Millions of Americans leave thousands of dollars on the table every year, not because they earn too little, but because they misunderstand how tax-advantaged accounts work. These accounts are not reserved for the wealthy or for financial professionals. They are government-designed tools built specifically to help everyday savers grow wealth faster by reducing what they owe in taxes. Whether you are saving for retirement, medical expenses, or education, understanding these accounts and using them strategically can dramatically change your financial future. This guide walks you through everything: the types, the rules, the limits, and the smartest ways to use them.

Table of Contents

- What are tax-advantaged accounts?

- Types of tax-advantaged accounts

- How tax rules and contribution limits work

- Advanced strategies: Backdoor Roth and mega backdoor Roth explained

- Optimizing your savings: How to prioritize contributions

- Common mistakes and pitfalls to avoid

- Take the next step with finblog.com

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Tax-advantaged accounts explained | These accounts let you reduce taxes and boost long-term savings through special government incentives. |

| Choose accounts based on goals | Pick between Traditional, Roth, HSA, and 529 based on your income, health, and retirement needs. |

| Optimize contributions and asset placement | Follow a strategic order and use asset location to maximize after-tax returns. |

| Avoid common mistakes | Watch for income limits, required withdrawals, and poor asset placement to keep more of your money working for you. |

What are tax-advantaged accounts?

A tax-advantaged account is any account the government has structured to give you a tax break in exchange for saving toward a specific goal. The incentive might come upfront, through a deduction on your current taxes, or later, through tax-free growth or withdrawals. Either way, the government is essentially subsidizing your savings.

Tax-advantaged accounts include retirement, health, and education-focused options, each designed for a different purpose but all sharing one core feature: they reduce your tax burden over time. The three main categories are:

- Retirement accounts: 401(k), Traditional IRA, Roth IRA, SEP-IRA

- Health accounts: Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs)

- Education accounts: 529 college savings plans and Coverdell Education Savings Accounts

The tax advantages work in three main ways. First, you may get a deduction when you contribute (pre-tax). Second, your money grows without being taxed each year (tax-deferred or tax-free growth). Third, you may withdraw funds without owing taxes if you meet the rules (tax-free withdrawals).

“The best time to open a tax-advantaged account was yesterday. The second best time is today.” Understanding the mechanics is the first step toward using them effectively.

If you want a broader look at how these fit into your overall plan, exploring the types of retirement accounts available to you is a great starting point.

Types of tax-advantaged accounts

Not all tax-advantaged accounts work the same way. Each has its own rules, benefits, and ideal use case. Here is a breakdown of the major types and how they compare.

