just the market adjusting.

Understanding dividend timelines helps you plan your purchases strategically rather than buying shares the day after a payout and waiting a full quarter for the next one.

Pro Tip: If you want to capture an upcoming dividend, make sure you buy shares at least two business days before the ex-dividend date to ensure your purchase settles in time.

Tracking these dates takes a little practice, but most brokerage platforms display them clearly on each stock’s dividend information page. Build the habit of checking before you buy.

Dividend yield and payout ratio: Measuring dividend value

Once you know how and when dividends are paid, it’s time to decode the numbers used to judge dividend stocks. Two metrics matter most: dividend yield and payout ratio.

Dividend yield tells you how much income you’re getting relative to the stock price. The formula is simple: dividend yield equals annual dividends per share divided by current stock price, multiplied by 100. If a stock pays $2 per year in dividends and trades at $40, the yield is 5%.

Dividend payout ratio tells you how much of a company’s earnings are being paid out as dividends. A payout ratio of 50% means the company pays half its earnings to shareholders and keeps the other half. Lower ratios often suggest more room to grow the dividend.

Here’s a quick look at how some well-known stocks compare:

| Company | Dividend yield | Payout ratio | Notes |

|---|---|---|---|

| Coca-Cola | ~3.1% | ~73% | Consistent, mature payer |

| Apple | ~0.5% | ~15% | Low yield, strong growth |

| Realty Income | ~5.5% | ~75% | Monthly payer, REIT structure |

| Johnson & Johnson | ~3.0% | ~45% | Balanced yield and coverage |

So what’s a “good” yield? It depends on your goals. A yield above 5% can look attractive, but it sometimes signals that the stock price has fallen sharply, which is a red flag. When calculating dividend yield, always ask why the yield is high.

Key things to watch:

- Yield between 2% and 5%: Generally considered healthy for most dividend stocks

- Payout ratio below 60%: Suggests the dividend is well-covered and sustainable

- Rising dividends over time: A company that consistently grows its dividend is often more valuable than one with a static high yield

Pro Tip: Focus on dividend investing strategies that prioritize dividend growth over raw yield. A stock yielding 2% today that grows its dividend 8% annually will outpace a static 5% yield in just a few years.

These two metrics together give you a much clearer picture of whether a dividend is genuinely attractive or just looks good on the surface.

Types of dividends and why strategies differ

Analyzing yield and payout is just part of the story. Dividends come in several flavors, and understanding the differences shapes how you invest.

| Type | Description | Tax treatment |

|---|---|---|

| Cash dividend | Direct cash payment to shareholders | Ordinary or qualified rates |

| Stock dividend | Additional shares instead of cash | Taxed when shares are sold |

| Regular dividend | Paid on a consistent schedule | Ordinary or qualified rates |

| Special dividend | One-time payment, often from asset sales | Ordinary income rates |

Types of dividends include regular, special, cash, and stock varieties, and the tax treatment varies significantly. Qualified dividends, which meet IRS holding period requirements, are taxed at the lower long-term capital gains rate. Nonqualified dividends are taxed as ordinary income, which can be a meaningful difference depending on your tax bracket.

To receive qualified tax treatment, you generally need to hold the stock for more than 60 days during the 121-day window surrounding the ex-dividend date. It’s a detail worth knowing before you trade in and out of dividend stocks quickly.

Why do some companies pay dividends and others don’t? Mature, stable companies with predictable cash flows, think consumer goods, utilities, and healthcare, tend to pay regular dividends. They don’t need to reinvest every dollar for growth, so sharing profits with shareholders makes sense.

Growth companies, especially in tech, often skip dividends entirely. They believe they can generate better returns by reinvesting profits into research, acquisitions, or market expansion.

Then there are Dividend Aristocrats, a select group of S&P 500 companies that have raised their dividends for at least 25 consecutive years. These companies have higher returns and lower volatility compared to the broader index. Names like Procter & Gamble, Coca-Cola, and 3M fall into this category.

Exploring different dividend investing approaches helps you match your strategy to your actual financial goals.

