Stocks often make headlines as the ticket to wealth, offering the kind of growth that captures imaginations. Yet, while shares can soar fast, bonds quietly command attention for their uncanny steadiness and lower risk profiles. Here’s the kicker that few expect: bonds have outperformed stocks in more than one-third of all 10-year periods since 1926, according to financial research. This flips the script for anyone who thinks investing success is only about chasing high-flying stocks with risky bets.

Table of Contents

- How Stocks And Bonds Work

- Key Differences In Risk And Return

- Choosing Between Stocks And Bonds

- Real-Life Scenarios And Practical Tips

Quick Summary

| Takeaway | Explanation |

|---|---|

| Investing in stocks involves ownership stakes | Stocks grant partial ownership in a company, allowing investors to benefit from capital appreciation and dividends. |

| Bonds function as debt instruments | Bonds are loans to entities, offering predictable interest payments and principal repayment, generally viewed as more stable. |

| Balance risk with strategic diversification | Combining stocks and bonds helps mitigate risks and align investment strategies with personal financial goals. |

| Assess personal financial goals before investing | Determine whether you seek growth or income, which will guide your investment in stocks, bonds, or both. |

| Adjust investment strategies with life stages | Investment approaches should evolve over time based on age, financial goals, and risk tolerance for effective wealth management. |

How Stocks and Bonds Work

Investors navigating the financial landscape encounter two primary investment vehicles: stocks and bonds. Understanding how these instruments function is crucial for making informed investment decisions. While they both serve as potential wealth-building tools, their underlying mechanics differ significantly.

The Mechanics of Stock Investments

Stocks represent partial ownership in a company, functioning as a direct stake in a business’s potential success. When you purchase stocks, you become a shareholder, which means you own a small portion of that corporation. According to the U.S. Securities and Exchange Commission, these equity investments offer potential for high returns but come with higher associated risks.

Companies issue stocks through initial public offerings (IPOs), allowing investors to purchase shares. The value of these shares fluctuates based on multiple factors including company performance, market conditions, and investor sentiment. Shareholders can potentially benefit through two primary mechanisms: capital appreciation (stock price increase) and dividend payments, where companies distribute a portion of their profits to investors.

Understanding Bond Investments

In contrast to stocks, bonds operate as debt instruments where investors essentially become lenders. When you purchase a bond, you are loaning money to an entity (which could be a corporation, municipality, or government) in exchange for periodic interest payments and the promise of principal repayment at maturity. The Tennessee Department of Commerce and Insurance clarifies that bonds are generally considered more stable investments compared to stocks.

Bonds have specific characteristics that distinguish them from stocks. They come with predetermined interest rates, known as coupon rates, and fixed maturity dates. Investors receive regular interest payments throughout the bond’s term and can expect to recover their full principal investment upon maturity. The risk level and interest rate depend on the bond issuer’s creditworthiness and the overall economic environment.

To help clarify the core differences between stocks and bonds, the following table compares their main features, benefits, and risks as discussed in the article.

| Feature/Aspect | Stocks | Bonds |

|---|---|---|

| Ownership | Partial ownership in a company | Lender to an entity (company, gov., etc.) |

| Return Type | Capital appreciation & dividends | Fixed interest payments (coupon) |

| Risk Level | Higher, more volatile | Lower, more stable |

| Return Potential | Unlimited upside potential | Predictable, constrained returns |

| Maturity Date | No fixed maturity date | Fixed maturity date |

| Suitability | Growth-oriented, long-term investors | Conservative, income-focused, capital preserve |

| Market Sensitivity | Highly sensitive to market and company news | Sensitive to interest rates & credit risk |

