As you start exploring investments, it’s important to understand exactly what separates stocks and bonds. Many beginners confuse stocks and bonds as similar investments, treating them interchangeably when building portfolios. Understanding their key differences is crucial for making informed investment decisions that align with your financial goals and risk tolerance. This guide will explain what stocks and bonds are, how they differ, and how to use them effectively in your portfolio to balance growth potential with stability.

Table of Contents

- What Are Stocks And Bonds?

- Comparing Key Characteristics Of Stocks And Bonds

- How Stocks And Bonds Fit In Your Investment Portfolio

- Current Trends And Practical Tips For Investing In 2026

- Explore More Resources On Finblog

Key takeaways

| Point | Details |

|---|---|

| Ownership vs lending | Stocks represent partial ownership in companies, while bonds are loans you make to issuers |

| Risk and return profiles | Stocks carry higher volatility with greater growth potential, bonds offer stability with predictable income |

| Income generation | Stock dividends vary based on company performance, bond interest payments are fixed and contractual |

| Portfolio diversification | Combining both asset classes reduces overall risk while maintaining growth opportunities |

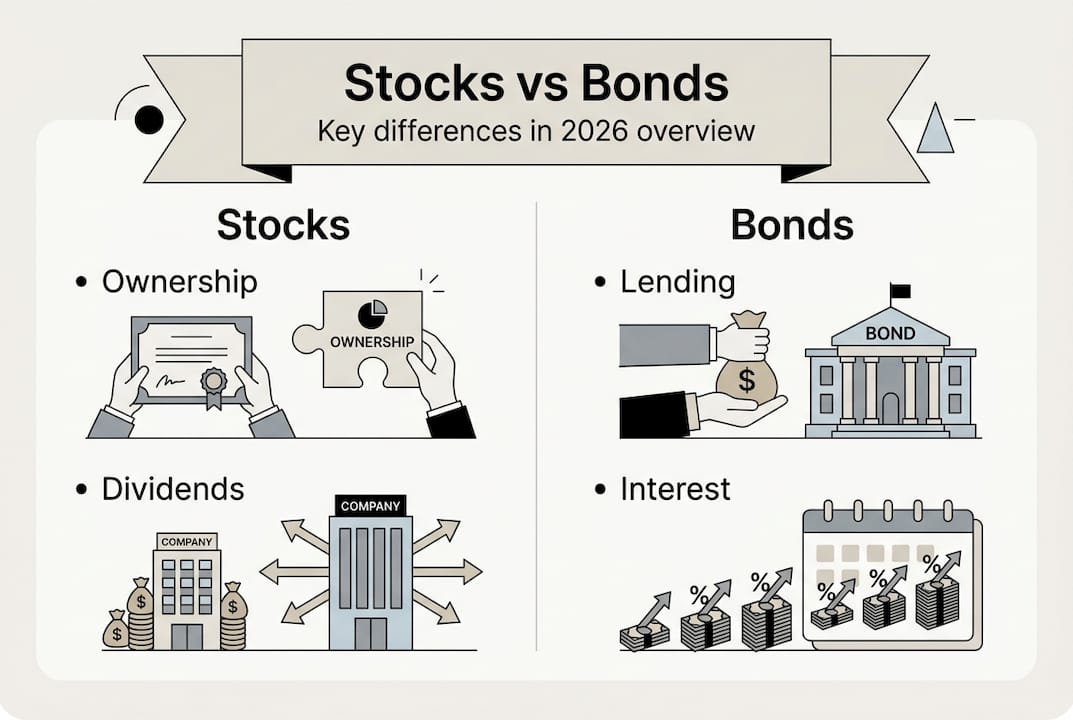

What are stocks and bonds?

When you buy stock, you become a partial owner of that company. Stocks represent ownership in a company and typically offer voting rights and dividends. Your investment grows when the company performs well and its stock price rises. You can profit through price appreciation when you sell shares at a higher price than you paid, or through dividend payments that some companies distribute to shareholders.

Bonds work completely differently. When you purchase a bond, you’re essentially lending money to a government, municipality, or corporation. The issuer promises to pay you regular interest payments, called coupon payments, and return your principal when the bond matures. Think of it like being the bank: you provide capital upfront and receive predictable interest income over time.

The fundamental difference between stocks and bonds lies in your relationship to the issuer. As a stockholder, you own a piece of the business and share in its success or failure. As a bondholder, you’re a creditor who has lent money and expects repayment regardless of how well the company performs.

Stocks generate returns through two mechanisms: capital gains when share prices increase, and dividends when companies distribute profits. Returns are variable and can be substantial during bull markets or negative during downturns. Bonds provide returns primarily through fixed interest payments, with some potential for price appreciation if interest rates fall. The predictability differs dramatically between these two asset classes.