Risks, rewards, and common dividend myths

With opportunity comes risk. Before you jump in, let’s separate fact from fiction and cover key realities about dividend investing.

First, the hard truth: dividends are not guaranteed and can be cut during downturns. Companies facing falling profits, rising debt, or economic pressure often reduce or eliminate dividends to preserve cash. It happened widely during the 2008 financial crisis and again in 2020.

“A high dividend yield can actually be a warning sign, not a reward. It often means the market expects the dividend to be cut.” — A core principle in value-based dividend analysis

Common myths worth busting:

- Myth: Only old or boring companies pay dividends. False. Many financially strong, innovative companies pay dividends.

- Myth: A high yield always means a great investment. False. High yields often reflect falling stock prices, not rising payouts.

- Myth: Dividends always signal financial health. False. Some companies borrow money to maintain dividends, which is unsustainable.

The rewards are real, though. Dividend stocks tend to offer lower volatility, steady income, and a built-in incentive for companies to stay financially disciplined. For retirees or anyone building passive income, that consistency is valuable.

Some experts emphasize that focusing on moderate payout ratios and earnings growth offers greater long-term sustainability than chasing the highest current yield.

A balanced approach means looking at:

- Company earnings stability and debt levels

- Dividend history, especially through recessions

- Payout ratio trends over multiple years

- Understanding growth vs value trade-offs in your portfolio

- Diversifying dividend stocks across sectors to reduce concentration risk

Dividends reward patient, informed investors. They punish those who buy blindly based on yield alone.

A fresh take: What most guides get wrong about dividends

Here’s something most dividend articles won’t tell you: chasing the highest yield is one of the most reliable ways to lose money in dividend investing. It feels logical. Higher yield means more income, right? Not always.

The smartest dividend investors we follow at finblog.com focus on total return, which means stock price appreciation plus dividends combined. A company growing earnings at 12% annually with a modest 2% yield will likely outperform a stagnant company yielding 6% over any meaningful time horizon.

Company quality matters more than current payout size. Look for businesses with durable competitive advantages, manageable debt, and a track record of growing dividends through tough markets. Avoid the behavioral trap of overreacting to short-term news. A single bad quarter doesn’t necessarily mean a dividend cut is coming.

Avoid dividend strategy pitfalls by setting realistic expectations. Dividends add stability and income to a portfolio. They are not a shortcut to wealth. The investors who benefit most treat dividends as one layer of a thoughtful, diversified strategy, not the whole plan.

Ready to learn more? Your next step

Armed with the facts and a fresh perspective, you’re already ahead of most investors when it comes to understanding dividends. But understanding the basics is just the starting point. Building a real income strategy takes the right tools, deeper knowledge, and a clear plan tailored to your goals.

At finblog.com, we publish step-by-step guides, stock analysis frameworks, and practical resources designed specifically for investors at every stage. Whether you’re just getting started or refining an existing portfolio, our dividend income resources give you the structure to move from learning to earning. Explore the guides, bookmark what’s useful, and take your next step with confidence.

Frequently asked questions

Can I earn living income just from dividends?

With a large enough portfolio of reliable dividend stocks, some investors do live off dividends, but most use them as supplemental income. Dividends can lower volatility and provide steady income, especially for retirees building a cash flow plan.

Are dividends better than stock buybacks?

Neither is always better. Dividends give you immediate cash, while buybacks can boost share value over time and are often favored by growth-focused companies. Some companies reinvest or buy back shares instead of paying dividends to maximize long-term growth.

Why would a company cut its dividend?

Dividends get cut when profits fall, management needs to conserve cash, or future business prospects weaken significantly. Cuts signal poor profits and high payout ratios that become unsustainable under financial pressure.

How are dividends taxed in the US?

Most dividends are taxed as ordinary income, but qualified dividends receive lower capital gains rates if shares are held long enough. Qualified dividends are taxed at preferential rates when the IRS holding period requirement is met.

Can all stocks pay dividends?

No. Many growing or early-stage companies skip dividends entirely and reinvest profits for expansion. Young and growth companies rarely pay dividends because reinvestment typically offers better returns at that stage of development.