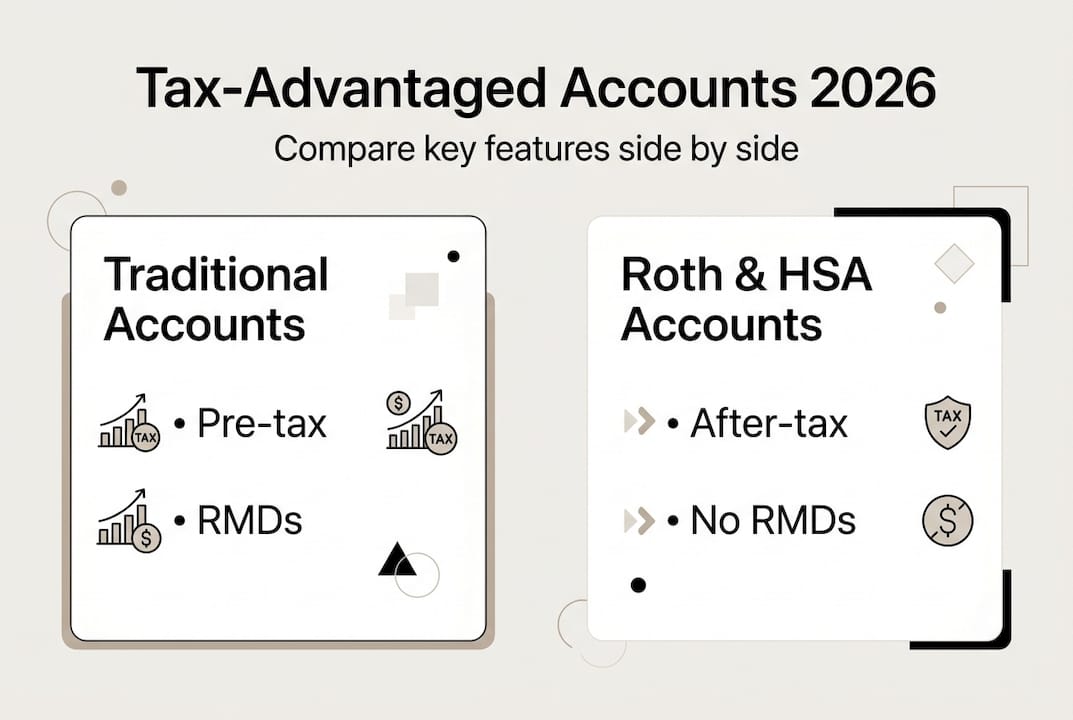

Traditional and Roth accounts have different tax treatments, and HSAs provide triple tax benefits. That triple benefit for HSAs means contributions are pre-tax, growth is tax-free, and withdrawals for qualified medical expenses are also tax-free. No other account type offers all three.

| Account type | Contribution type | Growth | Withdrawals | Best for |

|---|---|---|---|---|

| Traditional 401(k) | Pre-tax | Tax-deferred | Taxed as income | Reducing current taxable income |

| Roth 401(k) | After-tax | Tax-free | Tax-free (qualified) | Tax-free retirement income |

| Traditional IRA | Pre-tax (if eligible) | Tax-deferred | Taxed as income | Flexible retirement savings |

| Roth IRA | After-tax | Tax-free | Tax-free (qualified) | Long-term tax-free growth |

| HSA | Pre-tax | Tax-free | Tax-free (medical) | Healthcare and retirement |

| 529 Plan | After-tax | Tax-free | Tax-free (education) | College and K-12 expenses |

For 2026, the contribution limits are as follows:

- 401(k): $24,500 per year (plus $7,500 catch-up if you are 50 or older)

- IRA (Traditional or Roth): $7,500 per year (plus $1,000 catch-up if 50 or older)

- HSA: $4,400 for self-only coverage, $8,750 for family coverage

- 529 Plan: No annual federal limit, but contributions above $19,000 may trigger gift tax rules

For a side-by-side breakdown of how these accounts stack up, the 401(k) vs IRA comparison covers the key differences in detail.

How tax rules and contribution limits work

Knowing the account types is one thing. Understanding the specific rules that govern them is where most people get tripped up.

Income limits matter for some accounts. The Roth IRA phases out for single filers earning above $150,000 and married filers above $236,000 in 2026. However, the Roth 401(k) has no income limits, making it a powerful option for high earners who want tax-free retirement income.

Required Minimum Distributions (RMDs) are mandatory withdrawals the IRS requires you to take from most Traditional accounts starting at age 73. Roth IRAs owned by the original account holder are exempt from RMDs during the owner’s lifetime, which makes them excellent for estate planning.

Statistic: The Saver’s Credit can be worth up to 50% of your retirement contributions, up to $1,000 for single filers, yet millions of eligible Americans never claim it.

For HSAs, eligibility requires enrollment in a High-Deductible Health Plan (HDHP). In 2026, an HDHP must have a minimum deductible of $1,650 for self-only coverage. If you have a secondary insurance plan that is not an HDHP, you lose HSA eligibility entirely.

Pro Tip: If your income qualifies, always check whether you are eligible for the Saver’s Credit before filing. It is a direct reduction of your tax bill, not just a deduction, and it stacks on top of your contribution deduction.

For a full breakdown of how these rules interact across account types, the retirement account rules comparison is worth reviewing.

Advanced strategies: Backdoor Roth and mega backdoor Roth explained

Once you hit the Roth IRA income limits, you are not locked out of Roth benefits. Two advanced strategies can get you there.

Backdoor Roth and mega backdoor Roth strategies allow high earners to access Roth tax benefits even when direct contributions are off the table. Here is how each works:

- Backdoor Roth IRA: You make a non-deductible (after-tax) contribution to a Traditional IRA, then convert it to a Roth IRA. Since you already paid tax on the contribution, the conversion is generally tax-free.

- Pro-rata rule warning: If you have other pre-tax IRA balances, the IRS treats all your IRA funds as one pool. This means part of your conversion will be taxable. Many people skip the backdoor Roth because they miss this detail.

- Mega backdoor Roth: Some 401(k) plans allow after-tax contributions beyond the standard limit, up to a total of $70,000 in 2026 across all contribution types. You can then roll those after-tax funds into a Roth IRA or Roth 401(k) through an in-service rollover.

- Plan requirements: Not every employer plan allows after-tax contributions or in-service rollovers. You need to check your Summary Plan Description before assuming this strategy is available to you.