Risk and Return Dynamics

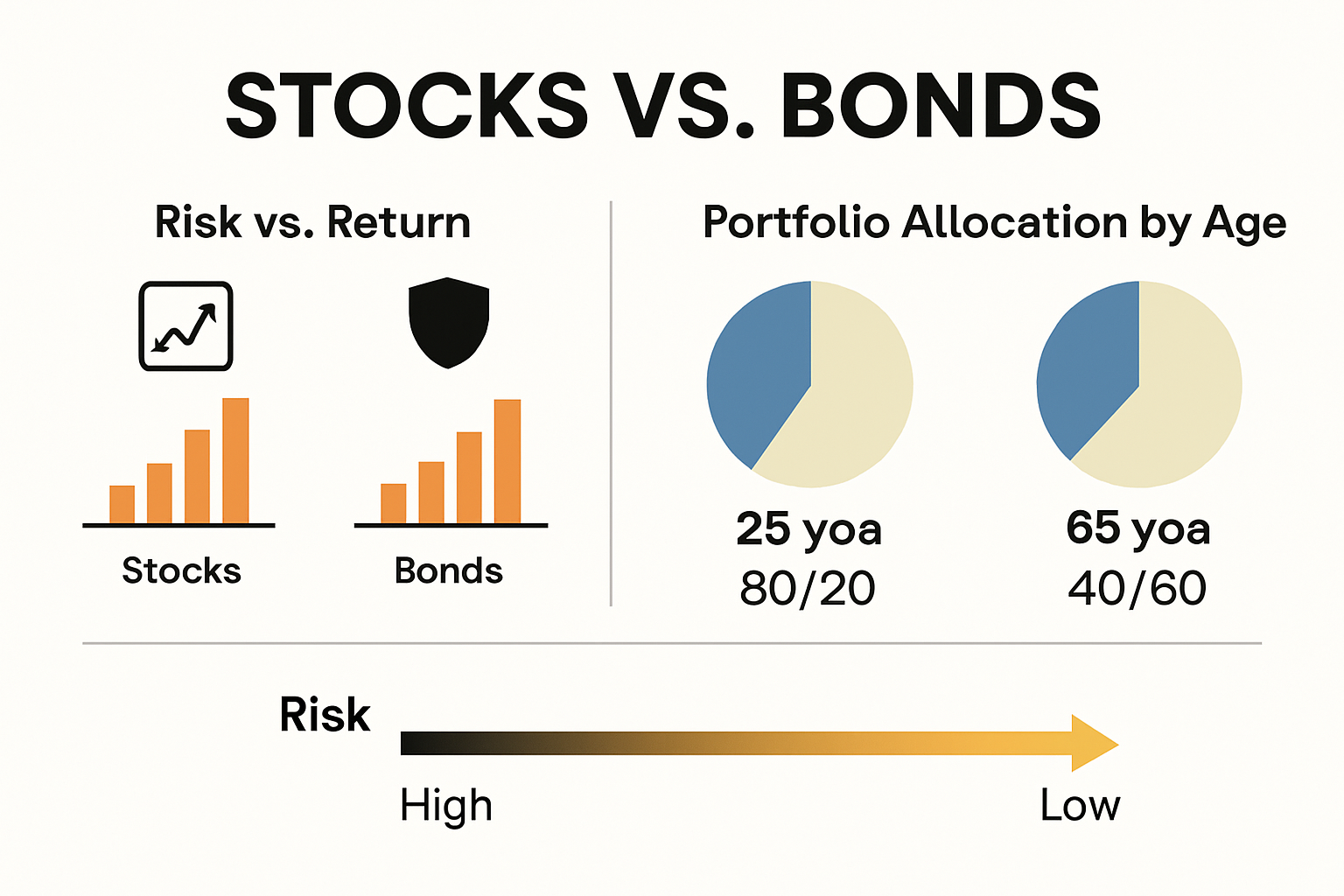

The fundamental difference between stocks and bonds lies in their risk and return profiles. As the Federal Reserve Education website explains, stocks typically offer higher potential returns but with increased volatility, while bonds provide more predictable, lower-risk income streams.

Investors often use a combination of stocks and bonds to create a balanced portfolio. Younger investors might lean towards a stock-heavy approach seeking growth, while those closer to retirement might shift towards more bond-oriented investments for stability and consistent income. The key is understanding your personal financial goals, risk tolerance, and investment timeline when deciding how to allocate your resources between these two distinct investment types.

Mastering the mechanics of stocks and bonds empowers investors to make strategic decisions that align with their financial objectives, transforming complex financial instruments into powerful wealth-building tools.

Key Differences in Risk and Return

Investors continuously seek strategies to optimize their financial portfolios, and understanding the nuanced relationship between risk and return is fundamental when comparing stocks and bonds. These investment vehicles exhibit dramatically different characteristics that directly impact potential gains and potential losses.

Risk Spectrum Analysis

The investment landscape presents a complex risk spectrum where stocks and bonds occupy distinct positions. According to the U.S. Securities and Exchange Commission, stocks have historically provided higher average returns compared to bonds, but this potential comes with substantially greater market volatility. Investors must recognize that higher potential rewards inherently correlate with increased risk exposure.