Pro Tip: Understanding whether you’re an owner or a lender fundamentally changes how you should evaluate investment opportunities and manage risk.

Comparing key characteristics of stocks and bonds

The risk profiles of stocks and bonds differ substantially. Stocks generally carry higher risk but greater potential returns compared to bonds, which offer more stability through fixed income. Stock prices fluctuate daily based on company performance, market sentiment, economic conditions, and countless other factors. You could see your investment double or lose half its value in a relatively short period.

Bonds present different risks. Credit risk exists if the issuer might default on payments, though government bonds carry minimal default risk. Interest rate risk affects bond prices inversely: when rates rise, existing bond prices fall because newer bonds offer higher yields. However, if you hold a bond to maturity, you’ll receive your principal back regardless of price fluctuations along the way.

| Characteristic | Stocks | Bonds |

|---|---|---|

| Ownership status | Equity owner with voting rights | Creditor with no ownership stake |

| Income type | Variable dividends (if any) | Fixed coupon payments |

| Return potential | Unlimited upside potential | Limited to interest and principal |

| Risk level | Higher volatility and uncertainty | Lower volatility, more predictable |

| Maturity | No maturity date | Fixed maturity date |

| Priority in bankruptcy | Last to receive assets | Paid before stockholders |

The income characteristics reveal another key distinction. Stock dividends are discretionary; companies can increase, decrease, or eliminate them based on financial performance and strategic priorities. Bond interest payments are contractual obligations that must be paid on schedule. Missing a bond payment constitutes default and can trigger serious legal consequences for the issuer.

Ownership versus creditor status fundamentally affects your position. Stockholders can vote on major company decisions, elect board members, and influence corporate direction. Bondholders have no such rights but enjoy priority if the company faces bankruptcy. In liquidation scenarios, bondholders get paid before stockholders receive anything.

Tax implications of investing vary between these assets. Qualified stock dividends often receive favorable tax treatment at lower capital gains rates. Bond interest is typically taxed as ordinary income at your marginal tax rate, which can significantly impact your after-tax returns. Municipal bonds offer tax-free interest for certain investors, adding another layer of complexity.

Pro Tip: Balancing risk and return requires understanding how each asset behaves under different market conditions and economic cycles.

How stocks and bonds fit in your investment portfolio

Stocks drive portfolio growth but introduce volatility that can test your nerves during market corrections. Over long periods, equities have historically delivered higher returns than bonds, making them essential for wealth accumulation. However, their unpredictable short-term behavior means you might see significant losses during bear markets or economic recessions.

Bonds provide ballast and income stability. Including both stocks and bonds in portfolios reduces risk and improves growth potential through diversification. When stock markets tumble, bonds often hold steady or even appreciate, cushioning your overall portfolio from severe losses. This inverse correlation makes bonds valuable for risk management.

Diversification using both asset classes creates a balanced approach. You capture stock market growth during expansions while maintaining bond stability during contractions. The specific allocation depends on your personal circumstances, but the principle remains constant: don’t put all your eggs in one basket.

Here’s how to determine your ideal allocation:

- Assess your investment timeline and when you’ll need the money

- Evaluate your risk tolerance and ability to withstand volatility

- Consider your income needs and whether you require regular cash flow

- Factor in your age and proximity to retirement

- Review your overall financial situation and emergency reserves

Younger investors with decades until retirement can typically allocate more heavily to stocks, accepting short-term volatility for long-term growth. As you approach retirement, gradually shifting toward bonds preserves capital and generates income when you can’t afford major losses. This lifecycle approach matches your asset allocation to your changing needs.

Portfolio diversification benefits extend beyond simple risk reduction. Combining assets that respond differently to economic conditions smooths your return pattern over time. While you might sacrifice some upside potential compared to an all-stock portfolio, you gain downside protection and more consistent performance.

Pro Tip: Rebalance periodically to maintain your intended risk profile, selling winners and buying underperformers to keep your target allocation intact.

Diversification is the only free lunch in investing.

Understanding why diversify investments guide principles helps you construct resilient portfolios. Different asset classes peak at different times, and maintaining exposure to both stocks and bonds ensures you participate in various market opportunities. This strategic approach reduces the impact of any single investment’s poor performance on your overall wealth.

Current trends and practical tips for investing in 2026

The investment landscape in 2026 shows increased focus on risk management amid ongoing market volatility. Investors are recognizing that traditional 60/40 stock-bond allocations may need adjustment based on interest rate environments and inflation expectations. Certain diversification and balancing strategies involving stocks and bonds have gained traction in 2026 due to market volatility and interest rate changes.