Pro Tip: Before executing a backdoor Roth, roll any existing pre-tax IRA balances into your employer’s 401(k) if the plan accepts rollovers. This eliminates the pro-rata problem entirely.

For a detailed walkthrough of the mega backdoor approach, the mega backdoor Roth guide is one of the most thorough resources available. You can also explore broader tax-efficient investing strategies to see how these tactics fit into a larger plan.

Optimizing your savings: How to prioritize contributions

Knowing which accounts exist is not enough. The order in which you fund them has a real impact on your long-term returns.

Prioritize employer match first, then max tax-advantaged accounts before moving to taxable brokerage accounts. Skipping your employer match is the equivalent of turning down free money, and it is one of the most common and costly mistakes investors make.

Here is a practical funding sequence to follow:

- Contribute enough to your 401(k) to capture the full employer match. This is an instant 50% to 100% return on your money.

- Max out your HSA if you are eligible. The triple tax benefit makes it the most tax-efficient account available.

- Max out your Roth or Traditional IRA depending on your income and tax situation.

- Return to your 401(k) and contribute up to the annual limit.

- Fund a taxable brokerage account with any remaining savings.

Asset location matters too. Active funds underperform after-tax vs. the S&P 500, and tax drag compounds over time. Place your least tax-efficient investments, like actively managed funds and bonds, inside tax-advantaged accounts. Keep index funds and ETFs in taxable accounts where their low turnover minimizes capital gains distributions.

Pro Tip: Think of your tax-advantaged accounts as your “tax shelter” and your taxable account as your “tax-exposed” space. Always fill the shelter first with your highest-tax-cost assets.

For more on this, the guides on active vs passive investing and the tax implications of investing offer practical frameworks you can apply immediately.

Common mistakes and pitfalls to avoid

Even experienced investors make avoidable errors with tax-advantaged accounts. Here are the ones that cost the most.

- Missing the employer match: Leaving any portion of your employer match unclaimed is a guaranteed loss.

- Ignoring HSA eligibility: Many people with HDHPs never open an HSA, missing years of triple-tax-free growth.

- Misunderstanding RMDs: Tax-deferred accounts can have significant drawbacks, including mandatory withdrawals that push you into higher tax brackets in retirement.

- Poor asset location: Placing high-turnover active funds in taxable accounts creates unnecessary capital gains taxes every year.

- Exceeding Roth IRA income limits: Contributing directly to a Roth IRA when your income exceeds the threshold triggers a 6% excess contribution penalty for every year the money stays in the account.

“The biggest tax mistakes are not dramatic errors. They are quiet omissions: the match you did not capture, the HSA you never opened, the Roth you forgot to check eligibility for.”

Strategies like tax loss harvesting can help offset gains in taxable accounts, and revisiting your asset allocation strategies annually ensures your money is always in the most tax-efficient position.

Take the next step with finblog.com

Understanding tax-advantaged accounts is one thing. Building a personalized strategy around them is where real wealth is created. At finblog.com, we provide in-depth guides, tools, and expert-level content designed specifically for investors who want to make every dollar work harder. Whether you are just starting to explore your options or you are ready to implement advanced strategies like the backdoor Roth, our resources are built to meet you where you are. Sign up for our newsletter to get the latest updates on contribution limits, tax law changes, and actionable investment strategies delivered directly to your inbox.

Frequently asked questions

What is the difference between a Traditional IRA and a Roth IRA?

Traditional IRAs use pre-tax contributions with tax-deferred growth and taxable withdrawals, while Roth IRAs use after-tax dollars and offer completely tax-free qualified withdrawals in retirement.

Who is eligible to open a Health Savings Account (HSA)?

You must be enrolled in a qualifying high-deductible health plan and cannot have any other disqualifying health coverage, including Medicare, to open and contribute to an HSA.

How do required minimum distributions (RMDs) work for tax-advantaged accounts?

Most Traditional retirement accounts require you to begin RMDs at age 73, but Roth IRAs are exempt from RMDs for the original account owner during their lifetime.

Can high earners contribute to a Roth IRA?

Direct Roth IRA contributions phase out above certain income thresholds, but backdoor and mega backdoor Roth strategies give high earners a legal path to the same tax-free benefits.

What is the Saver’s Credit and who qualifies?

The Saver’s Credit is a tax credit worth up to $1,000 for single filers who contribute to a retirement account and have an adjusted gross income below $23,000, making it one of the most overlooked benefits for moderate-income savers.