Stocks represent ownership stakes in companies, which means their value can fluctuate dramatically based on corporate performance, market sentiment, and broader economic conditions. A company might experience rapid growth or sudden decline, directly impacting shareholder value. Conversely, bonds represent debt instruments with more predictable return structures, offering more stable income streams but typically lower potential gains.

Return Potential Comparisons

The University of Illinois Chicago highlights the fundamental distinction in return potential between these investment types. Stocks offer unlimited upside potential, meaning investors can experience significant capital appreciation if the underlying company performs exceptionally well. A startup technology firm could potentially multiply an investor’s initial investment many times over, representing the high-reward potential of equity investments.

Bonds, by contrast, provide more constrained but more predictable returns. Their fixed interest payments create a more reliable income stream, making them attractive to conservative investors or those nearing retirement. The trade-off is clear: lower potential gains in exchange for greater stability and reduced risk of substantial capital loss.

Risk Mitigation Strategies

The Texas State Securities Board emphasizes that intelligent investors do not choose between stocks and bonds exclusively, but rather strategically combine them to balance risk and return. Diversification becomes the cornerstone of effective investment strategy.

Younger investors might construct portfolios heavily weighted toward stocks, accepting higher short-term volatility in exchange for potentially greater long-term growth. Older investors or those with lower risk tolerance typically shift toward bond-heavy portfolios, prioritizing capital preservation and consistent income. The ideal allocation depends on individual financial goals, time horizon, and personal risk comfort level.

Understanding these key differences empowers investors to make informed decisions. Stocks represent growth potential with higher risk, while bonds offer stability with more modest returns. The art of investing lies not in choosing one over the other, but in crafting a balanced approach that aligns with personal financial objectives and risk tolerance.

Choosing Between Stocks and Bonds

Selecting the right investment strategy requires careful consideration of personal financial goals, risk tolerance, and individual circumstances. Stocks and bonds represent two distinct pathways to potential financial growth, each offering unique advantages and challenges for investors.

Personal Financial Goals Assessment

Investment decisions are deeply personal and should align with your specific financial objectives. According to Fidelity Investments, investors must first evaluate their primary financial goals. Are you seeking long-term wealth accumulation, preparing for retirement, or looking to generate consistent income? These objectives will significantly influence whether stocks, bonds, or a combination best suits your needs.

Younger investors typically have longer investment horizons, allowing them to tolerate more risk and potentially allocate a larger portion of their portfolio to stocks. Those closer to retirement might prioritize capital preservation, shifting towards a more bond-heavy investment strategy. Your age, income stability, and future financial requirements play crucial roles in determining the optimal investment approach.

Risk Tolerance Evaluation

Understanding your personal risk tolerance is paramount when choosing between stocks and bonds. The Charles Schwab Investment Research emphasizes that investors must honestly assess their emotional and financial capacity to withstand market fluctuations. Some individuals become anxious with significant portfolio value changes, while others can remain calm during market volatility.

Stocks offer higher potential returns but come with greater market risk. They are ideal for investors who can withstand short-term market fluctuations and have the patience to ride out economic cycles. Bonds provide more stable, predictable returns and are better suited for conservative investors or those approaching a financial milestone where capital preservation becomes critical.

Strategic Portfolio Diversification

Most financial experts recommend a balanced approach that combines stocks and bonds to optimize investment performance. The key is finding the right allocation that matches your individual financial profile. A common strategy involves gradually shifting from a stock-heavy portfolio to a more bond-oriented approach as you age.

Beginning investors might start with a 70-30 or 80-20 stock-to-bond ratio, gradually rebalancing to become more conservative over time. This approach allows for potential growth while progressively reducing overall portfolio risk. Some investors utilize target-date funds that automatically adjust asset allocation based on anticipated retirement timeline.

The art of choosing between stocks and bonds is not about making a definitive selection, but creating a nuanced strategy that evolves with your financial journey. Your investment approach should remain flexible, allowing periodic reassessment and adjustment as your life circumstances and financial goals change.

Ultimately, successful investing requires ongoing education, self-awareness, and a willingness to adapt. Whether you lean towards stocks, bonds, or a balanced portfolio, the most important factor is developing a consistent, disciplined investment strategy that supports your long-term financial objectives.

Real-Life Scenarios and Practical Tips

Navigating the complex world of stocks and bonds requires more than theoretical knowledge. Real-world application demands practical strategies and a nuanced understanding of how these investment vehicles function in different life stages and financial circumstances.