A notable shift involves diversified bond types to hedge against inflation. Treasury Inflation-Protected Securities (TIPS), floating-rate bonds, and short-duration bonds are gaining popularity as investors seek protection from purchasing power erosion. These instruments adjust payments based on inflation or interest rate movements, providing dynamic income streams.

Active rebalancing strategies have become more prevalent. Rather than the traditional annual rebalancing, many investors now monitor their portfolios quarterly or even monthly to lock in gains and mitigate losses. This tactical approach responds to rapid market movements and helps maintain risk parameters during turbulent periods.

Newer ETFs blending stocks and bonds in single funds offer simplified diversification. These all-in-one solutions automatically rebalance and adjust allocations based on target risk levels or retirement dates. They’ve democratized sophisticated portfolio management for investors who lack time or expertise to manage multiple holdings.

Key practical tips for 2026:

- Monitor interest rate trends closely, as rising rates depress bond prices while potentially benefiting certain stock sectors

- Consider bond ladders that mature at different intervals, providing regular liquidity and reducing reinvestment risk

- Evaluate international bonds and stocks for additional diversification beyond domestic markets

- Use tax-advantaged accounts strategically, placing tax-inefficient bonds in retirement accounts and stocks in taxable accounts

- Stay informed about stock market trends 2026 to identify emerging opportunities

Pro Tip: Stay informed on interest rate changes impacting bond prices, as Federal Reserve policy shifts can dramatically affect your fixed income holdings’ market value.

The relationship between balancing risk and return has evolved with changing economic conditions. What worked in previous decades may not suit today’s environment of higher inflation and shifting monetary policy. Regularly reassessing your strategy ensures alignment with current market realities rather than outdated assumptions.

Explore more resources on Finblog

Ready to take your understanding further? Discover expert resources and practical tools on Finblog to help optimize your investment journey. Whether you’re building your first portfolio or refining an existing strategy, having access to comprehensive educational content makes all the difference in achieving your financial goals.

Our detailed guides break down complex investment concepts into actionable insights. Learn exactly how stocks and bonds explained in depth can transform your approach to wealth building. Explore proven methods for achieving portfolio diversification benefits that protect your capital while pursuing growth.

Understanding tax implications of investing can significantly boost your after-tax returns. Our resources help you navigate the complexities of investment taxation, ensuring you keep more of what you earn. From dividend taxation to capital gains strategies, we provide the knowledge you need to invest tax-efficiently.

FAQ

What is the main risk difference between stocks and bonds?

Stocks carry market risk with significant price volatility driven by company performance, economic conditions, and investor sentiment. You could experience substantial gains or losses in relatively short periods. Bonds have credit risk if the issuer might default and interest rate risk that affects prices inversely to rate movements, but they’re generally safer with more predictable outcomes. If you hold bonds to maturity, you receive your principal regardless of interim price fluctuations.

How do dividends and interest differ between stocks and bonds?

Dividends are variable payments to shareholders that companies can increase, decrease, or eliminate based on profitability and strategic priorities. They’re discretionary and reflect the company’s financial health and management decisions. Bond interest payments are fixed, predetermined amounts specified in the bond contract that must be paid on schedule. Missing a bond payment constitutes default with serious legal consequences, making interest payments far more reliable than dividends.

Can bonds protect my investments during stock market downturns?

Bonds tend to be less volatile and can provide steady income, helping cushion portfolio losses when stocks fall sharply. They often move inversely to stocks during market stress, appreciating when equities decline. This negative correlation makes bonds an effective diversification tool to stabilize overall portfolio value. However, bonds won’t eliminate losses entirely, and their protective benefit depends on the specific types of bonds you hold and prevailing interest rate environments.

What tax considerations should I keep in mind for stocks and bonds?

Tax treatment varies: stock dividends may be taxed differently than bond interest, affecting after-tax returns significantly. Qualified dividends often receive favorable capital gains tax rates, while bond interest is typically taxed as ordinary income at your marginal rate. Municipal bonds offer tax-free interest for certain investors, potentially making them attractive despite lower nominal yields. Tax-efficient investing strategies depend on understanding these distinctions and placing assets strategically across taxable and tax-advantaged accounts.

Recommended

- Understanding the Difference Between Stocks and Bonds – Finblog

- Understanding Mutual Funds vs Stocks: Key Concepts Explained – Finblog

- Why Invest in Bonds: Balancing Growth and Security – Finblog

- Which Diversification Strategies Are Winning in 2026?

- What is small cap stock? A 2026 guide for investors