Investment Scenarios Across Life Stages

Each life stage presents unique investment challenges and opportunities. A recent college graduate might approach investing differently compared to someone nearing retirement. According to Investor.gov, understanding the fundamental characteristics of stocks and bonds becomes crucial in making informed financial decisions.

For young professionals in their 20s and early 30s, a more aggressive investment strategy often makes sense. With a longer time horizon, they can tolerate higher risk and potentially allocate 80-90% of their portfolio to stocks. This approach allows for maximum growth potential and the ability to recover from market fluctuations. These investors can focus on growth-oriented stocks, including emerging technology companies and aggressive mutual funds that offer higher potential returns.

Practical Risk Management Strategies

Middle-aged investors typically need a more balanced approach. As family and career responsibilities increase, protecting accumulated wealth becomes equally important as generating returns. A 60-40 or 50-50 split between stocks and bonds can provide a reasonable balance between growth and stability. This strategy allows for continued portfolio growth while introducing more conservative elements to protect against market volatility.

Retirees and those approaching retirement should prioritize capital preservation. A bond-heavy portfolio with 60-70% allocated to fixed-income investments can provide more stable, predictable income streams.

The next table summarizes recommended stock-to-bond allocation strategies at different life stages, based on the article’s guidance for aligning investments with changing risk tolerance and financial needs over time.

| Life Stage | Recommended Stock % | Recommended Bond % | Rationale |

|---|---|---|---|

| Early Career (20s-30s) | 80-90% | 10-20% | Focus on growth, high risk tolerance |

| Mid-Career (40s-50s) | 50-60% | 40-50% | Balance growth with wealth protection |

| Approaching Retirement | 30-40% | 60-70% | Emphasize capital preservation, income |

| Retirement | ≤ 30% | ≥ 70% | Prioritize stability and predictable income |

Conservative stock investments can still play a role, ensuring some potential for growth while minimizing overall portfolio risk.

Strategic Investment Recommendations

Successful investing requires more than just understanding stocks and bonds. Practical tips can help investors maximize their potential returns and minimize risks. Consider these key strategies:

- Dollar-Cost Averaging: Invest consistently over time, reducing the impact of market volatility

- Regular Portfolio Rebalancing: Annually review and adjust your investment allocation

- Diversification: Spread investments across multiple sectors and asset types

- Emergency Fund: Maintain liquid savings before making significant investments

Tax considerations also play a crucial role in investment strategy. Different investment vehicles have varying tax implications. Stocks held for more than a year qualify for lower long-term capital gains tax rates, while bond interest is typically taxed as ordinary income. Understanding these nuances can help optimize your overall investment approach.

The most successful investors remain flexible, continually educating themselves and adapting their strategies to changing personal circumstances and broader economic conditions. Whether you’re just starting your investment journey or looking to refine an existing portfolio, understanding the practical application of stocks and bonds is key to long-term financial success.

Frequently Asked Questions

What is the primary difference between stocks and bonds?

Stocks represent ownership in a company, while bonds are debt instruments where investors lend money to entities in exchange for interest payments.

How do stocks and bonds perform in terms of risk and return?

Stocks generally offer higher potential returns but come with increased volatility, whereas bonds provide more stable income with lower potential gains, making them less risky.

Why should I consider diversifying between stocks and bonds?

Diversifying between stocks and bonds helps balance risk and return in your investment portfolio, aligning with your financial goals and risk tolerance.

How does my age affect my investment strategy between stocks and bonds?

Younger investors tend to lean towards stocks for growth due to a longer investment horizon, while older investors often shift towards bonds to preserve capital and generate stable income.

Ready to Balance Growth and Security in Your Portfolio?

If you have ever felt uncertain about striking the right balance between higher-risk stocks and stable bonds, you are not alone. Many readers come here searching for clarity on how to protect their wealth while pursuing future growth. This article walked you through key differences in ownership, risk, and returns, but making these decisions is not always easy. Navigating market volatility, aligning investments with your life stage, and finding the right risk mitigation strategies are personal challenges that require expert support.

Take action today to strengthen your investment plan. Join other serious investors who use finblog.com for personalized financial guidance, actionable tips, and exclusive access to financial experts. Whether you want to master portfolio diversification, evaluate your risk tolerance, or receive tailored investment recommendations, our secure consultation form is the first step. Do not wait while the markets change—get your questions answered by experienced advisors and start making smarter financial choices right now.